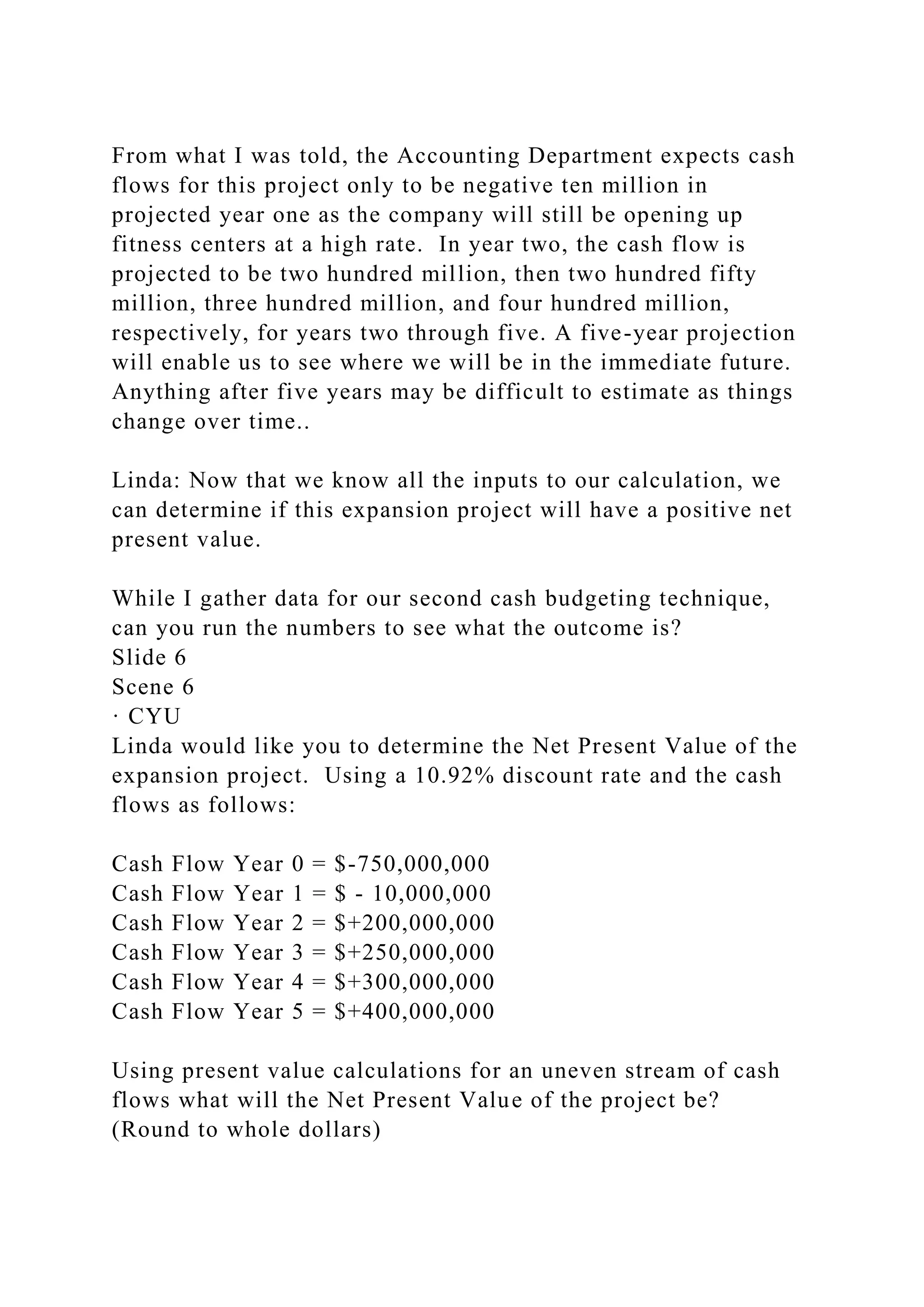

The document describes a scenario involving a capital budgeting analysis for an expansion project at a company, emphasizing key capital budgeting techniques like net present value (NPV), internal rate of return (IRR), modified internal rate of return (MIRR), and payback period. Linda and her intern are tasked with evaluating the project's viability based on projected cash flows and associated costs, concluding that the project should proceed due to a positive NPV. Relevant cash flows are emphasized, highlighting the importance of focusing only on cash transactions related to the project.