05:43 AM 1

PartII

Fundamental Concepts in Financial

Management

Chapter - 3

Time value of Money

2.

05:43 AM 2

TimeValue of Money

• The time value of money (TVM) is the concept that a sum of

money is worth more now than the same sum will be at a

future date due to its potential earnings in the interim.

• The birr on hand today can be used to invest and earn

interest or capital gains.

• A birr promised in the future is actually worth less than a

birr today because of inflation.

• States that the value of money changes overtime.

3.

05:43 AM 3

Future(compound) value of a single payment

• A birr you deposited in an interest-bearing account today

worth's you more in the future because the account earns

you interest on the money you have deposited.

• The process of going from today's values, or present values

(PV) to future values (FV) is called Compounding.

• To illustrate this, suppose you deposited 100 Birr at the

Commercial Bank of Ethiopia (CBE) which pays 5 percent

interest each year. How much would you have at the end of

one year?

4.

05:43 AM 4

Tobegin, it is very wise to define the following terms:

PV =Present value, or the beginning amount, in your account.

Here PV = 100 Birr.

i = interest rate that the bank pays per year. Here, i = 5%,

INT = Birrs of interest you earn during the year,

Here, INT = 100 x 0.05 = 5 Birr for the first year.

FVn =Future value, or ending amount, in your account at the end of

n years.

The PV is the value now, or the present value

FVn is the value of the money after n years into the future, after the

earned interests have been added to the account balance every year.

n = number of periods involved in the analysis, Here n = 1.

5.

05:43 AM 5

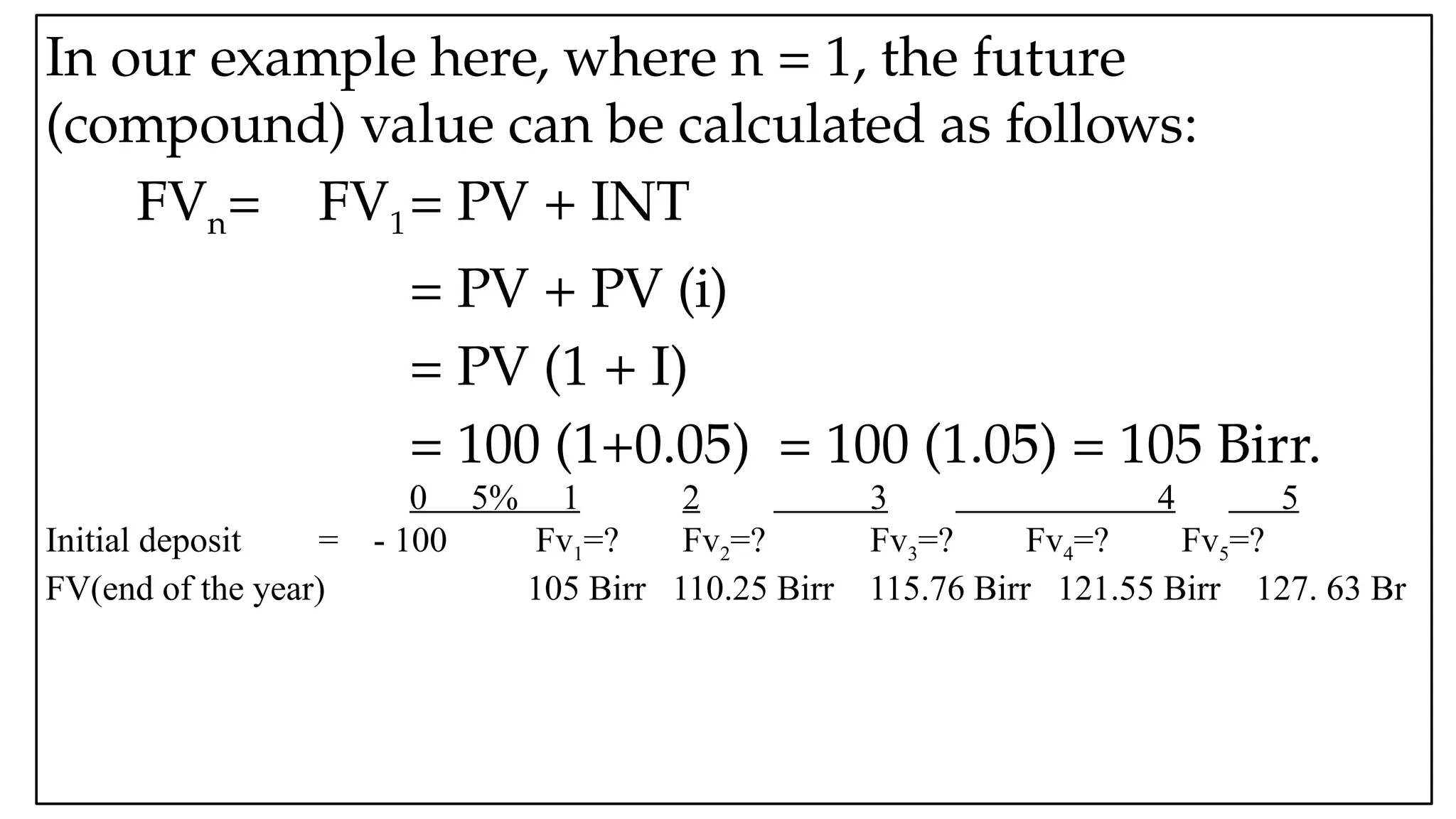

Inour example here, where n = 1, the future

(compound) value can be calculated as follows:

FVn= FV1= PV + INT

= PV + PV (i)

= PV (1 + I)

= 100 (1+0.05) = 100 (1.05) = 105 Birr.

0 5% 1 2 3 4 5

Initial deposit = - 100 Fv1=? Fv2=? Fv3=? Fv4=? Fv5=?

FV(end of the year) 105 Birr 110.25 Birr 115.76 Birr 121.55 Birr 127. 63 Br

6.

05:43 AM 6

UsingInterest Table

• The future value interest factor for i and n (FV1Fi,n,) is

defined as (1+i)n, and this factor can be found by using a

regular calculator.

• The interest table is the table that is constructed by using

the future value interest factors.

• It contains future value interest factors (FVIFi,n,) values for

the wide range of I and n values.

• Since the term (1+i)n is equal to the FV1Fi,n, the future

value equation for a single payment can be re-written as:

7.

05:43 AM 7

•To illustrate how to use future value interest factors (FVIF)

in computing the future (compound) value of any single

payment, consider our five-year, 5 percent interest rate

deposit of 100 Birr in the previous example.

• The future value of the 100 Birr at the end of year 5 can be

determined by looking for the FV1F 5%,5 in the interest

table.

8.

05:43 AM 8

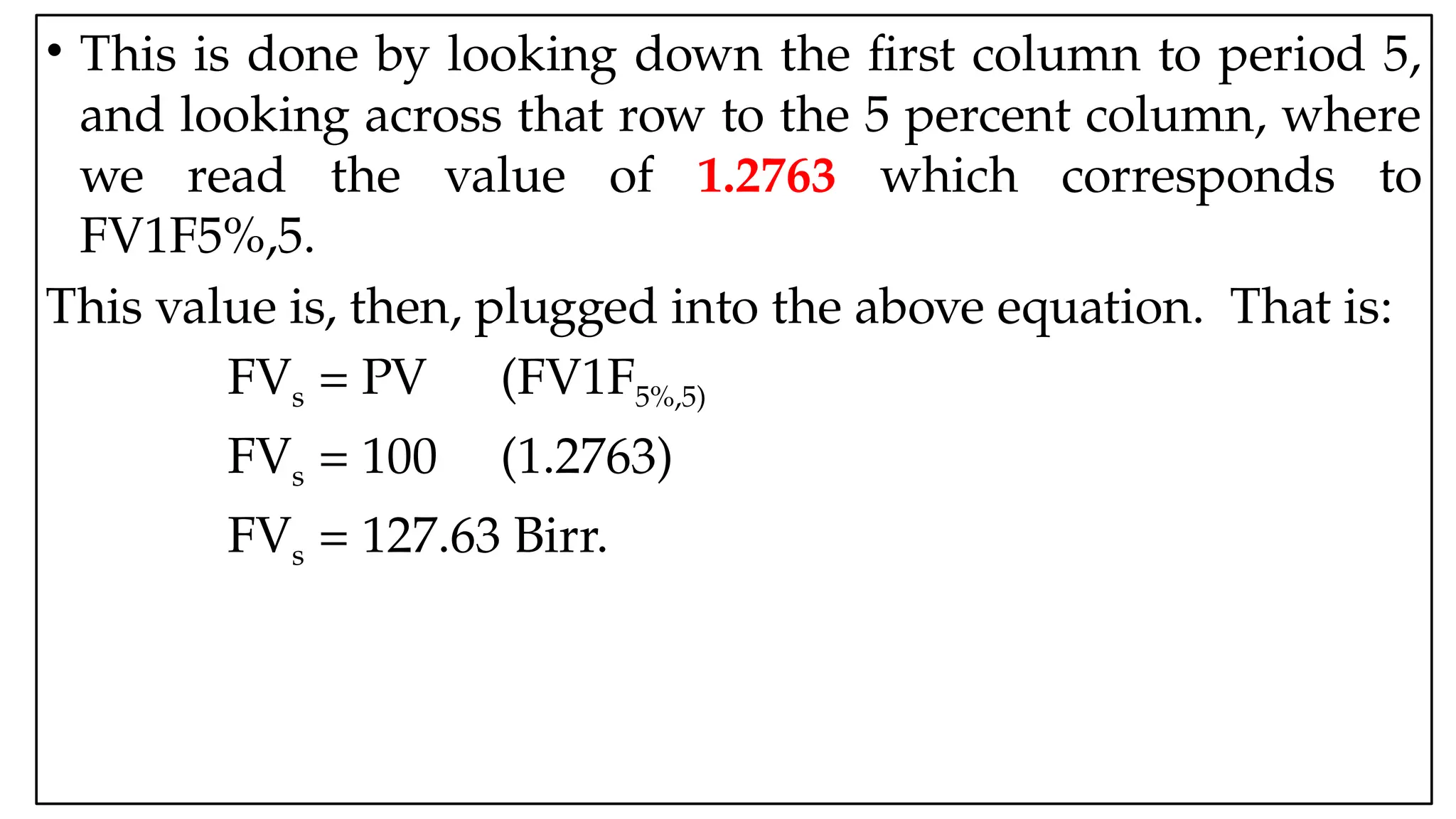

•This is done by looking down the first column to period 5,

and looking across that row to the 5 percent column, where

we read the value of 1.2763 which corresponds to

FV1F5%,5.

This value is, then, plugged into the above equation. That is:

FVs = PV (FV1F5%,5)

FVs = 100 (1.2763)

FVs = 127.63 Birr.

9.

05:43 AM 9

OtherApplications of future value amount of single

payment:

Finding the Interest rate:

• Estimating the interest rate on the deposited money is

a recurring problem when it is not explicitly stated.

• A useful approach is to treat the interest rate as an

implicit interest rate and found by using the interest

table (future value table of single payment).

•

10.

05:43 AM 10

•To illustrate, assume that you have invested 15,000 Birr

today at a bank where it can grow to the future value of

17,900 Birr within three years from now into the future.

• What is the interest rate that the bank should pay for

your account in order to fulfill your desire?

Thus, the interest that the bank actually has to pay to your

account is slightly greater than 6 percent.

11.

05:43 AM 11

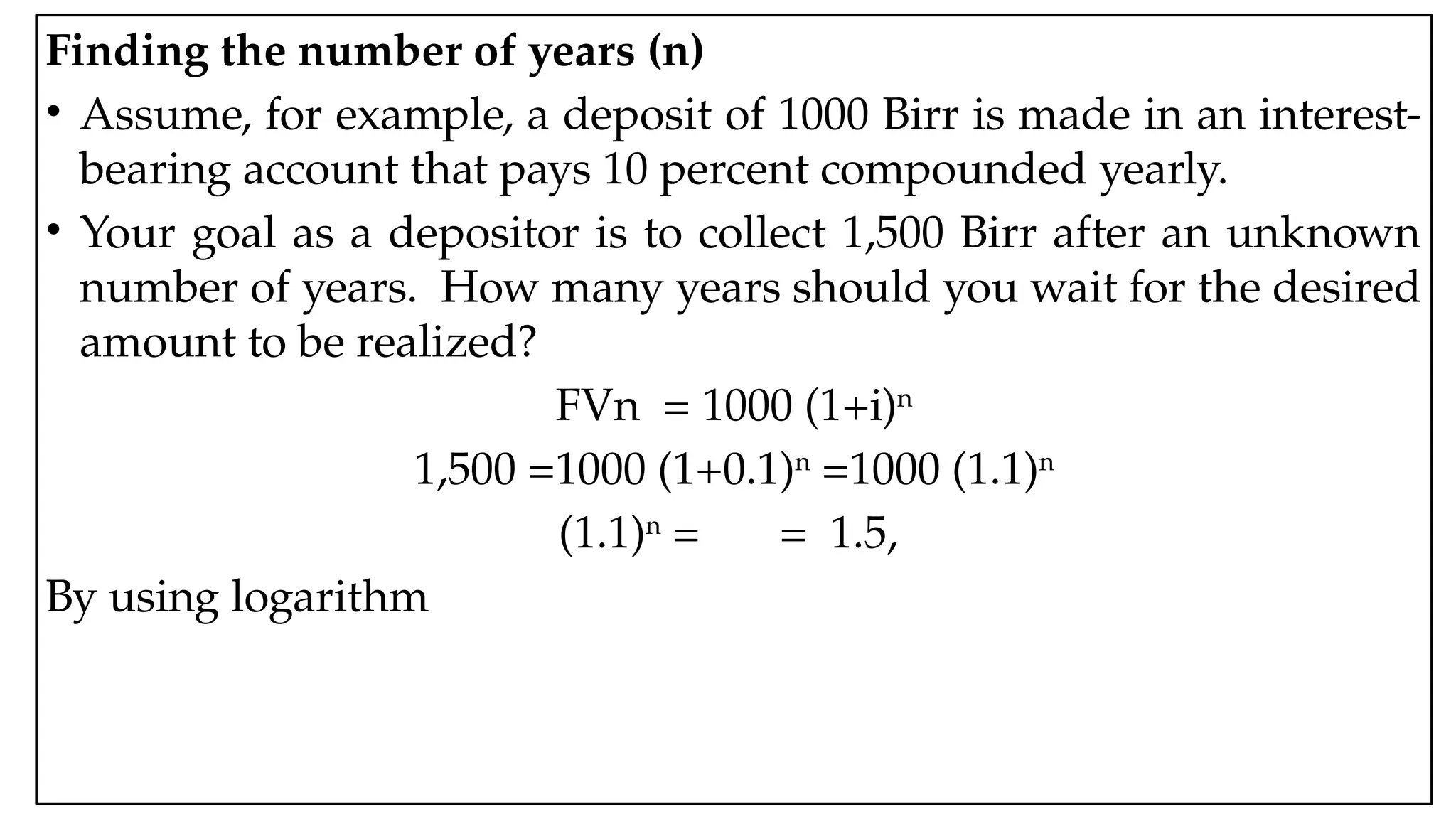

Findingthe number of years (n)

• Assume, for example, a deposit of 1000 Birr is made in an interest-

bearing account that pays 10 percent compounded yearly.

• Your goal as a depositor is to collect 1,500 Birr after an unknown

number of years. How many years should you wait for the desired

amount to be realized?

FVn = 1000 (1+i)n

1,500 =1000 (1+0.1)n

=1000 (1.1)n

(1.1)n

= = 1.5,

By using logarithm

12.

05:43 AM 12

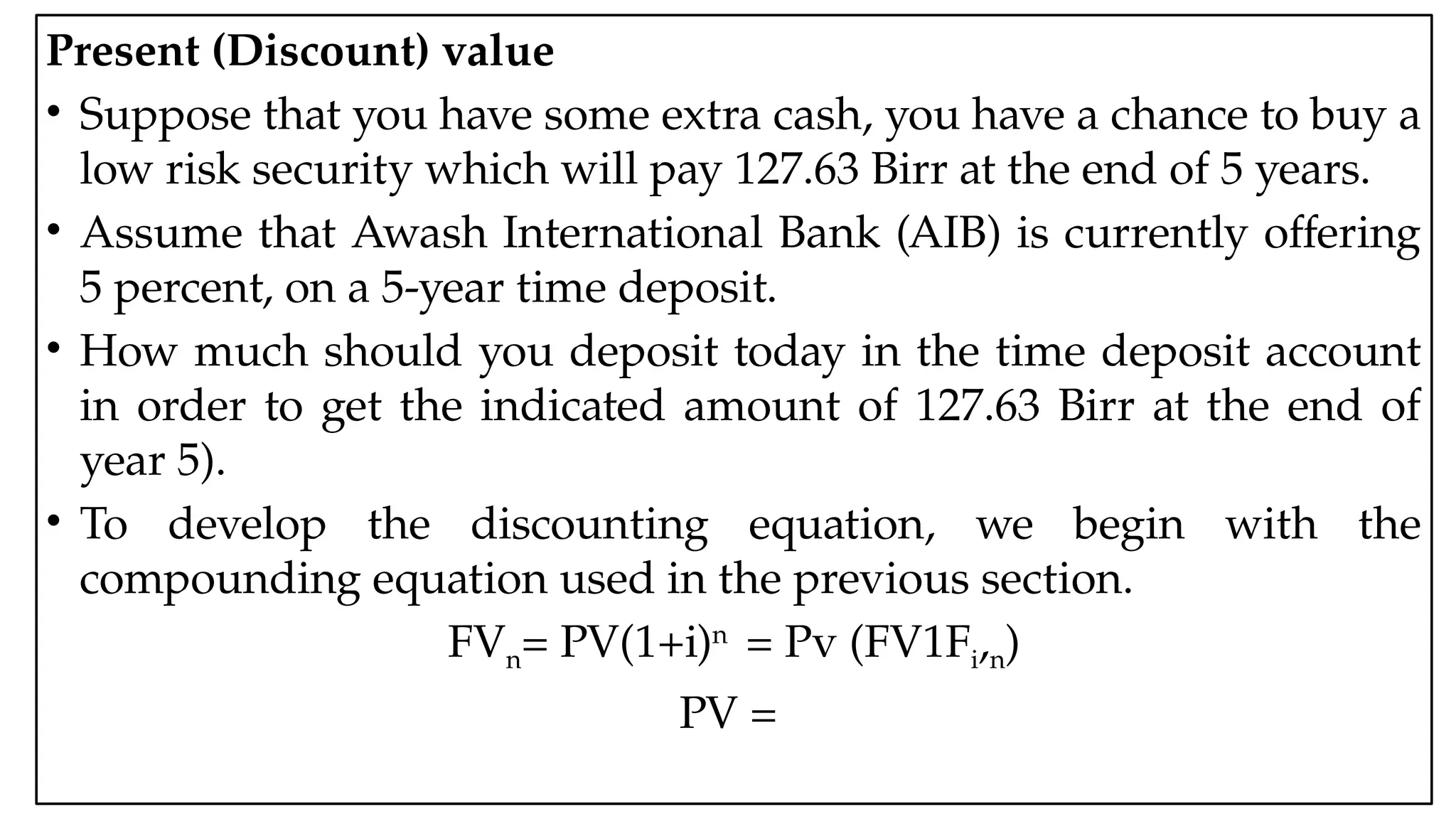

Present(Discount) value

• Suppose that you have some extra cash, you have a chance to buy a

low risk security which will pay 127.63 Birr at the end of 5 years.

• Assume that Awash International Bank (AIB) is currently offering

5 percent, on a 5-year time deposit.

• How much should you deposit today in the time deposit account

in order to get the indicated amount of 127.63 Birr at the end of

year 5).

• To develop the discounting equation, we begin with the

compounding equation used in the previous section.

FVn= PV(1+i)n

= Pv (FV1Fi,n)

PV =

13.

05:43 AM 13

•Hence, you can insert the figures into the present value

equation in order to determine the present value of 100 Birr

as indicated here:

PV =

= 100 Birr

14.

05:43 AM 14

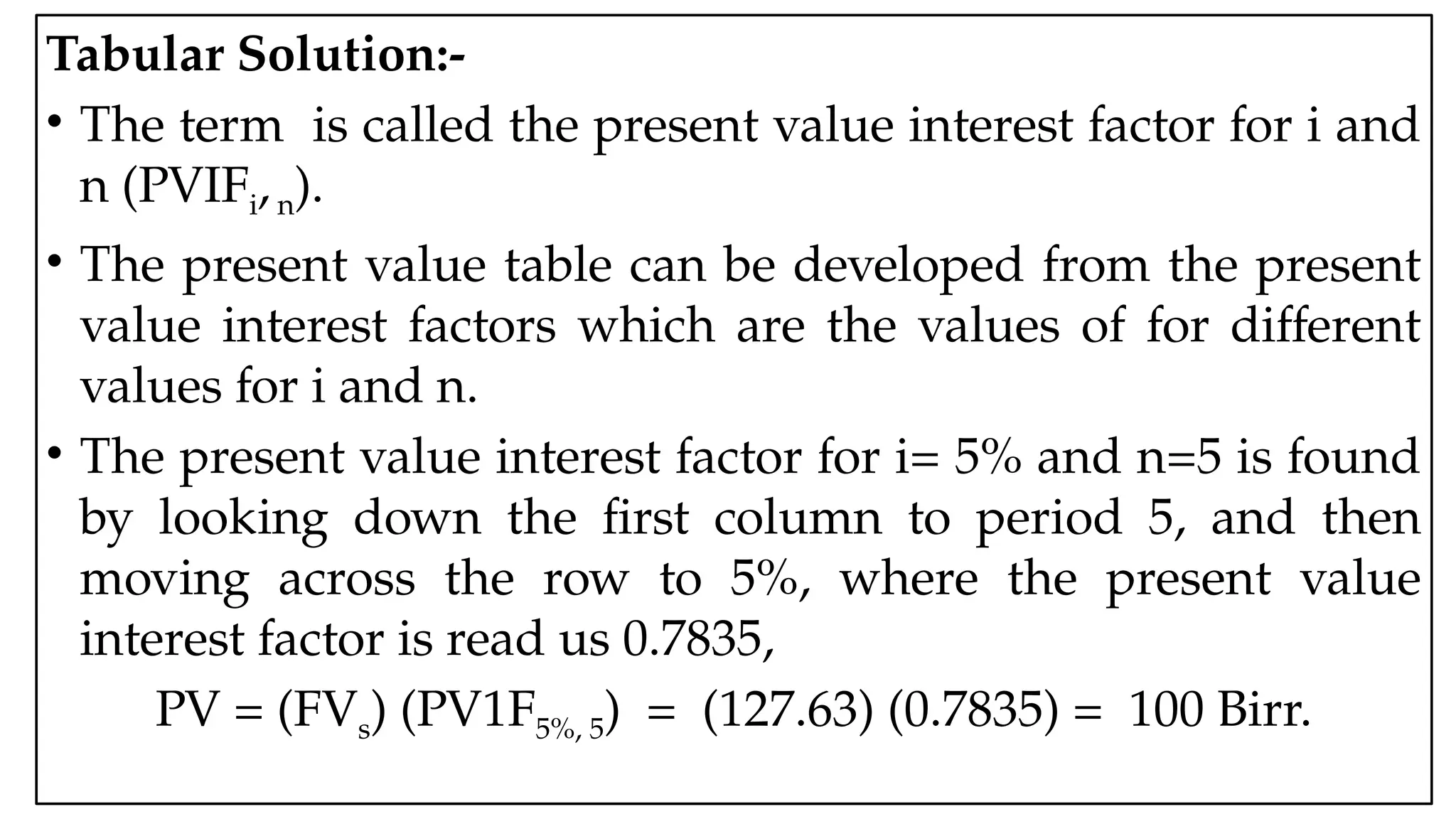

TabularSolution:-

• The term is called the present value interest factor for i and

n (PVIFi,n).

• The present value table can be developed from the present

value interest factors which are the values of for different

values for i and n.

• The present value interest factor for i= 5% and n=5 is found

by looking down the first column to period 5, and then

moving across the row to 5%, where the present value

interest factor is read us 0.7835,

PV = (FVs) (PV1F5%, 5) = (127.63) (0.7835) = 100 Birr.

15.

05:43 AM 15

OtherApplication of Present Value of the Single Payment

• Finding the Interest Rate:

• To illustrate this, suppose that you have taken a loan of 1200 Birr to day

which is to be paid after three years together with its interest by making a

payment of 1500 Birr.

• What is the rate of interest on the loan that you have taken?

16.

05:43 AM 16

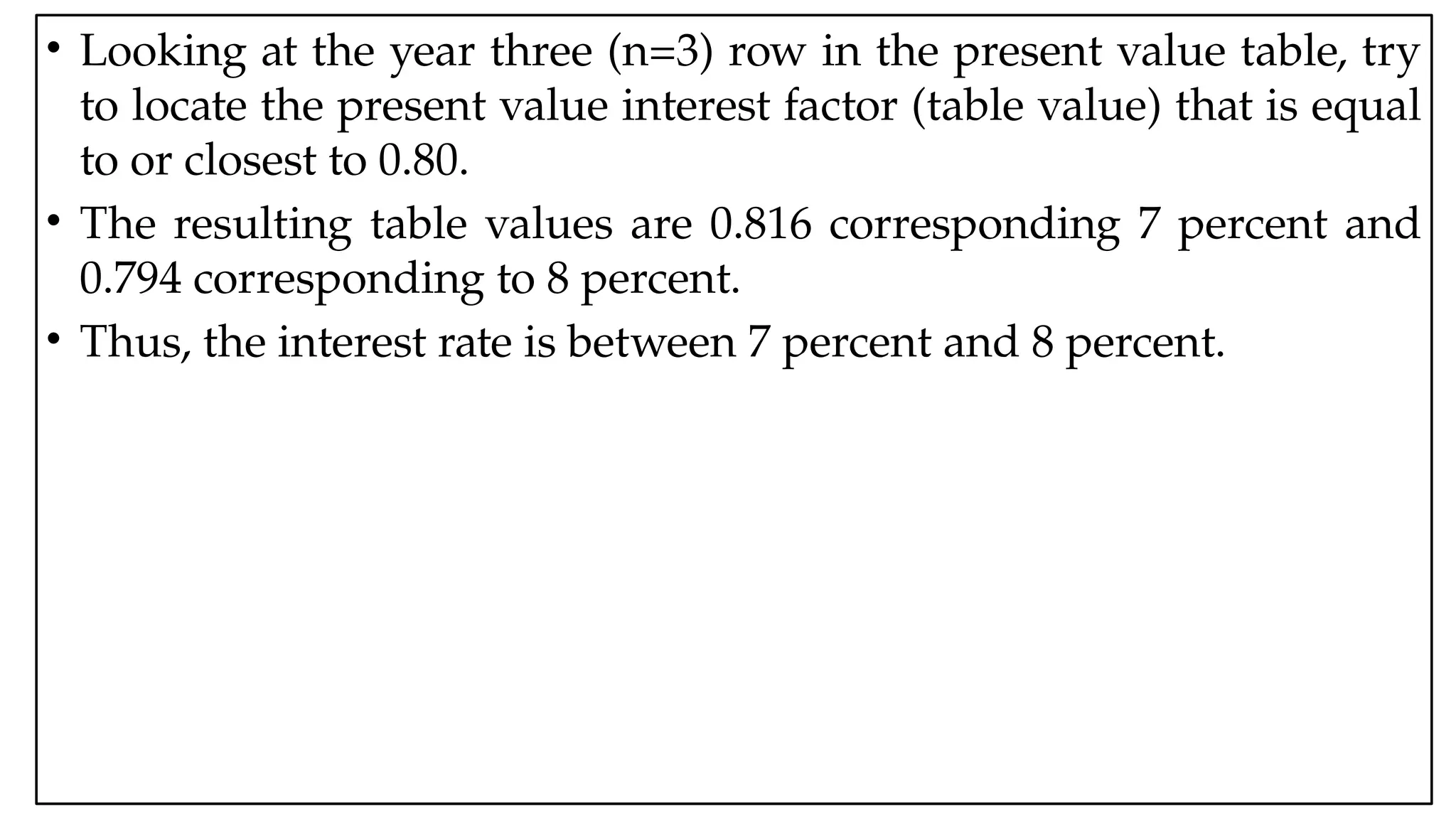

•Looking at the year three (n=3) row in the present value table, try

to locate the present value interest factor (table value) that is equal

to or closest to 0.80.

• The resulting table values are 0.816 corresponding 7 percent and

0.794 corresponding to 8 percent.

• Thus, the interest rate is between 7 percent and 8 percent.

17.

05:43 AM 17

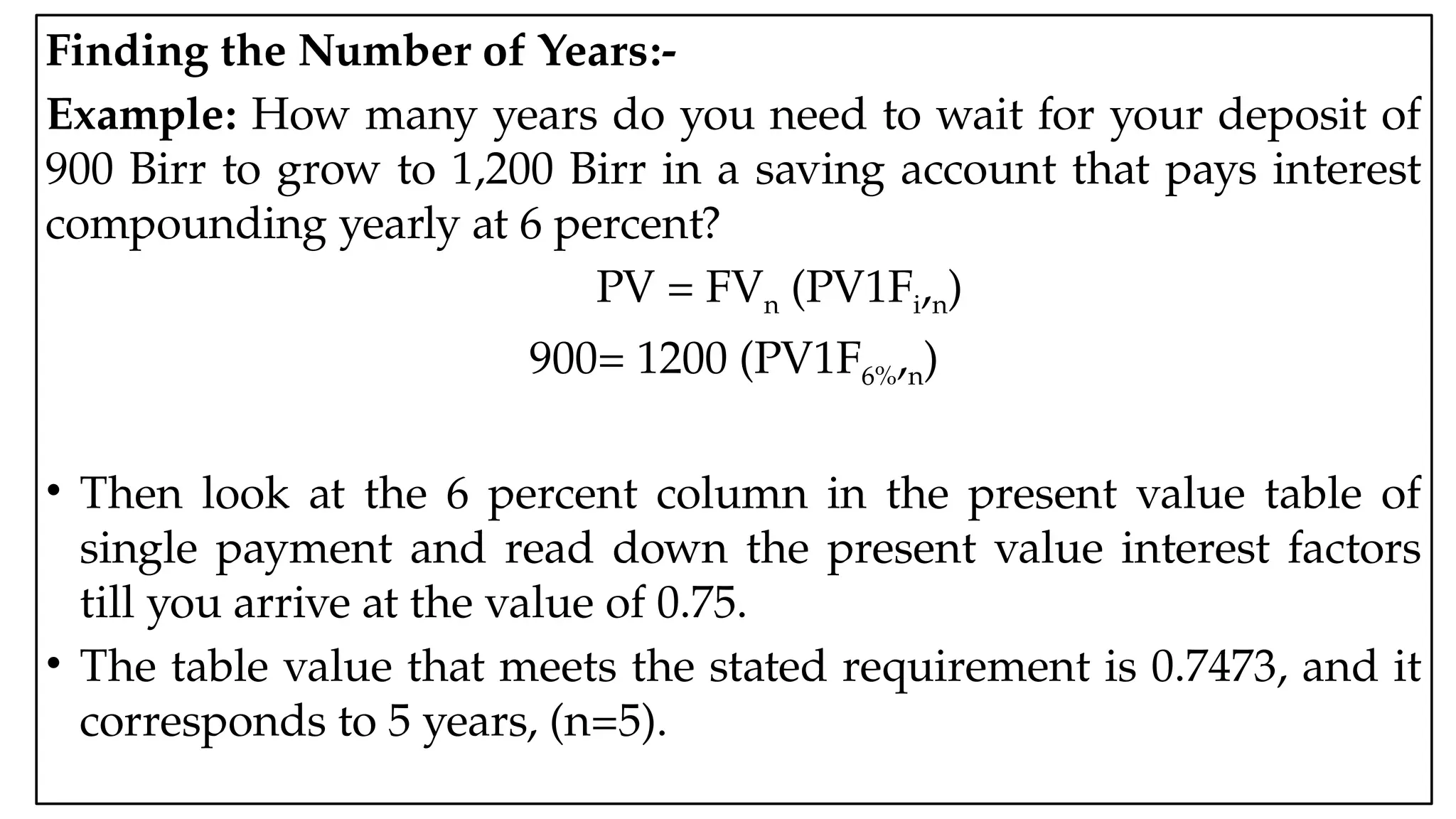

Findingthe Number of Years:-

Example: How many years do you need to wait for your deposit of

900 Birr to grow to 1,200 Birr in a saving account that pays interest

compounding yearly at 6 percent?

PV = FVn (PV1Fi,n)

900= 1200 (PV1F6%,n)

• Then look at the 6 percent column in the present value table of

single payment and read down the present value interest factors

till you arrive at the value of 0.75.

• The table value that meets the stated requirement is 0.7473, and it

corresponds to 5 years, (n=5).

18.

05:43 AM 18

Annuities

•An annuity is an equal amount of Birr payment for specified number of

years.

• Since annuities occur frequently in finance, such as bond interest

payments, you have to be able treat them accordingly.

• Although compounding and discounting of annuities can be dealt with for

single payment, these processes are time consuming, especially for longer

annuities.

• The annuity payments can occur at either the beginning or the end of

period.

• If the payments are made at the beginning of each period, the annuity is

known as annuity due.

• If the payments, on the other hand, occur at the end of each period, as

they typically do, the annuity is called an ordinary, or deferred annuity.

19.

05:43 AM 19

FutureValue of Ordinary Annuity (FVOA)

• An ordinary or deferred annuity consists of a series of equal payment

made at the end of each period.

• If you deposit 100 Birr at the end of each year for three years in a saving

account that pays 5 percent per year, how much will you have at the end of

year three (n=3)?

• To answer this question, you must find future value of an annuity, FVOAn.

• Each payment has to be compounded out to the end of period n, and the

sum of the compounded payments gives you the future value of an

annuity, FVAn.

20.

05:43 AM 20

TabularSolution:

• The future value for an annuity is formed from the future

value interest factor for an annuity (FVIFAi,n), which are the

values of the term in the above future value of annuity

FVAn = (PMT) (FVIFAi,n)

FVA3 = (100) (FVIFA5%, 3) = (100) (3.1525) = 315.25 Birr

21.

05:43 AM 21

OtherApplications Future value of Annuity

Finding the Interest Rate:

• To illustrate interest rate computation, three equal payments of 3,000 Birr

are offered in return for 9,800 Birr to be received upon making the last

annuity payment. What is the implied interest rate?

22.

05:43 AM 22

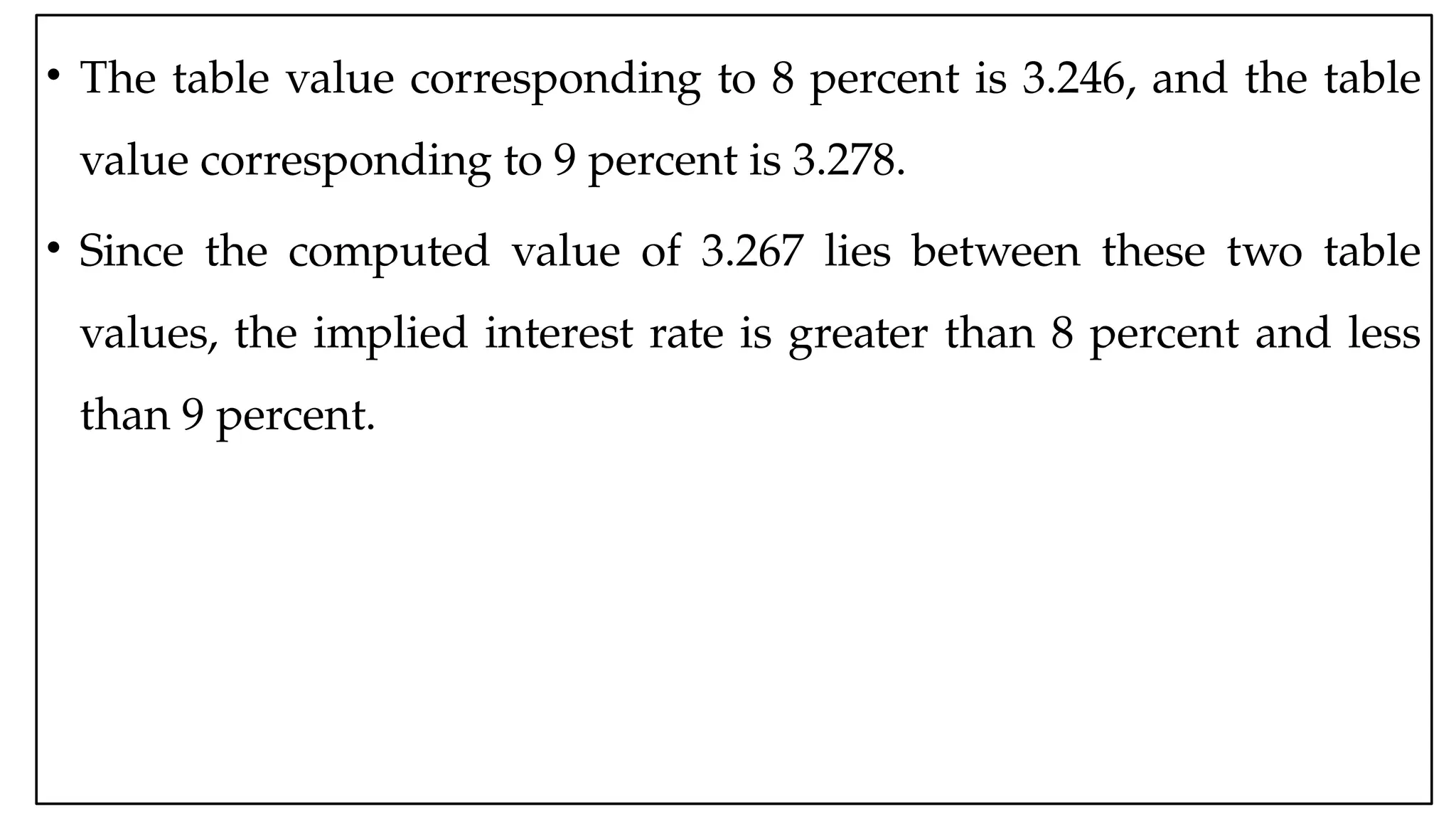

•The table value corresponding to 8 percent is 3.246, and the table

value corresponding to 9 percent is 3.278.

• Since the computed value of 3.267 lies between these two table

values, the implied interest rate is greater than 8 percent and less

than 9 percent.

23.

05:43 AM 23

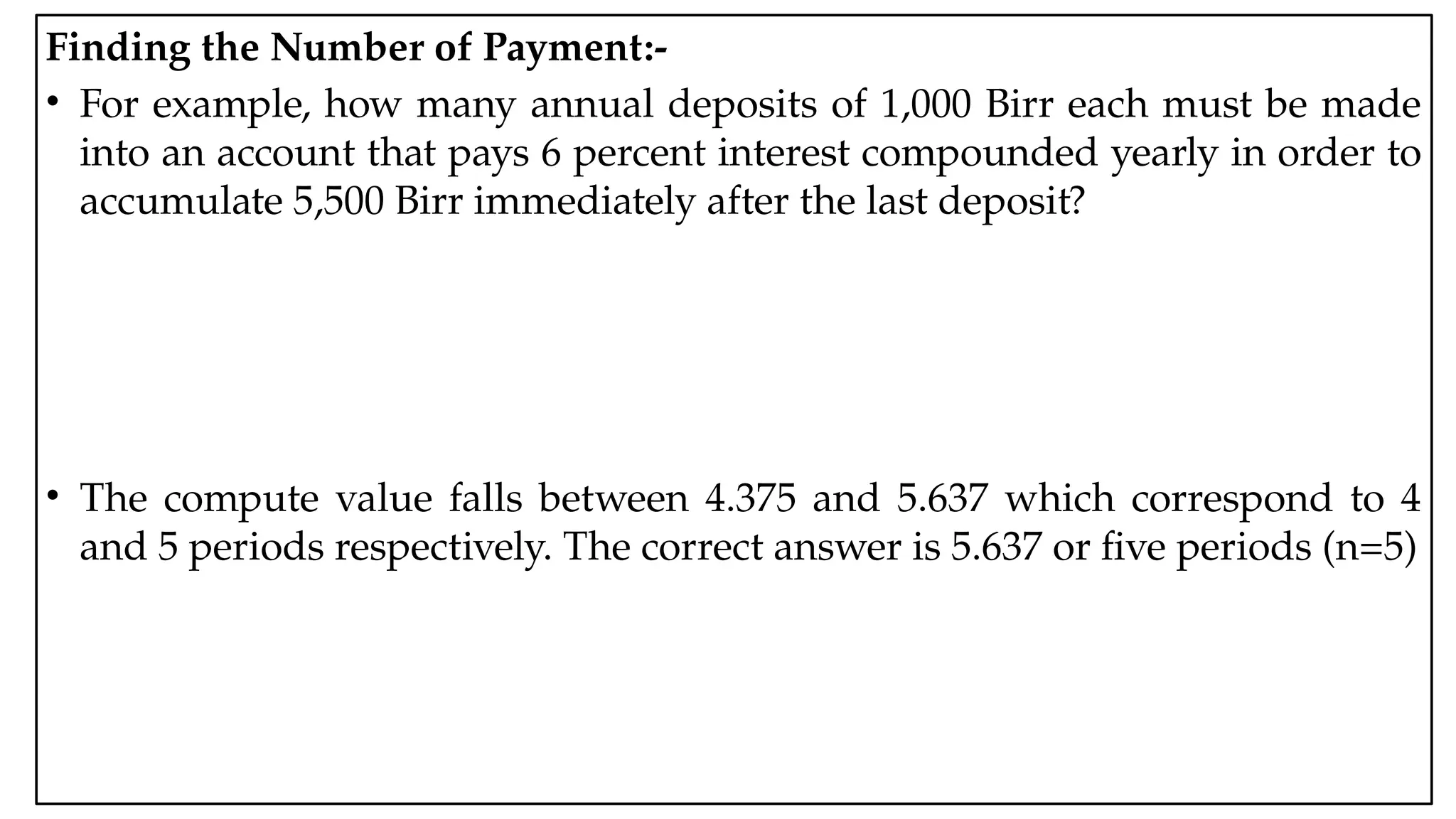

Findingthe Number of Payment:-

• For example, how many annual deposits of 1,000 Birr each must be made

into an account that pays 6 percent interest compounded yearly in order to

accumulate 5,500 Birr immediately after the last deposit?

• The compute value falls between 4.375 and 5.637 which correspond to 4

and 5 periods respectively. The correct answer is 5.637 or five periods (n=5)

24.

05:43 AM 24

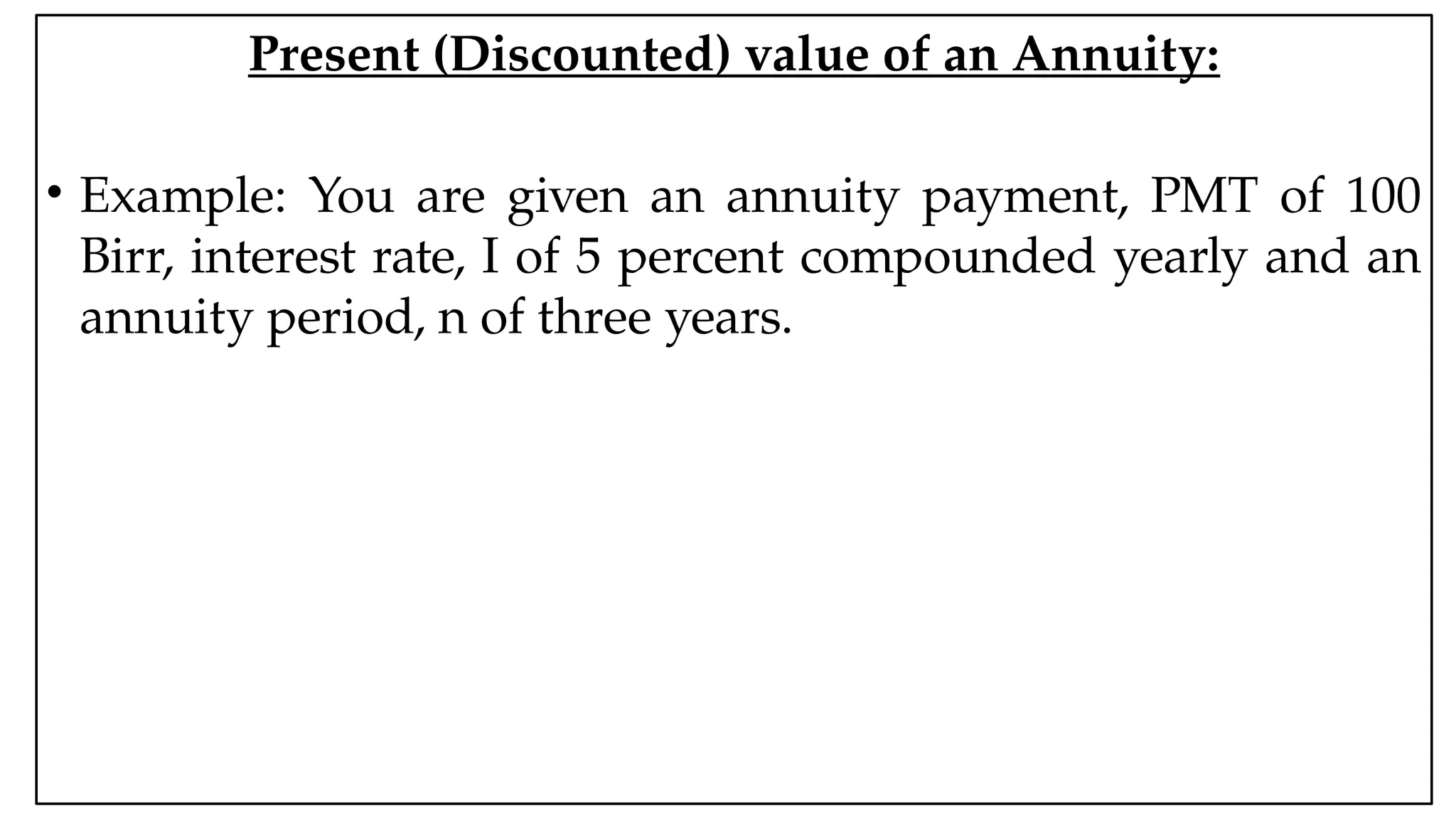

Present(Discounted) value of an Annuity:

• Example: You are given an annuity payment, PMT of 100

Birr, interest rate, I of 5 percent compounded yearly and an

annuity period, n of three years.

25.

05:43 AM 25

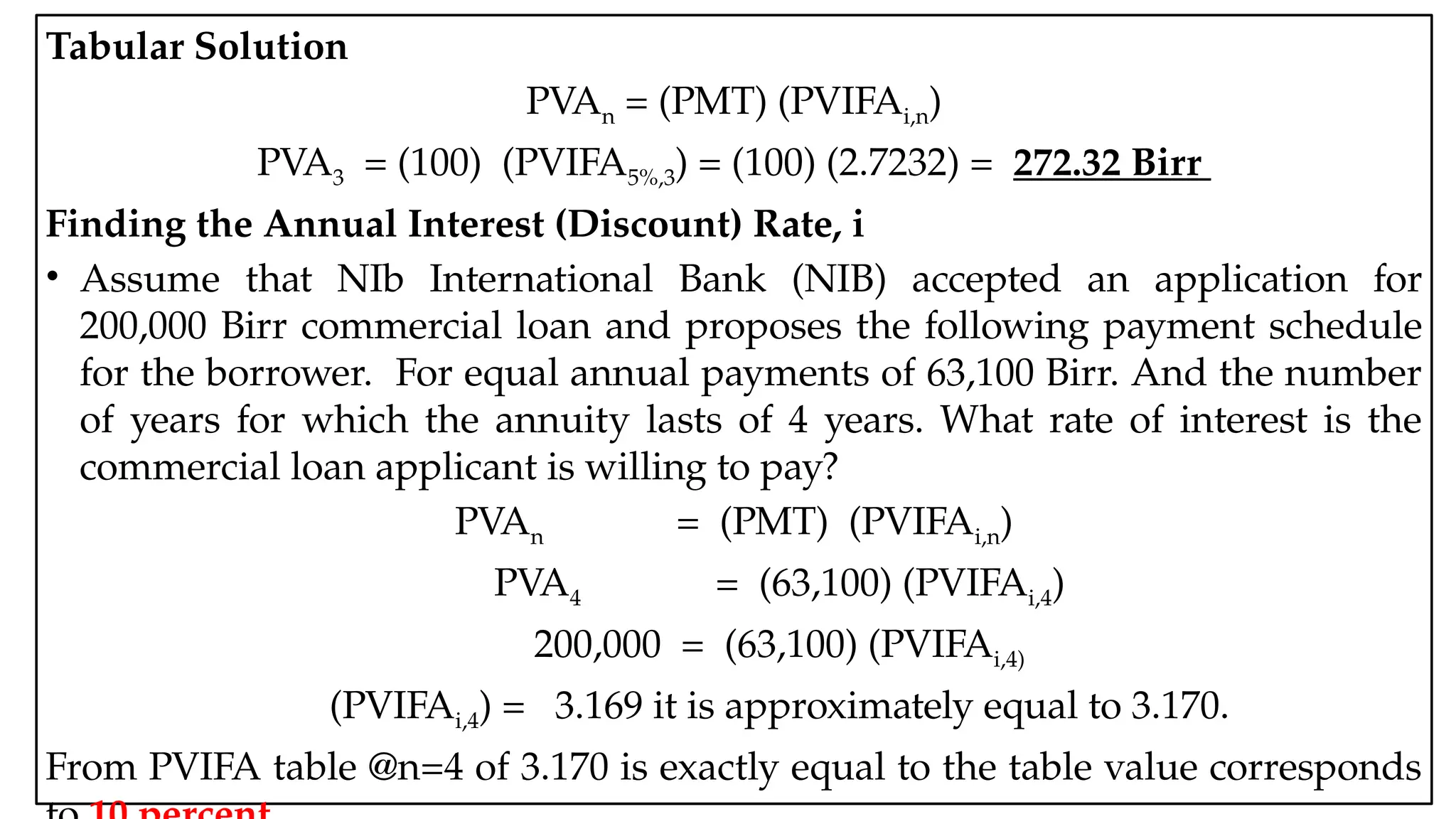

TabularSolution

PVAn = (PMT) (PVIFAi,n)

PVA3 = (100) (PVIFA5%,3) = (100) (2.7232) = 272.32 Birr

Finding the Annual Interest (Discount) Rate, i

• Assume that NIb International Bank (NIB) accepted an application for

200,000 Birr commercial loan and proposes the following payment schedule

for the borrower. For equal annual payments of 63,100 Birr. And the number

of years for which the annuity lasts of 4 years. What rate of interest is the

commercial loan applicant is willing to pay?

PVAn = (PMT) (PVIFAi,n)

PVA4 = (63,100) (PVIFAi,4)

200,000 = (63,100) (PVIFAi,4)

(PVIFAi,4) = 3.169 it is approximately equal to 3.170.

From PVIFA table @n=4 of 3.170 is exactly equal to the table value corresponds

26.

05:43 AM 26

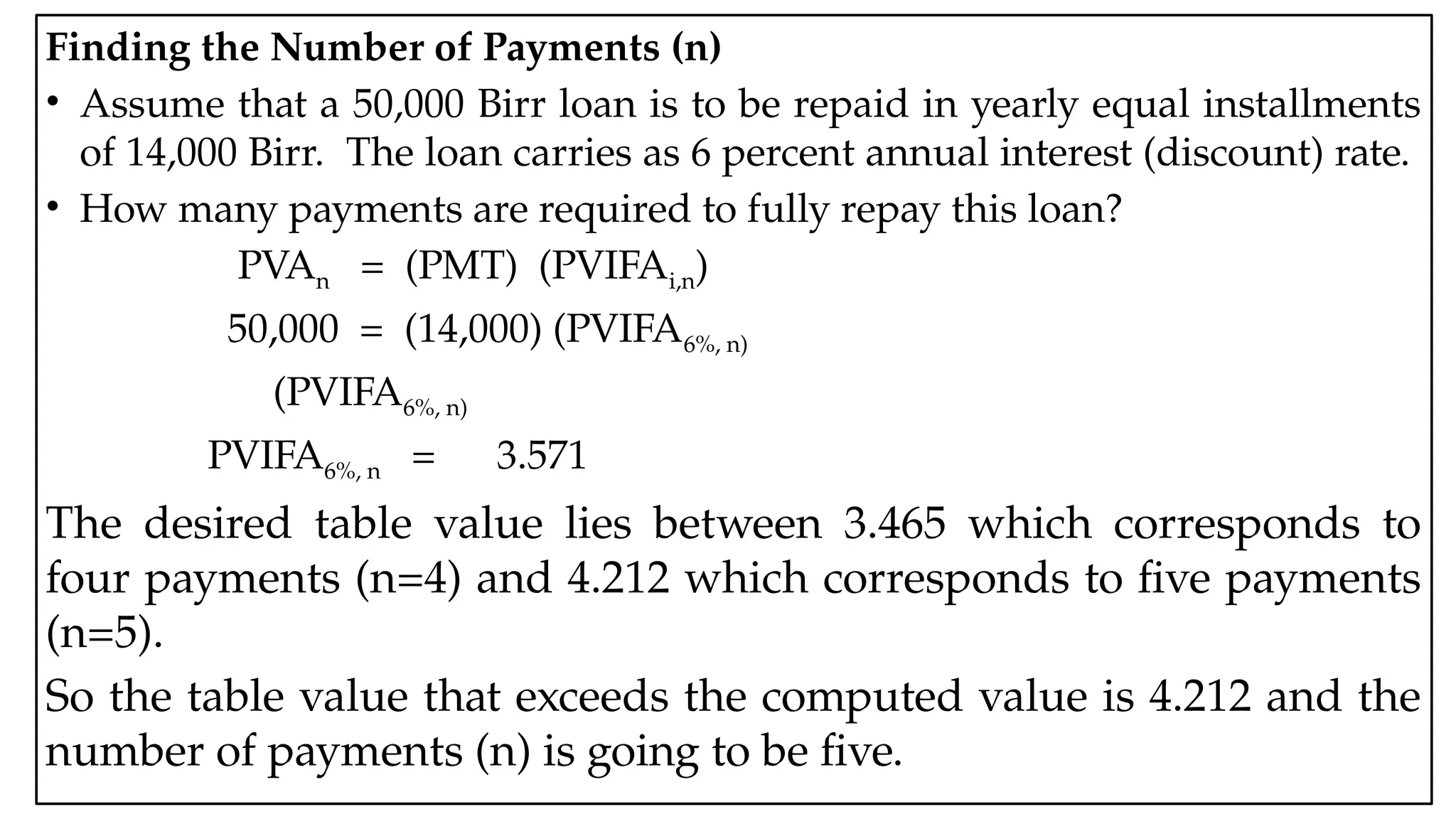

Findingthe Number of Payments (n)

• Assume that a 50,000 Birr loan is to be repaid in yearly equal installments

of 14,000 Birr. The loan carries as 6 percent annual interest (discount) rate.

• How many payments are required to fully repay this loan?

PVAn = (PMT) (PVIFAi,n)

50,000 = (14,000) (PVIFA6%, n)

(PVIFA6%, n)

PVIFA6%, n = 3.571

The desired table value lies between 3.465 which corresponds to

four payments (n=4) and 4.212 which corresponds to five payments

(n=5).

So the table value that exceeds the computed value is 4.212 and the

number of payments (n) is going to be five.

27.

05:43 AM 27

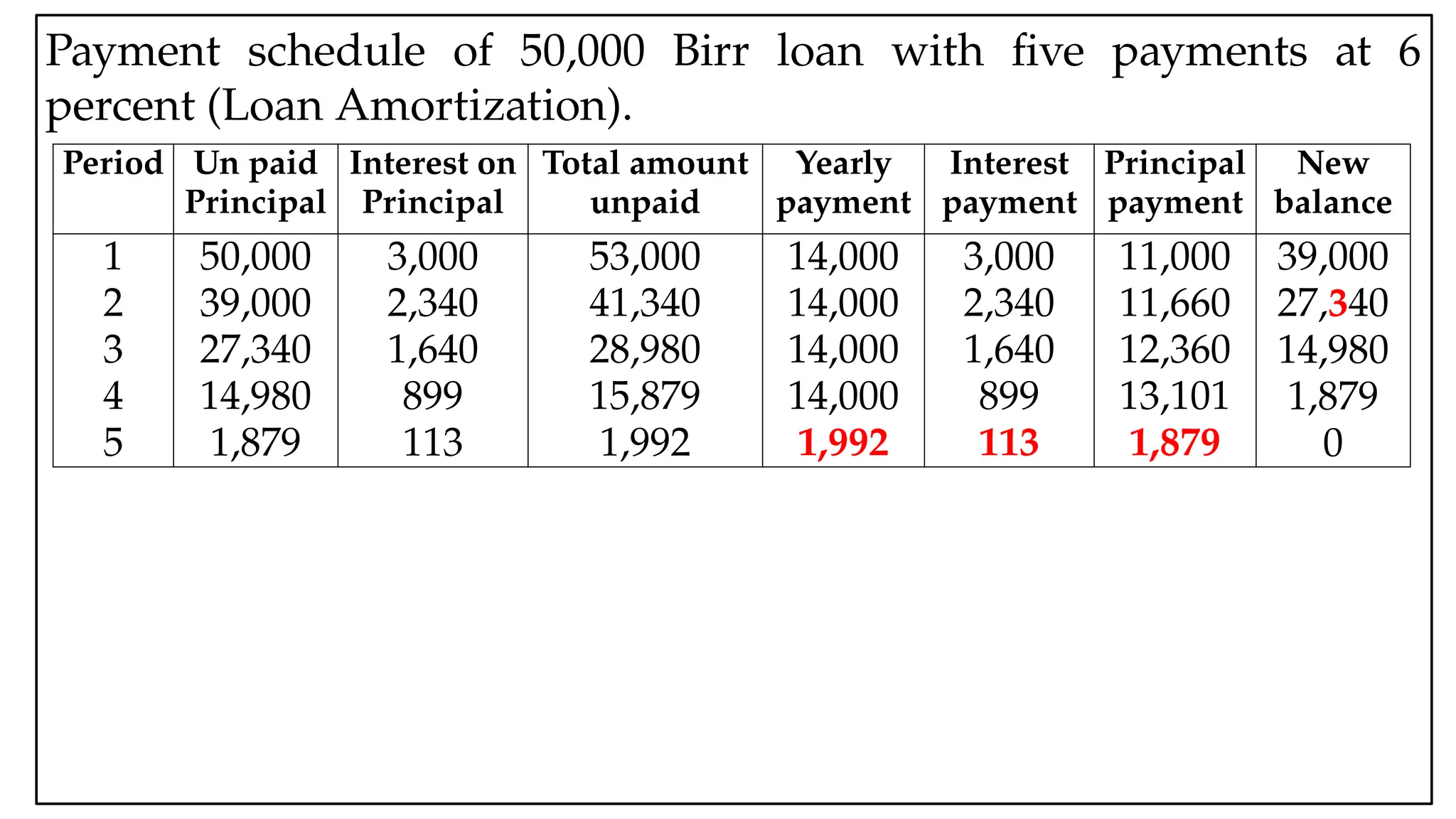

Paymentschedule of 50,000 Birr loan with five payments at 6

percent (Loan Amortization).

Period Un paid

Principal

Interest on

Principal

Total amount

unpaid

Yearly

payment

Interest

payment

Principal

payment

New

balance

1

2

3

4

5

50,000

39,000

27,340

14,980

1,879

3,000

2,340

1,640

899

113

53,000

41,340

28,980

15,879

1,992

14,000

14,000

14,000

14,000

1,992

3,000

2,340

1,640

899

113

11,000

11,660

12,360

13,101

1,879

39,000

27,340

14,980

1,879

0

28.

05:43 AM 28

Unevenor Unequal Cash flows:

• By definition an annuity includes the words 'constant

amount' , which is to underscore that an annuity involves

payments, or receipts that equal in every period, or at the

end of every over the life of the annuity.

• Although many financial decisions do involve annuities,

some important decisions involve unequal, or non-constant

payments, or receipts, or cash flows.

• For example. common stock as you know, pay fluctuating

level of dividends overtime, and fixed assets investments

such as machinery do not generate constant cash flows over

their lives as they depreciate.

29.

05:43 AM 29

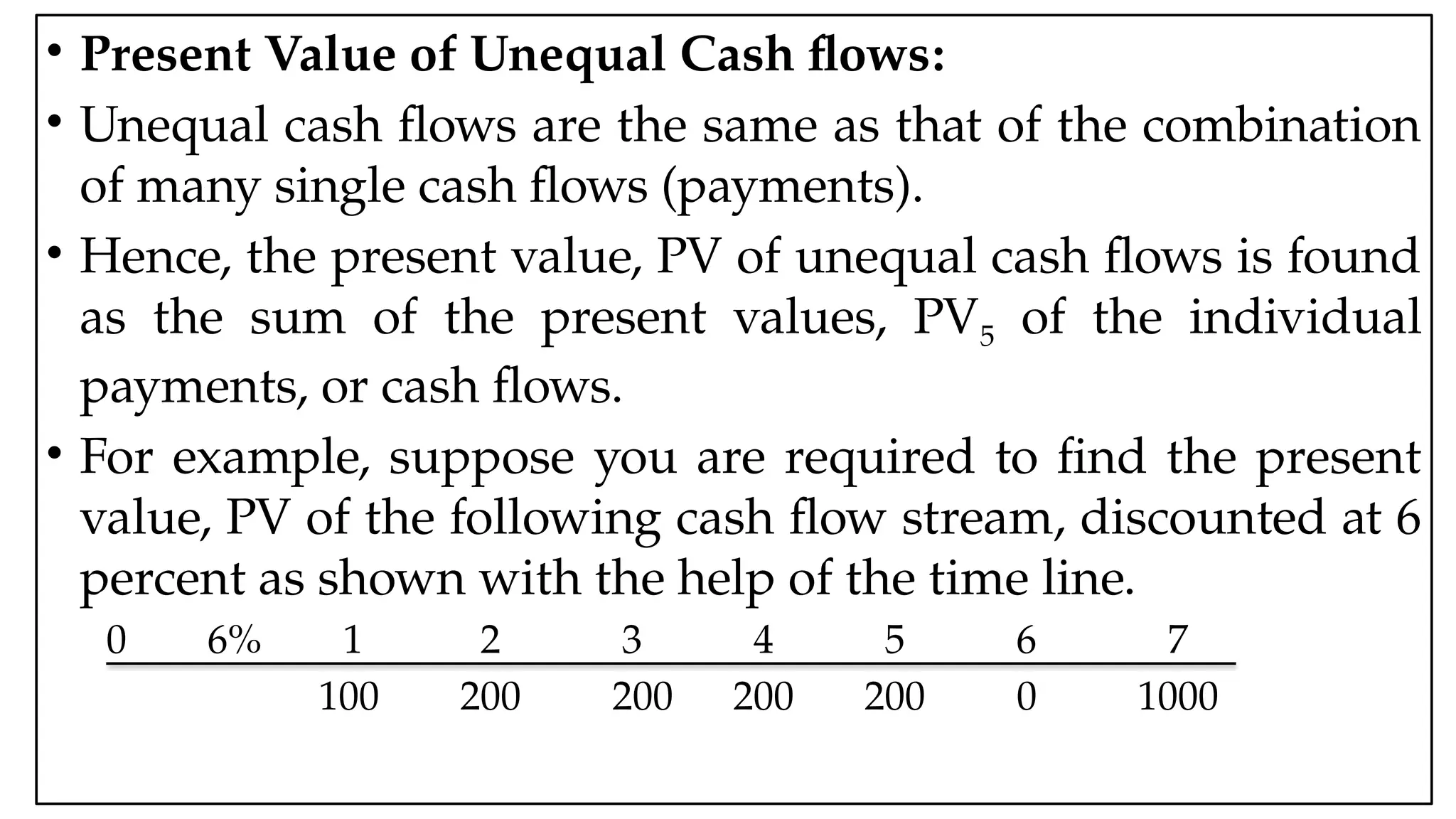

•Present Value of Unequal Cash flows:

• Unequal cash flows are the same as that of the combination

of many single cash flows (payments).

• Hence, the present value, PV of unequal cash flows is found

as the sum of the present values, PV5 of the individual

payments, or cash flows.

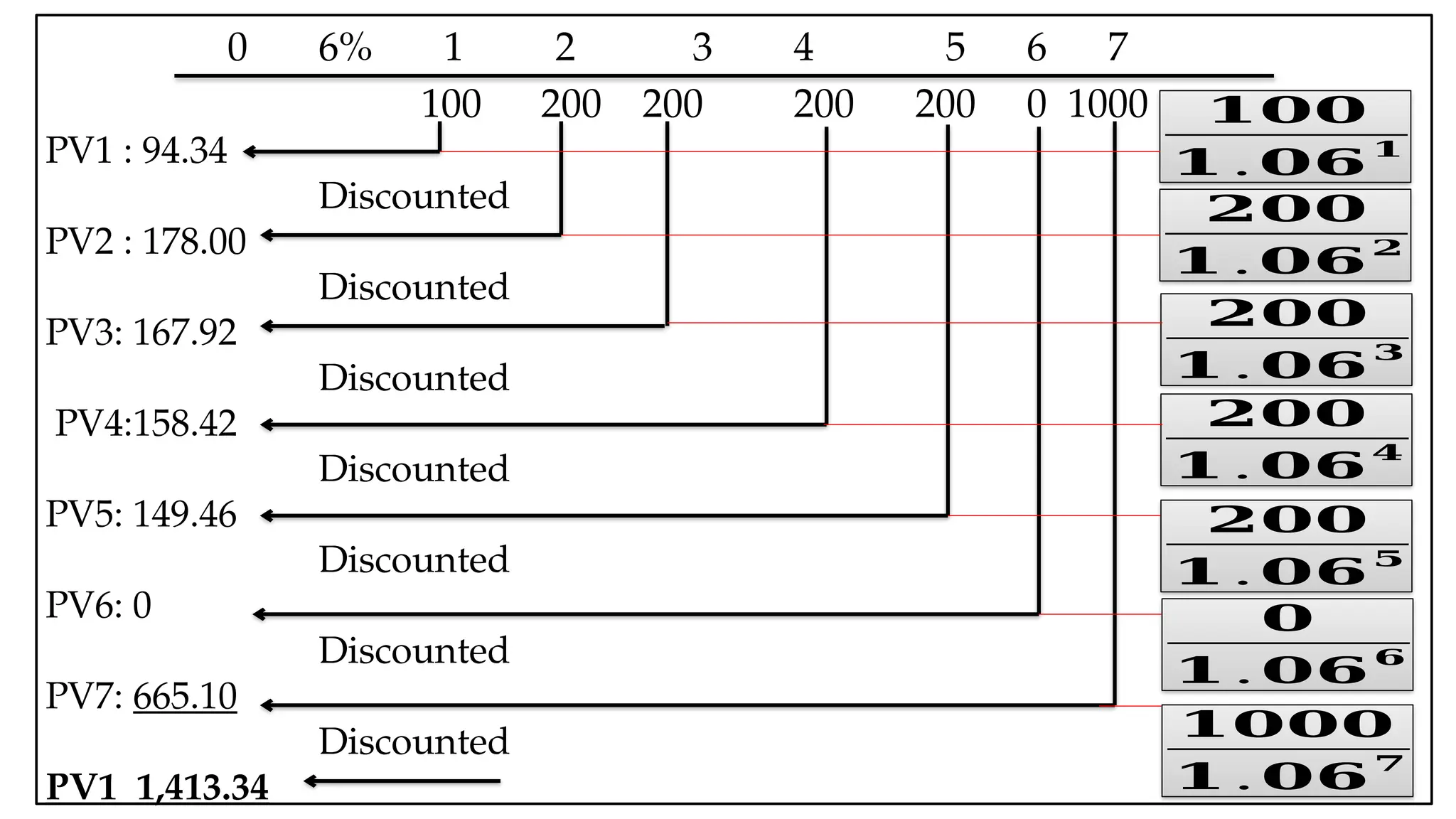

• For example, suppose you are required to find the present

value, PV of the following cash flow stream, discounted at 6

percent as shown with the help of the time line.

0 6% 1 2 3 4 5 6 7

100 200 200 200 200 0 1000

05:43 AM 31

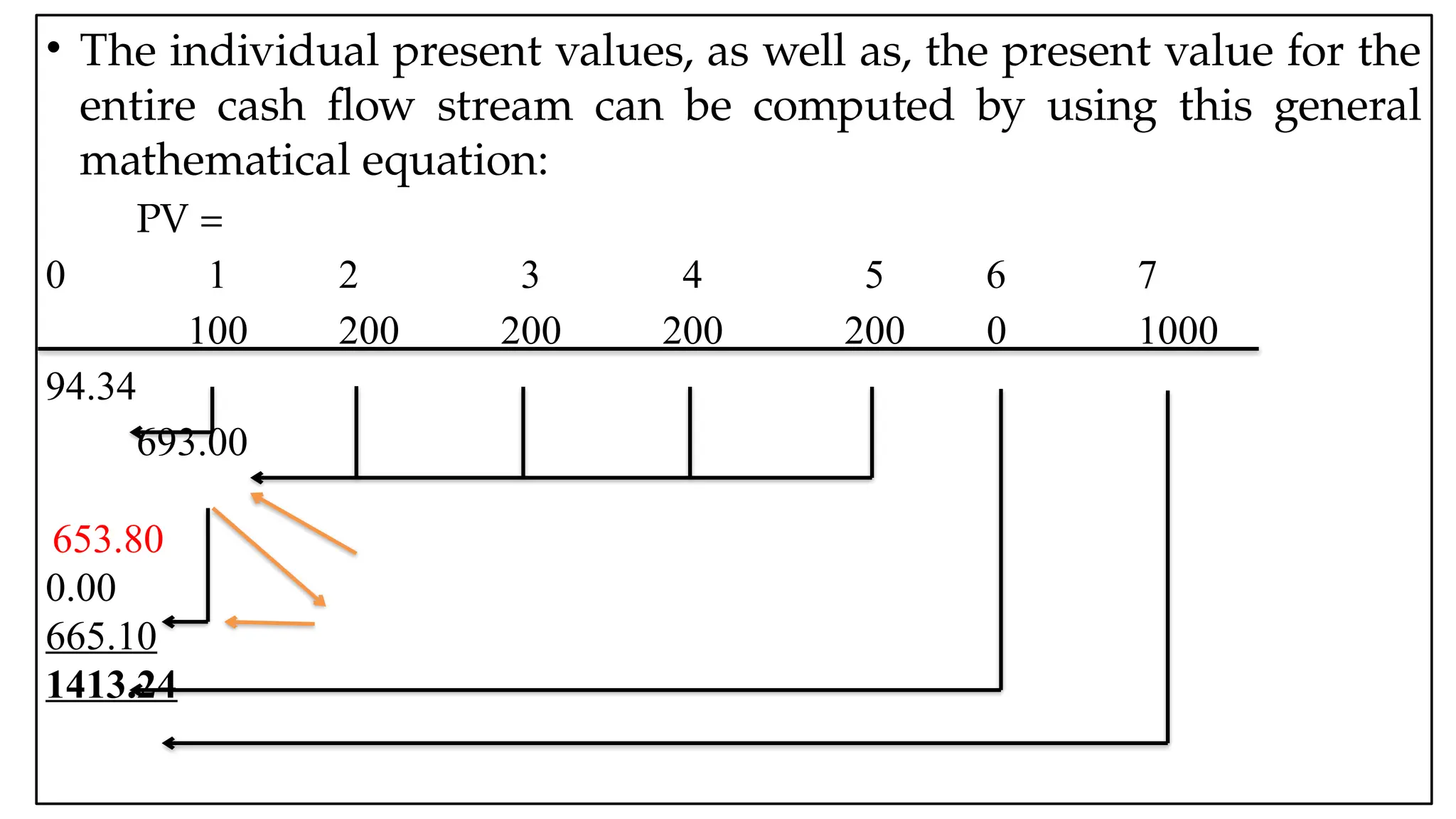

•The individual present values, as well as, the present value for the

entire cash flow stream can be computed by using this general

mathematical equation:

PV =

0 1 2 3 4 5 6 7

100 200 200 200 200 0 1000

94.34

693.00

653.80

0.00

665.10

1413.24

32.

05:43 AM 32

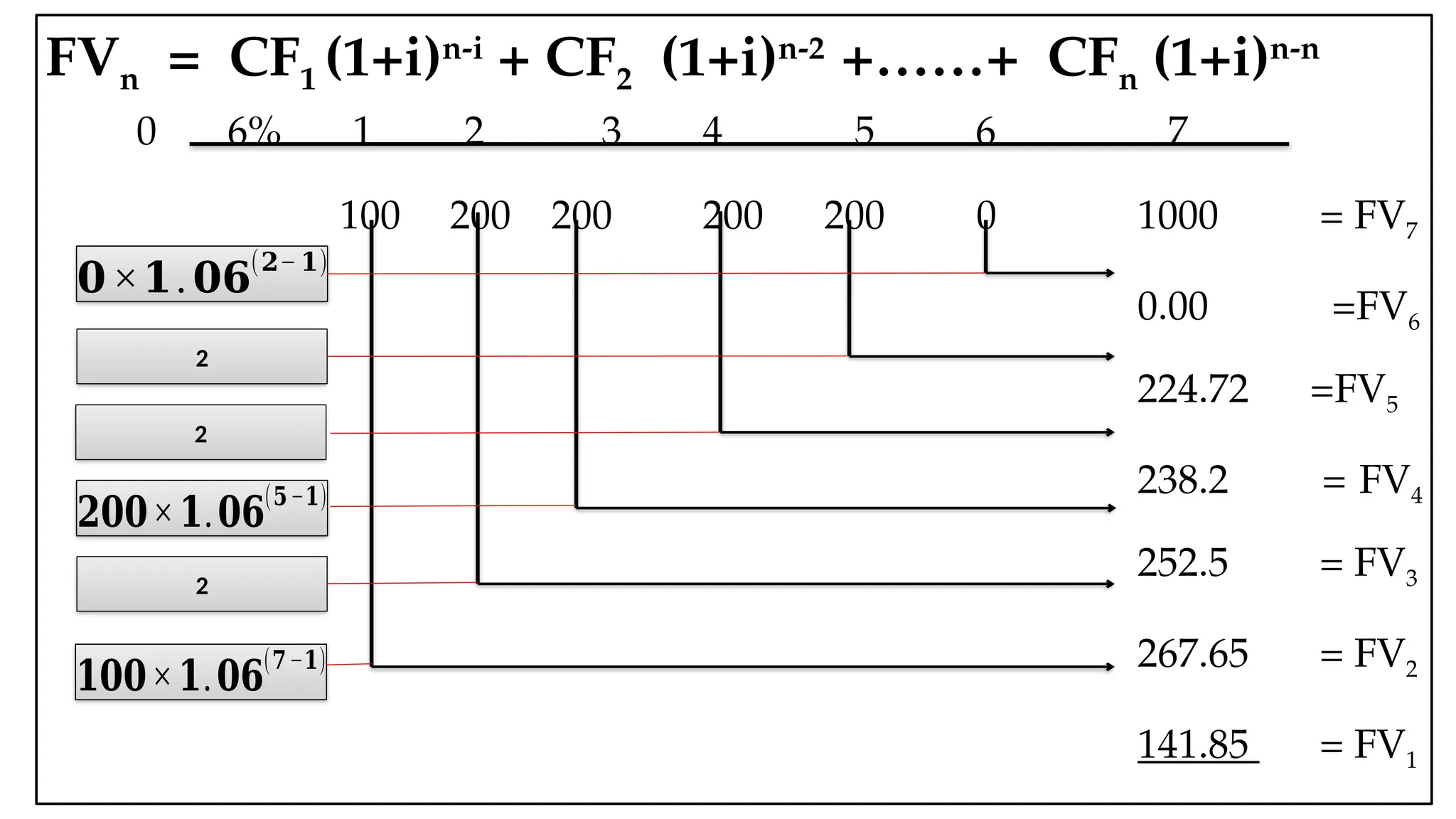

•Future value of unequal or uneven cash flow stream:

• The future value of unequal cash flows, or payments, or

receipts, sometimes called the terminal values) is found by

compounding each individual payment to the end of the

payment period, or end of cash flow stream.

• Then the individual compounded values (future values) are

added, to obtain the overall compounded value of the entire

cash flows in the stream.

• The following general compounding formula can be used to

determine both the individual compounded values and the

compounded, or future value of the entire cash flow stream.

05:43 AM 35

Semi-annualand Other Compounding Periods

• Suppose, that you placed 100 Birr into the bank account that

pays a 6 percent interest rate but the interest rate is

compounded each six months. This is commonly known as

Semi-annual compounding.

• How much would you accumulate at the end of three years?

36.

05:43 AM 36

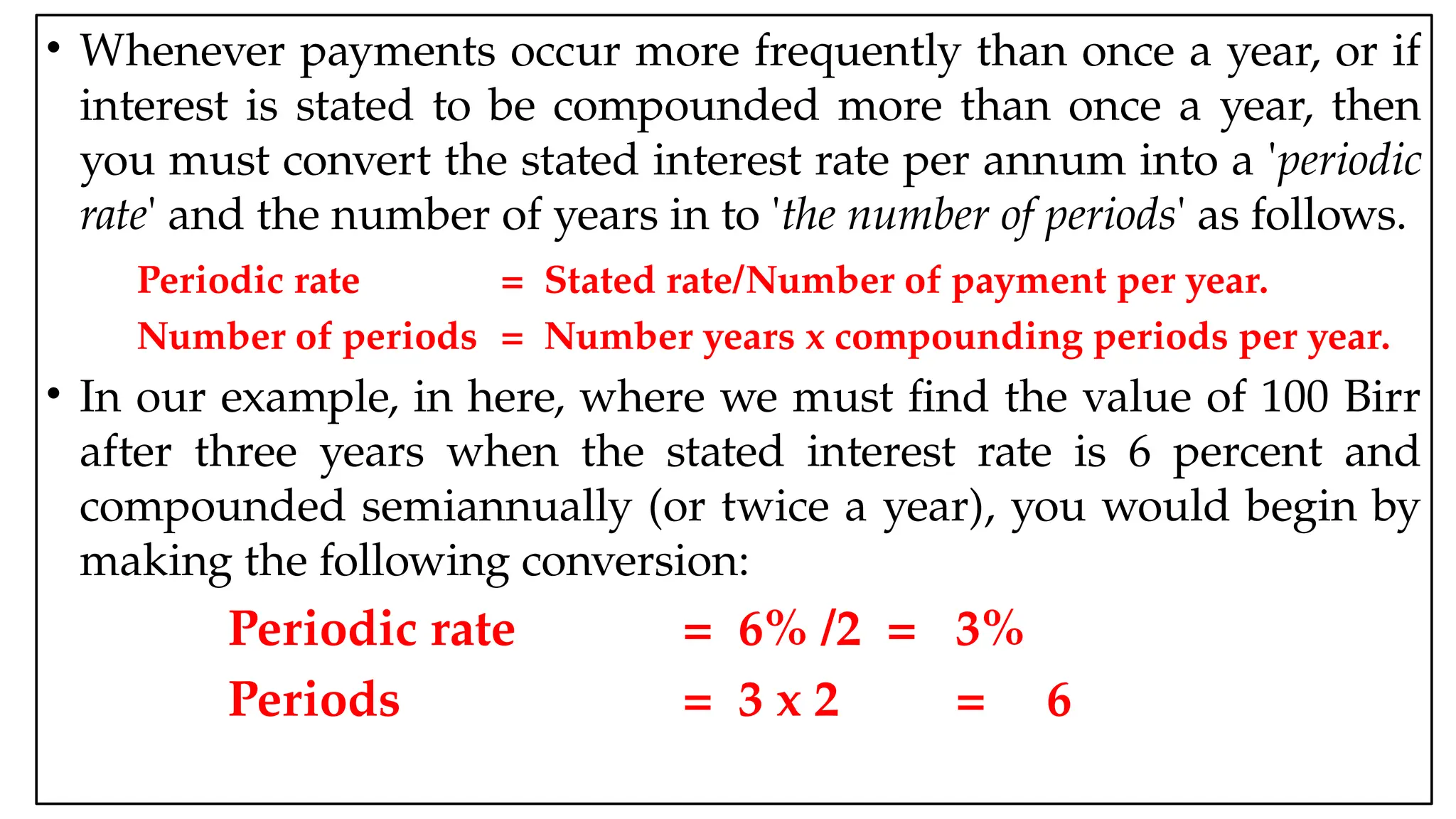

•Whenever payments occur more frequently than once a year, or if

interest is stated to be compounded more than once a year, then

you must convert the stated interest rate per annum into a 'periodic

rate' and the number of years in to 'the number of periods' as follows.

Periodic rate = Stated rate/Number of payment per year.

Number of periods = Number years x compounding periods per year.

• In our example, in here, where we must find the value of 100 Birr

after three years when the stated interest rate is 6 percent and

compounded semiannually (or twice a year), you would begin by

making the following conversion:

Periodic rate = 6% /2 = 3%

Periods = 3 x 2 = 6

37.

05:43 AM 37

•In this situation, the investment will earn 3% every 6 months for 6

periods.

• There is a significant difference between these two procedures.

• You should make the above conversion before you start solving the

problem, because compounding should generally be done using

number of periods and the periodic rate, not the number of years

and not the stated annual interest rate.

• The periodic rate and the number of periods, not yearly rate and

number of year 5, should be shown on the time-line and used in

the future value computation equation as well. Here is the time-

line.

38.

05:43 AM 38

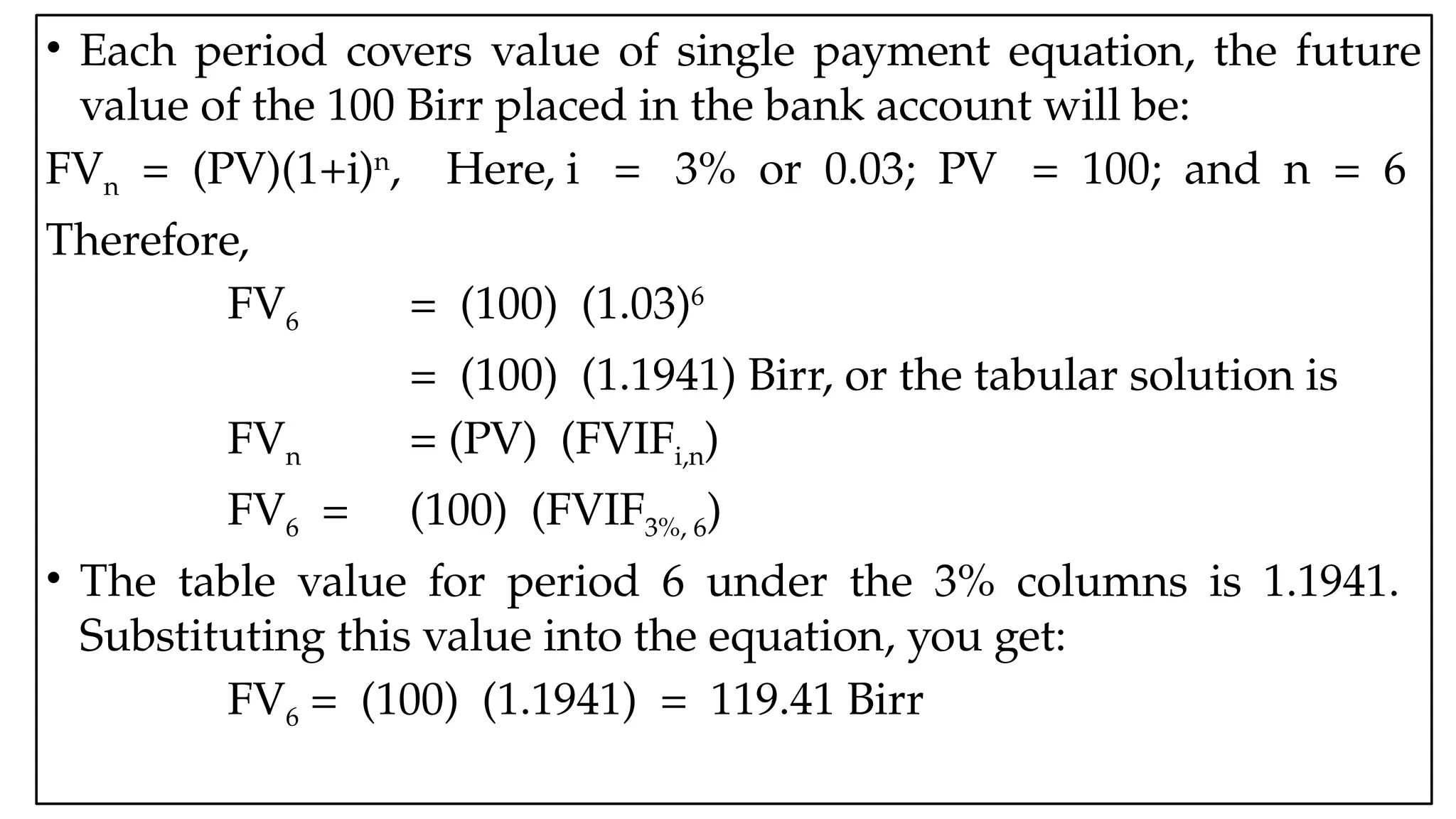

•Each period covers value of single payment equation, the future

value of the 100 Birr placed in the bank account will be:

FVn = (PV)(1+i)n

, Here, i = 3% or 0.03; PV = 100; and n = 6

Therefore,

FV6 = (100) (1.03)6

= (100) (1.1941) Birr, or the tabular solution is

FVn = (PV) (FVIFi,n)

FV6 = (100) (FVIF3%, 6)

• The table value for period 6 under the 3% columns is 1.1941.

Substituting this value into the equation, you get:

FV6 = (100) (1.1941) = 119.41 Birr

![05:43 AM 34

FVn = CF1 (1+i)n-i

+ CF2 (1+i)n-2

+……+ CFn (1+i)n-n

0 6% 1 2 3 4 5 6 7

100 200 200 200 200 0 1000 = FV7

0.00 =FV6

874.92

983.06 = FV2,3,4,5

141.85 = FV1

FVT = 2,124.92

𝟏𝟎𝟎×𝟏.𝟎𝟔

(𝟕−𝟏)

𝐹𝑉𝐴=200[(1+0.06)4

−1¿¿¿0.06]

𝟎×𝟏.𝟎𝟔𝟐−𝟏](https://image.slidesharecdn.com/fmichapter3tvm-251205054316-e92613ca/75/FM-I-Chapter-3-TVM-pptx-presentation-ppt-34-2048.jpg)

![Topic 3 1_[1] finance](https://cdn.slidesharecdn.com/ss_thumbnails/topic311-131107182625-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)