Download to read offline

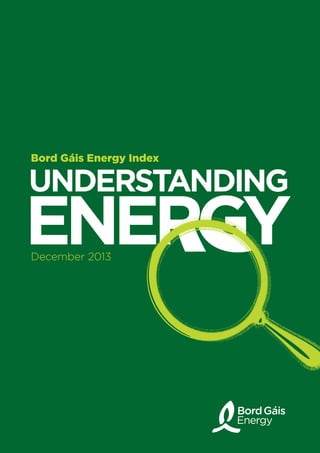

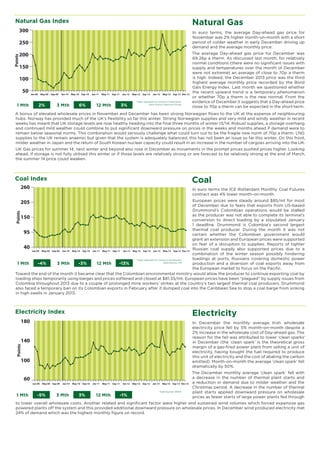

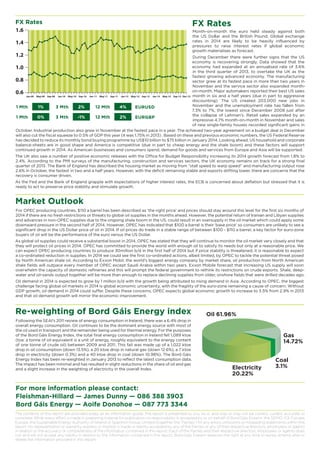

The Bord Gáis Energy Index fell 1% in December due to lower Irish wholesale electricity prices as a result of higher wind volumes which reduced costs. Brent crude oil prices were steady in December due to ongoing conflicts and supply disruptions in Libya and other regions. Natural gas and coal prices in Europe rose slightly over the month while the euro remained steady against the US dollar and British pound.