Egypt Economic Outlook

•

1 like•184 views

- The Egyptian economy has reached an alarming point with weak fundamentals across private consumption, investment, exports, and imports. - The new government has embarked on an expansionary fiscal and monetary policy including a stimulus package and interest rate cuts to boost growth. - The report forecasts GDP growth of 2.7% in the current fiscal year, below the government's 3.5% target. Private consumption is expected to grow 2.5% while government consumption grows 4.8%. Investment growth is forecasted at 2.3%. Exports are forecasted to decline 1.5% and imports 0.8%. - Structural issues like high unemployment and inflation continue to weigh on a full recovery in private consumption while

Recommended

Recommended

More Related Content

What's hot

What's hot (19)

Similar to Egypt Economic Outlook

Similar to Egypt Economic Outlook (20)

Egypt Economic Outlook

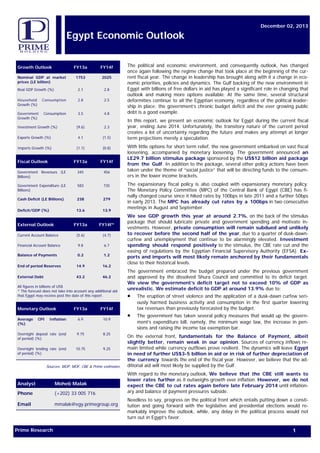

- 1. Prime Research 1 Egypt Economic Outlook December 02, 2013 The political and economic environment, and consequently outlook, has changed once again following the regime change that took place at the beginning of the cur- rent fiscal year. The change in leadership has brought along with it a change in eco- nomic priorities, policies and dynamics. The Gulf backing of the new environment in Egypt with billions of free dollars in aid has played a significant role in changing that outlook and making more options available. At the same time, several structural deformities continue to ail the Egyptian economy, regardless of the political leader- ship in place; the government’s chronic budget deficit and the ever growing public debt is a good example. In this report, we present an economic outlook for Egypt during the current fiscal year, ending June 2014. Unfortunately, the transitory nature of the current period creates a lot of uncertainty regarding the future and makes any attempt at longer term projections merely a speculation. With little options for short term relief, the new government embarked on vast fiscal loosening, accompanied by monetary loosening. The government announced an LE29.7 billion stimulus package sponsored by the US$12 billion aid package from the Gulf. In addition to the package, several other policy actions have been taken under the theme of “social justice” that will be directing funds to the consum- ers in the lower income brackets. The expansionary fiscal policy is also coupled with expansionary monetary policy. The Monetary Policy Committee (MPC) of the Central Bank of Egypt (CBE) has fi- nally changed course since it hiked rates by 100bps in late 2011 and a further 50bps in early 2013. The MPC has already cut rates by a 100bps in two consecutive meetings in August and September. We see GDP growth this year at around 2.7%, on the back of the stimulus package that should lubricate private and government spending and motivate in- vestments. However, private consumption will remain subdued and unlikely to recover before the second half of the year, due to a quarter of dusk-dawn- curfew and unemployment that continue to be alarmingly elevated. Investment spending should respond positively to the stimulus, the CBE rate cut and the easing of regulations by the Egyptian Financial Supervisory Authority (EFSA). Ex- ports and imports will most likely remain anchored by their fundamentals close to their historical levels. The government embraced the budget prepared under the previous government and approved by the dissolved Shura Council and committed to its deficit target. We view the government’s deficit target not to exceed 10% of GDP as unrealistic. We estimate deficit to GDP at around 13.9% due to: • The eruption of street violence and the application of a dusk-dawn curfew seri- ously harmed business activity and consumption in the first quarter lowering tax revenues than previously forecasted by the budget. • The government has taken several policy measures that would up the govern- ment’s expenditure bill, namely, the minimum wage law, the increase in pen- sions and raising the income tax exemption bar. On the external front, fundamentals for the Balance of Payment, albeit slightly better, remain weak in our opinion. Sources of currency inflows re- main limited while currency outflows prove resilient. The dynamics will leave Egypt in need of further US$3-5 billion in aid or in risk of further depreciation of the currency towards the end of the fiscal year. However, we believe that the ad- ditional aid will most likely be supplied by the Gulf. With regard to the monetary outlook, We believe that the CBE still wants to lower rates further as it outweighs growth over inflation. However, we do not expect the CBE to cut rates again before late February 2014 until inflation- ary and balance of payment pressures subside. Needless to say, progress on the political front which entails putting down a consti- tution and going forward with the legislative and presidential elections would re- markably improve the outlook, while, any delay in the political process would not turn out in Egypt’s favor. Analyst Moheb Malak Phone (+202) 33 005 716 Email mmalak@egy.primegroup.org FY14fFY13aGrowth Outlook 20251753Nominal GDP at market prices (LE billion) 2.82.1Real GDP Growth (%) 2.52.8Household Consumption Growth (%) 4.83.5Government Consumption Growth (%) 2.3(9.6)Investment Growth (%) (1.5)4.1Exports Growth (%) (0.8)(1.1)Imports Growth (%) FY14fFY13aFiscal Outlook 456345Government Revenues (LE Billions) 735583Government Expenditure (LE Billions) 279238Cash Deficit (LE Billions) 13.913.6Deficit/GDP (%) FY14f*FY13aExternal Outlook (4.7)(5.6)Current Account Balance 6.79.8Financial Account Balance 1.20.2Balance of Payments 16.214.9End of period Reserves All figures in billions of US$ * The forecast does not take into account any additional aid that Egypt may receive post the date of this report. FY14fFY13aMonetary Outlook 10.96.9Average CPI Inflation (%) 8.259.75Overnight deposit rate (end of period) (%) 9.2510.75Overnight lending rate (end of period) (%) 46.243.2External Debt Sources: MOP, MOF, CBE & Prime estimates

- 2. Prime Research 2 Egypt Economic Outlook December 02, 2013 Growth Outlook Weak Fundamentals After three years of political turbulence and sluggish growth the Egyptian economy has reached an alarming point. Fundamentals are weak across all expenditure items. Even the engine that has pushed growth for years fueled by a large population base, namely private con- sumption, has eventually slowed down burdened by stag- nant real incomes, staggering unemployment (which reached 13.4% in Q3 FY13), soaring inflation as well as street violence. Investment spending crippled since 2011 under the weight of heightened political risk, rocketing interest rates, looming currency depreciation and currency controls. Exports did not come to the rescue even with the cur- rency depreciation as many exporting industries either are capacity constrained or are energy intensive, amid an energy crisis in the country. Exports of services did not help either as tourism weakened further amid fragile se- curity conditions. On the other hand, imports proved resil- ient, as a lot of necessities and raw materials are im- ported. Expansionary Policy With little options for short term relief, the new govern- ment embarked on vast fiscal loosening, accompanied by monetary loosening. The government announced an LE29.7 billion stimulus package sponsored by the US$12 billion aid package from the Gulf (more on the package in the fiscal outlook). In addition to the package, several other policy actions have been taken under the theme of “social justice” that will be directing funds to the consum- ers in the lower income brackets. Examples of such poli- cies are, an LE1,200 minimum wage in the public sector, a 10% increase in pensions with a minimum increase of LE50 and raising the income tax exemption bar to LE12,000 annually. The expansionary fiscal policy is also coupled with expansionary monetary policy. The Monetary Policy Committee (MPC) of the Central Bank of Egypt (CBE) has finally changed course since it hiked rates by 100bps in late 2011 and a further 50bps in early 2013. The MPC has already cut rates by a 100bps in two consecutive meetings in August and September. It is worth mentioning that the government is mulling a second stimulus package. However, the timing, the size or the source of financing of the package remains unclear. Hence, we exclude the scenario of a second stimulus pack- age from the current estimates. Either way, we do not expect the second stimulus package to have a significant effect on this year’s economic performance since it will not be finalized before the third quarter with the first stimu- lus package yet to be completed. Growth Forecast The government aims at accelerating GDP growth this year targeting a real growth rate of 3.5%, hoping for a re- covery in tourism and investments, both domestic and FDI. On the other hand, the World Economic Outlook (WEO) for October 2013 seems overly pessimistic regarding Egypt’s growth rate this year forecasting a 1.8% real growth in output. We see GDP growth this year at around 2.7%, missing the government target, though still much better than the WEO forecast. Nominal GDP will culminate at LE2,025 billion. Our forecast is based on the below dynamics. FY14fFY13aFY12aFY11aFY10aLE billion 20251753157613711207GDP at market prices 2.82.12.21.85.1Real GDP Growth (%) 1637142312711036900Household Consump- tion 2.52.86.55.54.1Real Growth (%) 247205179157135Government Con- sumption 4.83.53.13.84.5Real Growth (%) 272249258235235Investment 2.3(9.6)5.8(2.2)8.0Real Growth (%) 306309275282258Exports (1.5)4.1(2.3)1.2(3.0)Real Growth (%) 436432407339321Imports (0.8)(1.1)10.88.4(3.2)Real Growth (%) 142125125178172Gross Domestic Sav- ings (130)(123)(133)(57)(63)Domestic Resource Gap Figures are nominal and in billions of Egyptian pounds, growth rates are real. Source: Ministry of Planning & Prime Estimates GDP Breakdown by expenditure Fundamentals are weak across all expenditure items Private consump- tion, has eventually slowed down Investment spend- ing crippled since 2011 Exports did not come to the rescue, while imports proved resilient LE29.7 billion stimulus package LE1,200 minimum wage 10% increase in pensions Raising the income tax exemption bar MPC has already cut rates by a 100bps We exclude the scenario of a sec- ond stimulus pack- age from the cur- rent estimates Government targets a real growth rate of 3.5% We see GDP growth this year at around 2.7%

- 3. Prime Research 3 Egypt Economic Outlook December 02, 2013 Growth Outlook Private Consumption For years, the Egyptian economy have relied on its huge population base and its rapid population growth to fuel the private consumption engine, which represents north of 80% of GDP. However, under the weight of stagnant real incomes, staggering unemployment (which reached 13.4% in Q3 FY13), soaring inflation as well as street violence, private consumption spending slew down to 2.8% in FY13 down from a resilient 6.5% in FY12. As mentioned above, the government’s “social justice” measures will be channeling funds to the consumers in the lowest income brackets through the minimum wage, rise in pensions and tax exemptions which should lead to a rise in consumption. However, we believe that consumption will remain subdued and unlikely to recover before the second half of the year for the following reasons: • While not much data is available regarding the first quarter yet, the dusk-to-dawn curfew must have weighed heavily on consumption. • Almost all of the social justice measures taken are exclusive for government employees. For example, the minimum wage will only apply to 4.8 million government employees, disregarding the remaining 18.8 million pri- vate sector employees. • Unemployment remains alarmingly high, registering 13.4% in the first quarter of the fiscal year, putting a cap on consumption spending. • Unchecked inflation, especially food inflation which represents roughly 40% of consumption spending, could eat away most of the nominal growth in consumption. Hence, we expect real private consumption growth around 2.5% in the current fiscal year. Government Consumption We predict that government consumption growth would accelerate in FY14 to 4.8%, up from 3.5% last year due to: • Aggressive spending by the government will continue amid a continued slowdown in the private sector to ap- pease the people and sustain the economy • The higher salary bill caused by the minimum wage law, which adds LE11 billion to salaries. In addition, we expect more hiring of temporary workers by the government for the projects planned in the stimulus package. • An LE3.4 billion in additional spending on salaries and purchases of goods and services allocated from the stimulus package. However, it is necessary to highlight that the aggressive spending by the government will take place at the cost of a continued high budget deficit and a ballooning public debt, but more on the deficit and the debt in the fiscal out- look. Private consump- tion spending slew down to 2.8% in FY13 down from a resilient 6.5% in FY12 C o n s u m p t i o n unlikely to recover before the second half of the year. We expect real private consump- tion growth around 2.5% in the current fiscal year. Government con- sumption growth would accelerate in FY14 to 4.8% Unemployment (%) Source: CAPMAS 8.0 9.0 10.0 11.0 12.0 13.0 14.0 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

- 4. Prime Research 4 Egypt Economic Outlook December 02, 2013 Growth Outlook Investments The government targets investments of around LE290 billion in the current fiscal year in order to reach its tar- geted growth rate of 3.5%. The LE290 billion are sup- posed to consist of LE120 billion public investments and LE170 billion in private investments. We expect invest- ments during the current year to culminate at LE270 bil- lion, yielding a real growth rate of 2.3% on the back of: • A major portion of the stimulus package designed by the government, LE 15.8 billion out of LE29.7 billion, is directed towards investments. The government plans to invest in projects that are close to completion (such as the third metro line) so that they would start production as soon as possible, in addition to invest- ing in the country’s infrastructure to encourage pri- vate sector investments. • The lower interest rates due to the CBE one percent- age point rate cut would encourage the business sec- tor to borrow and invest. • An easing of regulations by the EFSA would boost investments by listed companies. Indeed, the market has already witnessed several major capital increases since the beginning of the year. • On the other hand, we do not expect FDI to recover yet as it awaits further stability in the political scene as well as on the external front (looser capital con- trols and easier repatriation). However, the US$2.9 billion investments from the UAE as well as the US$900 million in oil investments from the 21 new contracts are expected to sustain FDI. Net Exports Despite the sharp pound depreciation during last year, we believe exports of goods and services would decline by 1.5% during this year for the following reasons: • Petroleum exports, especially natural gas, will decline as domestic consumption grows aggressively, while production stagnates as foreign oil companies ap- proach Egypt cautiously in the current period. • Non Petroleum goods exports face several supply constraints in the short term that would hinder it from re- sponding elastically to the depreciation of the pound. The main constrains are energy and capacity. • Exports of services would fall due to the plunge in tourism in the first quarter as many countries issued travel bans on Egypt on the back of the increased violence following the ousting of the former president. While most of the travel bans have been lifted already, the quarter of travel bans have already had a negative effect on tourism revenues. Imports will also decline, albeit with a smaller magnitude, by 0.8% during the year on the back of the foreign cur- rency rationing and the free shipments of petroleum from the Gulf which have saved Egypt US$4 billion in petro- leum imports. Still, most of Egypt’s imports are necessities or inputs to the production process which makes cutting down imports in response to the depreciation challenging, but more on exports and imports in the External Outlook below. FY13aFY12aLE billion %²GDPInv.%²GDPInv.Sectors 3.024382.92185Agriculture (2.7)291580.126258Extractions (1.2)125191.01117a) Crude Oil (4.0)15939(0.7)14552b) Natural Gas 2.9702.360c) Other Extractions 2.3263260.723820Manufacturing 2.7209-4.71710a) Oil Refining 2.2243171.022110b) Other Manufacturing 4.621165.91917Electricity 4.1554.645Water 5.97733.3672Construction & Build- ing 2.967212.86131Transportation & Storage 4.941155.23914Communications 3.4354.132Information (3.8)3203.9310Suez Canal 2.818482.01669Wholesale and retail 2.75512.2501Financial Intermediation 3.16002.5540Insurance & Social soli- darity 6.65372.3466Tourism 4.243353.23839Real Estate 2.81862.5166Education 3.12143.0194Health 2.9201232.917817Others³ 2.11,6772422.21,509236 ¹ GDP at factor cost, both GDP and implemented investments are in nominal ² %: real growth rate of GDP by sector ³ Others include sewage & drainage, general government and other services and settlements Source: Ministry of Planning GDP¹ and Implemented Investments by sector We expect invest- ments during the current year to culminate at LE270 billion, yielding a real growth rate of 2.3% We believe exports of goods and ser- vices would decline by 1.5% Imports will also decline, albeit with a smaller magni- tude, by 0.8%

- 5. Prime Research 5 Egypt Economic Outlook December 02, 2013 Fiscal Outlook New Government, Old Budget Despite the changing political and economic climate post June 30 which required the new government to set a new budget that reflects its own assumptions and plans, the government embraced the budget prepared under the previous government and approved by the dissolved Shura Council. The budget expected to spend LE692 bil- lion and collect LE497 billion in taxes and other revenues, leaving LE195 billion or 9.6% of GDP as budget deficit, a deficit level which the new government committed to. The only amendments to the budget, by the new government, represent the LE30 billion stimulus package on the expen- diture side and its financing from the Gulf on the revenue side. We view the government’s deficit target not to exceed 10% of GDP as unrealistic. We estimate deficit to GDP ratio at around 13.9% for the following reasons: 1) The changing economic environment had two main effects on the budget, namely: • The eruption of street violence and the application of a dusk-dawn curfew seriously harmed business activ- ity and consumption in the first quarter of the year thus, lowering sales and corporate taxes as well as taxes on international trade and other revenues than previously forecasted by the budget. • The fall in yields on the government’s T-bills and T- bonds, following the ousting of former President Mursi, is estimated to save the new government around LE21 billion in interest. 2) The government has taken several policy measures that would raise the government’s expenditure bill, namely: • Applying a minimum wage to all public sector employees of LE1,200 starting January 2014 (the Ministry of Fi- nance estimates that the policy will raise salaries and wages by LE11 billion in FY14) • Increasing pensions by 10% with a minimum increase of LE50 starting January (Estimated by official sources to add LE4 billion to the expenditure side of this year’s budget) • Raising the income tax exemption bar to LE12,000 annually (which will cost the government LE4 billion in lost income tax revenues according to official estimates). Before we briefly present our view on the budget’s main items for FY14, we would like to discuss a few longer term issues. Structural Problems Despite massive political change and the transfer of power between several regimes, the economic system remains widely unchanged and continues to suffer from the same deeply rooted structural problems. • Salaries, interest and subsidies continue to dominate the majority of government spending with north of 80% of total expenditure in FY13. Unlike other items in the budget, the above three are largely inflexible in the sense that cutting down on any of them would require major policy change (such as lifting subsidies, firing employees or defaulting on debt). Hence, the government’s budget has very little room for maneuvering to significantly lower deficits in the short term without tackling the above issues. • The government continues to make long term commitments while only considering the short term availability of funds. The new policies mentioned above will cost LE17 billion this year which sounds affordable against the LE60 billion aid from the Gulf. However, the same policies will burden FY15 budget by LE31 billion during times in which the deficit has already reached alarming rates and availability of financing is still unclear. FY14fFY14b**FY13a*FY12aFY11aLE billion 456527345304265Total Revenues 303357251207192Tax Revenue 32325102Grants 7195565641Property Income 5043323030Other Revenue 735718583471402Total Expenditure 19517514112396Compensation of Employees 3231252726Purchase of Goods & Services 16118214710485Interest 229212197150123Subsidies & Social Benefits 8080383640Purchase of Non- Financial Assets 3838353131Other Expenditure 279191238167137Cash Deficit 13.99.513.610.610.0Deficit (% of GDP) f: prime forecast b: government budget *FY13 figures are preliminary ** The figures represent the approved budget by the Shura Council in addition to the modifications to the budget approved by President Adly Mansour Source: Ministry of Finance & Prime Estimates State Budget The government embraced the budget prepared under the previous government We view the gov- ernment’s deficit target not to ex- ceed 10% of GDP as unrealistic. We estimate deficit to GDP ratio at around 13.9% Salaries, interest and subsidies dominate govern- ment spending The government continues to make long term commit- ments considering only the short term availability of funds

- 6. Prime Research 6 Egypt Economic Outlook December 02, 2013 Fiscal Outlook Compensation of Employees We expect the salaries bill to rise to LE195 billion up from LE141 billion last year on the back of: • The introduction of the minimum wage law starting January which will require salary increases and ad- justments not just for the lowest employment grades but to the whole grade ladder and most of the gov- ernment’s employees. The Ministry of Finance esti- mates the cost of the minimum wage LE21.4 billion, revised upwards from LE18 billion for the full year or around LE11 billion for 2H FY14. • Increased hiring by the government especially under the temporary workers category for the projects planned in the stimulus package. Debt Service The widening of the budget deficit to record levels in the previous three years led to a swift increase in government debt which further burdened the following budgets with debt servicing. We expect government gross domestic budget sector debt to continue to climb aggressively dur- ing FY14 to hit LE1.8 trillion on the back of another year of aggressive deficit spending by the government. Despite the continuation of the crowding out effect by the government, yields on T-bills and bonds started falling following June 30 on improved investor sentiment and the expectations of rate cuts by the CBE. Rates on T-bills fell by around 4 percentage points between June and October depending on maturity. Rates on bonds also declined al- beit with smaller magnitude. We expect T-bill and T-bond rates to stabilize at the current levels at least until the end of Q3 FY14. Of course, T-bills do not constitute all of the domestic debt but only 30% of it. The rest of the debt is mostly fixed rate, longer maturities, limiting the favorable effect of the decline in fixed income yields on the debt servicing bill of the government. As for external debt, we discuss it extensively in the external outlook below. However, we expect its debt servicing bill to come in slightly higher in LE terms than last year on the back of a weaker pound. Otherwise, we expect pay- ments in US$ to remain stable despite the rise in outstanding debt, as most of the new debt is interest free. Based on the above analysis we expect interest payments to stand at LE161 billion up from LE147 billion last year but lower than the budgeted LE182 billion due to lower rates than forecasted by the budget. Source: Ministry of Finance & Prime Estimates Salaries Source: Ministry of Finance & Prime Estimates Gross Domestic Debt T-bill auction yields 10.00 11.00 12.00 13.00 14.00 15.00 16.00 27-Jun 4-Jul 11-Jul 18-Jul 25-Jul 1-Aug 8-Aug 15-Aug 22-Aug 29-Aug 5-Sep 12-Sep 19-Sep 364 days 273 days 182 days 91 days Source: Ministry of Finance We expect the salaries bill to rise to LE195 billion We expect govern- ment gross domes- tic budget sector debt to continue to climb aggressively during FY14 to hit LE1.8 trillion We expect T-bill and T-bond rates to stabilize at the current levels at least until the end of Q3 FY14. we expect interest payments to stand at LE161 billion The composition of Egyptian debt (FY13) SIF bonds 16% T-bonds and notes issued to CBE 16% T-bills 30% T-bonds 23% Borrowing from other sources 4% Budget Sector Bank loans 11% Source: Ministry of Finance - 500 1,000 1,500 2,000 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14f LEbillion - 40 80 120 160 200 Gross Domestic Debt (left axis) Interest Payments (right axis) Principal Payments (right axis) - not forecasted for FY14 52 63 76 85 96 123 141 195 0 40 80 120 160 200 LEbillion FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14f

- 7. Prime Research 7 Egypt Economic Outlook December 02, 2013 Fiscal Outlook Subsidies, Grants and Social Benefits Subsidies are one of the most crucial items not just in the Egyptian fiscal budget but perhaps in the Egyptian econ- omy as a whole. The subsidy system, especially the en- ergy subsidy system, has been criticized for years for its inefficiency and its social value has been questioned re- peatedly. Indeed, the government has taken several measures towards adjusting the prices of energy delivered to different industries. However, the will to reform subsi- dies on consumer items (benzene, gas oil and butane) have been weak for fear of a major hike in inflation. The latest program to conserve oil subsidies has been the smart card system; the introduction of which has been delayed several times till now. The early phases of the program will require vehicle drivers to use the smart cards at the petrol stations, yet with no restrictions on quantities or price changes. This stage is planned to kick off during the current fiscal year. However, we are skeptic that it will cause major savings in subsidy spending. However, we believe that the smart card system could be used in later stages to deliver subsidies to those who need it exclu- sively or cut subsidies all together in an organized manner over phases (e.g. geographical areas or types of consumers). While writing this report, Prime Minister Hazem El-Beblawi said that the government will start the first phase of a five to seven year program to reform fuel subsidy, pending “a smooth passage of the roadmap”. While, we see that political will, public awareness and even media attention regarding the issue are remarkably improving, we remain doubtful that any actual cuts in subsidy will take place before the political situation in the country stabilizes through a new constitution in place and an elected parliament and president overseeing the government. Based on our analysis we expect subsidies and social benefits to amount to LE229 billion compared to a last year figure of LE197 billion and a budgeted figure of LE206 billion. Out of which food subsidies contribute LE39 billion (LE33 billion last year and LE31 budgeted), while petroleum products subsidies amount to LE108 billion (LE120 bil- lion last year and LE100 billion budgeted). Purchases of Non-Financial Assets (Investments) The government’s original budget figure for investments for FY14 was LE64 billion, almost double the final figure for last year of just LE38 billion. Furthermore, the major part of the stimulus package, LE15.8 billion, is directed towards investments, taking the government’s targeted investments level to a staggering LE80 billion. The gov- ernment plans to invest in projects that are close to com- pletion (such as the third metro line) so that they would start production as soon as possible, in addition to invest- ing in the country’s infrastructure to encourage private sector investments. While we will not speculate on how much of the govern- ment’s planned investments are going to be executed, we would like to highlight a certain trend with regard to investments in the budget. Before 2011, the govern- ment’s final investment figure used to overshoot the budgeted figure by at least 15%. On the contrary, since 2011, the government’s final investment figure started to come short of the budgeted figure as the government’s finances tighten amid a need to curb the deficit. Our deficit to GDP forecast of 13.9% implies that the government would meet its ambitious invest- ments target. While we will not speculate over how much will the government spend into investments, we would like to draw attention that the government might have an incentive to cut back in its investments to con- tain the deficit. Source: Ministry of Finance & Prime Estimates Stimulus Package Breakdown by category Acquisition of financial assets, 4.3 Investments, 15.8 Wages and Salaries, 2.6 Purchases of goods and services, 0.8 Subsidies, 6.2 Source: Ministry of Finance Energy subsidy vs. oil price No restrictions on quantities or price changes in the early phases of the smart card system We remain doubtful that any actual cuts in subsidy will take place before the political situation in the country stabi- lizes Subsidies and social benefits to amount to LE229 billion The major part of the stimulus pack- age, LE15.8 billion, is directed towards investments Since 2011, the government’s final investment figure started to come short of the budg- eted figure Government might have an incentive to cut back in its investments to contain the deficit - 20.0 40.0 60.0 80.0 100.0 120.0 140.0 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14f LEbillion 0.0 20.0 40.0 60.0 80.0 100.0 120.0 Petroleum Subsidy Brent Crude (US$/Barrel)

- 8. Prime Research 8 Egypt Economic Outlook December 02, 2013 Fiscal Outlook Revenues As mentioned earlier, the new government that took over in July did not amend the budget prepared during Mursi’s one year in power. The new Finance Minister Ahmed Galal repeatedly mentioned that deficit will not exceed 10% of GDP just like in the budget. One main reason why we see the budget deficit targeted by the Minister as unrealistic is that the tax revenue esti- mates in the budget were made in a different economic environment. The fundamentals of several sectors changed significantly with the regime change as well as the general level of economic activity. To elaborate, the budget did not foresee almost a quarter of dusk-dawn- curfew, neither did it predict tourism sector plunging that hard in Q1 FY14. Furthermore, we do not expect significant progress on any front that will lead to a higher tax revenue amid such a fragile political environment. The Minister of Finance had made it clear several times that the government does not currently intend to raise taxes. The government, however, cites efforts to widen tax base by formalizing the huge and unregulated informal sector in Egypt, which we see as a better option. Still, given the government’s short life and its long list of more critical priorities, significant progress in this front will also be unlikely. Hence, we believe that the tax and other revenue items in the budget are remarkably overstated. We expect the government to collect revenues of LE456 billion (vs. LE345 billion last year and LE497 billion budgeted). Out of which, tax revenue amounts to LE303 billion (LE251 billion last year and LE357 billion budgeted). Other revenues will bring around LE121 billion (vs. LE89 billion last year and LE138 billion budgeted). The rest is the LE32 billion grants from the Gulf aid package. Source: Ministry of Finance & Prime Estimates Revenues The tax revenue estimates in the budget were made in a different eco- nomic environment We do not expect significant progress on any front that will lead to a higher tax revenue amid such a fragile politi- cal environment We believe that revenues in the budget are re- markably over- stated. We expect the government to collect revenues of LE456 billion 0 50 100 150 200 250 300 350 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14f LEbillion Tax revenues Grants Other Revenues

- 9. Prime Research 9 Egypt Economic Outlook December 02, 2013 External Outlook Reserves Replenished By the end of June 2013, the CBE’s net international re- serves had reached US$14.9 billion covering only 3.1 months of imports, only slightly above its near decade low of US$13.1 billion reached in March 2013. The decline in reserves was accompanied by a steep depreciation of the pound that started in early 2013 when the pound lost around 15% of its value. The new government received a US$15.9 billion aid pack- age from the Gulf to replenish its reserves and cover Egypt’s domestic oil needs temporarily until economic activity picks up and Egypt can rely on its own sources of foreign currency again. The aid took different forms: grants, petroleum products, interest free deposits and FDI. BOP Fundamentals Still Weak Unfortunately, fundamentals for the Balance of Payment, albeit slightly better, remain weak in our opinion. Sources of currency inflows remain limited while currency outflows prove resilient. In our opinion, the trade deficit will marginally narrow to US$28.5 billion in the current fiscal year, down from US$31.5 billion last year. However, the services surplus will fall to US$4.2 billion from US$6.7 billion on the back of lower tourism and other transportation revenues offset- ting the improvement in the trade balance. Remittances will also stagnate as Saudi Arabia, the largest foreign mar- ket for Egyptian labor, proceeds with its labor reform to create more jobs domestically. All in all the current ac- count deficit would culminate at US$4.7 billion, slightly better than US$5.6 billion last year. Regarding the capital and financial account, most of the capital inflows will appear under Central Bank liabilities in the form of deposits from the Gulf at the bank to replen- ish reserves. we do not expect a recovery in net FDI to take place during this current year, only sustained by the US$2.9 billion investment in wheat silos from the UAE as well as 21 new petroleum contracts. Inwards portfolio In- vestment will be scarce discouraged by the capital controls. The financial account would culminate at US$6.8 billion down from US$9.8 billion last year leaving a balance of payments surplus of only US$1.2 billion. As a result, reserves will have to decline from their current levels to US$16.2 billion back to alarming levels (3.5 months of import coverage based on FY14 imports and lower in terms of FY15 imports). Downward pressures on the value of the pound could be renewed. The dynamics will leave Egypt in need of further aid or in risk of further depreciation of the currency towards the end of the fiscal year. We estimate that the Egyptian economy would need between US$3.0 and US$5 billion in additional aid during the current fiscal year to avoid a renewed crisis. FY14fFY13aFY12aFY11aFY10aUS$ billion 25.726.025.127.023.9Exports of goods 11.512.011.212.110.3Petroleum 14.214.013.814.913.6Non-Petroleum exports (54.2)(57.5)(59.2)(54.1)(49.0)Imports of goods (9.5)(12.5)(11.8)(9.3)(5.2)Petroleum (44.7)(45.0)(47.4)(44.8)(43.8)Non– Petroleum imports (28.5)(31.5)(34.1)(27.1)(25.4)Trade Balance 19.122.220.921.923.6Services Receipts, of which 8.99.28.68.17.2Transportation, of which 5.15.05.25.14.5Suez Canal 7.09.79.410.611.6Tourism (14.9)(15.5)(15.3)(14.0)(13.2)Services Payments 4.26.75.67.910.3Services Balance 19.519.318.413.110.5Transfers (4.7)(5.6)(10.1)(6.1)(4.3)Current Account 3.03.04.02.26.8Net FDI 0.71.5(5.0)(2.6)7.9Inwards Portfolio Inv. 6.89.81.1(4.2)9.0Financial Account 1.20.2(11.3)(9.8)3.4Balance of Payments 6.06.51.201.2Central Bank Liabilities 16.214.915.526.635.2End of Period Reserves Source: Central Bank of Egypt & Prime Estimates 12 16 20 24 28 32 36 Jan-11 Mar-11 May-11 Jul-11 Sep-11 Nov-11 Jan-12 Mar-12 May-12 Jul-12 Sep-12 Nov-12 Jan-13 Mar-13 May-13 Jul-13 Sep-13 5.8 6 6.2 6.4 6.6 6.8 7 7.2 NIR (US$ bn) EGP/USD Source: Central Bank of Egypt & Bloomberg Net International Reserves and exchange rate Current Account Fundamentals for the Balance of Payment, albeit slightly better, remain weak in our opinion Trade deficit will marginally narrow to US$28.5 billion. However, the ser- vices surplus will fall to US$4.2 billion. All in all the current account deficit would culminate at US$4.7 billion. Most of the capital inflows will appear under Central Bank liabilities in the form of deposits from the Gulf The financial ac- count would culmi- nate at US$6.8 billion Reserves will have to decline from their current levels to US$16.2 billion The Egyptian econ- omy would need between US$3.0 and US$5 billion in additional aid

- 10. Prime Research 10 Egypt Economic Outlook December 02, 2013 External Outlook Exports of Goods and Services While standard economic theory suggests that exports of goods should boom upon a currency depreciation as they become cheaper to the outside world, Egyptian exports face several supply constraints that would hamper the growth in exports at least in the short run. Petroleum exports, especially of natural gas, will come under pressure as domestic consumption grows aggressively motivated by the subsidized prices, while production stagnates as foreign oil companies approach Egypt cautiously in the current period on the back of the accumulating dues, political turbulence and the reluctance of the consecu- tive governments to proceed with subsidy reform. Hence, we see petroleum exports at US$11.5 billion in FY14. Regarding non petroleum exports, the chemicals industry, one of Egypt’s top non petroleum exporters, is facing severe shortages in natural gas supply, which represents its main input, and has reduced production capacity sharply since the beginning of 2013. Other energy intensive industries are all experiencing shortages in energy sup- ply and have reacted in a similar fashion. Meanwhile, agricultural exports can not grow to a significant level as they are already constrained by cultivated land, fertilizers supply and domestic consumption. Other export categories such as pharmaceuticals have a high imported component of raw materials that would offset most of their gain from the depreciation of the pound. As a result, we expect non petroleum exports to amount to US$14.2 billion in FY14, up from US$14.0 billion in FY13. Service receipts or exports of services are also not going to benefit from the depreciation. Tourism, which repre- sents 43% of service receipts and a staggering 20% of total exports of goods and services, has seen a severe slump on the back of the undermined security situation and the travel bans issued by countries which dominate Egypt’s tourism market. We count at least one quarter of extremely low levels of tourism revenue, while Egypt’s peak tourism season still faces a weak flow of tourists. Recovery is not expected before the third quarter of the year and could possibly take longer. Hence, we expect tourism revenues to fall sharply to US$7.0 billion from US$9.7 billion last year. Suez Canal receipts are expected to see a marginal improvement on the back of stronger recovery in Europe and Asia. However, transportation other than Suez Canal, mostly on land transportation that passes through Egypt, is expected to suffer from the instability in Sinai from the East and the developments in Libya from the West. As a result, transportation receipts are estimated to total US$8.9 billion, down from US$9.2 billion last year. Imports of Goods and Services The shortage and rationing of foreign currency, since the FX crisis hit early this calendar year and the introduction of the new FX auction system by the CBE, undoubtedly plays a crucial rule in squeezing imports and prioritizing them to the most essential. Furthermore, the petroleum products aid from the gulf (US$3 billion in the original aid package, in addition to an estimated US$1.3 billion from the UAE based on announcement by officials) will help offset part of the petroleum imports bill. Still, Egypt’s imports are mostly dominated by necessities which are harder to ration or substitute. Fuels, Wheat and Maize which are basic necessities represent around a third of the imports and are hard to ration. Intermediate goods represent another third and are used as inputs in produc- tion; squeezing them would add to the domestic slow- down and could possibly affect exports if some of them are to be re-exported. Investment goods are another US$10 billion (17% of imports) and are also needed to raise production capacity and accelerate growth. Con- sumer durables like cars, refrigerators, etc, which cost US$3.2 billion, are expected to decline as their prices rise on the back of the depreciation amid a period when Egyp- tians cut back on consumption. Consumer non-durables, US$9.3 billion is the category which is most likely to see sharp contractions as Egyptians substitute its components for cheaper local alternatives. All in all, we see goods im- ports declining 5% to US$54.2 billion in the current fiscal year, down from US$57.5 billion last year. Wheat US$2.0 Other (iron ore, cotton, etc) US$2.4 bn Undistributed Commodities US$0.6 bn Consumer non- durables US$9.7 bn Intermediate goods US$16.0 bn Investment goods US$9.8 bn Raw M aterials US$5.6 bn Consumar durables US$3.2 bn Fuels US$12.6 bn M aize, US$1.2 bn The breakdown is based on 2012 figures Source: Central Bank of Egypt Imports Breakdown by Degree of Processing Egyptian exports face several supply constraints Petroleum exports at US$11.5 billion N o n - p e t r o l e u m exports to amount to US$14.2 billion Tourism has seen a severe slump, recovery is not expected before the third quarter Tourism revenues to fall sharply to US$7.0 billion Egypt’s imports are mostly dominated by necessities which are harder to ration or substitute we see goods imports declining 5% to US$54.2 billion in the cur- rent fiscal year

- 11. Prime Research 11 Egypt Economic Outlook December 02, 2013 External Outlook Remittances It is worth mentioning that workers’ remittances have worked magnificently in the last few years to offset the weak- ness in tourism and FDI, doubling since 2010. However, the labor reforms taken in Saudi Arabia, the largest foreign market for Egyptian labor, to create more domestic jobs for Saudi citizens will in best case slow down the growth of remittances, if not reverse it. 40 thousand Egyptians have already left the Saudi Arabia and 38 thousands are facing troubles with their work permit disputes in the Kingdom. FDI Foreign Direct Investments in Egypt have always been dominated by the Petroleum sector which represented north of 60% of gross FDI inflows in any given year, even during the high growth years pre-2008. As already known, yearly net FDIs have fallen significantly since January 2011 due to both declining FDI inflows and rising FDI outflows. However, the remarkable outflows have been contributing more significantly to the falling net FDIs than the deterioration in inflows. While no official breakdown of the FDI outflows is avail- able, a large sum of which must have been attributed to the petroleum sector which represents the majority of foreign direct investments in the country. This can be seen in light of the fact that Egypt had accumulated dues to foreign oil companies operating in Egypt amounting to US$6.2 billion in addition to delaying contracted natural gas shipments and directing it to domestic use. Such prac- tices by the Egyptian authorities have definitely discour- aged foreign oil and gas companies from reinvesting their earnings in the country in order to limit their exposure. We see the new government keen on amending relation- ships with foreign oil and gas companies by scheduling its dues and planning to start repaying them quickly in order to draw investors back to the sector. The government had already signed 14 out of 21 new excavation agreements, which are the first since 2010, scheduled for this year. The 14 signed agreements amount to US$585 million in investments as well as US$91 million in signature bo- nuses. However, it is worth highlighting that the tough investment experience of oil and gas companies in Egypt in the past three years had made them reluctant to invest aggressively in the sector before subsidy reform measures are taken to cap the huge domestic demand leading to a repeated outcome of directing production to the domestic market and accumulating dues by the government. Still, we do not expect a recovery in net FDI to take place during this current year. In fact, we expect gross FDI in- flows to fall sharply during the year as foreign investors shun Egypt on the back of the political instability and the risk of inability of repatriation, but we also expect FDI outflow to fall offsetting the fall in gross inflows as inves- tors find difficulty in repatriation. As a result, We expect net FDIs to amount to roughly US$3.0 billion in FY14 dominated by the US$2.9 billion investment in wheat silos from the UAE as well as the petroleum contracts. There is potential however for further FDI from the Gulf as their aid to the Egyptian economy starts taking a more sustain- able shape. H1 FY13FY12aFY11aFY10aFY09aUS$ million 3,2427,1017,0157,5779,667Petroleum 160733804456852Manufacturing 94813026276Agriculture 9127109304226Construction 2886134305138Real Estate 260213114874441Finance 1442158247122Tourism 91391763727Communication & IT 42465207383283Other Services 8591,530996538305Undistributed 4,71911,7689,57411,00812,836Total FDI inflow 4,4187,7867,3864,2504,723FDI Outflows 3013,9822,1896,7588,113Net FDI Source: Central Bank of Egypt & Prime Estimates FDI by Economic Sector Source: Central Bank of Egypt FDI Inflows and Outflows The labor reforms taken in Saudi Arabia will in best case slow down the growth of remit- tances, if not re- verse it Remarkable out- flows have been contributing more significantly to the falling net FDIs than the deteriora- tion in inflows We see the new government keen on amending rela- tionships with foreign oil and gas companies we expect gross FDI inflows to fall sharply during the year but we also expect FDI outflow to fall offsetting the fall in gross inflows. Net FDIs to amount to roughly US$3.0 billion in FY14 0.00 2.00 4.00 6.00 8.00 10.00 12.00 14.00 FY09 FY10 FY11 FY12 FY13 US$billion FDI inflow FDI outflow

- 12. Prime Research 12 Egypt Economic Outlook December 02, 2013 External Outlook External Debt The last fiscal year has seen external debt balloon signifi- cantly rising by US$8.8 billion or a staggering 26%. The rise in external debt was the last resort, after net interna- tional reserves were consumed, if the country was to avoid a severe energy shortage, a freefalling exchange rate and skyrocketing inflation. Still, given that external borrowing was the only short term option for the government, we believe that the terms at which the government raised its external debt were rather favorable. The majority of the debt taken during the year was in the form of interest free deposits at the CBE, which saw its external debt leap around US$6.5 billion. Of which, US$2 billion are a Libyan deposit with a maturity of 8 years, while the rest were a US$4.5 billion Qatari deposits, US$1 billion of which was con- verted to a 3 year bond at 3.5% per annuam, US$2 billion were to be covered by bonds while the rest were to re- main as deposits. Bonds and notes increased by around US$2.25 billion on the back of the issuance of US$2.5 billion in bonds to Qatar maturing in November 2014 and carrying an interest of 4.25%. The favorable external financing obtained is reflected in stable interest payments on external debt. Interest paid in FY13 amounted to US$643 million compared to US$658 million in the previous year. External debt has continued to rise in FY14 as foreign assistance continues to be the only short term solution to the Balance of Payments problem. The Gulf aid package which included US$ 6 billion in interest free deposits are expected to take the monetary authorities debt higher even after the repayment of US$3 billion back to Qatar. External debt as of the date of this report is estimated at US$46 billion. Additional aid Based on our analysis above, it seems likely that balance of payments dynamics are going to lead reserves to de- cline again by FY14 end, which can potentially renew pressures on the currency and endanger the whole economy, unless further aid is secured which we view as the more likely scenario. The amount of additional aid needed to avoid another balance of payments squeeze during the current year is between US$3.0 and US$5.0 billion. We examine below the sources of additional financing potentially available: The Gulf states So far the Gulf states have provided massive amounts of aid to support the Egyptian economy. Till the date of writ- ing this report, Saudi Arabia, UAE and Kuwait have provided US$15.9 billion. However, the possibility of further aid from the Gulf remains unclear. On one hand, the Emirati Minister of presidential affairs was quoted saying that the Arab support to Egypt won’t last long . On the other hand, news are circulating that negotiations are under way with Saudi Arabia, Kuwait and the UAE regarding further aid whether grants or petroleum products. Still, we view additional aid from the Gulf as the most likely scenario. The International Monetary Fund (IMF) The IMF has already reiterated that it is ready to cooperate with the new government waiving its US$4.8 billion loan that has been on the table since January 2011. However, the IMF loan comes with pre-conditions, the most impor- tant of which is a committed and fast paced plan towards subsidy reform along with austerity measures that bring the budget deficit to a more sustainable level. While all the consecutive governments since January 2011 have avoided the loan for the harsh conditions that will come along with it, the loan will remain as the last resort to avoid a severe economic crisis driven by further devaluation, which would dismantle the subsidy system and enforce austerity measures any way. Source: Central Bank of Egypt External Debt and Debt Servicing Last fiscal year has seen external debt balloon significantly rising by US$8.8 billion The terms at which the government raised its external debt were rather favorable External debt has continued to rise in FY14 as foreign assistance contin- ues to be the only short term solution Additional aid needed to avoid another balance of payments squeeze during the current year is between US$3.0 and US$5.0 billion We view additional aid from the Gulf as the most likely scenario The IMF loan will remain as the last resort to avoid a severe economic crisis FY13aFY12aFY11aFY10aFY09aUS$ million 28,49025,59427,09226,24925,818Gross External Government Debt 5,1592,9012,8213,0801,926Bonds and notes 23,33122,69424,27123,17023,892Loans 14,7448,7907,8147,4455,713Gross External Non- Government Debt 9,0642,6121,5001,260212Monetary Authorities 1,6001,6241,7251,9641,797Banks 4,0804,5544,5894,2213,705Other Sectors 43,23334,38534,90633,69431,531Gross External Debt Source: Ministry of Finance & Central Bank of Egypt Gross External Debt Breakdown - 10,000 20,000 30,000 40,000 50,000 FY07 FY08 FY09 FY10 FY11 FY12 FY13 US$million - 1,000 2,000 3,000 4,000 5,000 External Debt (right axis) Interest Paid (left axis) Principal Repaid (left axis)

- 13. Prime Research 13 Egypt Economic Outlook December 02, 2013 Monetary Outlook In this section, we briefly include our position on monetary developments during the year. Inflation Inflation has picked up sharply starting this fiscal year due to many consecutive events starting with Ramadan then the dusk-dawn curfew, which drove upwards trans- portation costs, followed by the Adha Eid and the back to school season. Food inflation, which crossed the 15% mark, in October continued to climb at rates north of 1% monthly becoming a serious concern for the government. As a result the government has imposed “indicative prices”, among other policies, in order to combat further food price jumps. However, so far, government efforts have failed to contain the rising prices. We expect inflation to moderate until January growing at less than 1% per month. This comes due to a better functioning food supply chain following the removal of the curfew resulting in lower transportation costs and availability of food items in the markets. Post January, we see inflation averaging 1% per month till June due to a pick in consumption spending as the effects of “social justice” policies by the government kick in. Average y-o-y inflation for the year would culminate at 10.9%. Interest rates The expansionary fiscal policy followed by the Ministry of Finance has been matched with expansion monetary policy by the Central Bank of Egypt (CBE). Indeed, the Monetary Policy Committee (MPC) of the CBE has already cut rates twice, each time by 50 bps in two consecutive meetings in order to stimulate private investments and growth. The lowering in rates by the CBE coincided with falling yields on the government’s T-bills and T-bonds which lowers the government’s spending on debt servicing. We believe that the CBE still wants to lower rates further as it outweighs growth over inflation, according to the MPC’s communiqué, amid a three year long recession. A further rate cut by the CBE would encourage borrowing and investing which have reached record lows as shown by the loan to deposit ratios of the banking the system. Furthermore, by cutting rates, the debt servicing bill of the government’s T-bills and T-bonds declines helping to con- tain the budget deficit. However, we do not expect the CBE to cut rates again before late February 2014 in order to make sure that the inflationary risks from the introduction of the minimum wage law and the rise in pensions has subsided. In addi- tion, clarity regarding the balance of payments position and the ability to secure more aid will be needed before the CBE can lower rates further. Otherwise, the rate cut might actually add to the inflationary pressures and en- danger reserves and the currency. Once the CBE has made sure that risks have subsided, it would cut rates by another 50bps with potential for more cuts in the next fiscal year. -2.00% -1.00% 0.00% 1.00% 2.00% 3.00% Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 0.00% 4.00% 8.00% 12.00% m-o-m y-o-y Source: Central Bank of Egypt Headline annual and monthly inflation 46% 48% 50% 52% 54% FY10 FY11 FY12 9MFY13 Aggregate Banking system loans to deposits Source: Central Bank of Egypt CBE overnight lending and deposit rates 8.00% 8.50% 9.00% 9.50% 10.00% 10.50% 11.00% Mar-11 May-11 Jul-11 Sep-11 Nov-11 Jan-12 Mar-12 May-12 Jul-12 Sep-12 Nov-12 Jan-13 Mar-13 May-13 Jul-13 Sep-13 Deposit rate Lending rate Source: Central Bank of Egypt The government h a s i m p o s e d “indicative prices”, among other poli- cies, in order to combat further food price jumps. However, so far, government efforts have failed to contain the rising prices Average y-o-y inflation for the year would culmi- nate at 10.9% The expansionary fiscal policy fol- lowed by the Minis- try of Finance has been matched with expansion mone- tary policy We believe that the CBE still wants to lower rates further as it outweighs growth over infla- tion However, we do not expect the CBE to cut rates again before late Febru- ary 2014 Once the CBE has made sure that risks have sub- sided, it would cut rates by another 50bps

- 14. Prime Research 14 Disclaimer Information included in this report has no regard to specific investment objectives, financial situation, advices or particular needs of the report us- ers. The report is published for information purposes only and is not to be construed as a solicitation or an offer to buy or sell any securities or re- lated financial instruments. Unless specifically stated otherwise, all price information is only considered as indicator. No express or implied representation or guarantee is provided with respect to completeness, accuracy or reliability of information included in this report. Past performance is not necessarily an indication of future results. Fluctuation of foreign currency rates of exchange may adversely affect the value, price or income of any products mentioned in this report. Information included in this report should not be regarded by report users as a substitute for the exercise of their own due diligence and analysis based on own assessment and judgment criteria. Any opinions given are subject to change without notice and may significantly differ or be contrary to opinions expressed by other Prime business areas as a result of using different assumptions and criteria. Prime Group is under no obligation responsible to update or keep current the information contained herein. Prime Group, its directors, officers, employees or clients may have or have had interests or long or short positions in the securities and/or currencies referred to herein, and may at any time make purchases and/or sales in them as principal or agent. Prime Group, its related entities, directors, employees and agents accepts no liability whatsoever for any loss or damage of any kind arising from the use of all or part of these information included in this report. Certain laws and regulations impose liabilities which cannot be disclaimed. This disclaimer shall, in no way, constitute a waiver or limitation of any rights a person may have under such laws and/or regulations. Furthermore, Prime Group or any of the group companies may have or have had a relationship with or may provide or have provided other ser- vices, within its objectives to the relevant companies. Copyright 2013 Prime Group all rights reserved. You are hereby notified that distribution and copying of this document is strictly prohibited with- out the prior approval of Prime Group. HEAD OFFICE PRIME SECURITIES S.A.E. Regulated by CMA license no. 179 Members of the Cairo Stock Exchange 2 Wadi El Nil St., Liberty Tower, 7th-8th Floor, Mohandessin, Giza, Egypt Tel: +202 33005700/770/650/649 Fax: +202 3760 7543 PRIME EMIRATES LLC. (UAE) Members of the ADX and DFM Shiekh Zayed 1st Street, Khaldiyah, Abu Dhabi, UAE, PO Box 60355 Tel: +971 2 6910800 Fax: +971 2 6670907 Email: research@primegroup.org Egypt Economic Outlook December 02, 2013 PRIME SALES TEAM Hassan Samir Managing Director – PS +202 3300 5611 Hsamir@egy.primegroup.org Mohamed Ezzat Head of Branches +202 3300 5784 mezzat@egy.primegroup.org Shawkat Raslan Heliopolis Branch Manager +202 3300 5110 sraslan@egy.primegroup.org Amr Alaa, CFTe Supervisor- Local Institutional Desk +202 3300 5609 aalaa@egy.primegroup.org Mohamed Magdy SRM—Gulf & MENA Desk +202 3300 5653 mmagdy@egy.primegroup.org Amr El Sebaee Manager, High Networth +202 3300 5112 asebaee@egy.primegroup.org