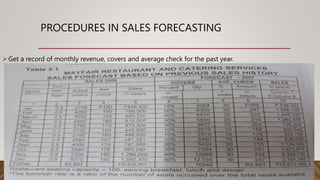

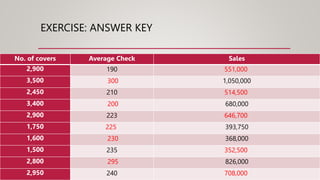

The document discusses establishing sales targets and forecasting for food and beverage businesses. It explains that sales forecasts are important as they provide specific, measurable targets for revenue, covers, and average check. This allows management to set direction, determine if the business can cover costs and make a profit, and inform budgeting and inventory decisions. The document outlines procedures for creating a sales forecast, which includes analyzing historical sales data and projecting increases in covers and average check based on assumptions. Forecasts are then calculated using a formula that multiplies projected covers by the average check. An example exercise applying this process is also included.