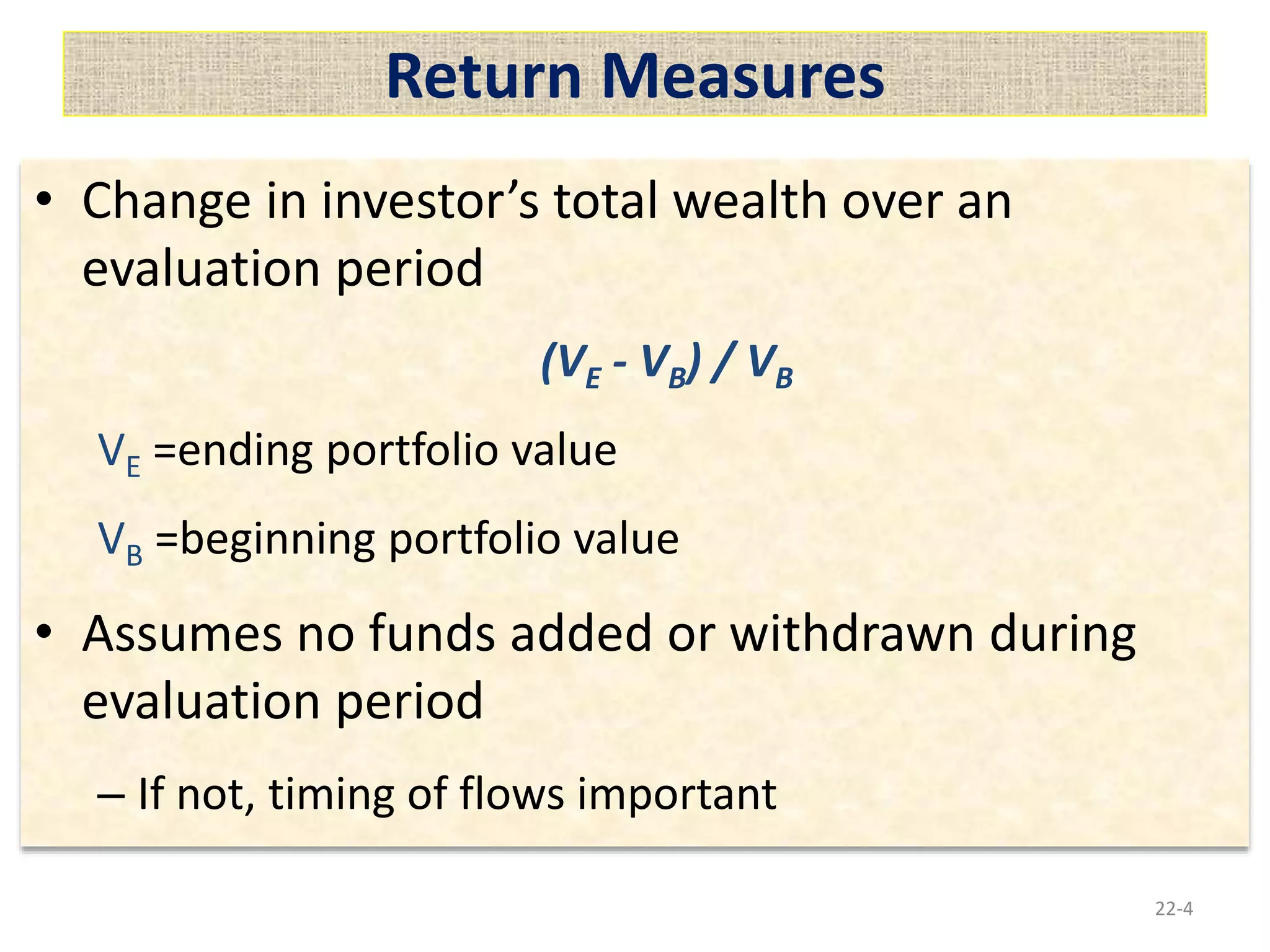

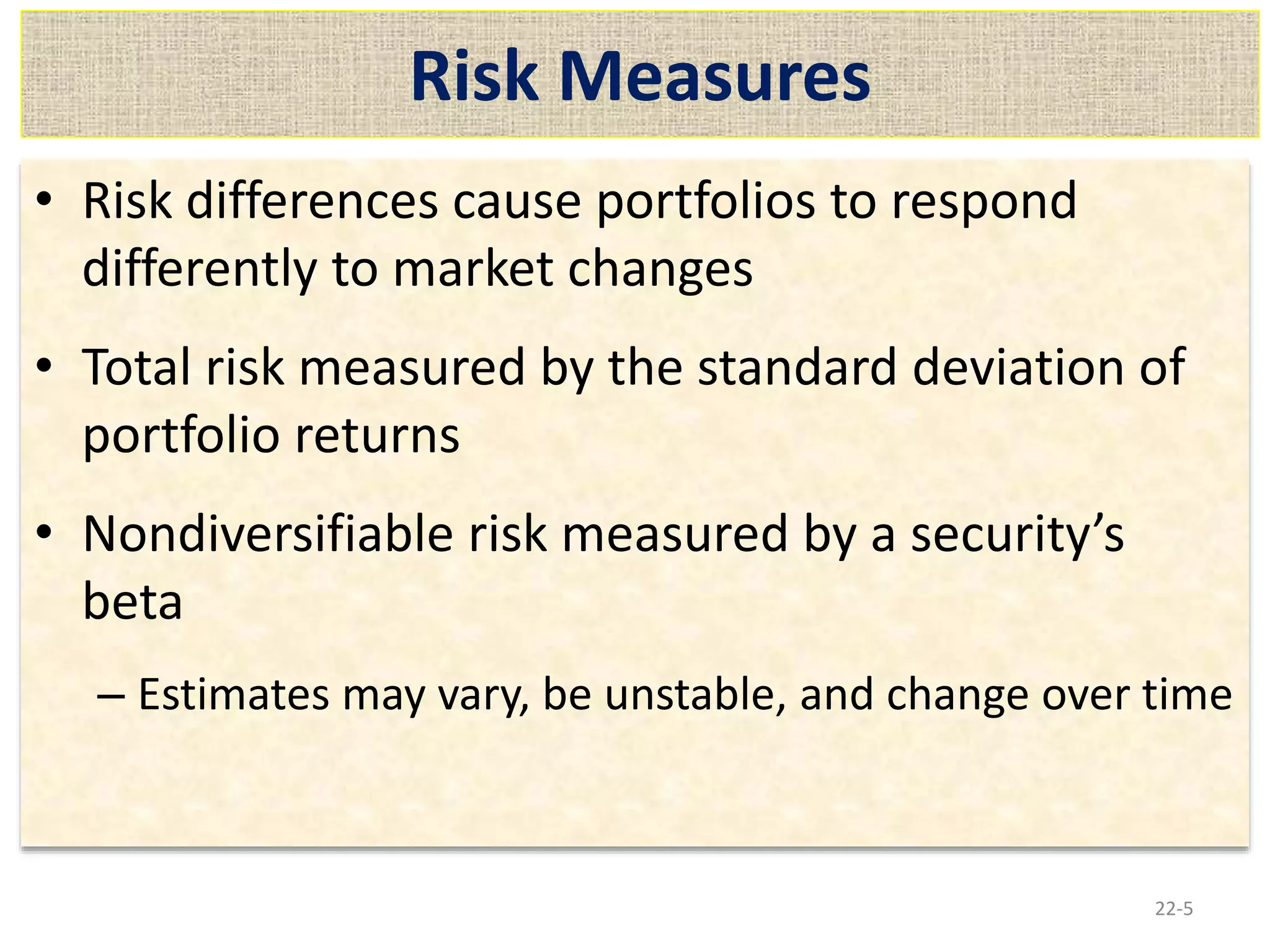

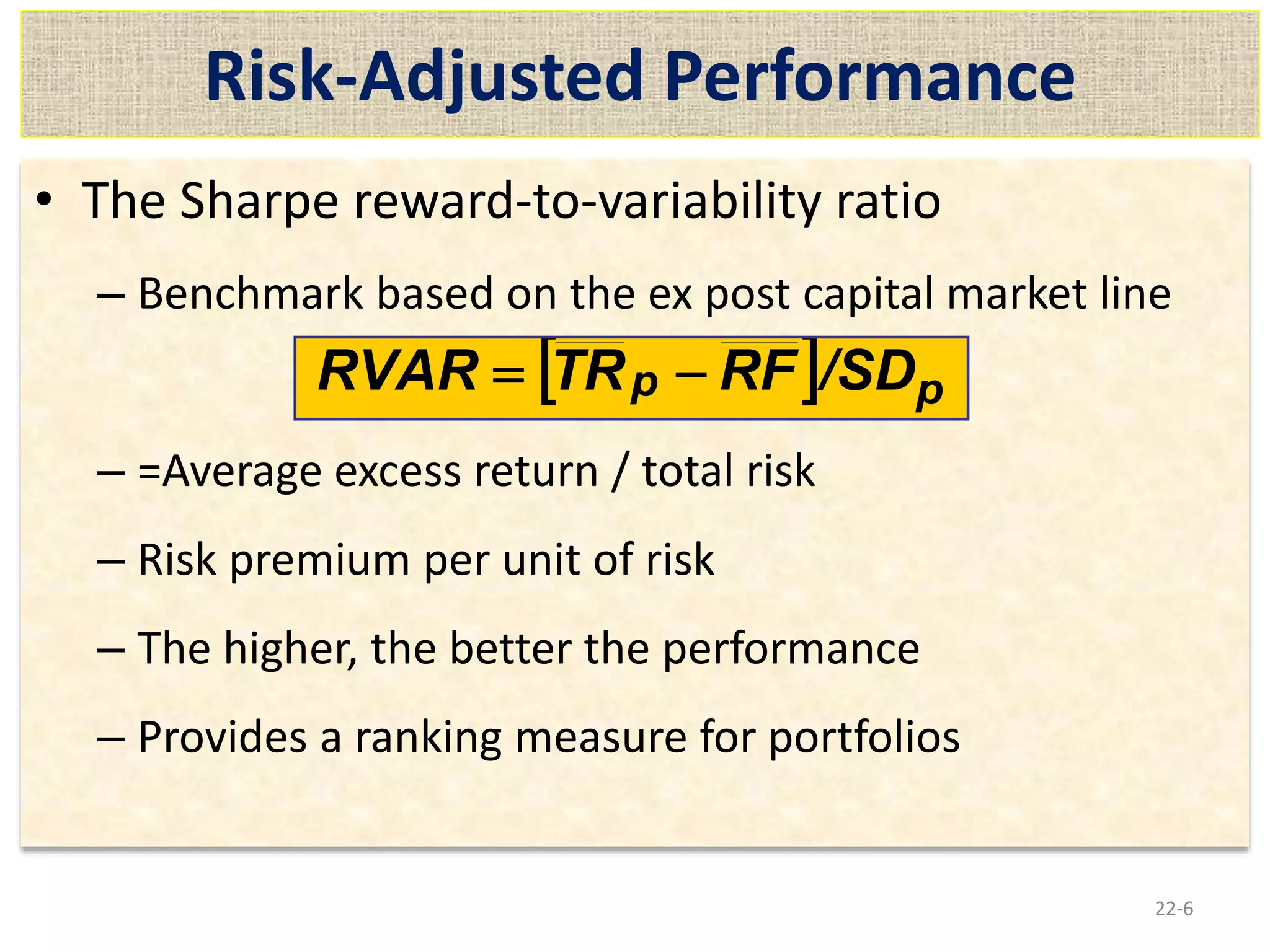

This document discusses various methods for evaluating investment performance, including return, risk, and risk-adjusted performance measures. It describes calculating total return as the change in wealth over a period, and measuring total risk as the standard deviation of returns. Risk-adjusted measures discussed include the Sharpe and Treynor ratios, with the Sharpe ratio using total risk and the Treynor using only systematic market risk. The document also covers measuring diversification through correlation to the market and Jensen's Alpha for determining manager performance beyond market returns.

![Measuring Diversification

• How correlated are portfolio’s returns to

market portfolio?

– R2 from estimation of

Rpt - RFt =ap +bp [RMt - RFt] +ept

– R2 is the coefficient of determination

– Excess return form of characteristic line

– The lower the R2, the greater the diversifiable risk

and the less diversified

22-9](https://image.slidesharecdn.com/evaluationofinvestmentperformance-230215180747-22c8cc9c/75/Evaluation-of-Investment-Performance-ppt-9-2048.jpg)

![Jensen’s Alpha

• The estimated a coefficient in

Rpt - RFt =ap +bp [RMt - RFt] +ept

is a means to identify superior or inferior portfolio performance

– CAPM implies a is zero

– Measures contribution of portfolio manager beyond return

attributable to risk

• If a >0 (<0,=0), performance superior (inferior, equals) to

market, risk-adjusted

22-10](https://image.slidesharecdn.com/evaluationofinvestmentperformance-230215180747-22c8cc9c/75/Evaluation-of-Investment-Performance-ppt-10-2048.jpg)

![Topic 4[1] finance](https://cdn.slidesharecdn.com/ss_thumbnails/topic41-131107182635-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)