Downloaded 11 times

![Mandatory Requirements

As per the latest update of 4th August 2015, the RBI Remains Cautious and there was no

change in the policy Rates.

The Repo rate under the liquidity adjustment facility (LAF) kept unchanged at 7.25 per

cent; the Reverse repo rate unchanged at 6.25 per cent, and the marginal standing

facility (MSF) rate and the Bank Rate at 8.25 per cent.

CRR continues to be at 4% [As per Third Bi-monthly Monetary Policy Review, 2015-

16 presented on 4th August, 2015]

According to the Reserve Bank of India (RBI), the banking sector in India is sound,

adequately capitalised and well-regulated. Indian financial and economic conditions are

much better than in many other countries of the world. In spite of India being a

developing nation for over the years, credit, market and liquidity risk studies show that

Indian banks are generally resilient and have withstood the global downturn very well as

compared to all the other developing or developed nations across the world. With a sense

of optimism slowly creeping in, the banking industry in India is expecting that 2015 will

bring better growth prospects. This optimism stems from factors such as the new

government working hard to revitalise the industrial growth in the country and the RBI

initiating a number of measures that would go a long way in helping the banks to

restructure. The recent announcements of RBI, it is felt, are a clear pointer to the future

of the restructured domestic banking industry.](https://image.slidesharecdn.com/5053afa6-f180-493d-9693-31ba8c463cd4-151028024412-lva1-app6891/85/TIMSR-14-320.jpg)

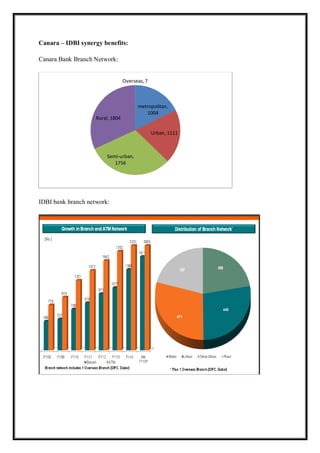

The document discusses the need for consolidation in the Indian banking industry due to factors such as increased competition from foreign banks, changes in banking regulations, and the need for Indian banks to grow in order to finance large acquisitions by Indian companies. It proposes merging IDBI Bank, which has a large MSME and infrastructure lending portfolio and strong technology, with Canara Bank, which has a large retail customer base and a strong presence in South India. This merger could create synergies and benefit both banks. The document provides an overview of the Indian banking sector and macroeconomic conditions in India, and discusses the types and benefits of bank mergers in India.