Download to read offline

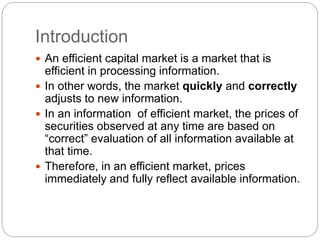

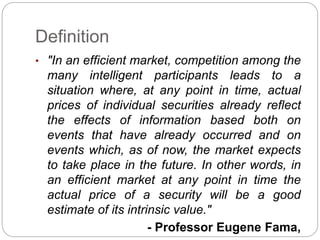

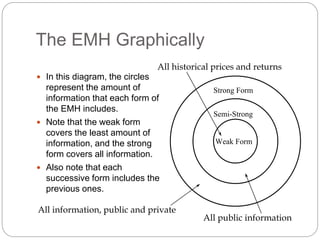

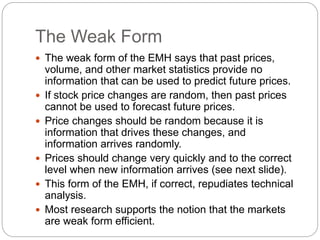

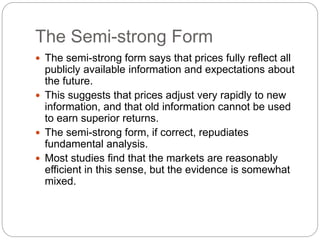

The document discusses the efficient market hypothesis (EMH), which states that market prices fully reflect all available public information and adjust quickly to new information. The EMH has three forms - weak, semi-strong, and strong. The weak form suggests past prices cannot predict future prices, while the semi-strong form suggests fundamental analysis cannot beat the market. The strong form believes even insider information cannot provide advantages. Most research supports the weak and semi-strong forms, showing technical and fundamental analysis are unlikely to consistently outperform the overall market.