Downloaded 1,367 times

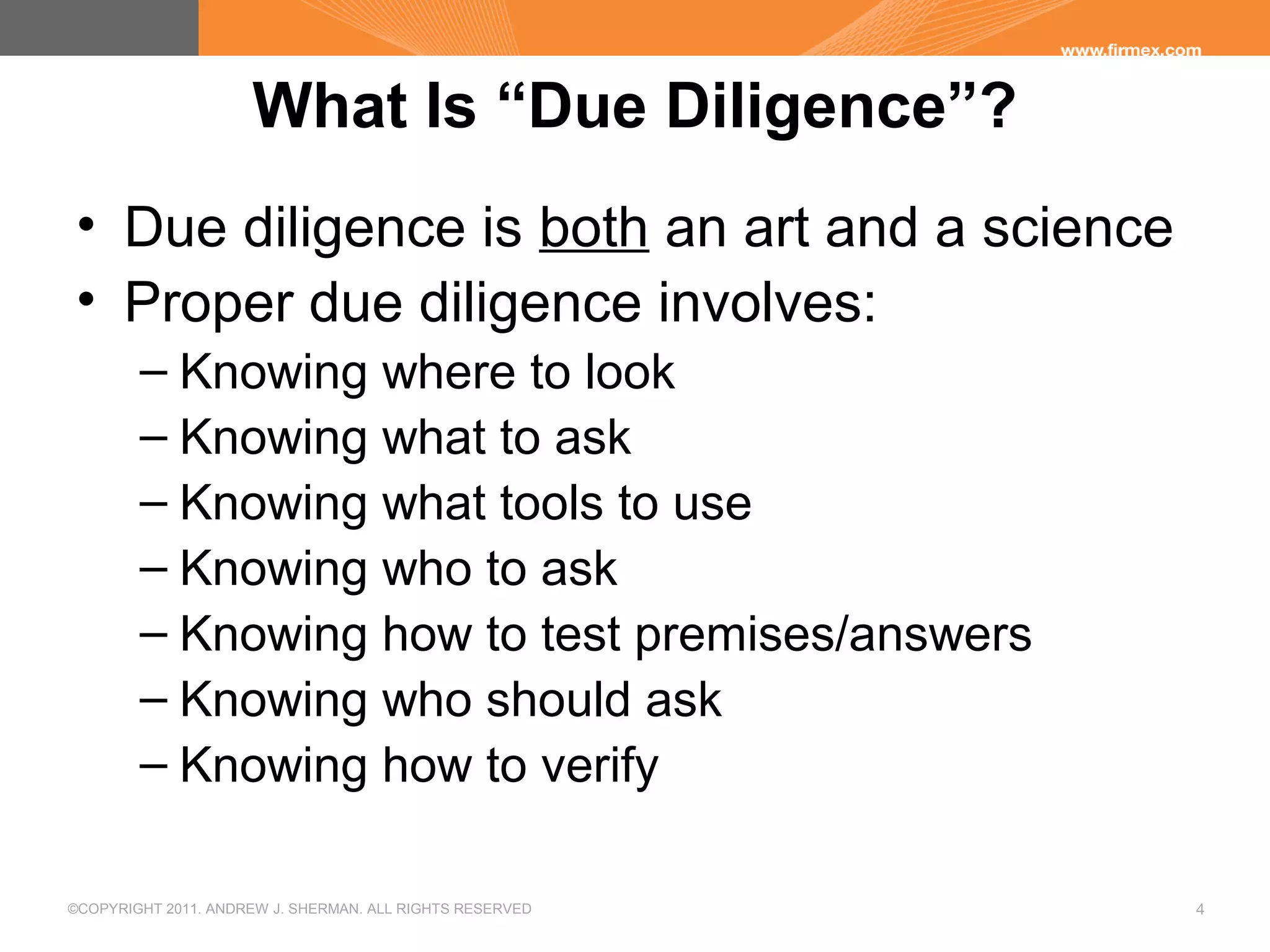

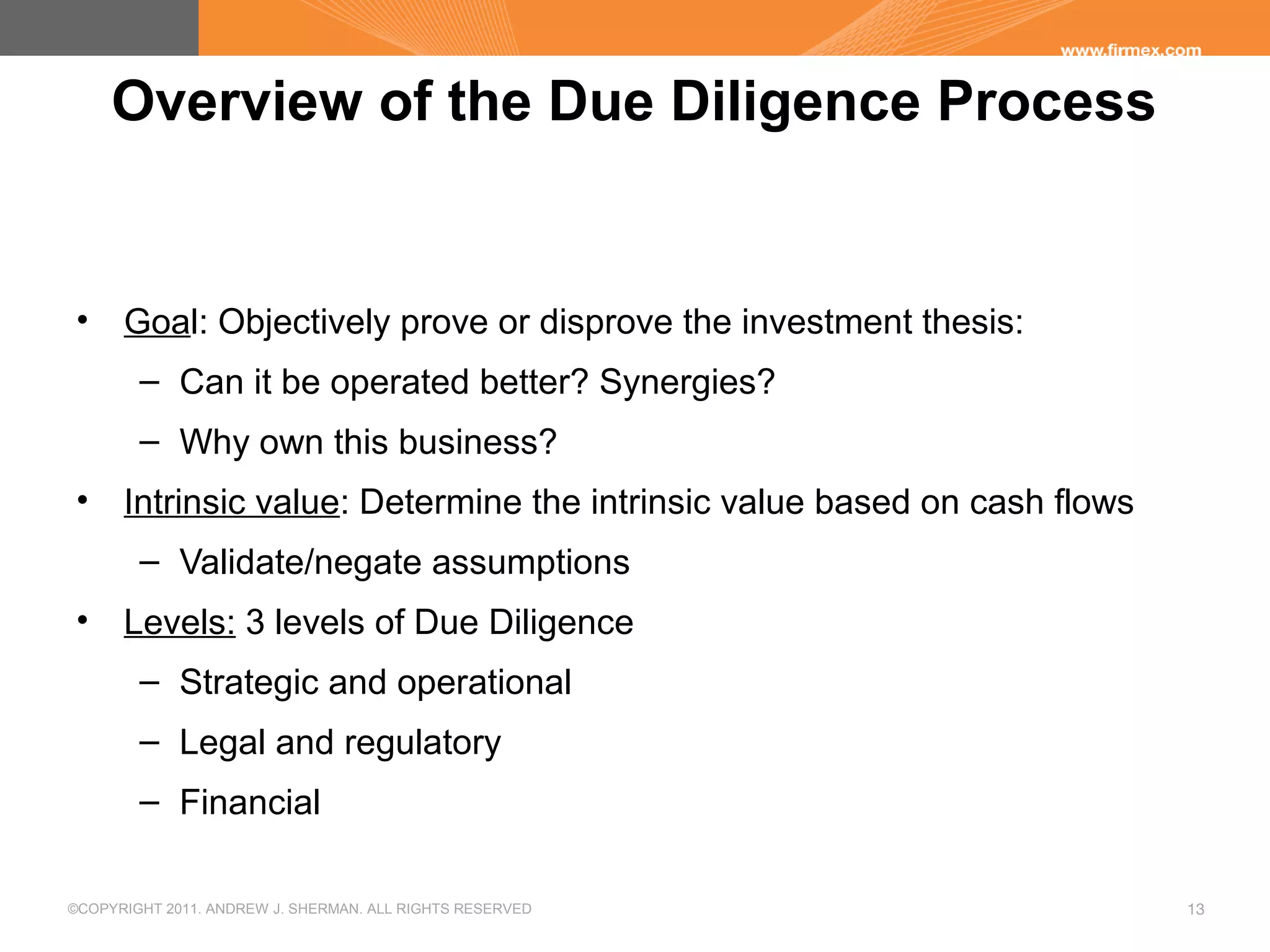

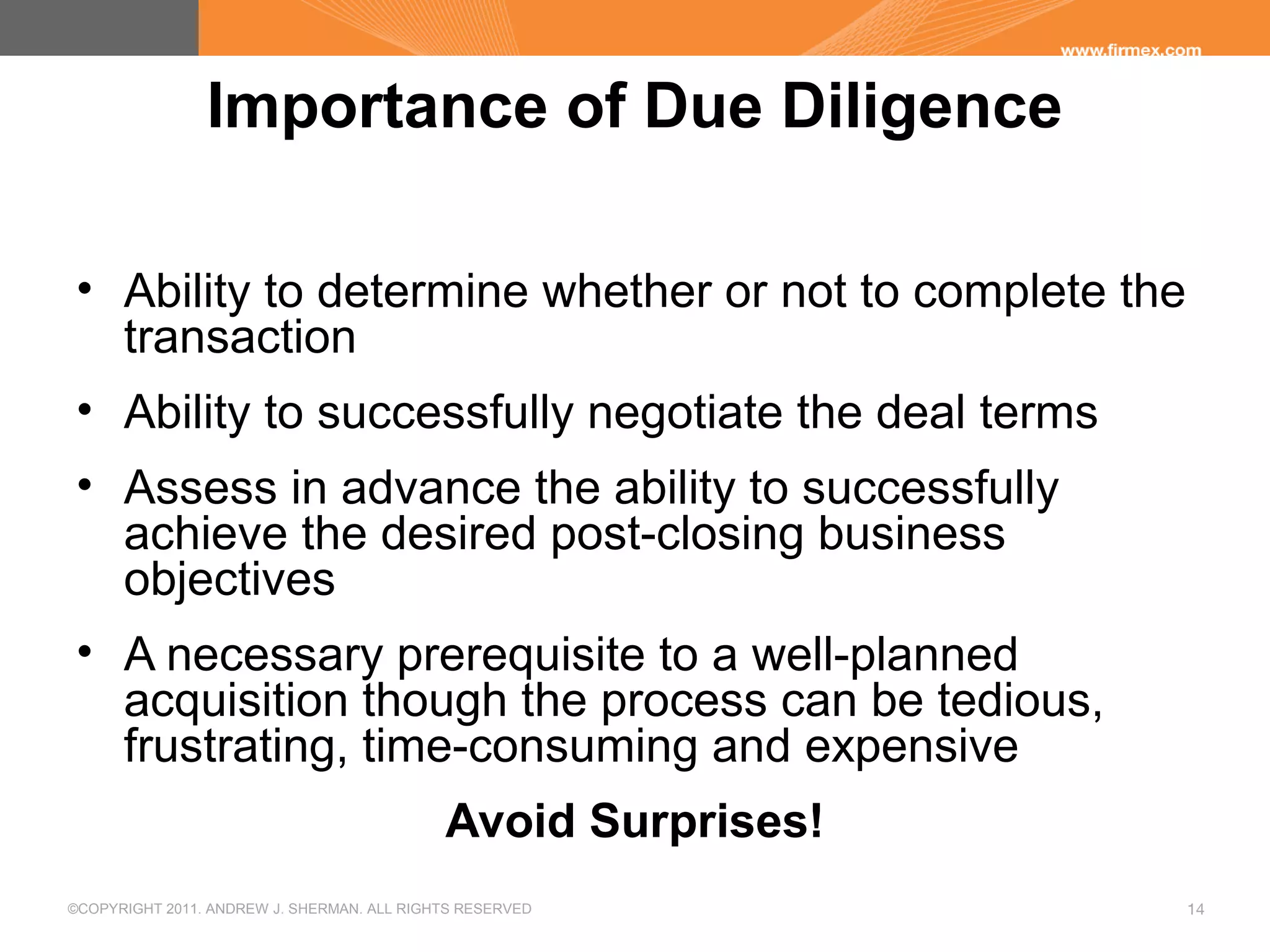

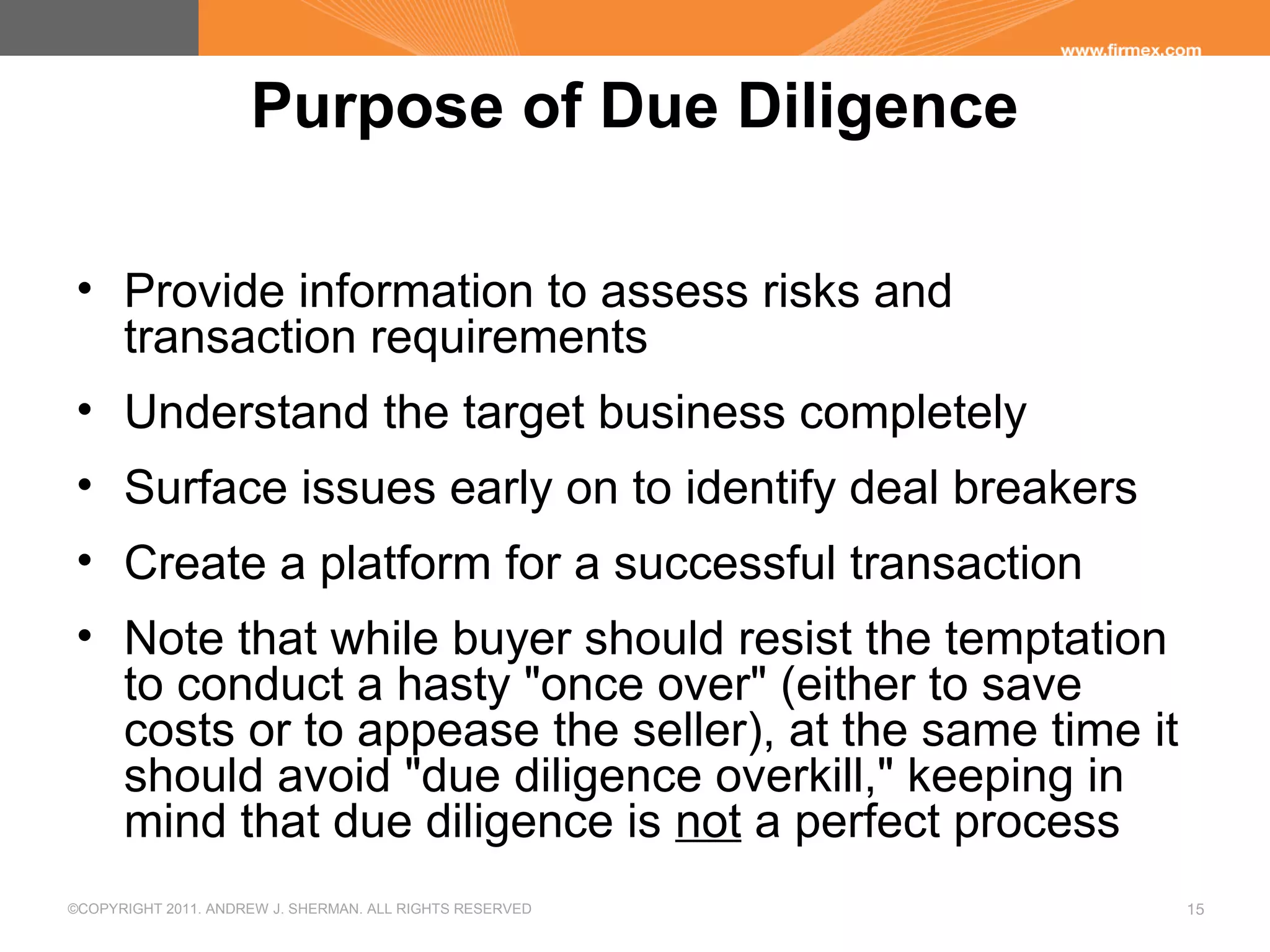

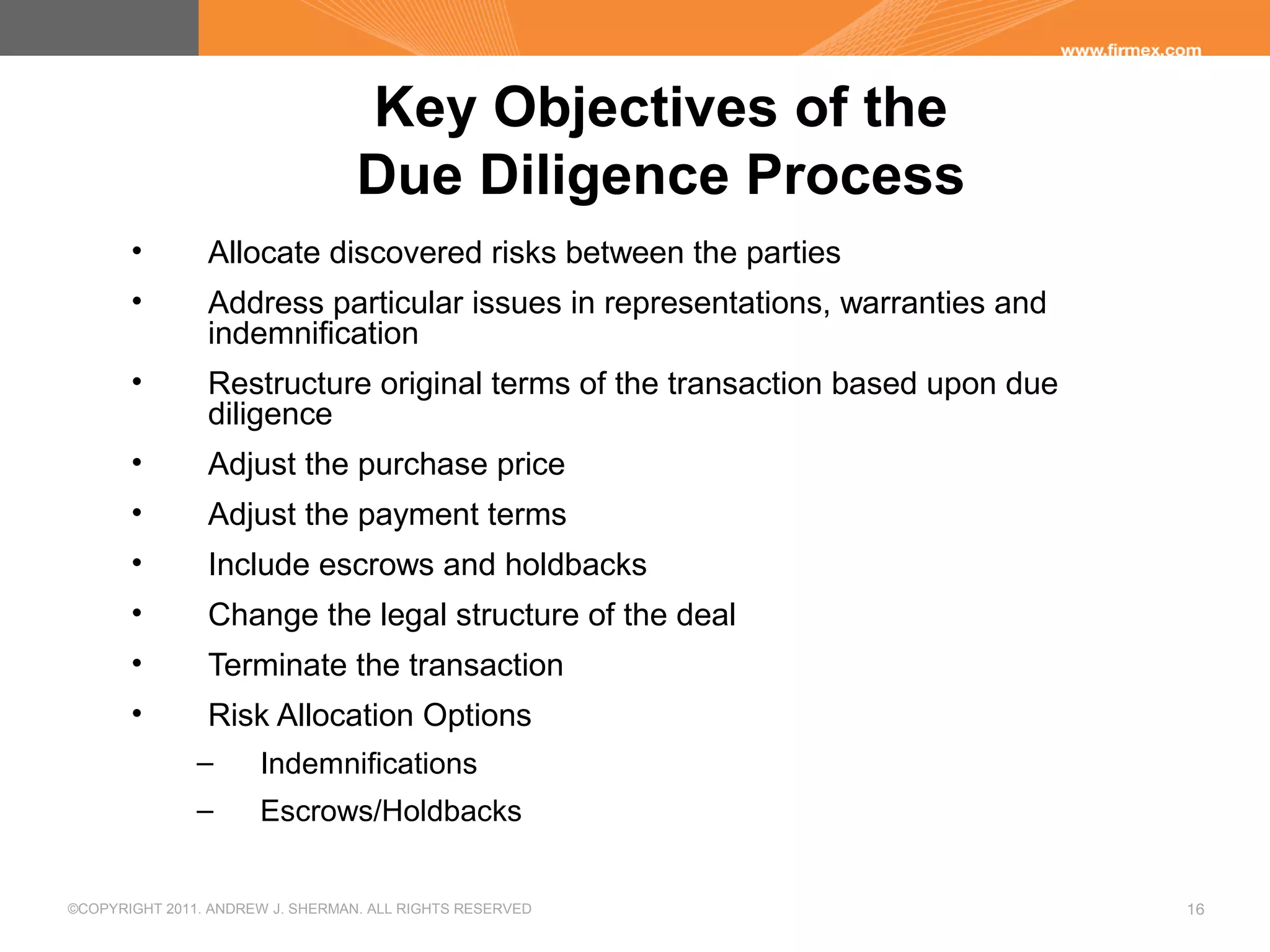

The document outlines best practices and common pitfalls in the due diligence process during M&A transactions, emphasizing its dual nature as both an art and a science. It highlights the importance of thorough preparation, effective communication, and the organization of due diligence teams, while also discussing the impact of external events and common mistakes made by buyers. Additionally, it emphasizes the role of virtual data rooms in facilitating efficient due diligence and the necessity of addressing potential legal issues and risks associated with transactions.

![[Gordon bing] due_diligence_planning,_questions,_(bookos.org)](https://cdn.slidesharecdn.com/ss_thumbnails/gordonbingduediligenceplanningquestionsbookos-131017040427-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)