Fed must relent. Our expectations now is for a state dependent (global financial conditions to stabilise, cushion rising debt repayment burden and allowing domestic leverage to level off, coupled with still moderate economic growth/inflation, policy options to widen positively globally, especially in China) Fed relent with scope for a final 25-50bps, if any (pause otherwise), in late 2019/2020, should the cycle extents, with the FFR hitting cycle terminal at 2.75-3.00%.

Lower for longer; constructive ambiguity. Chair Powell took pains to paint an image of constructive ambiguity, repeatedly highlighting that the Committee is focused on pursuing policy that is “appropriate” in achieving its dual mandate. The current policy stance is deemed appropriate with current projections achievable via modest policy adjustments (likely -75bps of cuts). Nonetheless, if the economy turns down, “a more extensive sequence of rate cuts is appropriate”. As we argued prior, “it is better to guide for looser policy in an open-ended manner (flattening backwardation of rate cut expectations) rather than encourage front-loading of rate cut expectations”. We think that the Chair has achieved such an outcome, together with “guidance” for an extended pause at a minimum; the best mix of policy, considering circumstances.

We like rates structurally, both on adequate valuations (breakeven levels: 5y, 3.55% (2.98%); and 10y, 3.36% (3.09%)) and as a hedge for risk assets, taking the under on the (largely) priced base case of a smooth 3 year (2018-2020) rate hiking cycle. Based on our macro risk-neutral model and pure expectations, we see 1.80-2.50% and 2.10-2.30% on the UST 5 and 10. Our view is to stay long on the UST 5-10y, prefer 7y; tactical view suggests range trading, 10T around 2.80-3.20%, into 1H19 (Fed hikes by 75bps to 2.75-3.00% by 1H19; anchor extent of rates rally; near term upside risks of a Republican sweep of the mid-terms, providing the President and the Republican Party with another opportunity to pursue even looser (pro-wealth) fiscal policy.

201906 FOMC - An ounce of prevention is worth a pound of cure, unless when th...QuanJianChingCFACAIA

Key drivers will revolve around, i) global trade negotiations/future framework and its implications; ii) contagion from global growth slowdown and weakness in the industrial sector (disruptions to semi-cons, autos, energy sectors; Boeing); and iii) changes, if any, to the Fed’s reaction function. We do not see sufficient evidence of a steep slowdown into an outright recession (though recognize the uncertainties) which markets have broadly priced. The scale of policy guidance and aggressively priced rates markets, we believe, will turn out to be an error. Global financial conditions are rapidly easing, pushing up asset valuations on highly uncertain fundamentals with aggressively dovish pricing limiting future policy room to support markets. Instead of seeking to dampen volatility, it would have been better to realign markets to the Fed’s (strategic) reaction function and allow global markets to find its own levels (via two way volatility).

Tactically, we think that duration is rich and see US5T and US10T closer to 2.30-2.60% into 1H20 (+10-15bps in breakevens; +30-40bps in TP), expecting a bear steepening; preferring rolling the 3 month. Duration-adjusted, prefer front/backend to 2-7 years.

With a backdrop of accommodative policy and our view of generally anchored inflation and resilient growth over coming quarters, we believe that risk/carry will remain supported into 2H19, within the current context (using more binary rather than probabilistic analytical lenses; prolonged clarity over the opportunity cost of risk-free asset amid broadly stable growth/inflation).

Ivo Pezzuto - "FED BITES THE BULLET - Implements First Rate Hike in Nearly a ...Dr. Ivo Pezzuto

The US Federal Reserve finally bites the bullet, increasing the

FFR – a key short-term interest rate – by quarter of a per cent.

With this, the regulator has clearly signaled that it might take

similar actions in future, if need arises, to take the economy

towards full recovery.

SandPointe

Investment Perspective

-----------------------------------------------------------------

Roger E. Brinner, PhD

Chief Market Strategist and Co-founding Partner

September 2014

Lower for longer; constructive ambiguity. Chair Powell took pains to paint an image of constructive ambiguity, repeatedly highlighting that the Committee is focused on pursuing policy that is “appropriate” in achieving its dual mandate. The current policy stance is deemed appropriate with current projections achievable via modest policy adjustments (likely -75bps of cuts). Nonetheless, if the economy turns down, “a more extensive sequence of rate cuts is appropriate”. As we argued prior, “it is better to guide for looser policy in an open-ended manner (flattening backwardation of rate cut expectations) rather than encourage front-loading of rate cut expectations”. We think that the Chair has achieved such an outcome, together with “guidance” for an extended pause at a minimum; the best mix of policy, considering circumstances.

We like rates structurally, both on adequate valuations (breakeven levels: 5y, 3.55% (2.98%); and 10y, 3.36% (3.09%)) and as a hedge for risk assets, taking the under on the (largely) priced base case of a smooth 3 year (2018-2020) rate hiking cycle. Based on our macro risk-neutral model and pure expectations, we see 1.80-2.50% and 2.10-2.30% on the UST 5 and 10. Our view is to stay long on the UST 5-10y, prefer 7y; tactical view suggests range trading, 10T around 2.80-3.20%, into 1H19 (Fed hikes by 75bps to 2.75-3.00% by 1H19; anchor extent of rates rally; near term upside risks of a Republican sweep of the mid-terms, providing the President and the Republican Party with another opportunity to pursue even looser (pro-wealth) fiscal policy.

201906 FOMC - An ounce of prevention is worth a pound of cure, unless when th...QuanJianChingCFACAIA

Key drivers will revolve around, i) global trade negotiations/future framework and its implications; ii) contagion from global growth slowdown and weakness in the industrial sector (disruptions to semi-cons, autos, energy sectors; Boeing); and iii) changes, if any, to the Fed’s reaction function. We do not see sufficient evidence of a steep slowdown into an outright recession (though recognize the uncertainties) which markets have broadly priced. The scale of policy guidance and aggressively priced rates markets, we believe, will turn out to be an error. Global financial conditions are rapidly easing, pushing up asset valuations on highly uncertain fundamentals with aggressively dovish pricing limiting future policy room to support markets. Instead of seeking to dampen volatility, it would have been better to realign markets to the Fed’s (strategic) reaction function and allow global markets to find its own levels (via two way volatility).

Tactically, we think that duration is rich and see US5T and US10T closer to 2.30-2.60% into 1H20 (+10-15bps in breakevens; +30-40bps in TP), expecting a bear steepening; preferring rolling the 3 month. Duration-adjusted, prefer front/backend to 2-7 years.

With a backdrop of accommodative policy and our view of generally anchored inflation and resilient growth over coming quarters, we believe that risk/carry will remain supported into 2H19, within the current context (using more binary rather than probabilistic analytical lenses; prolonged clarity over the opportunity cost of risk-free asset amid broadly stable growth/inflation).

Ivo Pezzuto - "FED BITES THE BULLET - Implements First Rate Hike in Nearly a ...Dr. Ivo Pezzuto

The US Federal Reserve finally bites the bullet, increasing the

FFR – a key short-term interest rate – by quarter of a per cent.

With this, the regulator has clearly signaled that it might take

similar actions in future, if need arises, to take the economy

towards full recovery.

SandPointe

Investment Perspective

-----------------------------------------------------------------

Roger E. Brinner, PhD

Chief Market Strategist and Co-founding Partner

September 2014

Inflation targeting in Emerging Market Economies Sarthak Luthra

The presentation represents inflation targeting in EMEs, with a focus on various exchange rate regimes in Asian countries and their susceptibility to financial crisis.

Since the previous meeting of the Monetary Policy Committee (MPC), several risks to the inflation outlook have begun to materialise. While headline inflation is comfortably within the inflation target band, indications are that we have passed the low point of the current cycle. Developments in the international environment have placed upward pressure on the inflation trajectory, while the domestic growth outlook remains challenging.

this presentation is currently have this upload set to Public. This means that it will be indexed by search engines and view able by anyone on the web.

Over the past thirty years the neutral real interest rate across developed economies has declined substantially. Evidence suggests that secular rather than transitory factors are driving its decline. A lower neutral interest rate implies that the cumulative amount of tightening required for monetary policy to become neutral is much smaller than previously thought.

Global Economic Update & Strategic Investment Outlook Q2 2014Cohen and Company

An informative overview of the current state of the global economy and the many factors that impact investment strategies, and a look at domestic economic indicators that may impact them.

Inflation targeting in Emerging Market Economies Sarthak Luthra

The presentation represents inflation targeting in EMEs, with a focus on various exchange rate regimes in Asian countries and their susceptibility to financial crisis.

Since the previous meeting of the Monetary Policy Committee (MPC), several risks to the inflation outlook have begun to materialise. While headline inflation is comfortably within the inflation target band, indications are that we have passed the low point of the current cycle. Developments in the international environment have placed upward pressure on the inflation trajectory, while the domestic growth outlook remains challenging.

this presentation is currently have this upload set to Public. This means that it will be indexed by search engines and view able by anyone on the web.

Over the past thirty years the neutral real interest rate across developed economies has declined substantially. Evidence suggests that secular rather than transitory factors are driving its decline. A lower neutral interest rate implies that the cumulative amount of tightening required for monetary policy to become neutral is much smaller than previously thought.

Global Economic Update & Strategic Investment Outlook Q2 2014Cohen and Company

An informative overview of the current state of the global economy and the many factors that impact investment strategies, and a look at domestic economic indicators that may impact them.

Both domestic consumption (higher debt service and cost of living, slower pace of asset price appreciation, low real income gains) and capital expenditure (higher debt service, elevated current spending vis-à-vis GDP, weakening domestic demand, external uncertainties) is expected to ease off, with the fiscal impulse peaking, financial conditions tightening, and negative impact of prior dollar strength. This should taper labour market gains and keep inflation pressures benign. The extent of slowdown will be dependent upon the resiliency of private sector balance sheet and the subsequent impact on demand. It is imperative that the Fed stays ahead in managing overall debt servicing costs (short-run implications on demand; longer-run may short-circuit the feedback from demand to capital spending and future productivity), and limit the negative impact of policy on overall growth.

We like rates structurally, both on adequate valuations and as a hedge for risk assets, taking the under on the (largely) priced base case of a smooth 3 year (2018-2020) rate hiking cycle.

ABOUT THIS PUBLICATION

This Overview is based on ESADE’s Economic Report, January 2014, produced by the Department of Economics. This article was written by Prof. Josep M. Comajuncosa. The original document was produced with the support of Banc de

Sabadell.

Fitch affirms south africa at 'bb+'; outlook stableSABC News

South Africa's ratings are weighed down by low trend growth, sizeable government debt and contingent liabilities and deteriorating governance standards. These weaknesses are balanced by a favourable government debt structure, deep local capital markets and a flexible exchange rate that helps to absorb external shocks. The affirmation reflects that while a number of developments point to a weaker fiscal outlook and consequent faster pace of debt accumulation, potential fiscal consolidation measures after the ANC's elective conference in December could mitigate those trends. Additionally, GDP growth could recover more strongly than currently anticipated if the outcome of the conference is viewed favourably by consumers and businesses.

Monetary policy is the policy adopted by the authority of a nation to control either the interest rate payable for very short term borrowings or the money supply, often as an attempt to reduce inflation or the interest rate, to ensure price stability and general trust of the value and stability of the nation's currency for every financial year based on the quarter, the new policy is made and executed for the growth of the economy. The RBI carries out the monetary policy through open market tasks, bank rate strategy, reserve system, credit control strategy, moral influence and through numerous different instruments.

In our latest report we provide our assessment of the impact that recent events had on the Greek economy as well as our macroeconomic forecast for the next 2 years

Currently pi network is not tradable on binance or any other exchange because we are still in the enclosed mainnet.

Right now the only way to sell pi coins is by trading with a verified merchant.

What is a pi merchant?

A pi merchant is someone verified by pi network team and allowed to barter pi coins for goods and services.

Since pi network is not doing any pre-sale The only way exchanges like binance/huobi or crypto whales can get pi is by buying from miners. And a merchant stands in between the exchanges and the miners.

I will leave the telegram contact of my personal pi merchant. I and my friends has traded more than 6000pi coins successfully

Tele-gram

@Pi_vendor_247

NO1 Uk Divorce problem uk all amil baba in karachi,lahore,pakistan talaq ka m...Amil Baba Dawood bangali

Contact with Dawood Bhai Just call on +92322-6382012 and we'll help you. We'll solve all your problems within 12 to 24 hours and with 101% guarantee and with astrology systematic. If you want to take any personal or professional advice then also you can call us on +92322-6382012 , ONLINE LOVE PROBLEM & Other all types of Daily Life Problem's.Then CALL or WHATSAPP us on +92322-6382012 and Get all these problems solutions here by Amil Baba DAWOOD BANGALI

#vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore#blackmagicformarriage #aamilbaba #kalajadu #kalailam #taweez #wazifaexpert #jadumantar #vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore #blackmagicforlove #blackmagicformarriage #aamilbaba #kalajadu #kalailam #taweez #wazifaexpert #jadumantar #vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore #Amilbabainuk #amilbabainspain #amilbabaindubai #Amilbabainnorway #amilbabainkrachi #amilbabainlahore #amilbabaingujranwalan #amilbabainislamabad

how to sell pi coins effectively (from 50 - 100k pi)DOT TECH

Anywhere in the world, including Africa, America, and Europe, you can sell Pi Network Coins online and receive cash through online payment options.

Pi has not yet been launched on any exchange because we are currently using the confined Mainnet. The planned launch date for Pi is June 28, 2026.

Reselling to investors who want to hold until the mainnet launch in 2026 is currently the sole way to sell.

Consequently, right now. All you need to do is select the right pi network provider.

Who is a pi merchant?

An individual who buys coins from miners on the pi network and resells them to investors hoping to hang onto them until the mainnet is launched is known as a pi merchant.

debuts.

I'll provide you the Telegram username

@Pi_vendor_247

Falcon stands out as a top-tier P2P Invoice Discounting platform in India, bridging esteemed blue-chip companies and eager investors. Our goal is to transform the investment landscape in India by establishing a comprehensive destination for borrowers and investors with diverse profiles and needs, all while minimizing risk. What sets Falcon apart is the elimination of intermediaries such as commercial banks and depository institutions, allowing investors to enjoy higher yields.

The European Unemployment Puzzle: implications from population agingGRAPE

We study the link between the evolving age structure of the working population and unemployment. We build a large new Keynesian OLG model with a realistic age structure, labor market frictions, sticky prices, and aggregate shocks. Once calibrated to the European economy, we quantify the extent to which demographic changes over the last three decades have contributed to the decline of the unemployment rate. Our findings yield important implications for the future evolution of unemployment given the anticipated further aging of the working population in Europe. We also quantify the implications for optimal monetary policy: lowering inflation volatility becomes less costly in terms of GDP and unemployment volatility, which hints that optimal monetary policy may be more hawkish in an aging society. Finally, our results also propose a partial reversal of the European-US unemployment puzzle due to the fact that the share of young workers is expected to remain robust in the US.

when will pi network coin be available on crypto exchange.DOT TECH

There is no set date for when Pi coins will enter the market.

However, the developers are working hard to get them released as soon as possible.

Once they are available, users will be able to exchange other cryptocurrencies for Pi coins on designated exchanges.

But for now the only way to sell your pi coins is through verified pi vendor.

Here is the telegram contact of my personal pi vendor

@Pi_vendor_247

NO1 Uk Rohani Baba In Karachi Bangali Baba Karachi Online Amil Baba WorldWide...Amil baba

Contact with Dawood Bhai Just call on +92322-6382012 and we'll help you. We'll solve all your problems within 12 to 24 hours and with 101% guarantee and with astrology systematic. If you want to take any personal or professional advice then also you can call us on +92322-6382012 , ONLINE LOVE PROBLEM & Other all types of Daily Life Problem's.Then CALL or WHATSAPP us on +92322-6382012 and Get all these problems solutions here by Amil Baba DAWOOD BANGALI

#vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore#blackmagicformarriage #aamilbaba #kalajadu #kalailam #taweez #wazifaexpert #jadumantar #vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore #blackmagicforlove #blackmagicformarriage #aamilbaba #kalajadu #kalailam #taweez #wazifaexpert #jadumantar #vashikaranspecialist #astrologer #palmistry #amliyaat #taweez #manpasandshadi #horoscope #spiritual #lovelife #lovespell #marriagespell#aamilbabainpakistan #amilbabainkarachi #powerfullblackmagicspell #kalajadumantarspecialist #realamilbaba #AmilbabainPakistan #astrologerincanada #astrologerindubai #lovespellsmaster #kalajaduspecialist #lovespellsthatwork #aamilbabainlahore #Amilbabainuk #amilbabainspain #amilbabaindubai #Amilbabainnorway #amilbabainkrachi #amilbabainlahore #amilbabaingujranwalan #amilbabainislamabad

how can I sell my pi coins for cash in a pi APPDOT TECH

You can't sell your pi coins in the pi network app. because it is not listed yet on any exchange.

The only way you can sell is by trading your pi coins with an investor (a person looking forward to hold massive amounts of pi coins before mainnet launch) .

You don't need to meet the investor directly all the trades are done with a pi vendor/merchant (a person that buys the pi coins from miners and resell it to investors)

I Will leave The telegram contact of my personal pi vendor, if you are finding a legitimate one.

@Pi_vendor_247

#pi network

#pi coins

#money

US Economic Outlook - Being Decided - M Capital Group August 2021.pdfpchutichetpong

The U.S. economy is continuing its impressive recovery from the COVID-19 pandemic and not slowing down despite re-occurring bumps. The U.S. savings rate reached its highest ever recorded level at 34% in April 2020 and Americans seem ready to spend. The sectors that had been hurt the most by the pandemic specifically reduced consumer spending, like retail, leisure, hospitality, and travel, are now experiencing massive growth in revenue and job openings.

Could this growth lead to a “Roaring Twenties”? As quickly as the U.S. economy contracted, experiencing a 9.1% drop in economic output relative to the business cycle in Q2 2020, the largest in recorded history, it has rebounded beyond expectations. This surprising growth seems to be fueled by the U.S. government’s aggressive fiscal and monetary policies, and an increase in consumer spending as mobility restrictions are lifted. Unemployment rates between June 2020 and June 2021 decreased by 5.2%, while the demand for labor is increasing, coupled with increasing wages to incentivize Americans to rejoin the labor force. Schools and businesses are expected to fully reopen soon. In parallel, vaccination rates across the country and the world continue to rise, with full vaccination rates of 50% and 14.8% respectively.

However, it is not completely smooth sailing from here. According to M Capital Group, the main risks that threaten the continued growth of the U.S. economy are inflation, unsettled trade relations, and another wave of Covid-19 mutations that could shut down the world again. Have we learned from the past year of COVID-19 and adapted our economy accordingly?

“In order for the U.S. economy to continue growing, whether there is another wave or not, the U.S. needs to focus on diversifying supply chains, supporting business investment, and maintaining consumer spending,” says Grace Feeley, a research analyst at M Capital Group.

While the economic indicators are positive, the risks are coming closer to manifesting and threatening such growth. The new variants spreading throughout the world, Delta, Lambda, and Gamma, are vaccine-resistant and muddy the predictions made about the economy and health of the country. These variants bring back the feeling of uncertainty that has wreaked havoc not only on the stock market but the mindset of people around the world. MCG provides unique insight on how to mitigate these risks to possibly ensure a bright economic future.

how to sell pi coins in all Africa Countries.DOT TECH

Yes. You can sell your pi network for other cryptocurrencies like Bitcoin, usdt , Ethereum and other currencies And this is done easily with the help from a pi merchant.

What is a pi merchant ?

Since pi is not launched yet in any exchange. The only way you can sell right now is through merchants.

A verified Pi merchant is someone who buys pi network coins from miners and resell them to investors looking forward to hold massive quantities of pi coins before mainnet launch in 2026.

I will leave the telegram contact of my personal pi merchant to trade with.

@Pi_vendor_247

The secret way to sell pi coins effortlessly.DOT TECH

Well as we all know pi isn't launched yet. But you can still sell your pi coins effortlessly because some whales in China are interested in holding massive pi coins. And they are willing to pay good money for it. If you are interested in selling I will leave a contact for you. Just telegram this number below. I sold about 3000 pi coins to him and he paid me immediately.

Telegram: @Pi_vendor_247

how to sell pi coins on Bitmart crypto exchangeDOT TECH

Yes. Pi network coins can be exchanged but not on bitmart exchange. Because pi network is still in the enclosed mainnet. The only way pioneers are able to trade pi coins is by reselling the pi coins to pi verified merchants.

A verified merchant is someone who buys pi network coins and resell it to exchanges looking forward to hold till mainnet launch.

I will leave the telegram contact of my personal pi merchant to trade with.

@Pi_vendor_247

Empowering the Unbanked: The Vital Role of NBFCs in Promoting Financial Inclu...Vighnesh Shashtri

In India, financial inclusion remains a critical challenge, with a significant portion of the population still unbanked. Non-Banking Financial Companies (NBFCs) have emerged as key players in bridging this gap by providing financial services to those often overlooked by traditional banking institutions. This article delves into how NBFCs are fostering financial inclusion and empowering the unbanked.

What price will pi network be listed on exchangesDOT TECH

The rate at which pi will be listed is practically unknown. But due to speculations surrounding it the predicted rate is tends to be from 30$ — 50$.

So if you are interested in selling your pi network coins at a high rate tho. Or you can't wait till the mainnet launch in 2026. You can easily trade your pi coins with a merchant.

A merchant is someone who buys pi coins from miners and resell them to Investors looking forward to hold massive quantities till mainnet launch.

I will leave the telegram contact of my personal pi vendor to trade with.

@Pi_vendor_247

1. FOMC Dec 2018 statement. Highlights (1)

•+25bps to 2.25-2.50%, unanimous. IOER, +20bps to 2.40%; Overnight reverse repo, +25bps to 2.25%.

•Characterisation of economic activities unchanged. Economic activity is seen to be “rising at a strong rate”, household spending “continued to

grow strongly” while growth of business fixed investment has “moderated from its rapid pace earlier”. The labour market has “continued to strengthen”;

job gains have been “strong”, on average, and the unemployment rate remained low.

•Inflation mandate broadly fulfilled. Both headline and core prices remain “near 2%”. Indicators of longer-term inflation expectations are “little

changed”, on balance (inaccurate depiction as 5y5y breakeven inflation have fallen by close to 30bps since Sep). During QnA, the Chair did highlight that

persistent under-shooting of inflation is not desirable and that the Committee have yet declared “victory” (on its inflation mandate) and that (inflation

mandate) “remains to be accomplished”.

•Slight dovish tilt in its judgement monetary policy stance (“judges” rather than “expects”; “some” being a unspecified but

quantifiable pronoun rather than an open-ended “further”). Monetary policy conducted with the objective of sustaining the current

cycle (but still via further tightening). The Committee judges (instead of “expects”) that “some” further gradual increases in the FFR will be

consistent with sustained expansion of economic activity, strong labour market conditions and inflation near the symmetric 2% objective over the

medium term.

2. FOMC Dec 2018 statement. Highlights (2)

•Rising risk aversion, though stance of risk remains unchanged. Risks to the economic outlook are “roughly balanced”. However, the statement

explicitly highlighted that the Committee will continue to monitor “global economic and financial developments and assess their implications for the

economic outlook”.

In the Press Conference Statement, the Chair detailed reasons behind rising Committee risk aversion and the slightly lower economic projections.

Concerns predominantly arise from weaker than expected global growth (though “still solid levels”) and tightening financial conditions that have become

“less supportive” of growth. The gentler path of policy reflects these conditions and the Committee still expect the economy to “perform well” in 2019.

The Chair also highlighted policy is “still” accommodative and that considering the state of the economy, policy “does not need to be accommodative” and

can move to “neutral”.

The Committee is cognizant of the differing economic context for 2019 vis-a-via 2018, highlighting a moderating (rather than accelerating) growth

trajectory, less accommodative monetary policy amid weaker external growth and tighter financial conditions. Data dependency will be the key

determinant in policy-setting, considering that the spot FFR’s position (following prior hikes) vis-à-vis the “true” neutral is highly uncertain. Essentially a

high degree of uncertainty to policy-making.

•Data dependency. In determining the timing and size of adjustments to the FFR, realized and expected economic conditions will be assessed relative

to the i) maximum employment objective and ii) symmetric 2% inflation target. The Committee will take into account a wide range of information

including labour market conditions, inflation pressures and expectations, and readings on financial and international developments.

3. FOMC Dec 2018 statement. Highlights (3)

•Cosmetic changes made to economic projections; tilted slightly lower. Median growth rates was lowered for 2019 by 20bps to 2.3%,

unchanged for 2020-2021 at 2.0% and 1.8% respectively; longer run growth estimates higher by 10bps to 1.9%. No secular uplift to potential from fiscal

spending were deemed by the Fed. Unemployment rates barely moved, unchanged at 3.5% for 2019; higher by 10bps for both 2020-2021; longer-run

seen lower by 10bps at 4.4%. Core inflation projections was lowered by 10bps for 2019-2021, all at 2.0%.

•Slight dovish change to Fed path; lower terminal (3.125%) and neutral (2.75%). Dec’s Fed’s median expectations, 2019 = 2.875% (from

3.125%; 6:5:6; 11/17=<Median); 2020 = 3.125% (from 3.375%; 8:4:5; 12/17=<Median); 2021 = 3.125% (from 3.375%; 8:6:3; 14/17=<Median) and longer

run = 2.75% (from 3.00%; 4:5:7; 9/16=<Median). This suggests 2-1-0 hikes from 2019-2021, following by 2 rate cuts in the longer-run; monetary policy

will be slightly “tight” between 2019-2021. Longer-run projection (neutral) is anchored around 2.75-3.00%.

The average FOMC, on the whole, too reflects the median changes. Dec’s Fed’s average expectations, 2019 = 2.9% (-17bps); 2020 = 3.1% (-22bps); 2021 =

3.0% (-23bps); and longer run = 2.8% (-4bps).

•Balance sheet policy on auto-pilot. High hurdle to changes being made to balance sheet policy with the Chair highlighting the primacy of interest

rate policy.

•On financial conditions. The Committee will take “on-board” “sustained” tightening in financial conditions insofar as such changes impact upon its

economic forecasts (as per Dec’s forecasts) and hence moved to a gentler path for policy hikes.

5. Thoughts (1)

Model-driven policy-making. Monetary policy, as expected, followed Fed guidance with a hike in Dec. The Fed now anticipates a shallower upward

rate path, reflecting tighter financial conditions and weaker external growth. However, there were no sign of any intention to re-introduce uncertainty

into the trajectory of the Fed path, despite a sharp downturn in financial conditions (close to -1.75 stdev move peak-to-trough). This likely reflects a mix

of model-based policy-making and policy stance inertia, considering current levels of employment/inflation (with both mandates deemed broadly met)

coupled with prior belief that policy, going forward, should be conducted with the objective of sustaining the cycle via further tightening. Hence, based on

economic trajectory and policy inertia, the Fed may continue to tighten policy in 1H19 (+50bps to 2.50-3.00%).

Based on Fed’s projections, the risk-neutral fair value of the US5T and US10T is at 2.95% and 2.85%. Our internal models based on Fed’s 2019 nominal

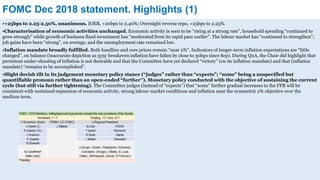

GDP (4.2%) points to US5T and US10T FV at 1.97% and 2.30%. Marking-to-market the better growth/inflation outlook and rolling prior rate hikes, YTD,

the UST curve shifted higher with the curve up by 30-116bps with a flattening bias.

Too blunt? Just-in-time policy-making may not be in time? We think that will be a mistake, with a Fed relent at this juncture key in extending

the cycle, considering the prior goal of tightening financial conditions have been met via the turn in markets (which reflects the impossibility for central

bankers to manage/time the impact of monetary policy adjustments on financial conditions reflecting inherent complexities of markets). Instead of

having to hike till the economic cycle breaks before stroking a turn in the financial cycle, the sharp tightening in financial markets sets up an unique

opportunity for the Fed pause to extend the economic cycle. Data dependency, at this juncture, may be too late and blunt, forcing a sharper tightening of

global financial conditions amid an environment of heightened concerns over risks in China, global growth, and domestic and global political

uncertainties. The median Fed is projecting a further +50bps increase in 2019 (2.75-3.00%), +25bps increase in 2020 (3.00-3.25%) and then a pause in

2021.

6. Thoughts (2)

Fed must relent. Our expectations now is for a state dependent (global financial conditions to stabilise, cushion rising debt repayment burden and

allowing domestic leverage to level off, coupled with still moderate economic growth/inflation, policy options to widen positively globally, especially in

China) Fed relent with scope for a final 25-50bps, if any (pause otherwise), in late 2019/2020, should the cycle extents, with the FFR hitting cycle

terminal at 2.75-3.00%. The Fed needs to stabilise and lower real risk neutral to a level that market perceived as being adequate to

avoid risks of a policy error – essentially flattening risk-neutral while inducing breakevens and term premiums to rise – a curve

steepener. As argued, we expect both domestic consumption (higher debt service, slower pace of asset price appreciation, low real income gains) and

capital expenditure (higher debt service, elevated current spending vis-à-vis GDP, weakening domestic demand, external uncertainties) to ease off, with

the fiscal impulse peaking, financial conditions tightening, and impact of dollar strength. This should taper labour market gains and keep inflation

pressures benign. The extent of slowdown will be dependent upon the resiliency of private sector balance sheet and the subsequent impact on demand. It

is imperative that the Fed stays ahead in managing overall debt servicing costs (short-run implications on demand; longer-run may short-circuit the

feedback from demand to capital spending and future productivity), and limit the negative impact of policy on overall growth.

-0.5

0.0

0.5

1.0

1.5

2.0

Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18

% 5Yr Implied Real Rate 10Yr Implied Real Rate

-12 -9

-33 -15

91

5946

34

-60

-40

-20

0

20

40

60

80

100

5Y 10Y

2018, bps chng TP Breakevens Implied Real Rate Nominal

0

1

2

3

4

5

6

1Q62 1Q68 1Q74 1Q80 1Q86 1Q92 1Q98 1Q04 1Q10 1Q16

% Laubach-Williams Real Neutral Interest Rate

7. USTs, Scenarios (1)

1. All is well. As per guidance, the Committee will continue hiking insofar as the labour market remains robust (unemployment stable/falling), inflation

near/above target, growth stable, coupled with stabilising financial markets and a balanced risk profile. This will enable the Fed to sustain the

expansion, by getting ahead of the labour market under-shoot, sustaining/containing inflation, before moving back towards neutral with growth at

target. End of cycle is likely to be caused by a build-up of fundamental fragility with time, leading to a break in the economic equilibrium. This

scenario assumes certain degree of macro-economic resiliency, provide scope for productivity improvements, and anchored inflation expectations.

This is probably the Fed’s dream scenario (balancing the need to be reactive vis-à-vis pre-emptive). Rates should predominantly be driven by stable

risk neutral (no policy error, ex-post), rising break-evens and higher (but anchored) term premiums; 5T and 10T near Fed’s risk-neutral of 2.95%

and 2.85%. Scope for transition into curve steepening with higher long rates on realisation of higher productivity, pushing real potential growth and

real neutral rate higher (front end pushing long end higher, subsequently, long end dragging short end higher; economic cycle extended).

2. Fed behind the curve. The Fed lose control of the labour market, unable to rein in the under-shoot, leading to higher wages with no productivity

offset, margin compression and partial pass through to higher inflation. Term premium rises on a Fed that is deemed behind the curve. Fed guide for

even higher rates, pushing risk neutral higher, in order to anchor term premiums, inverting the curve on a higher perceived terminal but still low

neutral; curve steepener to curve flattener with low real neutral – long rates can trade substantially wider, >3.50% - depending on magnitude of

imbalance, Fed’s subsequent reaction and perceived loss and recovery in policy credibility - but should remain bounded; short end can rise

substantially. The combination of high terminal and low neutral will have a significant adverse impact on risk markets.

3. Fed policy error. The Fed continues to hike without due consideration to domestic/global financial conditions, triggering feed-back loops which

break the cycle. Debt sustainability issues reach critical/breaking points, weakening demand and triggering re-financing uncertainties, ending with a

global recession. A world deprived of US demand and facing dire domestic policy options leads to a sharp global downturn, financial market turmoil,

and likely adverse political instability repercussions. Curve will collapse with rates, with time, trading near zero, in a likely deflationary bust.

8. USTs, Scenarios (2)

4. Structural changes starts to bind; no escape velocity. Growth and inflation starts to taper off as i) boost from the fiscal stimulus fades; ii) prior

monetary tightening starts to bite; and iii) the downward pull from unresolved US (credit, wealth-driven economy; skewed labour/capital share) and

global imbalances (Euro-zone fragmentation, internal balance; China de-leveraging, re-structuring; EM stresses). This should be reflected in a peak

in growth and inflation soon, coupled with a slowdown in labour gains as demand weakens. The Fed should pause/reverse the tightening cycle, in

order to lower short rates to anchor longer-run risk neutral and term premiums. 5T and 10T should ease and re-anchor at a new perceived neutral

and terminal (<2.50%). High valuations of markets will ensure that risk markets perform poorly on the turn in the cycle; narrative of omnipotent

central banks will be tested, considering that monetary policy will have limited traction on growth outcomes, going forward (wealth/debt-driven

consumption/investment via credit/portfolio re-balancing/signalling limited by debt-servicing/asset valuations – defaults/sell-off required first;

broken monetary models); fiscal, FX, reforms will be required as policy tools (no global equilibrium).

9. USTs, Views (1)

Markets have switched to trading on an less grim variant of scenario 3; having priced scenario 1 for most of 2018. Rates markets are

priced for a Fed that is on hold for 2019 and then a cut and hold for 2020 and 2021 with a neutral around 2.5%; a dovish outcome vis-à-vis the Fed. YTD

higher 10T (+34bps) is wholly driven by higher implied real growth with markets re-pricing real risk neutral higher to 1.6-1.7% (Fed forward estimate

approx. 0.75-1.00%; nominal GDP assumption around 3.9%; PCE at 2.0%) while break-evens and term premiums fall; suggesting market

perceptions of Fed over-tightening. Key drivers will revolve around, i) global growth trajectory (especially over China’s growth uncertainties;

political event risks), ii) extent of US growth/inflation momentum moderation via-a-vis Fed’s outlook, and iii) markets’ perception of i) and ii), its

subsequent impact on financial conditions, and the feed-back to Fed policy and rates.

Our base case remains 4, with 3 a clear downside risk. We like rates structurally and as a hedge for risk assets. Based on our risk-neutral model, we see

1.80-2.50% and 2.10-2.30% on the UST 5 and 10. We are, however, positioned for a Fed relent, likely soon in 1Q19, and am neutral duration with a

preference for steepeners. Our view is to stay long on the UST 5-10y, still prefer 7y; tactical view suggests likely further flattening until a relent with a flat

curve, 10T anchored around 2.75%, into 1H19. Risk neutral need to re-price lower with real risk-neutral 5y5y at close to 1.6-1.7%.

We maintain that private sector debt loads remain too high to withstand sustained higher interest rates. We believe that current growth drivers are

cyclical (fiscal policy will have a transitory impact on the economy via demand channels with spending targeted at wrong segments of the economy), not

structural, and that latent secular dis-inflation impulses remains. To repeat, certain factors underlying the US (and global) economy seems highly

persistent, a structural reflection of the current global growth model/political paradigm/broken models everywhere; Phillips curve (lower cost labour

driven growth; no productivity); r* on consumption and investment and thus not transient (non-linear, easing have limited impact/tightening massive);

a lack of substance in global re-balancing; rise in oligarchy); continued dependence on orthodox global central bank policy put – continues to suggest that

one can ultimately position for the scenario of a shortened rate hiking cycle as limits are reached once cyclical strength fades. We maintain our view of a

neutral no >2.5%.