This document discusses the concepts of leverage in financial management, including:

- Operating leverage refers to using fixed operating costs to magnify changes in profits relative to sales changes. It establishes the relationship between EBIT and sales.

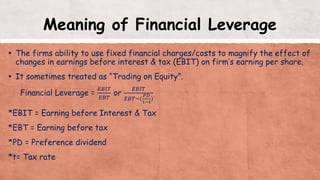

- Financial leverage refers to using fixed financial charges to magnify the effect of EBIT changes on earnings per share. It establishes the relationship between EBIT and EPS.

- Combined leverage is the product of operating leverage and financial leverage, representing the relationship between contribution and taxable income. It measures the percentage change in EPS resulting from a percentage change in sales.

- Examples are provided to illustrate how to calculate operating, financial, and combined leverage based on information about a company's sales, costs,