This document discusses principles of working capital management. It defines working capital as current assets used in operations, including cash, accounts receivable, inventory, and other current assets. Net working capital is current assets minus current liabilities. The document also discusses the cash conversion cycle, which is the time between a firm paying for supplies and collecting payment from customers, less any period where customer payments can be delayed. Efficient working capital management is important for business liquidity and profitability.

![RVU-Woliso

Financial Management II

Chapter 2 -5

30

Upper limit = lower limit + 3[

0.75( )( )

3

]

EXAMPLE. KK co. has experienced a stochastic demand for its product, which results in

fluctuating cash balances randomly. The following information supplied:

Fixed cost of a securities transaction $200

Variance of daily net cash flows $20,000

Daily interest rate on securities(opportunity cost ) 0.01%

Lower limit $10,000

The optimal cash balance (return point), and the upper limit of cash neededis determined as

follows:

= $10,000 +

0.75(200)(20,000)

0.0001

3

= 13,107

Upper limit = $10,000 + 3($3,107) = $19,321

What we have just determined using the Miller-Orr model is thatthe cash balance is allowed to

fluctuate between $13,107 and $19,321.If the cash balance exceeds $19,321, we invest the

difference betweenthe cash balance and the return point, restoring the cash balance to thereturn

point. If the cash balance is below the lower limit, marketablesecurities are sold to bring the cash

balance to the return point. Eachtime the cash balance is outside either the lower or the upper

limit, webounce back to the return point.

3.5 Investing Idle Cash

If a firm has a temporary cash surplus, it can invest in short-term securities. The market for

short-term financial assets is called themoney market. The maturity of short-term financial assets

that trade in the money marketis one year or less.](https://image.slidesharecdn.com/financialmanagementii-chapter2-5-231022071853-336e99ce/85/Financial-Management-II-Chapter-2-5-pdf-30-320.jpg)

![RVU-Woliso

Financial Management II

Chapter 2 -5

46

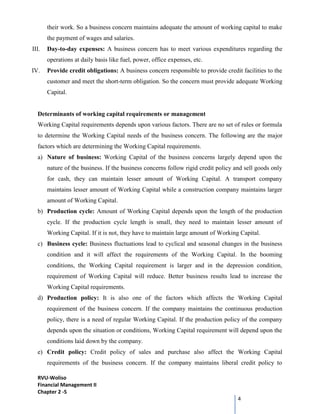

If the required return, R, is 2 percent per month, should Company make the switch?

Currently, XX has monthly sales of P xQ = $4,900. Variable costs each monthare v xQ =$2,000,

so the monthly cash flow from this activity is:

Cash flow with old policy = (P -v)Q

= ($49 - 20) x100=$2,900

If XX does switch to net 30 days on sales, then the quantity sold will rise to Q’=110. Monthly

revenues will increase to P xQ’, and costs will be v xQ’.

The monthlycash flow under the new policy will thus be:

Cash flow with new policy = (P -v) Q’

=($49 -20) x110 =$3,190

The relevant incremental cash flow is the differencebetween the new and old cash flows:

Incremental cash inflow = (P - v)(Q’- Q)

= ($49 - 20) (110 - 100)= $290

This means the benefit each month of changing policies is equal to the gross profit perunit sold,

P -v = $29, multiplied by the increase in sales, Q’-Q = 10.

The presentvalue of the future incremental cash flows is thus:

PV = [(P -v)(Q’ -Q)]/R

For XX, the present value of future incremental cash flow:

PV = ($29 X 10)/.02 = $14,500

Now we know the benefit of switching, what’s the cost? There are two componentsto consider.

First, because the quantity sold will rise from Q to Q’, the firm will have to produceQ’-Q more

units at a cost of v(Q’-Q) = $20 x (110 - 100) = $200.

Second,the sales that would have been collected this month under the current policy (P xQ =

$4,900) will not be collected. Under the new policy, the sales made this month won’t becollected

until 30 days later. The cost of the switch is the sum of these two components:

Cost of switching = PQ + v(Q’ - Q)

For XX, this cost would be $4,900 +200 = $5,100.

Thus, the NPV of the switch is:

NPV of switching = -[PQ + v(Q’ -Q)] + [(P -v)(Q’ -Q)]/R

For XX, the cost of switching is $5,100. As we saw earlier, the benefit is $290 permonth,

forever. At 2 percent per month, the NPV is:

NPV=-$5,100 + 290/.02](https://image.slidesharecdn.com/financialmanagementii-chapter2-5-231022071853-336e99ce/85/Financial-Management-II-Chapter-2-5-pdf-46-320.jpg)

![RVU-Woliso

Financial Management II

Chapter 2 -5

47

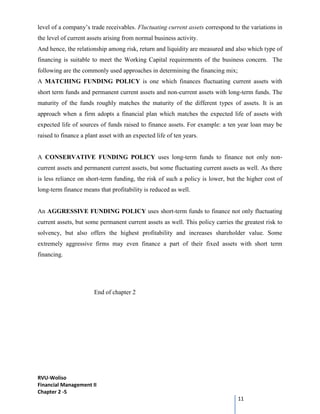

= - $5,100 +14,500 =$9,400

Therefore, the switch is very profitable.

A Break-Even ApplicationBased on our discussion thus far, the key variable for XX is

Q’ -Q, the increase in unit sales. The projected increase of 10 units is only anestimate, so there is

some forecasting risk. Under the circumstances, it’s natural to wonderwhat increase in unit sales

is necessary to break even.

Earlier, the NPV of the switch was defined as:

NPV= -[PQ +v(Q’ -Q)] + [(P -v)(Q’ -Q)]/R

We can calculate the break-even point explicitly by setting the NPV equal to zero andsolving for

(Q’ -Q):

NPV = 0 =-[PQ + v(Q’ -Q)] + [(P -v)(Q’ -Q)]/R

Q’-Q = PQ/[(P -v)/R -v]

For XX, the break-even sales increase is thus:

Q’ -Q =$4,900/(29/.02 -20)= 3.43 units

This tells us that the switch is a good idea as long as the Company is confident that it can sellat

least 3.43 more units per month.

OPTIMAL CREDIT POLICY

Optimal credit policy:is a policy that maximizes the firm’s value. In principle, the optimal

amount of credit is determined by the point at which the incremental cash flows from increased

sales are exactly equal to the incremental costs of carrying the increase in investment in accounts

receivable. Hence the value of the firm is maximized when; the incremental or marginal rate of

return of an investment is equal to the incremental or marginal cost of funds used to finance the

investment.

The incremental rate of return can be calculated as incremental operating profit divided by the

incremental investment in receivable. The incremental cost of funds is the rate of return required

by suppliers of funds given the risk of investment in accounts receivables.](https://image.slidesharecdn.com/financialmanagementii-chapter2-5-231022071853-336e99ce/85/Financial-Management-II-Chapter-2-5-pdf-47-320.jpg)