Developments in the UK Economy

•

2 likes•4,869 views

The document analyzes economic developments in the UK including growth, inflation, output gap, unemployment, aggregate demand, housing market, consumer spending, investment, employment trends, and monetary policy. It finds that real GDP growth has been slow since the recession, inflation is low, unemployment remains above pre-recession levels, and the Bank of England has kept interest rates low through its new policy of forward guidance.

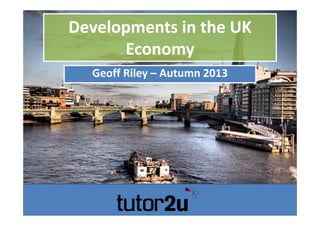

![Growth and inflation in the UK Economy

Real GDP growth (%) [ar 4 quarters] Consumer Price Inflation (%)

Source: UK Statistics Agency

Percent

Percent

Consumer price inflation

Real GDP growth](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Developments in the UK Economy

Similar to Developments in the UK Economy (20)

More from tutor2u

More from tutor2u (20)

Recently uploaded

Recently uploaded (20)

Developments in the UK Economy

- 2. Growth and inflation in the UK Economy Real GDP growth (%) [ar 4 quarters] Consumer Price Inflation (%) Source: UK Statistics Agency Percent Percent Consumer price inflation Real GDP growth

- 3. Real GDP for the UKQuarterly value of real GDP (at constant prices, value added measure) Source: Office of National Statistics £(billions) £(billions)

- 4. Growth and the Output GapTop pane: Real GDP Bottom Pane: Output Gap measured as a % of potential GDP source: OECD UK Real GDP and Output Gap Source: Reuters EcoWin 05 06 07 08 09 10 11 12 13 14 -5 -4 -3 -2 -1 0 1 2 3 4 PercentageofpotentialGDP -5 -4 -3 -2 -1 0 1 2 3 4 thousandbillions 1.350 1.375 1.400 1.425 1.450 1.475 1.500 atconstantprices(thousandbillions) 1.350 1.375 1.400 1.425 1.450 1.475 1.500 PLOG ‐ a persistent large output gap

- 5. Output gap and unemploymentOutput Gap (% of potential GDP), Unemployment - Labour Force Survey measure The Output Gap and Unemployment in the UK Source: Reuters EcoWin 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 -5.0 -2.5 0.0 2.5 5.0 7.5 10.0 12.5 Percent -5.0 -2.5 0.0 2.5 5.0 7.5 10.0 12.5 Unemployment rate (LFS measure) Output gap (% of potential GDP)

- 6. Aggregate Demand (AD)£bn per year at constant 2003 prices The Components of Aggregate Demand Consumer spending Capital investment Government consumption Imports Exports Source: UK Statistics Commission 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 thousandbillions 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0 GBP(thousandbillions) 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0

- 7. Trying to achieve macro stability Source: Reuters EcoWin Percent Percent CPI Inflation GDP growth Unemployment Rate

- 8. Another look at the cycleAnnual percentage change in real GDP measured at constant prices Growth in UK Real National Output Source: UK Statistics Commission 00 01 02 03 04 05 06 07 08 09 10 11 12 13 Percent -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 Percent -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 New normal growth rate likely to be slow .............

- 9. Tracking output by sectorIndex of Output (Value Added) at Constant Prices, Seasonally Adjusted, Index, 2009=100 Manufacturing Construction UK Real GDP Finance and Insurance Source: Office for National Statistics 00 01 02 03 04 05 06 07 08 09 10 11 12 13 Indexofoutput2009=100 70 75 80 85 90 95 100 105 110 115 Indexofoutput2009=100 70 75 80 85 90 95 100 105 110 115

- 10. The employment rate remains below peak levels United Kingdom, Employment, Rate, Aged 16-64, seasonally adjusted Employment Rate in the UK Economy Source: Reuters EcoWin 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 68.0 68.5 69.0 69.5 70.0 70.5 71.0 71.5 72.0 72.5 73.0 73.5 Percent 68.0 68.5 69.0 69.5 70.0 70.5 71.0 71.5 72.0 72.5 73.0 73.5

- 11. Trend growth is falling – why? Source: OECD World Economic Outlook 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 thousandbillions RealGDP£(thousandbillions) Potential GDP Percentperyear Estimated UK Trend Growth Rate Recession may have inflicted damage on trend growth

- 12. The output gap is negativePercentage Percent Percent Output Gap CPI InflationUK Policy Rates Plenty of spare capacity No change in policy base rates for nearly 4 years

- 13. % annual change in household spending and GDP at constant 2000 prices Source: Office of National Statistics Annual%change Annual%change Real GDP Consumer spending Household demand is main short term driver of AD

- 14. Average UK House PricesAll properties, average, £s Source: Reuters EcoWin 00 01 02 03 04 05 06 07 08 09 10 11 12 13 70000 80000 90000 100000 110000 120000 130000 140000 150000 160000 170000 180000 190000 Averagepropertyprices£s 70000 80000 90000 100000 110000 120000 130000 140000 150000 160000 170000 180000 190000

- 15. Housing affordability Source: HBoS Housing Research Ratioofhousepricestoaverageearnings

- 16. Construction and JobsTop pane: Construction sector employment Lower Pane: Housing Starts Construction employment Housing Starts per quarter, England, seasonally adjusted Source: Reuters EcoWin 00 01 02 03 04 05 06 07 08 09 10 11 12 13 10000 20000 30000 40000 50000 Newhousesstarted 10000 20000 30000 40000 50000 millions 1.85 1.95 2.05 2.15 2.25 2.35 Employment(millions) 1.85 1.95 2.05 2.15 2.25 2.35

- 17. Consumer Borrowing Secured on Property£ billion per month, seasonally adjusted Source: Reuters EcoWin 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 billions -1 0 1 2 3 4 5 6 7 8 9 10 11 GBP(billions) -1 0 1 2 3 4 5 6 7 8 9 10 11

- 18. Real House PricesReal, house prices, Percentage change from previous year Asset Price Deflation - Real Property Prices in Selected Countries United Kingdom Spain Greece Ireland Germany Source: OECD World Economic Outlook 02 03 04 05 06 07 08 09 10 11 12 Percent -15 -10 -5 0 5 10 15 20 Percent -15 -10 -5 0 5 10 15 20

- 19. Consumer confidence remains weakExpectations over next 12 months, % balance of optimists over pessimists Source: Reuters EcoWin PercentageBalanceofrespondents State of the economy Likely to make major purchases People's Own Financial Situation

- 20. State of the EconomyPer cent of respondents Survey about the State of the UK Economy UK Current Economic Situation, Bad UK Current Economic Situation, Don't know UK Current Economic Situation, Good UK Current Economic Situation, Normal Source: Reuters EcoWin Jan May Sep Jan May Sep Jan May Sep Jan May Sep Jan May Sep Jan May Sep Jan 06 07 08 09 10 11 12 0 10 20 30 40 50 60 70 80 90 Percent 0 10 20 30 40 50 60 70 80 90

- 21. Low wage growth and the squeeze on real incomes continues Annual growth of regular weekly pay, consumer price inflation (%) Annual Change in Weekly Regular Pay and CPI Inflation Average Weekly Pay, 3 month average, seasonally adjusted Consumer Price Index (All Items) Source: Office of National Statistics Jan May Sep Jan May Sep Jan May Sep Jan May Sep Jan May Sep Jan May Sep Jan May 07 08 09 10 11 12 13 Percent 0.0 1.0 2.0 3.0 4.0 5.0 6.0 Percent 0.0 1.0 2.0 3.0 4.0 5.0 6.0 Consumer Price Inflation (%) Regular Weekly Pay (% annual change)

- 22. Spending on consumer durablesReal spending at constant prices, seasonally adjusted, £ billion per quarter Source: Reuters EcoWin billions £satconstant2002prices(billions)

- 23. Total Real Capital Investment Spending UK United Kingdom, Short-term interest rate Source: UK Statistics Commission percent billions £(billions)

- 24. Jobs and prices Source: Reuters EcoWin Percent UK Unemployment Rate (Labour Force Survey, % of labour force) Inflation Rate (CPI, annual % change)

- 25. Oil prices affect AD and SRAS Source: Reuters EcoWin USdollarsperbarrel The external environment matters a lot for the UK economy World oil price seems to have stabilised around $100 a barrel................

- 26. Annual % change in UK GDP at constant prices,% of labour force unemployed Source: UK Statistics Commission Percentofthelabourforce PercentagegrowthofGDP Real GDP (Annual % Change) LHS Unemployment (% of the labour force) RHS Deep recession (> 6% fall in output) and weak recovery (GDP grew only 0.7% in 2011) Economy needs to grow at least 2% for unemployment to start falling

- 28. Monthly level of redundanciesMonthly total Redundancies in the UK Economy Source: Reuters EcoWin 04 05 06 07 08 09 10 11 12 13 100000 125000 150000 175000 200000 225000 250000 275000 300000 325000 redundancies 100000 125000 150000 175000 200000 225000 250000 275000 300000 325000

- 29. Regional Unemployment RatesA selection of regional unemployment rates, per cent of the labour force, LFS measure London North East Northern Ireland Scotland South East Yorks and Humber UK Source: UK Labour Market Statistics 05 06 07 08 09 10 11 12 3 4 5 6 7 8 9 10 11 12 GBP 3 4 5 6 7 8 9 10 11 12

- 30. Employment in two key industriesQuarterly level of employment, seasonally adjusted, million Employment in UK Manufacturing and Construction Industries Construction Industry Employment Manufacturing Industry Employment Source: UK Office of National Statistics 00 01 02 03 04 05 06 07 08 09 10 11 12 13 Personsemployed(millions) 1.75 2.00 2.25 2.50 2.75 3.00 3.25 3.50 3.75 4.00 4.25 Personsemployed(millions) 1.75 2.00 2.25 2.50 2.75 3.00 3.25 3.50 3.75 4.00 4.25 Manufacturing Construction

- 31. Duration of unemployment Source: Reuters EcoWin millions Persons(millions) Unemployed for up to six months Unemployed for over 12 months Unemployed for over 24 months

- 32. Greece Ireland Italy Spain Germany United Kingdom South Korea United States Source: OECD World Economic Outlook Percentofthelabourforce Youth unemployment in Greece and Spain is over 50% of the labour force

- 33. Long term youth unemploymentThousands, people out of work for at least a year Long Term Unemployment for people Aged 18-24 Source: Reuters EcoWin 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 25000 50000 75000 100000 125000 150000 175000 200000 225000 250000 275000 25000 50000 75000 100000 125000 150000 175000 200000 225000 250000 275000

- 34. Unemployment and Trend Growth (UK)Source: OECD World Economic Outlook Source: OECD World Economic Outlook 04 05 06 07 08 09 10 11 12 13 14 Percent 0 1 2 3 4 5 6 7 8 9 Percent 0 1 2 3 4 5 6 7 8 9 Unemployment rate (%) Estimated UK Trend Growth Rate

- 35. Euro Zone Jobs Crisis Unemployment Employment Labour force Source: OECD World Economic Outlook 02 03 04 05 06 07 08 09 10 11 12 13 14 millions 135.0 137.5 140.0 142.5 145.0 147.5 150.0 152.5 155.0 157.5 160.0 Person(millions) 135.0 137.5 140.0 142.5 145.0 147.5 150.0 152.5 155.0 157.5 160.0 Total Employment Size of Labour Force millions 11 12 13 14 15 16 17 18 19 20 Person(millions) 11 12 13 14 15 16 17 18 19 20 Total Unemployment in the Euro Area

- 36. Base Interest RatesPer cent Source: Reuters EcoWin Percent Percent

- 37. Forward Guidance Arrives!Percentage Forward Guidance: Base Interest Rates and UK Unemployment 05 06 07 08 09 10 11 12 13 Percent 0 1 2 3 4 5 6 7 8 9 Percent 0 1 2 3 4 5 6 7 8 9 Unemployment rate UK policy interest rates

- 38. The Cost of Credit Personal Lending Rates, Bank and Building Society, Average Credit Card Rate Average Overdraft Interest Rate Bank Rate (Policy Rate) Set by Bank of England MPC Fixed Mortgage Interest Rate, average Source: Bank of England 07 08 09 10 11 12 13 Percentinterestonloans 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0 20.0 Percentinterestonloans 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0 20.0 Mortgage rates Base Interest Rates (set by Bank of England) Overdrafts Credit cards Official interest rates are about as low as they can go and government bond yields are at record lows. Yet regular borrowers are paying well above these rates

- 39. Bank lending M4 lending, Chg Y/Y M4 Lending, 3 month M4 Lending, 6 month Source: Reuters EcoWin Percent QE started in March 2009

- 40. Mortgage approvalsMonthly figure, seasonally adjusted Number of loans approved for UK house purchase Source: Council for Mortgage Lenders 00 01 02 03 04 05 06 07 08 09 10 11 12 13 0 20000 40000 60000 80000 100000 120000 140000 Numberof 0 20000 40000 60000 80000 100000 120000 140000

- 41. Sterling exchange rate index Source: Reuters EcoWin Tradeweightedindex Tradeweightedindex Fall in the index shows a depreciation of sterling against a basket of major currencies

- 42. Top pane: Effective exchange rate index, Bottom pane: Trade balance in goods and services Effective Exchange Rate Index, annual average value Trade balance in Goods & Services, annual balance £bn Source: IMF, UK Balance of Trade Statistics 90 92 94 96 98 00 02 04 06 08 10 12 billions -40 -30 -20 -10 0 10 Tradebalance(billions) -40 -30 -20 -10 0 10 70 80 90 100 110 ExchangeRateIndex 70 80 90 100 110 Trade balance has been negative since 1997, mainly as the result of a chronic deficit in goods trade Depreciation of sterling from 2007 to 2009

- 43. Current Account Services Net Investment Income Transfers Balance Goods Source: Statistics Commission BoP Statistics £(billions) £(billions) Trade in Goods Current account Transfers Investment income Trade in Services High trade surplus in services Trade deficit in goods now over £100bn

- 44. Seasonally adjusted, quarterly trade balance, £ billion Source: Reuters EcoWin 00 01 02 03 04 05 06 07 08 09 10 11 12 13 billions -30 -25 -20 -15 -10 -5 0 5 10 15 20 25 Sterling(£)(billions) -30 -25 -20 -15 -10 -5 0 5 10 15 20 25 Trade in services Trade in goods Key services: Business services Financial services Transport and tourism Education and Health Creative industries Research and development Key goods: Manufactured goods Oil / gas / minerals Food and drink Components Services UK is the largest service exporter in the EU

- 45. UK Balance of Trade in OilTrade Balance £bn and Brent Crude ($s per barrel) UK Trade in Oil and Brent Crude Oil Price Source: Reuters EcoWin 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 10 20 30 40 50 60 70 80 90 100 110 120 USD/Barrel 10 20 30 40 50 60 70 80 90 100 110 120 Annual average price for Brent crude oil billions -17.5 -15.0 -12.5 -10.0 -7.5 -5.0 -2.5 0.0 2.5 5.0 7.5 GBP(billions) -17.5 -15.0 -12.5 -10.0 -7.5 -5.0 -2.5 0.0 2.5 5.0 7.5 Annual UK balance of trade in oil

- 46. Trade Balance in Gas£ billion - annual value of exports and imports at constant 2006 prices Source: UK Trade Statistics 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 billions 5.0 7.5 10.0 12.5 15.0 17.5 20.0 22.5 25.0 £(billions) 5.0 7.5 10.0 12.5 15.0 17.5 20.0 22.5 25.0 Exports of Gas from the UK Imports of Gas into the UK

- 47. Trade balance in finished manufacturedTrade balance (Exports - Imports) £ billion per quarter, source: ONS UK Trade Balance in Finished Manufactured Goods Source: Reuters EcoWin 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 billions -17.5 -15.0 -12.5 -10.0 -7.5 -5.0 -2.5 0.0 GBP(billions) -17.5 -15.0 -12.5 -10.0 -7.5 -5.0 -2.5 0.0 The structural trade deficit in manufactured goods seems to have stabilised but why is the UK such a large net importer of manufactured products?

- 48. UK – EU27 Trade BalanceMonthly balance of trade in goods and services, £ billion, seasonally adjusted United Kingdom Trade Balance with EU27 Source: Reuters EcoWin 00 01 02 03 04 05 06 07 08 09 10 11 12 13 billions -6 -5 -4 -3 -2 -1 0 GBP(billions) -6 -5 -4 -3 -2 -1 0

- 49. UK – India TradeAnnual data, £ billion Source: Reuters EcoWin 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 billions -3 -2 -1 0 1 2 3 4 5 6 7 8 9 GBP(billions) -3 -2 -1 0 1 2 3 4 5 6 7 8 9 Exports to India Imports from India Annual Balance of Trade

- 50. UK China Trade£ billion per month, trade in goods and services UK, Exports to and Imports from China Source: Reuters EcoWin 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 billions 0.0 0.5 1.0 1.5 2.0 2.5 3.0 GBP(billions) 0.0 0.5 1.0 1.5 2.0 2.5 3.0 Exports to China Imports from China

- 51. Exports and Imports as Share of GDPAnnual value of UK exports as a percentage of GDP UK- Exports and Imports of Goods and Services as % of GDP Exports of goods & services, % Imports of goods & services, % Source: Euro Stat 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 %ofGDP 15 20 25 30 35 40 45 50 %ofGDP 15 20 25 30 35 40 45 50

- 52. FDI into the UK EconomyValue of external liabilities - direct and portfolio investment Foreign Investment in the UK Economy Source: Reuters EcoWin 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 thousandbillions 0.0 0.5 1.0 1.5 2.0 2.5 3.0 £(thousandbillions) 0.0 0.5 1.0 1.5 2.0 2.5 3.0 Portfolio investment Direct investment

- 53. Fiscal PolicyMeasured as a % of national income, data for 2013-14 is a forecast Source: OECD World Economic Outlook 03 04 05 06 07 08 09 10 11 12 13 14 34.0 36.0 38.0 40.0 42.0 44.0 46.0 48.0 50.0 52.0 PercentofGDP 34.0 36.0 38.0 40.0 42.0 44.0 46.0 48.0 50.0 52.0 Tax Revenue (% of GDP) Government Spending (% of GDP) The big issue in fiscal policy is fiscal austerity – i.e. Cutting the budget deficit through spending cuts and tax rises G>T = budget deficit

- 54. How much borrowing can the UK take? Source: OECD World Economic Outlook 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 -12.0 -10.0 -8.0 -6.0 -4.0 -2.0 0.0 2.0 4.0 %ofGDP -12.0 -10.0 -8.0 -6.0 -4.0 -2.0 0.0 2.0 4.0 Annual government budget balance Budget deficit Budget surplus 20 40 60 80 %ofGDP 20 40 60 80 Net Government Debt (% of GDP) Fiscal austerity as Coalition aims to cut the size of the budget deficit over the next five years – will the pain work?

- 55. monthly average 10 year bond yield, per cent, source: IMF Greece Ireland UK Spain Italy Source: IMF 08 09 10 11 12 13 0 5 10 15 20 25 30 Percent 0 5 10 15 20 25 30 The UK government can borrow money for 10 years at cheap interest rates (around 2%) – whereas the cost of borrowing for other countries is significantly higher – this gives the UK an advantage – has it been used well?

- 56. Interest on UK Government Debt£ billion at current prices, non-seasonally adjusted Interest Payable on United Kingdom Government Debt Source: Reuters EcoWin 00 01 02 03 04 05 06 07 08 09 10 11 12 £(billions) 20 25 30 35 40 45 50 £(billions) 20 25 30 35 40 45 50

- 57. Government spendingAnnual % change in government spending at constant prices, 2013 and 2014 is a forecast UK Government Spending and the Economic Cycle Real government spending Real GDP [ar 1 year] Source: OECD World Economic Outlook 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 Percent -5 -4 -3 -2 -1 0 1 2 3 4 5 Percent -5 -4 -3 -2 -1 0 1 2 3 4 5 Growth of Real GDP Growth of Govt Spending Govt spending chart does not include capital spending

- 58. The squeeze on public sector jobsPer cent, seasonally adjusted UK Public Sector Employment as % of Total Employment Source: Reuters EcoWin 00 01 02 03 04 05 06 07 08 09 10 11 12 13 millions 19.0 19.5 20.0 20.5 21.0 21.5 22.0 22.5 GBP(millions) 19.0 19.5 20.0 20.5 21.0 21.5 22.0 22.5

- 59. BRICs growth Source: International Monetary Fund Annual%changeinrealGDP Annual%changeinrealGDP China India Brazil

- 60. Germany United Kingdom Ireland Greece Spain Euro Zone Source: OECD World Economic Outlook 04 05 06 07 08 09 10 11 12 13 14 Annual%changeinrealGDP -8.0 -6.0 -4.0 -2.0 0.0 2.0 4.0 6.0 Annual%changeinrealGDP -8.0 -6.0 -4.0 -2.0 0.0 2.0 4.0 6.0

- 61. Productivity in the UKIndex of output per hour worked, whole economy, seasonally adjusted Source: Reuters EcoWin 01 02 03 04 05 06 07 08 09 10 11 12 87.5 90.0 92.5 95.0 97.5 100.0 102.5 105.0 Index 87.5 90.0 92.5 95.0 97.5 100.0 102.5 105.0 One of the puzzles of the period since the recession came to an end – why has labour productivity grown so slowly?