Download to read offline

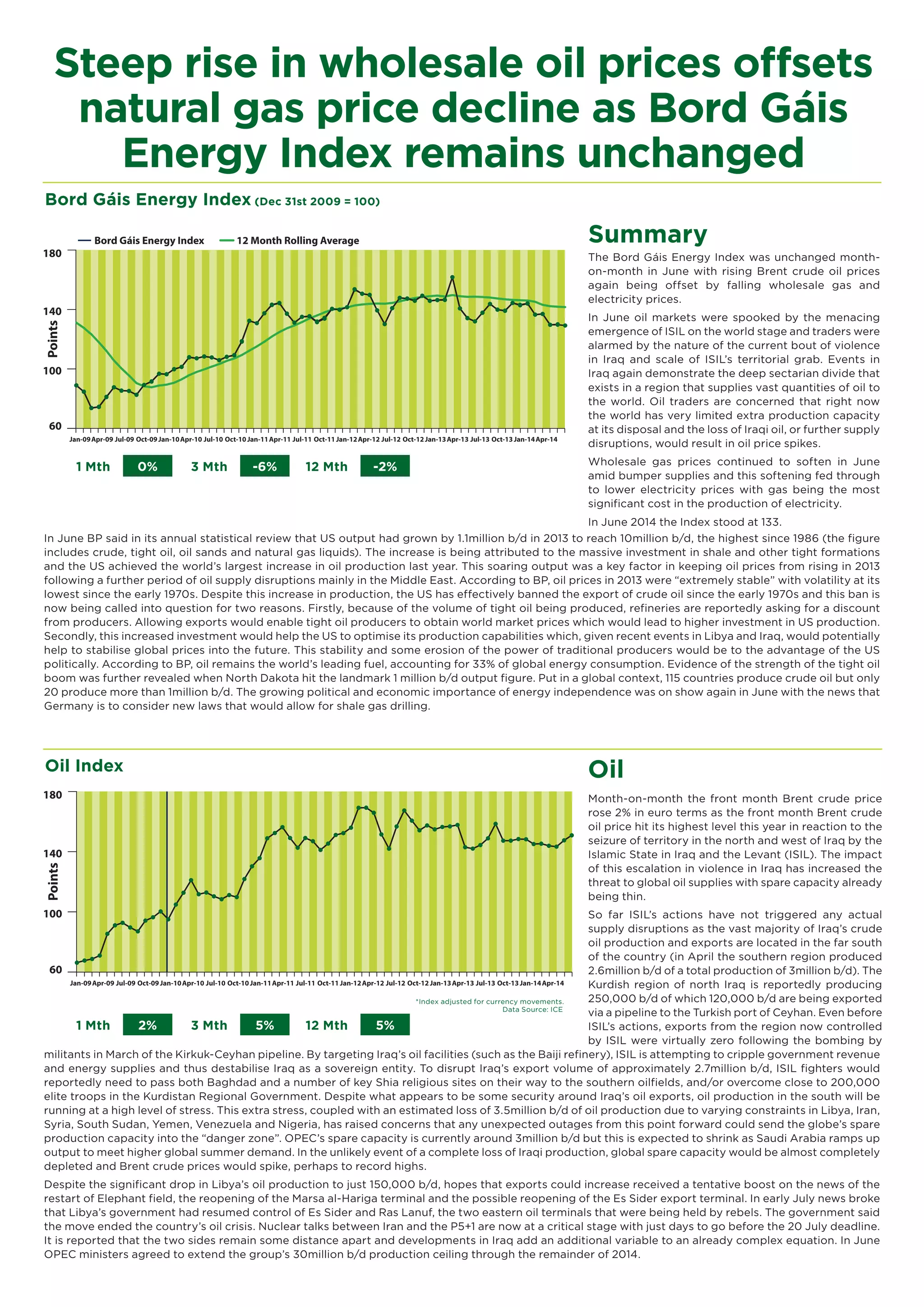

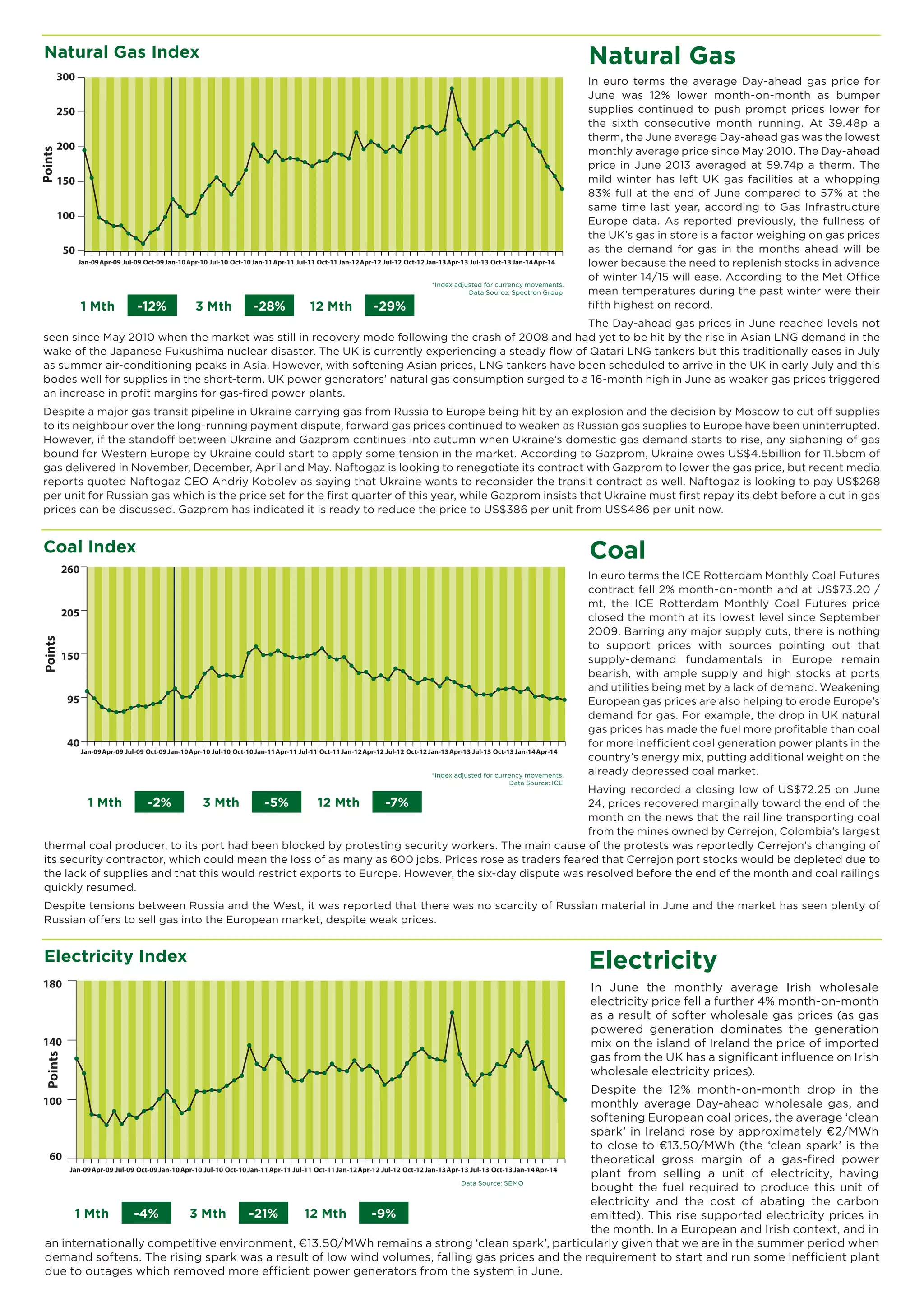

- Brent crude oil prices rose in June due to escalating violence in Iraq from the militant group ISIL seizing territory, raising concerns over global oil supply stability. However, the majority of Iraq's oil production and exports so far remain unaffected. - Wholesale natural gas and electricity prices in Europe continued to decline due to ample gas supply, offsetting the rise in oil prices and leaving the Bord Gáis Energy Index unchanged month-over-month. - Coal prices also fell slightly due to weak demand and high stockpiles in Europe.