Download as PDF, PPTX

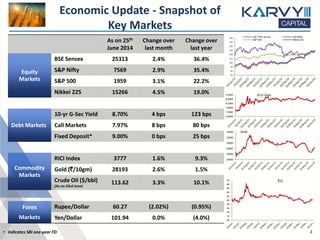

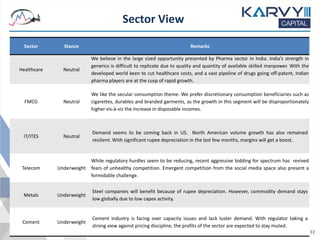

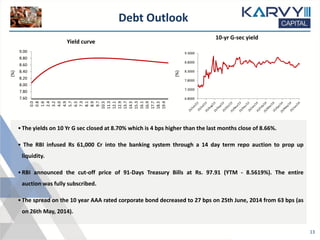

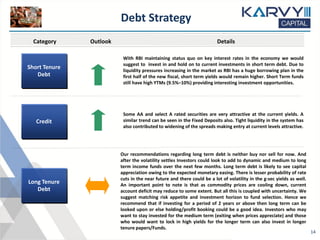

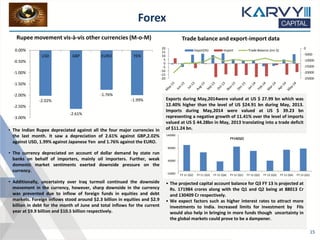

The document provides an economic and market update and outlook for India. It discusses that while May saw the beginning of a bull run, June was more of a reality check with several domestic and global concerns emerging. However, the overall diagnostic is still positive in the short term. It summarizes key economic data points and provides an outlook for various sectors such as banking, energy, infrastructure, and automobiles. The equity market outlook remains positive given reforms by the new government and expectations of improved earnings growth.