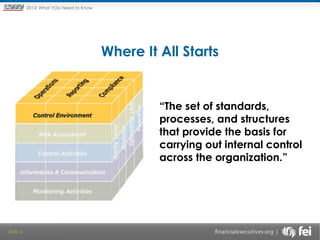

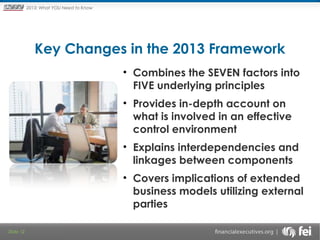

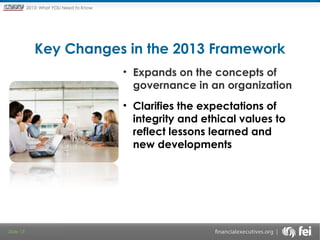

The document outlines a webinar discussing the key principles and changes in the 2013 control environment framework, emphasizing its importance in internal control systems. It highlights the framework's shift from seven factors to five underlying principles, aiming to improve organizational governance and risk management. The control environment is portrayed as foundational to ensuring effective internal controls, with significant implications for compliance, particularly regarding Sarbanes-Oxley applications.