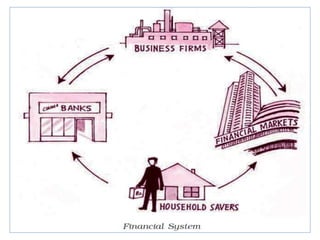

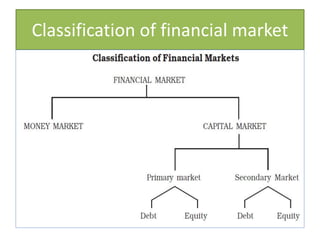

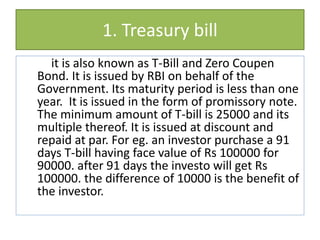

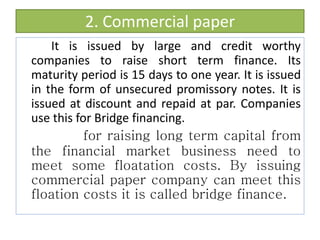

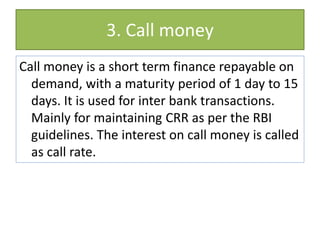

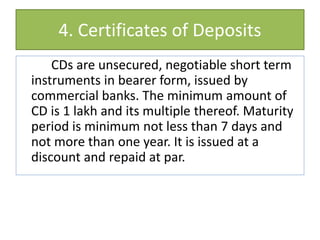

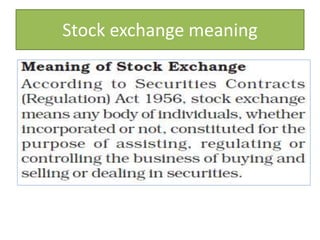

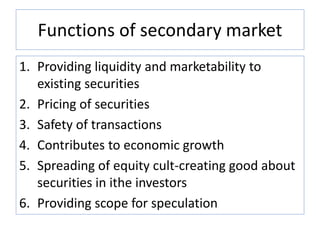

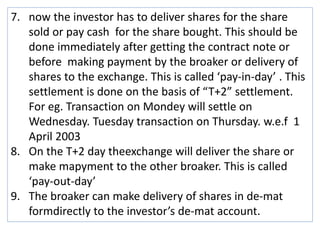

The document provides an overview of business finance and financial markets. It discusses that businesses need finance for fixed assets and working capital. Financial markets help mobilize savings from households and channel them to businesses through financial intermediation. There are two major mechanisms for this - banks and financial markets. Financial markets deal in the creation and exchange of financial assets in both the primary market (new issues) and secondary market (existing securities). Money markets deal in short-term funds of less than 1 year, while capital markets deal in long and medium-term funds. The key stock exchanges in India are the National Stock Exchange and Bombay Stock Exchange.