This document provides an overview and outline of a finance course for non-finance professionals. The summary includes:

- The course is aimed at professionals without financial backgrounds like doctors, engineers, and managers to teach them basic finance concepts.

- The outline covers why financial education is important, definitions of accounting, the accounting equation, examples of accounting transactions, financial statements, and the three main financial decisions around investments, financing, and dividends.

- Key concepts defined include assets, liabilities, revenues, expenses, accounting, the accounting equation, double-entry accounting, balance sheets, income statements, and the three main types of business entities.

The document outlines the steps for completing incomplete accounting records:

1) Prepare an opening statement of affairs with headings like assets, liabilities, capital.

2) Set up control accounts for debtors, creditors, cash, and the bank account.

3) Insert available figures and calculate any missing values, like gross profit or fixed assets.

4) Draft the required statements, including profit and loss, balance sheet.

This document discusses accounting concepts related to types of accounts, transactions, and journal entries. It covers the four main types of accounts - assets, liabilities, income, and expenses. It also discusses the differences between capital and revenue expenditures, and how to classify transactions as affecting personal, real, or nominal accounts. The document provides examples of journal entries and explains the rules for debiting and crediting different types of accounts.

This document provides information to prepare final accounts with adjustments for Ravinder, including:

1. The Trial Balance is given for Ravinder with various account balances.

2. Additional adjustments are provided, including manager's commission calculated as 10% of net profits before commission.

3. Interest on a 12% loan taken on July 1, 1987 is to be calculated and any outstanding amount adjusted.

4. Goods worth Rs. 1,500 taken by the proprietor for personal use requires an adjustment.

The student is to prepare the Trading and Profit & Loss Account, Balance Sheet, and make the necessary adjustments based on the Trial Balance and additional information given.

This document outlines areas that should be covered in an internal audit of a manufacturing company. It discusses 12 key areas: purchases, sales, creditors, debtors, subcontracting, inventory, export incentives, price escalation, cash management, payroll, labor contractors, and a review of management information systems and internal controls. The goal is to evaluate financial records, internal processes, and risks to help management ensure efficiency, effectiveness and compliance.

This document provides an overview and outline of a finance course for non-finance professionals. The summary includes:

- The course is aimed at professionals without financial backgrounds like doctors, engineers, and managers to teach them basic finance concepts.

- The outline covers why financial education is important, definitions of accounting, the accounting equation, examples of accounting transactions, financial statements, and the three main financial decisions around investments, financing, and dividends.

- Key concepts defined include assets, liabilities, revenues, expenses, accounting, the accounting equation, double-entry accounting, balance sheets, income statements, and the three main types of business entities.

The document outlines the steps for completing incomplete accounting records:

1) Prepare an opening statement of affairs with headings like assets, liabilities, capital.

2) Set up control accounts for debtors, creditors, cash, and the bank account.

3) Insert available figures and calculate any missing values, like gross profit or fixed assets.

4) Draft the required statements, including profit and loss, balance sheet.

This document discusses accounting concepts related to types of accounts, transactions, and journal entries. It covers the four main types of accounts - assets, liabilities, income, and expenses. It also discusses the differences between capital and revenue expenditures, and how to classify transactions as affecting personal, real, or nominal accounts. The document provides examples of journal entries and explains the rules for debiting and crediting different types of accounts.

This document provides information to prepare final accounts with adjustments for Ravinder, including:

1. The Trial Balance is given for Ravinder with various account balances.

2. Additional adjustments are provided, including manager's commission calculated as 10% of net profits before commission.

3. Interest on a 12% loan taken on July 1, 1987 is to be calculated and any outstanding amount adjusted.

4. Goods worth Rs. 1,500 taken by the proprietor for personal use requires an adjustment.

The student is to prepare the Trading and Profit & Loss Account, Balance Sheet, and make the necessary adjustments based on the Trial Balance and additional information given.

This document outlines areas that should be covered in an internal audit of a manufacturing company. It discusses 12 key areas: purchases, sales, creditors, debtors, subcontracting, inventory, export incentives, price escalation, cash management, payroll, labor contractors, and a review of management information systems and internal controls. The goal is to evaluate financial records, internal processes, and risks to help management ensure efficiency, effectiveness and compliance.

Vouching involves examining documentary evidence to verify transactions recorded in accounting books. It establishes the accuracy and authenticity of entries.

Some key aspects of vouching include checking that vouchers are numbered and cancelled, examining high risk transactions like those with owners, and verifying dates, amounts, and names match the cash book. The auditor must also consider the nature of payments.

Vouching is important as it forms the basis for further audit work and fulfills the purpose of checking entries. It helps ensure transactions are valid, correctly recorded, and supported by evidence. This detects errors and potential fraud.

La conciliación bancaria compara las transacciones registradas en el estado de cuenta bancario con los movimientos en los libros de la empresa mensualmente. Incluye información de la contabilidad y permite conciliar automáticamente usando números de referencia. Se usan métodos como cuatro columnas o saldos correctos para identificar diferencias entre los saldos iniciales, cheques en tránsito, depósitos pendientes, errores y saldos finales.

Unit 6 International Accounting Standard on Foreign Transactions (IAS 21)Charu Rastogi

This presentations discusses International Accounting Standard on Foreign Transactions (IAS 21). Important definitions, functional currency, initial recognition, subsequent measurement & recognition of exchange difference at initial stage and use of temporal and net investment method at the time of consolidation of financial statements are covered.

Show the appropriate adjusting entries at the end of

accounting period.

Rental earned (Oct & Nov 2005) : 2 months x RM200 = RM400

Rental received in advance (Jan 2006) : 1 month x RM200 = RM200

This document defines and explains the bank reconciliation statement. [1] It reconciles the differences between the bank balance shown in a business's cash book and the balance in their bank statement or passbook. [2] Common causes of differences include outstanding checks and deposits, as well as bank charges and interest that have been applied. [3] Preparing the reconciliation statement regularly helps ensure accurate accounting records and identifies potential errors or fraud.

The cash flow statement summarizes the cash inflows and outflows for A Ltd. for the year ended March 31, 2012. It shows that cash from operating activities was Rs. 40,000, which was primarily from net profit adjusted for depreciation. Cash used in investing activities was Rs. Nil. Cash from financing activities was Rs. Nil as bank loan repayment was offset by dividend payment. Overall, cash and cash equivalents increased by Rs. 8,000 to Rs. 30,000.

Este documento resume las transacciones contables del Gobierno Autónomo Descentralizado Parroquial de Muyuna entre el 1 de enero y el 31 de agosto de 2013. Comenzó sus operaciones el 1 de enero con $3,718.05 en bancos y patrimonio. A lo largo del período registró ingresos, gastos en servicios públicos, nómina, suministros y proyectos de infraestructura.

The document defines key terms related to a cash flow statement such as cash flows, cash equivalents, and the three categories of cash flows - operating, investing, and financing activities. It explains that the cash flow statement classifies cash inflows and outflows according to these three activities. The objectives are to determine the sources and uses of cash from each activity. The document also provides examples of cash inflows and outflows that would be included in each of the three activities.

This document discusses IAS 2 on inventories, including definitions of inventory, measurement of cost, and specific inventory issues for service providers and deferred settlement terms. It provides guidance on what constitutes inventory, what costs should be included in inventory cost, treatment of work-in-progress for service providers, and how to account for deferred settlement terms with different customers.

Consolidated financial statement in acquisitions at book valueArthik Davianti

This document discusses one-line consolidation and equity method accounting. It provides an example of a parent company, Payne Co, purchasing 30% of another company, Sloan Co, for cash and shares. It also discusses situations where the investment cost is equal to, greater than, or less than the book value of the subsidiary's net assets when a parent acquires a subsidiary. Worksheets are provided to consolidate the financial statements in each situation at the date of acquisition and for subsequent periods. Key consolidation concepts like noncontrolling interest are also explained.

The document discusses bank reconciliation, which is the process of ensuring the bank statement balance matches the business's records. It explains items that may appear in only one record like deposits not cleared. The purpose is to identify and correct discrepancies by preparing a bank reconciliation statement that lists unpresented checks, uncredited deposits, and other adjustments to calculate the correct balance. Instructions are provided on updating records, identifying reconciling items, and preparing the final reconciliation statement to match the business and bank records.

Vouching involves testing the accuracy of transactions recorded in accounting books by examining supporting documentation. It helps auditors ensure transactions are valid, all entries are supported, and nothing has been omitted or misrecorded. Key aspects auditors examine when vouching cash receipts include cash sales records, bank deposit slips, and reconciling receipts to entries in cash books and bank statements. This helps auditors verify revenues have been completely and properly recorded.

The document discusses revenue recognition standards. It defines revenue as income from ordinary business activities like sales, fees, interest and dividends. Revenue is recognized when earned and realized/realizable, such as when goods/services are exchanged for cash. For long-term contracts, revenue can be recognized using percentage-of-completion or completed contract methods depending on certainty of costs and contract terms.

Accounting

9706

Cambridge A Level (9706)

Financial Accounting

Consignment Accounts

Consignor

Consignee

Commission

Valuation of closing inventory with the agent

Del Credere Agent

Del Credere Commission

Steps in preparing accounts in the books of coonsignor

O documento discute os aspectos contábeis dos lucros ou prejuízos acumulados. O saldo líquido da demonstração de resultado é transferido para a conta "Lucros ou Prejuízos Acumulados" no patrimônio líquido. Esta conta pode receber lançamentos relativos a resultados, ajustes de exercícios anteriores, reversões de reservas e transferências para reservas.

1) The accounting equation shows that a company's assets are always equal to its liabilities plus equity.

2) Double entry accounting requires every transaction to have equal debits and credits so the accounting equation remains balanced.

3) Examples of transactions that affect the accounting equation include purchasing inventory, receiving payment from customers, and paying expenses.

La conciliación bancaria compara los registros de la empresa con el estado de cuenta del banco para determinar el saldo correcto. Se presentan diferencias por depósitos y cheques en tránsito, así como errores. El documento explica los métodos de saldos correctos y encontrados para elaborar la conciliación mediante ajustes contables.

Preparation of financial statements using incomplete recordsSheham Aliyar

This document discusses techniques for preparing financial statements using incomplete records, including constructing opening and closing balance sheets to calculate profit or loss based on changes in capital amounts. It provides examples of using cash/bank summaries to calculate missing sales or purchase amounts, constructing control accounts to calculate missing sales figures, and using gross/net profit percentages to calculate missing costs, sales, or stock amounts from available data. The examples walk through calculations of profit, closing stock, and preparing statements of profit or loss based on incomplete records about assets, liabilities, capital introduced or withdrawn, and gross profit percentages.

This document provides an overview of IAS 2 on inventory. It discusses the objective and scope of IAS 2, which is to prescribe the accounting treatment for inventory. Key areas covered include measurement of inventory at the lower of cost or net realizable value, techniques for determining cost, and required disclosures. Measurement of inventory requires identifying applicable costs and allocating fixed and variable production overheads. Inventory is recognized as an expense when the related revenue is recognized.

This document discusses key accounting concepts related to accrual basis accounting, adjusting entries, and accounting for various transactions through journal entries. It defines accrual basis and cash basis accounting. It explains that adjusting entries are made at the end of an accounting period to properly state accounts and recognize revenues and expenses according to the matching principle. Various types of adjusting entries are described for expenses/revenues due or received, prepaid/deferred items, closing stock, depreciation, bad debts, and more. Examples of adjusting entries for specific transactions are provided.

Vouching involves examining documentary evidence to verify transactions recorded in accounting books. It establishes the accuracy and authenticity of entries.

Some key aspects of vouching include checking that vouchers are numbered and cancelled, examining high risk transactions like those with owners, and verifying dates, amounts, and names match the cash book. The auditor must also consider the nature of payments.

Vouching is important as it forms the basis for further audit work and fulfills the purpose of checking entries. It helps ensure transactions are valid, correctly recorded, and supported by evidence. This detects errors and potential fraud.

La conciliación bancaria compara las transacciones registradas en el estado de cuenta bancario con los movimientos en los libros de la empresa mensualmente. Incluye información de la contabilidad y permite conciliar automáticamente usando números de referencia. Se usan métodos como cuatro columnas o saldos correctos para identificar diferencias entre los saldos iniciales, cheques en tránsito, depósitos pendientes, errores y saldos finales.

Unit 6 International Accounting Standard on Foreign Transactions (IAS 21)Charu Rastogi

This presentations discusses International Accounting Standard on Foreign Transactions (IAS 21). Important definitions, functional currency, initial recognition, subsequent measurement & recognition of exchange difference at initial stage and use of temporal and net investment method at the time of consolidation of financial statements are covered.

Show the appropriate adjusting entries at the end of

accounting period.

Rental earned (Oct & Nov 2005) : 2 months x RM200 = RM400

Rental received in advance (Jan 2006) : 1 month x RM200 = RM200

This document defines and explains the bank reconciliation statement. [1] It reconciles the differences between the bank balance shown in a business's cash book and the balance in their bank statement or passbook. [2] Common causes of differences include outstanding checks and deposits, as well as bank charges and interest that have been applied. [3] Preparing the reconciliation statement regularly helps ensure accurate accounting records and identifies potential errors or fraud.

The cash flow statement summarizes the cash inflows and outflows for A Ltd. for the year ended March 31, 2012. It shows that cash from operating activities was Rs. 40,000, which was primarily from net profit adjusted for depreciation. Cash used in investing activities was Rs. Nil. Cash from financing activities was Rs. Nil as bank loan repayment was offset by dividend payment. Overall, cash and cash equivalents increased by Rs. 8,000 to Rs. 30,000.

Este documento resume las transacciones contables del Gobierno Autónomo Descentralizado Parroquial de Muyuna entre el 1 de enero y el 31 de agosto de 2013. Comenzó sus operaciones el 1 de enero con $3,718.05 en bancos y patrimonio. A lo largo del período registró ingresos, gastos en servicios públicos, nómina, suministros y proyectos de infraestructura.

The document defines key terms related to a cash flow statement such as cash flows, cash equivalents, and the three categories of cash flows - operating, investing, and financing activities. It explains that the cash flow statement classifies cash inflows and outflows according to these three activities. The objectives are to determine the sources and uses of cash from each activity. The document also provides examples of cash inflows and outflows that would be included in each of the three activities.

This document discusses IAS 2 on inventories, including definitions of inventory, measurement of cost, and specific inventory issues for service providers and deferred settlement terms. It provides guidance on what constitutes inventory, what costs should be included in inventory cost, treatment of work-in-progress for service providers, and how to account for deferred settlement terms with different customers.

Consolidated financial statement in acquisitions at book valueArthik Davianti

This document discusses one-line consolidation and equity method accounting. It provides an example of a parent company, Payne Co, purchasing 30% of another company, Sloan Co, for cash and shares. It also discusses situations where the investment cost is equal to, greater than, or less than the book value of the subsidiary's net assets when a parent acquires a subsidiary. Worksheets are provided to consolidate the financial statements in each situation at the date of acquisition and for subsequent periods. Key consolidation concepts like noncontrolling interest are also explained.

The document discusses bank reconciliation, which is the process of ensuring the bank statement balance matches the business's records. It explains items that may appear in only one record like deposits not cleared. The purpose is to identify and correct discrepancies by preparing a bank reconciliation statement that lists unpresented checks, uncredited deposits, and other adjustments to calculate the correct balance. Instructions are provided on updating records, identifying reconciling items, and preparing the final reconciliation statement to match the business and bank records.

Vouching involves testing the accuracy of transactions recorded in accounting books by examining supporting documentation. It helps auditors ensure transactions are valid, all entries are supported, and nothing has been omitted or misrecorded. Key aspects auditors examine when vouching cash receipts include cash sales records, bank deposit slips, and reconciling receipts to entries in cash books and bank statements. This helps auditors verify revenues have been completely and properly recorded.

The document discusses revenue recognition standards. It defines revenue as income from ordinary business activities like sales, fees, interest and dividends. Revenue is recognized when earned and realized/realizable, such as when goods/services are exchanged for cash. For long-term contracts, revenue can be recognized using percentage-of-completion or completed contract methods depending on certainty of costs and contract terms.

Accounting

9706

Cambridge A Level (9706)

Financial Accounting

Consignment Accounts

Consignor

Consignee

Commission

Valuation of closing inventory with the agent

Del Credere Agent

Del Credere Commission

Steps in preparing accounts in the books of coonsignor

O documento discute os aspectos contábeis dos lucros ou prejuízos acumulados. O saldo líquido da demonstração de resultado é transferido para a conta "Lucros ou Prejuízos Acumulados" no patrimônio líquido. Esta conta pode receber lançamentos relativos a resultados, ajustes de exercícios anteriores, reversões de reservas e transferências para reservas.

1) The accounting equation shows that a company's assets are always equal to its liabilities plus equity.

2) Double entry accounting requires every transaction to have equal debits and credits so the accounting equation remains balanced.

3) Examples of transactions that affect the accounting equation include purchasing inventory, receiving payment from customers, and paying expenses.

La conciliación bancaria compara los registros de la empresa con el estado de cuenta del banco para determinar el saldo correcto. Se presentan diferencias por depósitos y cheques en tránsito, así como errores. El documento explica los métodos de saldos correctos y encontrados para elaborar la conciliación mediante ajustes contables.

Preparation of financial statements using incomplete recordsSheham Aliyar

This document discusses techniques for preparing financial statements using incomplete records, including constructing opening and closing balance sheets to calculate profit or loss based on changes in capital amounts. It provides examples of using cash/bank summaries to calculate missing sales or purchase amounts, constructing control accounts to calculate missing sales figures, and using gross/net profit percentages to calculate missing costs, sales, or stock amounts from available data. The examples walk through calculations of profit, closing stock, and preparing statements of profit or loss based on incomplete records about assets, liabilities, capital introduced or withdrawn, and gross profit percentages.

This document provides an overview of IAS 2 on inventory. It discusses the objective and scope of IAS 2, which is to prescribe the accounting treatment for inventory. Key areas covered include measurement of inventory at the lower of cost or net realizable value, techniques for determining cost, and required disclosures. Measurement of inventory requires identifying applicable costs and allocating fixed and variable production overheads. Inventory is recognized as an expense when the related revenue is recognized.

This document discusses key accounting concepts related to accrual basis accounting, adjusting entries, and accounting for various transactions through journal entries. It defines accrual basis and cash basis accounting. It explains that adjusting entries are made at the end of an accounting period to properly state accounts and recognize revenues and expenses according to the matching principle. Various types of adjusting entries are described for expenses/revenues due or received, prepaid/deferred items, closing stock, depreciation, bad debts, and more. Examples of adjusting entries for specific transactions are provided.

Transition Management of Product as PlatformTiket.com

This document discusses transitioning a monolithic technology system to microservices as well as transitioning to a product as a platform model. It notes that as technology systems and businesses grow, scalability becomes more strategic. Transitioning requires organizational culture change, aligning product roadmaps and architectures, and using a strangler pattern where a new system is built around the edges of the old one over several years until the old system is replaced.

Mali Tablo ve Analizi

Devlet Muhasebesinin Gelişimi

Kamu Kurumları Mali Tabloları

Sayıştayca Yapılacak Mali Tablo Denetimi

Mali Tablolarının Analizi

5.1. Teorik Rasyolar

5.2. Mali Oranlar

5.3. İdari Rasyolar

5.4. Yasal Rasyolar

5.5. Uluslararası Rasyolar

The document discusses key accounting concepts such as debits and credits, T-accounts, the general journal, posting journal entries to ledger accounts, and preparing a trial balance. It provides examples of analyzing business transactions and recording debits and credits to the appropriate accounts. It also explains how a trial balance is used to prove the equality of total debits and credits after journal entries have been posted to ledger accounts.

Yağmur Öğretim Teknolojileri ve Materyal TasarımıYağmur Usta

University education offers many opportunities for personal and intellectual growth. It allows students to develop their talents and abilities while preparing for their future careers. The academic, social, and international aspects of university combine to provide "windows of opportunity" through which students can gain a global perspective and expand their cultural understanding. Universities offer activities, facilities, and a sense of community to enhance students' experiences. The friendships formed during this time are often the most memorable part and can cultivate close relationships with other students and staff. Overall, a university education gives students tools to discover themselves and refine who they are through scholarly pursuits.

Bi̇lanço okuma tekni̇kleri̇ ve makyajlanmiş mali̇ tablolarin tespi̇ti̇DERYA KALE ERDEMLİ

Finansal raporlar ve finansal tabloların bilinmesi, analizlerinin doğru yapılarak yorumlanabilmesi, sürdürülebilir büyüme için önemli kriterlerdendir. Bu eğitimde işletmelerde kredi kullanma kararı veren, finans kuruluşlarıyla müzakereleri yürüten, finans, pazarlama veya iş geliştirmeden sorumlu uzman ve yöneticilerin finansal tabloları analiz edebilme ve karar alabilme yetilerinin geliştirilmesi hedeflenmektedir. Ayrıca mali müşavirlerin, müşterilerinin ya da çalıştıkları kurumun durumu hakkında yeterli analiz yapabilmesi ve doğru ve zamanında yönlendirebilmeleri amaçlanmaktadır.

Genel muhasebe için ayrıntılı ve hızlı kavramaya yönelik örnekli adım adım konu anlatımı.Gerçekten çok açık ve net. Muhasebe düşünce yapısını bir türlü kavrayamıyorum diyenler için.

Mali Tablolar Analizi - Yataş Yatak ve Yorgan San. Tic. A.Ş.Gamze Saba

Yataş Yatak ve Yorgan San. Tic. A.Ş’nin 1 Ocak-31 Aralık 2010 ve 1 Ocak-31 Aralık 2011 yılları arasındaki bilanço, gelir tablosu, dikey yüzde ve oran analizlerini içeren yorumlar.

fethiye web tasarım ekibi olarak buradan saçma bir backlink alıp deneme yapmak istedik bakalım ne kadar faydalı olacak https://www.fethiyewebtasarim.com

iin aadaki ilemler gerekleti:

LeroyLeroy

Mhendislik:

YKLENYOR...

(lemleri grntlemek iin ikona tklayn.)

lemleri gnle kaydetmek

LeroyLeroy

Mhendislik. Her gnlk girdisine bir aklama ekleyin. Aadaki hesaplar kullann: Nakit; Alacak Hesaplar;

Ofis Malzemeleri; Tehizat; Alacak Hesaplar; Bor Senetleri; Hisse Senedi; Temettler; Hizmet Geliri;

Kamu Hizmetleri Gideri. (nce borlar, ardndan alacaklar kaydedin. Yevmiye kayd tablosunun son

satrndaki aklamay sein.)

2: Alnd

17$ virgl 000$17.000$

katks

John Leroy John Leroy

adi hisse senedi karlnda.

Tarih

Hesaplar ve Aklama

bor

Kredi

2 Temmuz

TemmuzTemmuz

4: denen kamu hizmetleri gideri

390$390$.

Tarih

Hesaplar ve Aklama

bor

Kredi

4 Temmuz

TemmuzTemmuz

5: Hesaba satn alnan ekipman,

2 $ virgl 600 $2,600.

Tarih

Hesaplar ve Aklama

bor

Kredi

5 Temmuz

TemmuzTemmuz

10: Mteri hesabna verilen hizmetler,

2 $ virgl 900 $2,900.

Tarih

Hesaplar ve Aklama

bor

Kredi

10 Temmuz

TemmuzTemmuz

12: dn alnd

7 dolar virgl 700$7.700

nakit, denecek senetlerin imzalanmas.

Tarih

Hesaplar ve Aklama

bor

Kredi

12 Temmuz

TemmuzTemmuz

19: nakit temett

550$550$

hissedarlara denmitir.

Tarih

Hesaplar ve Aklama

bor

Kredi

19 Temmuz

TemmuzTemmuz

21: iin satn alnan ofis malzemeleri

800$800$

ve nakit dedi.

Tarih

Hesaplar ve Aklama

bor

Kredi

21 Temmuz

TemmuzTemmuz

27: Sorumluluu dedi

TemmuzTemmuz

5.

Hesaplar ve Aklama

bor

Kredi

27 Temmuz

2

17$ virgl 000$17.000$

John Leroy John Leroy

4

390$390$.

5

2 $ virgl 600 $2,600.

10

2 $ virgl 900 $2,900.

12

7 dolar virgl 700$7.700

19

550$550$

21

800$800$

27

TemmuzTemmuz

Tarih Hesaplar ve Aklama bor Kredi

2 Temmuz.

08 - Yurtiçi ve Yurtdışı Varlıkların Af Kanunu Kapsamında Beyanı

Donem Sonu İşlemleri Çözüm

1. 30.11.2012 TARİHLİ AYRINTILI BİLANÇO

DONEM LTD.ŞTİ

Sayfa No : 1 / 1

AÇIKLAMA CARİ DÖNEM (2012)

AKTİF (VARLIKLAR)

AÇIKLAMA CARİ DÖNEM (2012)

PASİF (KAYNAKLAR)

I - DÖNEN VARLIKLAR I - KISA VADELİ YABANCI KAYNAKLAR

A - Hazır Değerler 48.000,00 A - Mali Borçlar 110.000,00

1 - Kasa 35.000,00 1 - Banka Kredileri 110.000,00

2 - Alınan Çekler 7.000,00 B - Ticari Borçlar 70.000,00

3 - Bankalar 15.000,00 1 - Satıcılar 70.000,00

4 - Verilen Çekler ve Ödeme Emirleri (-) (9.000,00) F - Ödenecek Vergi ve Diğer Yükümlülükler 9.000,00

C - Ticari Alacaklar 238.000,00 1 - Ödenecek Vergi ve Fonlar 4.000,00

1 - Alıcılar 180.000,00 2 - Ödenecek Sosyal Güvenlik Kesintileri 5.000,00

2 - Alacak Senetleri 50.000,00 KISA VADELİ YABANCI KAY. TOPLAMI 189.000,00

7 - Şüpheli Ticari Alacaklar 8.000,00 II - UZUN VADELİ YABANCI KAYNAKLAR

D - Diğer Alacaklar 1.000,00 UZUN VADELİ YABANCI KAY. TOPLAMI

4 - Personelden Alacaklar 1.000,00 III - ÖZKAYNAKLAR

E - Stoklar 80.000,00 A - Ödenmiş Sermaye 270.000,00

4 - Ticari Mallar 80.000,00 1 - Sermaye 270.000,00

H - Diğer Dönen Varlıklar 12.000,00 ÖZKAYNAKLAR TOPLAMI 270.000,00

1 - Devreden KDV 12.000,00 PASİF (KAYNAKLAR) TOPLAMI 459.000,00

DÖNEN VARLIKLAR TOPLAMI 379.000,00

II - DURAN VARLIKLAR

D - Maddi Duran Varlıklar 80.000,00

5 - Taşıtlar 90.000,00

6 - Demirbaşlar 30.000,00

8 - Birikmiş Amortismanlar (-) (40.000,00)

DURAN VARLIKLAR TOPLAMI 80.000,00

AKTİF (VARLIKLAR) TOPLAMI 459.000,00

2. 1

Bilançodan ve bilgilerden yararlanarak aşağıdaki işlemleri ve istenilenleri yapınız.

Bilgiler :

- Açılışta mevcut 80.000 tl tutarındaki ticari mallar stoklarda yer alan 2.000 adet mala aittir.

- İşletmede 1.000 tl brüt ücret ile 2 pazarlamacı, 8 idari personel çalışmaktadır.

- Stoklar aralıklı envanter ve ağırlıklı ortalama maliyet yöntemi ile değerlenmektedir.

- Taşıtların faydalı ömrü 5 yıl, Demirbaşların faydalı ömrü 4 yıl'dır. Normal amortisman yöntemi uygulanmaktadır.

- İşletmenin yabancı para borç ve alacağı bulunmamaktadır.

Aralık 2012 dönemine ait işlemler :

1. Açılış kaydını yapınız.

2. 1.500 adet ticari mal toplam 60.000 tl + kdv bedel ile 2 ay vadeli (kredili) satın alınmıştır.

3. 120.000 tl + kdv tutarında ticari mal satılmış, kdv peşin tahsil edilmiş, 70.000 tl’lik çek alınmıştır. Kalan kısım 2 ay vadelidir.

4. 2.000 adet ticari mal toplam 100.000 tl + kdv bedel ile veresiye satın alınmıştır.

5. 40.000 tl + kdv tutarında ticari mal kredili (veresiye) olarak satılmıştır.

6. Kasada mevcut 20.000 tl karşılığında 15.000 usd satın alınmıştır.

7. 8000 adet ticari mal 160.000 tl + kdv bedel ile 2 ay kredili (veresiye) satın alınmıştır.

8. 200.000 tl +kdv tutarında ticari mal satılmıştır. 2 ay ileri tarihli çekler alınmıştır.

9. Önceki dönemde tahakkuk eden 4.000 tl Gelir Vergisi Kesintileri ile 5.000 SSK kesintileri ilgili kurumlara banka hesabından

ödenmiştir.

10. Müşterilerden 230.000 TL’lik tahsilat banka havalesi ile yapılmıştır.

11. Yapılan kasa sayımında kasada 750 tl’lik noksanlık tespit edilmiş olup, araştırılmak üzere geçici olarak düzeltilmiştir.

12. Yeni bir bayilik anlaşması için anlaşma yapılacak (üretici) firmaya 500.000 tl tutarında teminat mektubu verilmiştir. Teminat

mektubu için bankaya 2.500 tl komisyon ödenmiştir.

13. 300.000 tl + kdv tutarında toplam 15.000 adet ticari mal bedelinin yarısı veresiye satın alınırken, yarısı için 120 gün ileri tarihli

çekler keşide edilmiştir.

14. Kasadaki 10.000 tl ile 7.500 $ satın alınmıştır.

15. Yurt dışına 50.000 $’lık ticari mal ihracatı 3 ay vadeli yapılmıştır. (1$ = 1,60 tl)

16. Yurt içindeki müşterilere 350.000 tl + kdv tutarında ticari mal senet karşılığı satılmıştır.

17. Kayıtlı değeri 30.000 tl, birikmiş amortismanı 12.000 tl olan bir adet taşıt, 20.000 tl+kdv bedel ile peşin satılmıştır.

18. Daha önce veresiye satış yapılan müşterilerden biri 5.000 tl + kdv tutarında iade faturası göndermiştir.

19. İşletme muhasebe kayıtlarını tutmaya başlayan SMMM’e 500 tl + kdv peşin ödemiştir.

20. 7.000 tl +kdv tutarında elektrik, su ve telefon faturaları işletmeye ulaşmış, ödemeleri takip eden ay içerisinde yapılacaktır.

21. 400.000 tl’lik alacak senedi, 200.000 tl’lik çek; satıcı firmalara ciro edilmiştir.

22. Ay sonunda ücret bordroları düzenlenmiş, henüz personele ödemeleri yapılmamıştır.

3. 2

ENVANTER VE 31/12/2012 DÖNEM SONU İŞLEMLERİ

(Geçici mizandan yararlanarak aşağıdaki belirtilen muhasebe dışı envanter sonuçları için dönem sonu işlemlerini yapınız.)

Yabancı Para ve Yabancı Para Cinsinden Borç ve Alacakların 31/12/2012 Tarihli Değerlemesinde Dikkate Alınacak Kur: 1 $ =

1,50 tl

23. Kasa sayımı yapılmış TL mevcudunun 48.860 tl olduğu ve TL kasa hesabı ile eşit olduğu tespit edilmiştir. USD mevcudunun ise

22.500 $ olduğu tespit edilmiştir. (Sayım sonucu ile TL hesabın eşit olması nedeni ile herhangi bir muhasebe kaydı yapılmasına

gerek yoktur. YP para mevcudunun ise dönem sonu kuru ile değerlemesi yapılacaktır.)

Portföyde mevcut çeklerin sayımı yapılmış ve 113.000 tl tutarında oldukları tutanak ile tespit edilmiştir.

24. Bankalardan alınan hesap özetlerine (ekstre) göre bankada 233.600 tl olduğu anlaşılmıştır. İşletmenin banka hesabı ise 233.500

tl borç kalanı vermektedir. Farklılığın bankanın, hesaba işlettiği 600 tl faiz gelirinden ve hesaptan çektiği 500 tl teminat mektubu

komisyonlarından kaynaklandığı anlaşılmıştır.

25. Ticari alacaklar için yurt içi müşterilere mutabakat mektupları gönderilmiş ve müşteriler ile hesap bakiyelerinde mutabık

kalınmıştır. 50.000 $’lık yurt dışı alacağın ise dönem sonu kur üzerinden değerlemesi yapılmıştır.

Portföyde mevcut alacak senetlerinin sayımı ve dökümü yapılmış ve 63.000 tl tutarında senet olduğu ve Alacak senetleri hesabı

ile eşit tutarda olduğu tespit edilmiştir.

26. Nominal değeri 63.000 tl olan Alacak Senetleri için 1.800 tl reeskont hesaplanmıştır.

27. 8.000 tl şüpheli alacak için, 2012 yılı içerisinde icra/takip davası açıldığından, şüpheli alacak için karşılık ayrılmıştır.

28. Geçici mizana göre personele olan borç 7.165 tl, personelden olan alacak ise 1.000 tl’dir. Personelden olan alacakların

personelin ücretinden (maaşından) kesilmesine karar verilmiştir.

29. Ticari mal stoklarında 4.000 adet ticari mal kaldığı sayım sonucu tutanak ile tespit edilmiştir.

30. 191 ve 391 hesaplar kapatılarak KDV mahsup kaydı yapılmıştır.

31. Geçici mizanda Sayım ve Tesellüm Noksanlıkları hesabında görülen 750 tl’nin nedeni bulunamamıştır. Bu nedenle gider

kaydedilmesine karar verilmiştir.

Taşıtların ve demirbaşların sayımı yapılmış mutabakatları sağlanmıştır.

32. Maddi Duran Varlıklarlar (ATİK) için son 3 aylık dönem için amortisman kaydı yapılmıştır. (Taşıtların faydalı ömrü 5 yıl,

Demirbaşların faydalı ömrü 4 yıl'dır. Normal amortisman yöntemi uygulanmaktadır. Taşıtlar pazarlama ve dağıtımda,

demirbaşlar yönetimde kullanılmaktadır.)

33. Bankalara olan kredi borçları, bankalardan temin edilen hesap ekstreleri ile karşılaştırılarak mutabakatı sağlanmıştır. Hesap

ekstrelerinin kontrolü sırasında bankanın 3.500 tl faiz tahakkuku yaptığı anlaşılmıştır.

Satıcılara olan borçlar, satıcılardan gelen mutabakat mektupları ile kontrol edilmiş ve hesapların mutabakatı sağlanmıştır.

Ödenecek Vergi ve Fonlar ile Ödenecek Sosyal Güvenlik Kesintileri hesapları muhtasar beyanname ve SSK bildirgeleri ile

kontrol edilerek doğrulukları tespit edilmiştir.

Sermaye hesabı kuruluş ve en son sermaye artırımı hakkında ticaret sicil gazetesindeki sermaye tutarı ile karşılaştırılmış ve

doğruluğu tespit edilmiştir.

34. Aralık 2012 döneminin gelir tablosunun elde edilebilmesi amacı ile 7’li gider hesaplarının 6’lı hesaplara yansıtılması yapılmış

ve gelir tablosu elde edilmiştir.

35. Aralık 2012 dönem karı üzerinden %20 oranında kurumlar vergisi karşılığı ayrılmıştır.

36. Tüm yansıtma hesapları kapatılmıştır.

37. 6’ile başlayan gelir/gider hesapları 690 Dönem Kar ya da Zararı hesabına aktarılmıştır.

38. 690 hesap bakiyesi 692 Dönem Net Karı ya da Zararı hesabına aktarılmıştır.

39. 692 hesap bakiyesi kar/zarar durumuna göre 590 Dönem Net Karı veya 591 Dönem Net Zararı hesabına aktarılmıştır.

Kesin Mizan Düzenlenmiştir.

31.12.2012 tarihli bilanço düzenlenmiştir.

Bilanço ve gelir tablosu dipnotları düzenlenmiştir.

40. Tüm hesapların kapanış kaydı yapılmıştır.

2013 YILI OCAK AYI BAŞINDA YAPILACAK ZORUNLU KAYITLAR

41. Açılış kaydını yapınız.

42. Dönem net karı hesabı, Önceki dönem karı hesabına aktarılmıştır.

43. Reeskont hesapları kapatılmıştır.

4. Yevmiye Defteri

Unvan : DONEM LTD.ŞTİ

AÇIKLAMA DETAY BORÇ ALACAKHESAP KODU

Madde No : ---- 30.11.2012 ---- 000000001 Nolu Açılış Fişi1

100 KASA 35.000,00

101 ALINAN ÇEKLER 7.000,00

102 BANKALAR 15.000,00

120 ALICILAR 180.000,00

121 ALACAK SENETLERİ 50.000,00

128 ŞÜPHELİ TİCARİ ALACAKLAR 8.000,00

135 PERSONELDEN ALACAKLAR 1.000,00

153 TİCARİ MALLAR 80.000,00

190 DEVREDEN KDV 12.000,00

254 TAŞITLAR 90.000,00

255 DEMİRBAŞLAR 30.000,00

103 VERİLEN ÇEKLER VE ÖDEME EMİRLERİ (-) 9.000,00

257 BİRİKMİŞ AMORTİSMANLAR (-) 40.000,00

300 BANKA KREDİLERİ 110.000,00

320 SATICILAR 70.000,00

360 ÖDENECEK VERGİ VE FONLAR 4.000,00

361 ÖDENECEK SOSYAL GÜVENLİK KESİNTİLERİ 5.000,00

500 SERMAYE 270.000,00

--

Madde No : ---- 03.12.2012 ---- 000000002 Nolu Mahsup Fişi0

153 TİCARİ MALLAR 60.000,00

191 İNDİRİLECEK KDV 10.800,00

320 SATICILAR 70.800,00

--TİCARİ MAL ALIŞ

Madde No : ---- 04.12.2012 ---- 000000003 Nolu Mahsup Fişi0

100 KASA 21.600,00

101 ALINAN ÇEKLER 70.000,00

120 ALICILAR 50.000,00

391 HESAPLANAN KDV 21.600,00

600 YURTİÇİ SATIŞLAR 120.000,00

--SATIŞ

Madde No : ---- 05.12.2012 ---- 000000004 Nolu Mahsup Fişi0

153 TİCARİ MALLAR 100.000,00

191 İNDİRİLECEK KDV 18.000,00

320 SATICILAR 118.000,00

--TİCARİ MAL ALIŞ

Madde No : ---- 06.12.2012 ---- 000000005 Nolu Mahsup Fişi0

120 ALICILAR 47.200,00

391 HESAPLANAN KDV 7.200,00

600 YURTİÇİ SATIŞLAR 40.000,00

--SATIŞ

Madde No : ---- 07.12.2012 ---- 000000006 Nolu Mahsup Fişi0

100 KASA 20.000,00

100 KASA 20.000,00

--DÖVİZ ALIŞ

Madde No : ---- 08.12.2012 ---- 000000007 Nolu Mahsup Fişi0

153 TİCARİ MALLAR 160.000,00

191 İNDİRİLECEK KDV 28.800,00

320 SATICILAR 188.800,00

--TİCARİ MAL ALIŞ

Madde No : ---- 10.12.2012 ---- 000000008 Nolu Mahsup Fişi0

101 ALINAN ÇEKLER 236.000,00

391 HESAPLANAN KDV 36.000,00

600 YURTİÇİ SATIŞLAR 200.000,00

--SATIŞ

Madde No : ---- 11.12.2012 ---- 000000009 Nolu Mahsup Fişi0

360 ÖDENECEK VERGİ VE FONLAR 4.000,00

361 ÖDENECEK SOSYAL GÜVENLİK KESİNTİLERİ 5.000,00

102 BANKALAR 9.000,00

--VERGİ ÖDEMELERİ

Madde No : ---- 12.12.2012 ---- 000000010 Nolu Mahsup Fişi0

102 BANKALAR 230.000,00

120 ALICILAR 230.000,00

--TAHSİLAT

Madde No : ---- 13.12.2012 ---- 000000011 Nolu Mahsup Fişi0

197 SAYIM VE TESELLÜM NOKSANLARI 750,00

100 KASA 750,00

--SAYIM NOKSANLIĞI

Madde No : ---- 14.12.2012 ---- 000000012 Nolu Mahsup Fişi0

Sayfa Toplamı : 1.570.150,00 1.570.150,00

5. Yevmiye Defteri

Unvan : DONEM LTD.ŞTİ

AÇIKLAMA DETAY BORÇ ALACAKHESAP KODU

Nakli Toplam : 1.570.150,00 1.570.150,00

Madde No : ---- 14.12.2012 ---- 000000012 Nolu Mahsup Fişi0

780 FİNANSMAN GİDERLERİ 2.500,00

901 TEMİNAT MEKTUBUNDAN BORÇLAR 500.000,00

102 BANKALAR 2.500,00

900 TEMİNAT MEKTUBUNDAN ALACAKLAR 500.000,00

--TEMİNAT MEKTUBU

Madde No : ---- 15.12.2012 ---- 000000013 Nolu Mahsup Fişi0

153 TİCARİ MALLAR 300.000,00

191 İNDİRİLECEK KDV 54.000,00

103 VERİLEN ÇEKLER VE ÖDEME EMİRLERİ (-) 177.000,00

320 SATICILAR 177.000,00

--

Madde No : ---- 16.12.2012 ---- 000000014 Nolu Mahsup Fişi0

100 KASA 10.000,00

100 KASA 10.000,00

--DÖVİZ ALIŞ

Madde No : ---- 17.12.2012 ---- 000000015 Nolu Mahsup Fişi0

120 ALICILAR 80.000,00

601 YURTDIŞI SATIŞLAR 80.000,00

--YURT DIŞI SATIŞ (İHRACAT)

Madde No : ---- 18.12.2012 ---- 000000016 Nolu Mahsup Fişi0

121 ALACAK SENETLERİ 413.000,00

391 HESAPLANAN KDV 63.000,00

600 YURTİÇİ SATIŞLAR 350.000,00

--SATIŞ

Madde No : ---- 19.12.2012 ---- 000000017 Nolu Mahsup Fişi0

100 KASA 23.600,00

257 BİRİKMİŞ AMORTİSMANLAR (-) 12.000,00

254 TAŞITLAR 30.000,00

391 HESAPLANAN KDV 3.600,00

679 DİĞER OLAĞANDIŞI GELİR VE KARLAR 2.000,00

--MADDİ DURAN VARLIK SATIŞI

Madde No : ---- 20.12.2012 ---- 000000018 Nolu Mahsup Fişi0

191 İNDİRİLECEK KDV 900,00

610 SATIŞTAN İADELER (-) 5.000,00

120 ALICILAR 5.900,00

--SATIŞ İADESİ

Madde No : ---- 21.12.2012 ---- 000000019 Nolu Mahsup Fişi0

191 İNDİRİLECEK KDV 90,00

770 GENEL YÖNETİM GİDERLERİ 500,00

100 KASA 590,00

--MUHASEBE ÜCRETİ

Madde No : ---- 22.12.2012 ---- 000000020 Nolu Mahsup Fişi0

191 İNDİRİLECEK KDV 1.260,00

770 GENEL YÖNETİM GİDERLERİ 7.000,00

320 SATICILAR 8.260,00

--ELEKTRİK SU TELEFON FATURALARI

Madde No : ---- 23.12.2012 ---- 000000021 Nolu Mahsup Fişi0

320 SATICILAR 600.000,00

101 ALINAN ÇEKLER 200.000,00

121 ALACAK SENETLERİ 400.000,00

--BORÇ ÖDEMELERİ

Madde No : ---- 24.12.2012 ---- 000000022 Nolu Mahsup Fişi0

760 PAZARLAMA, SATIŞ VE DAĞITIM GİDERLERİ 2.440,00

770 GENEL YÖNETİM GİDERLERİ 9.760,00

335 PERSONELE BORÇLAR 7.165,00

360 ÖDENECEK VERGİ VE FONLAR 1.335,00

361 ÖDENECEK SOSYAL GÜVENLİK KESİNTİLERİ 3.700,00

--ÜCRET TAHAKKUKU

Toplam Tutarlar : 3.592.200,00 3.592.200,00

7. Yevmiye Defteri

Unvan : DONEM LTD.ŞTİ

AÇIKLAMA DETAY BORÇ ALACAKHESAP KODU

Nakli Toplam : 3.592.200,00 3.592.200,00

Madde No : ---- 31.12.2012 ---- 000000023 Nolu Mahsup Fişi0

100 KASA 3.750,00

646 KAMBİYO KARLARI 3.750,00

--D.SONU İŞLEMİ - KASA DEĞERLEME

Madde No : ---- 31.12.2012 ---- 000000024 Nolu Mahsup Fişi0

102 BANKALAR 600,00

780 FİNANSMAN GİDERLERİ 500,00

102 BANKALAR 500,00

642 FAİZ GELİRLERİ 600,00

--D.SONU İŞLEMİ - BANKA HESABI DÜZELTME

Madde No : ---- 31.12.2012 ---- 000000025 Nolu Mahsup Fişi0

656 KAMBİYO ZARARLARI (-) 5.000,00

120 ALICILAR 5.000,00

--D.SONU İŞLEMİ - DÖVİZ ALACAK DEĞERLEME

Madde No : ---- 31.12.2012 ---- 000000026 Nolu Mahsup Fişi0

657 REESKONT FAİZ GİDERLERİ (-) 1.800,00

122 ALACAK SENETLERİ REESKONTU (-) 1.800,00

--D.SONU İŞL. - REESKONT HESAPLAMA

Madde No : ---- 31.12.2012 ---- 000000027 Nolu Mahsup Fişi0

654 KARŞILIK GİDERLERİ (-) 8.000,00

129 ŞÜPHELİ TİCARİ ALACAKLAR KARŞILIĞI (-) 8.000,00

--D. SONU İŞL. - ŞÜPHELİ ALACAK KARŞILIĞI

Madde No : ---- 31.12.2012 ---- 000000028 Nolu Mahsup Fişi0

335 PERSONELE BORÇLAR 1.000,00

135 PERSONELDEN ALACAKLAR 1.000,00

--D.SONU İŞL - PERSONEL HESAPLARI

Madde No : ---- 31.12.2012 ---- 000000029 Nolu Mahsup Fişi0

621 SATILAN TİCARİ MALLAR MALİYETİ (-) 601.754,00

153 TİCARİ MALLAR 601.754,00

--D.SONU - SMM HESAPLANMASI

Madde No : ---- 31.12.2012 ---- 000000030 Nolu Mahsup Fişi0

391 HESAPLANAN KDV 131.400,00

190 DEVREDEN KDV 12.000,00

191 İNDİRİLECEK KDV 113.850,00

360 ÖDENECEK VERGİ VE FONLAR 5.550,00

--D.SONU - KDV MAHSUBU

Madde No : ---- 31.12.2012 ---- 000000031 Nolu Mahsup Fişi0

689 DİĞER OLAĞANDIŞI GİDER VE ZARARLAR (-) 750,00

197 SAYIM VE TESELLÜM NOKSANLARI 750,00

--D.SONU - SAYIM NOKSANLIĞININ GİDERLEŞTİRİLMESİ

Madde No : ---- 31.12.2012 ---- 000000032 Nolu Mahsup Fişi0

760 PAZARLAMA, SATIŞ VE DAĞITIM GİDERLERİ 3.000,00

770 GENEL YÖNETİM GİDERLERİ 1.875,00

257 BİRİKMİŞ AMORTİSMANLAR (-) 4.875,00

--D.SONU- AMORTİSMAN HESAPLAMA

Madde No : ---- 31.12.2012 ---- 000000033 Nolu Mahsup Fişi0

780 FİNANSMAN GİDERLERİ 3.500,00

300 BANKA KREDİLERİ 3.500,00

--D.SONU - KREDİ FAİZ TAHAKKUKU

Madde No : ---- 31.12.2012 ---- 000000034 Nolu Mahsup Fişi0

631 PAZARLAMA, SATIŞ VE DAĞITIM GİDERLERİ(-) 5.440,00

632 GENEL YÖNETİM GİDERLERİ (-) 19.135,00

660 KISA VADELİ BORÇLANMA GİDERLERİ (-) 6.500,00

761 PAZARLAMA, SATIŞ VE DAĞITIM GİD.YAN.HES. 5.440,00

771 GENEL YÖNETİM GİDERLERİ YANSITMA HESABI 19.135,00

781 FİNANSMAN GİDERLERİ YANSITMA HESABI 6.500,00

--D.SONU YANSITMA KAYITLARI (GELİR TABLOSU)

Madde No : ---- 31.12.2012 ---- 000000035 Nolu Mahsup Fişi0

691 DÖNEM KARI VERGİ VE DİĞ.YAS.YÜK.KAR. (-) 28.594,00

370 DÖNEM KARI VERGİ VE Dİ.YAS.YÜK.KARŞILIK. 28.594,00

--D.SONU - KURUMLAR VERGİSİ HESAPLAMA

Toplam Tutarlar : 4.414.798,00 4.414.798,00

8. DÖNEME AİT GELİR TABLOSU 2012 2012

Yurtiçi Satışlar 710.000

Yurtdışı Satışlar 80.000

Satıştan İadeler (-) -5.000

NET SATIŞLAR 785.000

Satılan Ticari Mallar Maliyeti (-) -601.754

BRÜT SATIŞ KARI VEYA ZARARI 183.246

Pazarlama, Satış ve Dağıtım Giderleri (-) -5.440

Genel Yönetim Giderleri (-) -19.135

FAALİYET KARI VEYA ZARARI 158.671

Faiz Gelirleri 600

Kambiyo Karları 3.750

Karşılık Giderleri (-) -8.000

Kambiyo Zararları (-) -5.000

Reeskont Faiz Giderleri (-) -1.800

Kısa Vadeli Borçlanma Giderleri (-) -6.500

OLAĞAN KAR VEYA ZARAR 141.721

Diğer Olağandışı Gelir ve Karlar 2.000

Diğer Olağandışı Gider ve Zararlar (-) -750

DÖNEM KARI VEYA ZARARI 142.971

Dön.Karı vergi ve Diğ. Yasal Yük. Karş. -28.594

DÖNEM NET KARI VEYA ZARARI 114.377

9. Yevmiye Defteri

Unvan : DONEM LTD.ŞTİ

AÇIKLAMA DETAY BORÇ ALACAKHESAP KODU

Nakli Toplam : 4.414.798,00 4.414.798,00

Madde No : ---- 31.12.2012 ---- 000000036 Nolu Mahsup Fişi36

761 PAZARLAMA, SATIŞ VE DAĞITIM GİD.YAN.HES. 5.440,00

771 GENEL YÖNETİM GİDERLERİ YANSITMA HESABI 19.135,00

781 FİNANSMAN GİDERLERİ YANSITMA HESABI 6.500,00

760 PAZARLAMA, SATIŞ VE DAĞITIM GİDERLERİ 5.440,00

770 GENEL YÖNETİM GİDERLERİ 19.135,00

780 FİNANSMAN GİDERLERİ 6.500,00

--D.SONU - KAPANIŞ İŞLEMLERİ (YANSITMA HS. KAPANIŞI)

Madde No : ---- 31.12.2012 ---- 000000037 Nolu Mahsup Fişi37

600 YURTİÇİ SATIŞLAR 710.000,00

601 YURTDIŞI SATIŞLAR 80.000,00

642 FAİZ GELİRLERİ 600,00

646 KAMBİYO KARLARI 3.750,00

679 DİĞER OLAĞANDIŞI GELİR VE KARLAR 2.000,00

610 SATIŞTAN İADELER (-) 5.000,00

621 SATILAN TİCARİ MALLAR MALİYETİ (-) 601.754,00

631 PAZARLAMA, SATIŞ VE DAĞITIM GİDERLERİ(-) 5.440,00

632 GENEL YÖNETİM GİDERLERİ (-) 19.135,00

654 KARŞILIK GİDERLERİ (-) 8.000,00

656 KAMBİYO ZARARLARI (-) 5.000,00

657 REESKONT FAİZ GİDERLERİ (-) 1.800,00

660 KISA VADELİ BORÇLANMA GİDERLERİ (-) 6.500,00

689 DİĞER OLAĞANDIŞI GİDER VE ZARARLAR (-) 750,00

690 DÖNEM KARI VEYA ZARARI 114.377,00

691 DÖNEM KARI VERGİ VE DİĞ.YAS.YÜK.KAR. (-) 28.594,00

--D.SONU KAPANIŞ - GELİR GESAPLARININ KAPATILMASI

Madde No : ---- 31.12.2012 ---- 000000038 Nolu Mahsup Fişi38

690 DÖNEM KARI VEYA ZARARI 114.377,00

590 DÖNEM NET KARI 114.377,00

--D.SONU KAPANIŞ - KAR ZARAR

Toplam Tutarlar : 5.356.600,00 5.356.600,00

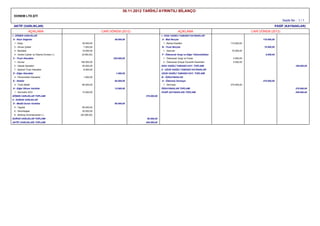

11. AKTİF (VARLIKLAR) PASİF (KAYNAKLAR)

I - DÖNEN VARLIKLAR 518.956 III - KISA VADELİ YABANCI KAYNAKLAR 191.704

Hazır Değerler 243.210 Mali Borçlar 113.500

Kasa 82.610 Banka Kredileri 113.500

Alınan Çekler 113.000 Ticari Borçlar 32.860

Bankalar 233.600 Satıcılar 32.860

Verilen Çekler (-) -186.000 Diğer Borçlar 6.165

Ticari Alacaklar 177.500 Personele Borçlar 6.165

Alıcılar 116.300 Ödenecek Vergi ve Diğer Yükümlülükler 10.585

Alacak Senetleri 63.000 Ödenecek Vergi ve Fonlar 6.885

Alacak Senetleri Reeskontu (-) -1.800 Ödenecek Sosyal Güvenlik Kesintileri 3.700

Şüpheli Ticari Alacaklar 8.000 Borç ve Gider Karşılıkları 28.594

Şüpheli Ticari Alacaklar Karşılığı (-) -8.000 Dön.Karı Vergi ve Diğ. Yas. Yük. Kar. 28.594

Stoklar 98.246

Ticari Mallar 98.246 IV - UZUN VADELİ YABANCI KAYNAKLAR 0

II - DURAN VARLIKLAR 57.125 V - ÖZKAYNAKLAR 384.377

Maddi Duran Varlıklar 57.125 Sermaye 270.000

Taşıtlar 60.000 Dönem Net Karı 114.377

Demirbaşlar 30.000

Birikmiş Amortismanlar (-) -32.875

AKTİF (VARLIKLAR) TOPLAMI 576.081 PASİF (KAYNAKLAR) TOPLAMI 576.081

Bilanço Dipnotları

3. Aktif değerlerin toplam sigorta tutarı / Sigorta yaptırılmamıştır.

6. Pasifte yer almayan taahhütlerin toplam tutarı / Bankalardan kullanılan 500.000 TL teminat mektubu mevcuttur.

7. Kasa ve bankalardaki döviz mevcutları

Döviz Cinsi Miktar TL Kuru Toplam Tutar

USD - ABD DOLARI 22.500 1,5 33.750

8. Yurtdışından alacaklar (avanslar dahil)

Döviz Cinsi Miktar TL Kuru Toplam Tutar

USD - ABD DOLARI 50.000 1,5 80.000

20. Cari dönemdeki ortalama toplam personel sayısı / 8 İdari, 2 Pazarlamacı olmak üzere toplam 10 Personel

31.12.2012 TARİHLİ AYRINTILI BİLANÇO