Introduction

The performance evaluationof a portfolio is nothing

but checking out whether a target level of activity has been

achieved or not or how well the portfolio has performed in

comparison to other portfolios or market index.

It is an assessment of the functioning of the portfolio,

its risk and return. In fact, the performance evaluation of

portfolio is nothing but evaluating and examining the overall

performance of the portfolio managers/ asset management

companies

3.

Introduction

following reasons:

i. Ithelps the investor to examine how well the manager has

achieved the targeted rate of return.

ii. It enables the investor to examine how well the manager

has achieved the desired targets in comparison to other

portfolios.

iii. It helps to evaluate the performance of investment

decisions in relative terms i.e. per unit of risk.

4.

Introduction

Portfolio performance evaluationcan be viewed as a

feedback and control mechanism that can make the

investment management process more effective. Portfolio

performance is evaluated by measuring and comparing

portfolio return and associated risk.

There are three major methods of assessing performance

1. Return per unit of risk

2. Differential return.

3. Components of performance

5.

Introduction

Key Aspects ofPortfolio Evaluation

1. Performance Measurement

Return Assessment: Calculate the actual returns of the portfolio over

a specific period. This includes both absolute returns and relative

returns compared to a benchmark or index.

Benchmark Comparison: Compare the portfolio's performance

against a relevant benchmark to determine how well it is doing in the

context of the broader market or specific asset class.

6.

Introduction

Key Aspects ofPortfolio Evaluation

2. Risk Assessment

Risk Analysis: Measure the risk taken to achieve the returns.

Common metrics include volatility, beta (market risk), and alpha

(excess return over a benchmark).

Risk-Adjusted Returns: Evaluate returns in the context of the risk

taken. Ratios like the Sharpe Ratio and Sortino Ratio are used to

assess how much return the investment is generating per unit of risk.

7.

Introduction

Key Aspects ofPortfolio Evaluationa

3. Cost Analysis

Expenses and Fees: Analyze all costs associated with

managing the portfolio, including fund management fees,

transaction fees, and any other expenses. High costs can

significantly erode net returns.

8.

Introduction

4. Portfolio Alignment

StrategicAlignment: Check if the

portfolio still aligns with the

initial investment strategy and

objectives.

Life events, economic changes, or shifts in financial goals

may require adjustments to the portfolio strategy.

9.

Measuring Portfolio Return

Therate of return of a portfolio is measured as the sum of

cash received (dividend) and the change in the portfolio

market value (capital gain/loss) divided by the market value

of the portfolio at the beginning of the period.

10.

Risk-adjusted Returns

Theperformance of a fund should be assessed in terms

of return per unit of risk. The funds that provide the

highest return per unit of risk would be considered the

best performer.

For well-diversified portfolios in all asset categories, the

standard deviation is the relevant measure of risk.

When evaluating individual stocks and not so well

diversified portfolios, the relevant measure of risk is the

systematic or market risk, which can be assessed using

the beta co-efficient (b). Beta signifies the relationship

between covariance (stock, market) and variance of

11.

Sharpe’s Ratio

Sharpe’smeasure is called the “Reward-to-Variability”

Ratio. The returns from a portfolio are initially adjusted

for risk-free returns.

These excess returns attributable as reward for investing

A ratio developed by Nobel laureate

William F. Sharpe to measure risk-adjusted

performance.

It is calculated by subtracting the risk-free

rate – such as that of the 10 year US

Treasury bond – from the rate of return for

a portfolio and dividing the result by the

standard deviation of the portfolio returns.

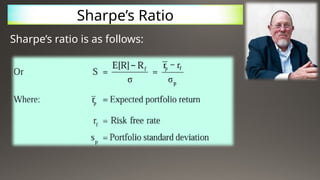

Sharpe’s Ratio

Sharpe’s ratiois as follows:

The Sharpe ratio tells us whether the returns of a portfolio are due to

smart investment decisions or a result of excess risk.

This measurement is very useful because although one portfolio or fund

can reap higher returns than its peers, it is only a good investment if

those higher returns do not come with too much additional risk.

The greater a portfolio’s Sharpe ratio, the better its risk-adjusted

performance will be.

A variation of the Sharpe ratio is the Sortino ratio, which removes the

effects of upward price movements on standard deviation to instead

measure only the return against downward price volatility.

14.

Treynor Portfolio PerformanceMeasure

This measure was developed by Jack Treynor in

1965. Treynor (helped developed CAPM) argues

that, using the characteristic line, one can

determine the relationship between a security and

the market. Deviations from the characteristic line

(unique returns) should cancel out if you have a

fully diversified portfolio.

Treynor’s Composite Performance Measure: He was interested in a

performance measure that would apply to all investors regardless of

their risk preferences. He argued that investors would prefer a CML

with a higher slope (as it would place them on a higher utility curve).

15.

Differential Return

Differentialreturn is a risk-adjusted measure of a

portfolio's performance compared to a benchmark,

representing the difference between the portfolio's risk-

adjusted return and the benchmark's return.

It goes beyond a simple return difference by factoring in

risk, providing a more accurate assessment of whether a

manager's performance was due to skill or simply taking on

more or less risk

16.

Differential Return

First, itis important to recognize that differential return is a rate of

return. As you might guess from its name, it is an excess return (i.e., a

difference in returns). More specifically, it is a risk-adjusted excess

return.

In this first post on this measure, I compare differential return to

subtraction alpha. Subtraction alpha is simply the portfolio return

minus the benchmark return:

17.

Differential Return

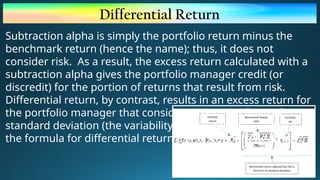

Subtraction alphais simply the portfolio return minus the

benchmark return (hence the name); thus, it does not

consider risk. As a result, the excess return calculated with a

subtraction alpha gives the portfolio manager credit (or

discredit) for the portion of returns that result from risk.

Differential return, by contrast, results in an excess return for

the portfolio manager that considers risk in the form of

standard deviation (the variability of past returns). Here is

the formula for differential return using standard deviation: