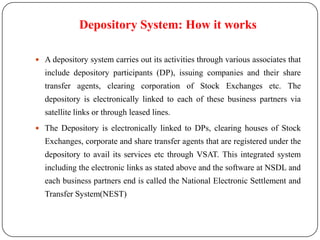

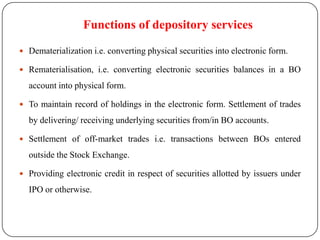

Bhaskar Joshi presented on depository services in India. A depository allows investors to hold financial assets like stocks, bonds, and mutual funds in dematerialized electronic form. There are two main depositories in India - NSDL and CDSL. Depositories operate through depository participants like banks and brokers. Benefits of the depository system include eliminating paperwork, reducing costs and risks of lost or fraudulent certificates. However, the system also introduces risks like potential for uncontrolled trading if not properly regulated. NSDL and CDSL play a key role in facilitating electronic trading of securities in the stock market.