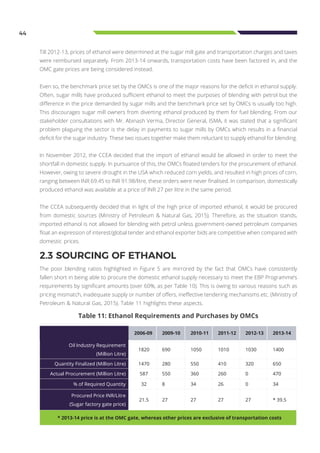

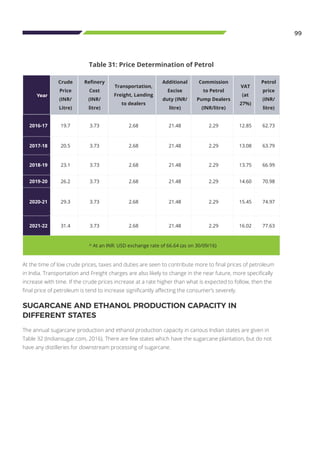

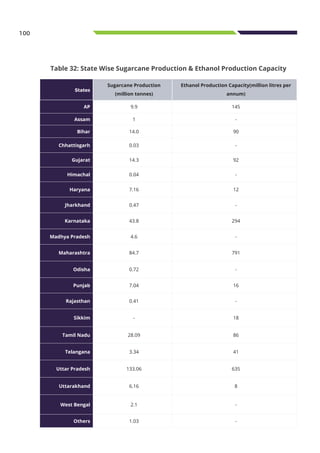

This document provides an overview of fuel blending in India, including learnings and a way forward. It discusses India's Ethanol Blended Petrol (EBP) Program, which aims to promote the usage of biofuels. The document covers the background and history of ethanol blending in India. It highlights challenges to the EBP program, such as varied taxes on inter-state ethanol movement and procedural difficulties. The potential economic and environmental advantages of adopting ethanol as a biofuel in India are explored. Global best practices from the US, Philippines, and Brazil are analyzed. The document concludes by setting out policy recommendations to address roadblocks and help India transition to a broader biofuels economy.