January 2014 Housing Sales Statistics

•

0 likes•219 views

The document provides an analysis of the real estate market in Oklahoma for January 2014. It shows that total housing inventory decreased 6.61% compared to the previous year. The months supply of inventory also decreased from 5.99 to 5.27. Average home sale prices rose 2.04% while average days on market increased slightly. Overall sales success was positive with prices up and more homes pending sale, though new listings declined slightly year-over-year.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (7)

Similar to January 2014 Housing Sales Statistics

Similar to January 2014 Housing Sales Statistics (20)

Recently uploaded

Recently uploaded (17)

January 2014 Housing Sales Statistics

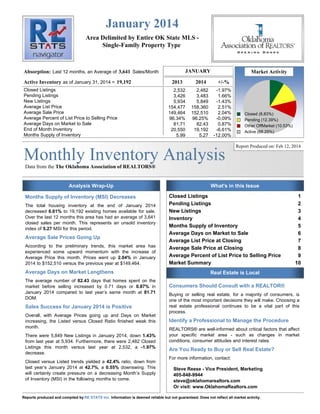

- 1. January 2014 Area Delimited by Entire OK State MLS Single-Family Property Type JANUARY Absorption: Last 12 months, an Average of 3,641 Sales/Month Active Inventory as of January 31, 2014 = 19,192 Closed Listings Pending Listings New Listings Average List Price Average Sale Price Average Percent of List Price to Selling Price Average Days on Market to Sale End of Month Inventory Months Supply of Inventory Market Activity 2013 2014 +/-% 2,532 3,426 5,934 154,477 149,464 96.34% 81.71 20,550 5.99 2,482 3,483 5,849 158,360 152,510 96.25% 82.43 19,192 5.27 -1.97% 1.66% -1.43% 2.51% 2.04% -0.09% 0.87% -6.61% -12.00% Monthly Inventory Analysis Closed (8.83%) Pending (12.39%) Other OffMarket (10.53%) Active (68.25%) Report Produced on: Feb 12, 2014 Data from the The Oklahoma Association of REALTORS® Analysis Wrap-Up Months Supply of Inventory (MSI) Decreases The total housing inventory at the end of January 2014 decreased 6.61% to 19,192 existing homes available for sale. Over the last 12 months this area has had an average of 3,641 closed sales per month. This represents an unsold inventory index of 5.27 MSI for this period. Average Sale Prices Going Up According to the preliminary trends, this market area has experienced some upward momentum with the increase of Average Price this month. Prices went up 2.04% in January 2014 to $152,510 versus the previous year at $149,464. Average Days on Market Lengthens The average number of 82.43 days that homes spent on the market before selling increased by 0.71 days or 0.87% in January 2014 compared to last year’s same month at 81.71 DOM. Sales Success for January 2014 is Positive Overall, with Average Prices going up and Days on Market increasing, the Listed versus Closed Ratio finished weak this month. There were 5,849 New Listings in January 2014, down 1.43% from last year at 5,934. Furthermore, there were 2,482 Closed Listings this month versus last year at 2,532, a -1.97% decrease. Closed versus Listed trends yielded a 42.4% ratio, down from last year’s January 2014 at 42.7%, a 0.55% downswing. This will certainly create pressure on a decreasing Month’s Supply of Inventory (MSI) in the following months to come. What's in this Issue Closed Listings Pending Listings New Listings Inventory Months Supply of Inventory Average Days on Market to Sale Average List Price at Closing Average Sale Price at Closing Average Percent of List Price to Selling Price Market Summary 1 2 3 4 5 6 7 8 9 10 Real Estate is Local Consumers Should Consult with a REALTOR® Buying or selling real estate, for a majority of consumers, is one of the most important decisions they will make. Choosing a real estate professional continues to be a vital part of this process. Identify a Professional to Manage the Procedure REALTORS® are well-informed about critical factors that affect your specific market area - such as changes in market conditions, consumer attitudes and interest rates. Are You Ready to Buy or Sell Real Estate? For more information, contact: Steve Reese - Vice President, Marketing 405-848-9944 steve@oklahomarealtors.com Or visit: www.OklahomaRealtors.com Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity.

- 2. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® January 2014 Closed Sales as of Feb 12, 2014 Closed Listings Report Produced on: Feb 12, 2014 Area Delimited by Entire OK State MLS - Single-Family Property Type JANUARY 2010 1,719 2011 1,982 2012 2,307 YEAR TO DATE (YTD) 2013 2014 2,532 2010 2,482 1,719 2011 2012 2013 2,532 2,307 1,982 2014 2,482 1 Year -1.97% 2 Year +7.59% 1 Year -1.97% 2 Year +7.59% 5 YEAR MARKET ACTIVITY TRENDS 5yr JAN AVG = 2,204 High Jul 2013 = 4,628 Low Jan 2010 = 1,719 5,000 4,000 3,000 Closed Listings 2,000 1,000 0 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 Dec 2012 Jun 2013 Dec 2013 3 MONTHS N 3,114 O V D 3,153 E C 1.25% Closed Listings this month at 2,482, above the 5 yr JAN J 2,482 A average of 2,204 N -21.28% CLOSED LISTINGS & BEDROOMS DISTRIBUTION BY PRICE Distribution of Closed Listings by Price Range % AVDOM 2 Beds 3 Beds 4 Beds 5 Beds+ 125 5.04% 83.5 57 62 4 2 $25,001 $50,000 243 9.79% 79.6 87 127 23 6 $50,001 $100,000 Ready to Buy or Sell Real Estate? Contact an experienced REALTOR $25,000 and less 569 22.93% 83.3 160 354 54 1 $100,001 $150,000 580 23.37% 78.9 81 402 87 10 $150,001 $200,000 376 15.15% 76.9 54 218 95 9 $200,001 $275,000 315 12.69% 86.6 41 136 129 9 $275,001 and up 274 11.04% 92.9 20 59 155 40 Total Closed Units: Total Closed Volume: Average Closed Price: 2,482 378,530,713 $152,510 82.4 500 1358 547 77 52.04M 175.14M 125.56M 25.80M $104,075 $128,966 $229,542 $335,035 Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. Steve Reese 405-848-9944 steve@oklahomarealtors.com pp. 1

- 3. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® January 2014 Pending Listings as of Feb 12, 2014 Pending Listings Report Produced on: Feb 12, 2014 Area Delimited by Entire OK State MLS - Single-Family Property Type JANUARY 2010 2011 2012 3,124 2,411 YEAR TO DATE (YTD) 2013 2014 3,426 3,483 2,574 2010 2011 2012 2013 3,426 3,124 2,411 2014 3,483 2,574 1 Year +1.66% 2 Year +11.49% 1 Year +1.66% 2 Year +11.49% 5 YEAR MARKET ACTIVITY TRENDS 5yr JAN AVG = 3,004 High Apr 2010 = 4,937 Low Dec 2010 = 2,050 5,000 4,000 3,000 Pending Listings 2,000 1,000 0 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 Dec 2012 Jun 2013 Dec 2013 3 MONTHS N 2,968 O V D 2,374 E C -20.01% Pending Listings this month at 3,483, above the 5 yr JAN J 3,483 A average of 3,004 N 46.71% PENDING LISTINGS & BEDROOMS DISTRIBUTION BY PRICE Distribution of Pending Listings by Price Range % AVDOM 2 Beds 3 Beds 4 Beds 5 Beds+ 336 9.65% 72.9 149 163 21 3 $40,001 $70,000 365 10.48% 83.4 124 212 26 3 $70,001 $110,000 Ready to Buy or Sell Real Estate? Contact an experienced REALTOR $40,000 and less 608 17.46% 79.1 135 406 60 7 $110,001 $160,000 874 25.09% 76.4 119 617 129 9 $160,001 $200,000 463 13.29% 77.9 59 269 128 7 $200,001 $290,000 487 13.98% 83.8 53 200 212 22 $290,001 and up 350 10.05% 98.5 21 103 181 45 Total Pending Units: Total Pending Volume: Average Listing Price: 3,483 553,736,349 $143,886 88.3 660 1970 757 96 70.11M 276.14M 175.92M 31.56M $106,232 $140,172 $232,391 $328,785 Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. Steve Reese 405-848-9944 steve@oklahomarealtors.com pp. 2

- 4. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® January 2014 New Listings as of Feb 12, 2014 New Listings Report Produced on: Feb 12, 2014 Area Delimited by Entire OK State MLS - Single-Family Property Type JANUARY 2010 2012 2013 2014 6,112 5,108 2011 YEAR TO DATE (YTD) 5,934 5,849 5,464 2010 2012 2013 2014 6,112 5,108 2011 5,934 5,849 5,464 1 Year -1.43% 2 Year -4.30% 1 Year -1.43% 2 Year -4.30% 5 YEAR MARKET ACTIVITY TRENDS 5yr JAN AVG = 5,693 High Apr 2010 = 7,793 Low Dec 2013 = 3,468 8,000 7,000 6,000 5,000 New Listings 4,000 3,000 2,000 1,000 0 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 Dec 2012 Jun 2013 Dec 2013 3 MONTHS N 4,405 O V D 3,468 E C -21.27% New Listings this month at 5,849, above the 5 yr JAN J 5,849 A average of 5,693 N 68.66% NEW LISTINGS & BEDROOMS DISTRIBUTION BY PRICE Distribution of New Listings by Price Range % 2 Beds 3 Beds 4 Beds 5 Beds+ 584 9.98% 251 292 39 2 $50,001 $80,000 658 11.25% 227 381 46 4 $80,001 $110,000 Ready to Buy or Sell Real Estate? Contact an experienced REALTOR $50,000 and less 769 13.15% 168 510 85 6 $110,001 $170,000 1,538 26.30% 250 1,051 217 20 $170,001 $230,000 917 15.68% 122 475 305 15 $230,001 $350,000 809 13.83% 82 314 360 53 $350,001 and up 574 9.81% 46 124 303 101 Total New Listed Units: Total New Listed Volume: Average New Listed Listing Price: 5,849 1,109,158,137 $144,216 1146 3147 1355 201 149.91M 488.73M 369.61M 100.91M $130,813 $155,301 $272,772 $502,031 Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. Steve Reese 405-848-9944 steve@oklahomarealtors.com pp. 3

- 5. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® January 2014 Active Inventory as of Feb 12, 2014 Active Inventory Report Produced on: Feb 12, 2014 Area Delimited by Entire OK State MLS - Single-Family Property Type END OF JANUARY 2010 2011 2012 23,956 ACTIVE DURING JANUARY 2013 22,955 19,934 2010 19,192 2011 2012 2013 2014 29,483 20,534 2014 29,123 26,694 25,636 5,083 1 Year -6.54% 2 Year -16.39% 1 Year -3.96% 2 Year -11.97% 5 YEAR MARKET ACTIVITY TRENDS 5yr JAN AVG = 21,314 Active Inventory High Jul 2011 = 26,728 Low Jan 2014 = 19,192 30,000 20,000 10,000 0 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 Dec 2012 Jun 2013 Dec 2013 Inventory this month at 19,192, below the 5 yr JAN average of 21,314 3 MONTHS N 21,368 O V D 19,797 E C -7.35% J 19,192 A N -3.06% INVENTORY & BEDROOMS DISTRIBUTION BY PRICE Distribution of Inventory by Price Range % AVDOM 2 Beds 3 Beds 4 Beds 5 Beds+ 1,970 10.26% 127.6 980 870 111 9 $50,001 $75,000 2,027 10.56% 133.9 793 1,081 137 16 $75,001 $100,000 Ready to Buy or Sell Real Estate? Contact an experienced REALTOR $50,000 and less 2,315 12.06% 118.7 639 1,438 218 20 $100,001 $175,000 5,373 28.00% 110.5 973 3,457 859 84 $175,001 $225,000 2,450 12.77% 111.4 389 1,256 751 54 $225,001 $375,000 3,153 16.43% 119.7 442 1,074 1,401 236 $375,001 and up 1,904 9.92% 127.5 206 388 910 400 Total Active Inventory by Units: Total Active Inventory by Volume: Average Active Inventory Listing Price: 19,192 3,841,508,192 $200,162 119.0 4,422 9,564 4,387 819 621.23M 1.50B 1.29B 430.29M $140,485 $157,348 $292,937 $525,388 Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. Steve Reese 405-848-9944 steve@oklahomarealtors.com pp. 4

- 6. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® January 2014 Active Inventory as of Feb 12, 2014 Months Supply of Inventory Report Produced on: Feb 12, 2014 Area Delimited by Entire OK State MLS - Single-Family Property Type MSI FOR JANUARY 2010 2011 2012 8.2 INDICATORS FOR JANUARY 2014 Inventory 7.7 6.3 2013 2014 Closed Absorption MSI MSI % 5.3 18.972% Months Supply of Inventory Percent Months Supply of Inventory 43,693 6.0 5.3 19,192 1 Year -11.93% 2 Year -31.79% End of Month Active Inventory Closed Last 12 Months 5 YEAR MARKET ACTIVITY TRENDS 3,641 Average Closed per Month over 12 Months 5yr JAN AVG = 6.7 High Jun 2011 = 9.7 Low Jan 2014 = 5.3 Months Supply 10 9 8 7 6 5 4 3 2 1 0 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 Dec 2012 Jun 2013 Dec 2013 Months Supply this month at 5.3, below the 5 yr JAN average of 6.7 3 MONTHS N 5.9 O V D 5.4 E C -7.44% J 5.3 A N -2.95% MONTHS SUPPLY & BEDROOMS DISTRIBUTION BY PRICE Distribution of Active Inventory by Price Range and MSI % MSI 2 Beds 3 Beds 4 Beds 5 Beds+ 1,970 10.26% 4.7 5.3 4.2 4.1 2.2 $50,001 $70,000 1,643 8.56% 6.5 8.2 5.8 5.3 4.9 $70,001 $110,000 Ready to Buy or Sell Real Estate? Contact an experienced REALTOR $50,000 and less 3,300 17.19% 5.4 6.3 5.0 6.1 8.0 $110,001 $170,000 4,458 23.23% 4.1 4.6 3.9 4.1 7.4 $170,001 $240,000 3,267 17.02% 4.9 5.7 4.9 4.5 5.4 $240,001 $370,000 2,576 13.42% 6.2 8.5 6.6 5.4 7.2 $370,001 and up 1,978 10.31% 11.0 16.5 11.6 9.8 11.7 6.1 4,422 4.8 9,564 5.4 4,387 8.3 819 MSI: Total Active Inventory: 5.3 19,192 Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. Steve Reese 405-848-9944 steve@oklahomarealtors.com pp. 5

- 7. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® January 2014 Closed Sales as of Feb 12, 2014 Average Days on Market to Sale Report Produced on: Feb 12, 2014 Area Delimited by Entire OK State MLS - Single-Family Property Type JANUARY 2010 2011 2012 93 YEAR TO DATE (YTD) 2013 92 2010 82 2011 2012 93 82 80 2014 2013 2014 92 82 82 80 1 Year +0.87% 2 Year -9.98% 1 Year +0.87% 2 Year -9.98% 5 YEAR MARKET ACTIVITY TRENDS 5yr JAN AVG = 86 Average Days on Market High Mar 2011 = 98 Low Jul 2013 = 69 100 90 80 70 60 50 40 30 20 10 0 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 Dec 2012 Jun 2013 Dec 2013 Average DOM this month at 82, below the 5 yr JAN average of 86 3 MONTHS N 78 O V D 83 E C 5.72% J 82 A N -0.64% AVERAGE DOM OF CLOSED SALES & BEDROOMS DISTRIBUTION BY PRICE Distribution of Average Days on Market to Sale by Price Range % AVDOM 2 Beds 3 Beds 4 Beds 5 Beds+ Ready to Buy or Sell Real Estate? Contact an experienced REALTOR $25,000 and less 125 5.04% 83.5 97.1 74.9 54.8 21.0 $25,001 $50,000 243 9.79% 79.6 97.6 68.2 70.3 98.5 $50,001 $100,000 569 22.93% 83.3 88.7 82.5 74.2 8.0 $100,001 $150,000 580 23.37% 78.9 103.6 72.8 81.3 101.9 $150,001 $200,000 376 15.15% 76.9 93.1 76.2 71.0 59.4 $200,001 $275,000 315 12.69% 86.6 101.0 80.8 86.0 118.1 $275,001 and up 274 11.04% 92.9 117.1 110.1 85.0 85.8 96.2 500 52.04M 77.9 1358 175.14M Average Closed DOM: Total Closed Units: Total Closed Volume: 82.4 2,482 378,530,713 80.3 547 125.56M Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. Steve Reese 405-848-9944 steve@oklahomarealtors.com 86.9 77 25.80M pp. 6

- 8. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® January 2014 Closed Sales as of Feb 12, 2014 Average List Price at Closing Report Produced on: Feb 12, 2014 Area Delimited by Entire OK State MLS - Single-Family Property Type JANUARY 2010 2011 2012 YEAR TO DATE (YTD) 2013 154,477 150,211 2014 158,360 2011 2012 2013 2014 154,477 150,211 142,068 139,073 2010 158,360 142,068 139,073 1 Year +2.51% 2 Year +11.47% 1 Year +2.51% 2 Year +11.47% 5 YEAR MARKET ACTIVITY TRENDS 5yr JAN AVG = 149K Average List Price High Jul 2013 = 176,626 Low Jan 2010 = 139,073 200,000 100,000 0 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 Dec 2012 Jun 2013 Dec 2013 3 MONTHS N 169,908 O V D 164,936 E Average LPrice this C -2.93% month at 158,360, above the 5 yr JAN J 158,360 A average of 148,838 N -3.99% AVERAGE LIST PRICE OF CLOSED SALES & BEDROOMS DISTRIBUTION BY PRICE Distribution of Average List Price at Closing by Price Range % AVL$ 2 Beds 3 Beds 4 Beds 5 Beds+ 105 4.23% 17,528 18,643 23,524 16,600 15,950 $25,001 $50,000 246 9.91% 39,415 40,877 45,809 39,523 36,700 $50,001 $100,000 Ready to Buy or Sell Real Estate? Contact an experienced REALTOR $25,000 and less 551 22.20% 77,196 75,590 81,033 79,814 70,000 $100,001 $150,000 578 23.29% 127,970 130,783 129,837 135,722 143,895 $150,001 $200,000 398 16.04% 172,875 177,375 174,288 175,675 183,475 $200,001 $275,000 315 12.69% 235,966 236,947 237,450 241,061 253,177 $275,001 and up 289 11.64% 421,720 390,713 403,416 416,071 533,195 Average List Price: Total Closed Units: Total List Volume: $158,360 2,482 393,048,974 $108,828 $134,202 $236,508 $350,893 500 1358 547 77 54.41M 182.25M 129.37M 27.02M Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. Steve Reese 405-848-9944 steve@oklahomarealtors.com pp. 7

- 9. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® January 2014 Closed Sales as of Feb 12, 2014 Average Sold Price at Closing Report Produced on: Feb 12, 2014 Area Delimited by Entire OK State MLS - Single-Family Property Type JANUARY 2010 2011 143,656 133,432 2012 YEAR TO DATE (YTD) 2013 2014 149,464 2010 2011 2012 152,510 143,656 136,117 133,432 2013 2014 149,464 152,510 136,117 1 Year +2.04% 2 Year +12.04% 1 Year +2.04% 2 Year +12.04% 5 YEAR MARKET ACTIVITY TRENDS 5yr JAN AVG = 143K Average Sold Price High Jul 2013 = 171,577 Low Jan 2010 = 133,432 200,000 100,000 0 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 Dec 2012 Jun 2013 Dec 2013 3 MONTHS N 164,003 O V D 159,616 E Average SPrice this C -2.68% month at 152,510, above the 5 yr JAN J 152,510 A average of 143,036 N -4.45% AVERAGE SOLD PRICE OF CLOSED SALES & BEDROOMS DISTRIBUTION BY PRICE Distribution of Average Sold Price at Closing by Price Range % AVS$ 2 Beds 3 Beds 4 Beds 5 Beds+ 125 5.04% 17,242 15,857 18,643 15,677 16,426 $25,001 $50,000 243 9.79% 38,034 36,844 39,216 37,304 33,049 $50,001 $100,000 Ready to Buy or Sell Real Estate? Contact an experienced REALTOR $25,000 and less 569 22.93% 75,469 71,931 77,087 75,591 62,500 $100,001 $150,000 580 23.37% 126,300 124,132 125,613 130,291 136,765 $150,001 $200,000 376 15.15% 171,356 173,619 170,358 171,630 179,053 $200,001 $275,000 315 12.69% 233,034 231,344 230,252 236,038 239,710 $275,001 and up 274 11.04% 412,780 375,204 385,807 403,017 509,188 Average Closed Price: Total Closed Units: Total Closed Volume: $152,510 2,482 378,530,713 $104,075 $128,966 $229,542 $335,035 500 1358 547 77 52.04M 175.14M 125.56M 25.80M Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. Steve Reese 405-848-9944 steve@oklahomarealtors.com pp. 8

- 10. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® January 2014 Closed Sales as of Feb 12, 2014 Average Percent of List Price to Selling Price Report Produced on: Feb 12, 2014 Area Delimited by Entire OK State MLS - Single-Family Property Type JANUARY 2010 2011 2013 2014 96.34% 95.46% 2012 YEAR TO DATE (YTD) 96.25% 2011 2012 95.22% 2013 2014 96.34% 95.46% 95.30% 95.22% 2010 96.25% 95.30% 1 Year -0.09% 2 Year +0.99% 1 Year -0.09% 2 Year +0.99% 5 YEAR MARKET ACTIVITY TRENDS 5yr JAN AVG=95.71% Average List/Sell Price High Dec 2013 = 97.23% Low Jan 2011 = 95.22% 98 97 96 95 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 Dec 2012 Jun 2013 Dec 2013 3 MONTHS N 96.25% O V D 97.23% E Average List/Sell this C 1.02% month at 96.25%, above the 5 yr JAN J 96.25% A average of 95.71% N -1.01% AVERAGE L/S% OF CLOSED SALES & BEDROOMS DISTRIBUTION BY PRICE Distribution of $avgmed L/S % by Price Range % AVL/S% 2 Beds 3 Beds 4 Beds 5 Beds+ 125 5.04% 89.79% 86.85% 91.77% 94.34%102.87% $25,001 $50,000 243 9.79% 91.81% 92.05% 90.88% 95.86% 92.55% $50,001 $100,000 Ready to Buy or Sell Real Estate? Contact an experienced REALTOR $25,000 and less 569 22.93% 96.75% 96.16% 97.08% 96.51% 89.29% $100,001 $150,000 580 23.37% 96.56% 95.09% 96.94% 96.28% 95.66% $150,001 $200,000 376 15.15% 98.36% 97.91% 98.72% 97.87% 97.68% $200,001 $275,000 315 12.69% 97.54% 97.77% 97.15% 98.03% 95.22% $275,001 and up 274 11.04% 97.05% 96.33% 97.04% 97.28% 96.51% Average List/Sell Ratio: Total Closed Units: Total Closed Volume: 96.20% 2,482 378,530,713 94.54% 500 52.04M 96.48% 1358 175.14M 97.24% 547 125.56M Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. Steve Reese 405-848-9944 steve@oklahomarealtors.com 96.15% 77 25.80M pp. 9

- 11. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® January 2014 Inventory as of Feb 12, 2014 Market Summary Report Produced on: Feb 12, 2014 Area Delimited by Entire OK State MLS - Single-Family Property Type Inventory Inventory Market Activity New Listings 5,849 = 22.80% Closed Sales 2,482 = 8.83% Start Inventory 19,802 Pending Sales 3,483 = 12.39% Total Inventory Units 25,651 Volume $5,026,512,991 Other Off Market 2,962 = 10.53% Active Inventory 19,192 = 68.25% JANUARY Absorption: Last 12 months, an Average of 3,641 Sales/Month Pending Listings 2,482 3,483 5,849 158,360 152,510 96.25% 82.43 19,192 5.27 -1.97% 1.66% -1.43% 2.51% 2.04% -0.09% 0.87% -6.61% -12.00% 2013 2014 2,482 3,483 5,849 158,360 152,510 96.25% 82.43 19,192 5.27 2,532 3,426 5,934 154,477 149,464 96.34% 81.71 20,550 5.99 +/-% -1.97% 1.66% -1.43% 2.51% 2.04% -0.09% 0.87% -6.61% -12.00% 2013 2014 AVERAGE PRICES List Price Sale Price 158,360 5,849 154,477 3,426 -1.43% 3,483 149,464 +1.66% +2.51% 2013 2014 INVENTORY 20,550 +/-% 2013 2014 JANUARY MARKET Active Inventory 2014 2,532 3,426 5,934 154,477 149,464 96.34% 81.71 20,550 5.99 Closed Sales Pending Sales New Listings Average List Price Average Sale Price Average Percent of List Price to Selling Price Average Days on Market to Sale Monthly Inventory Months Supply of Inventory 5,934 Year To Date 2013 Active Inventory as of January 31, 2014 = 19,192 New Listings Market Activity Monthly Supply of Inventory 5.99 +2.04% AVERAGE L/S% & DOM % of List to Sale Price 82.43 5.27 96.25% -6.61% -12.00% -0.09% 81.71 +0.87% Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. 405-848-9944 2013 2014 Days on Market to Sale 96.34% 19,192 Steve Reese 152,510 steve@oklahomarealtors.com pp. 10