Download as PDF, PPTX

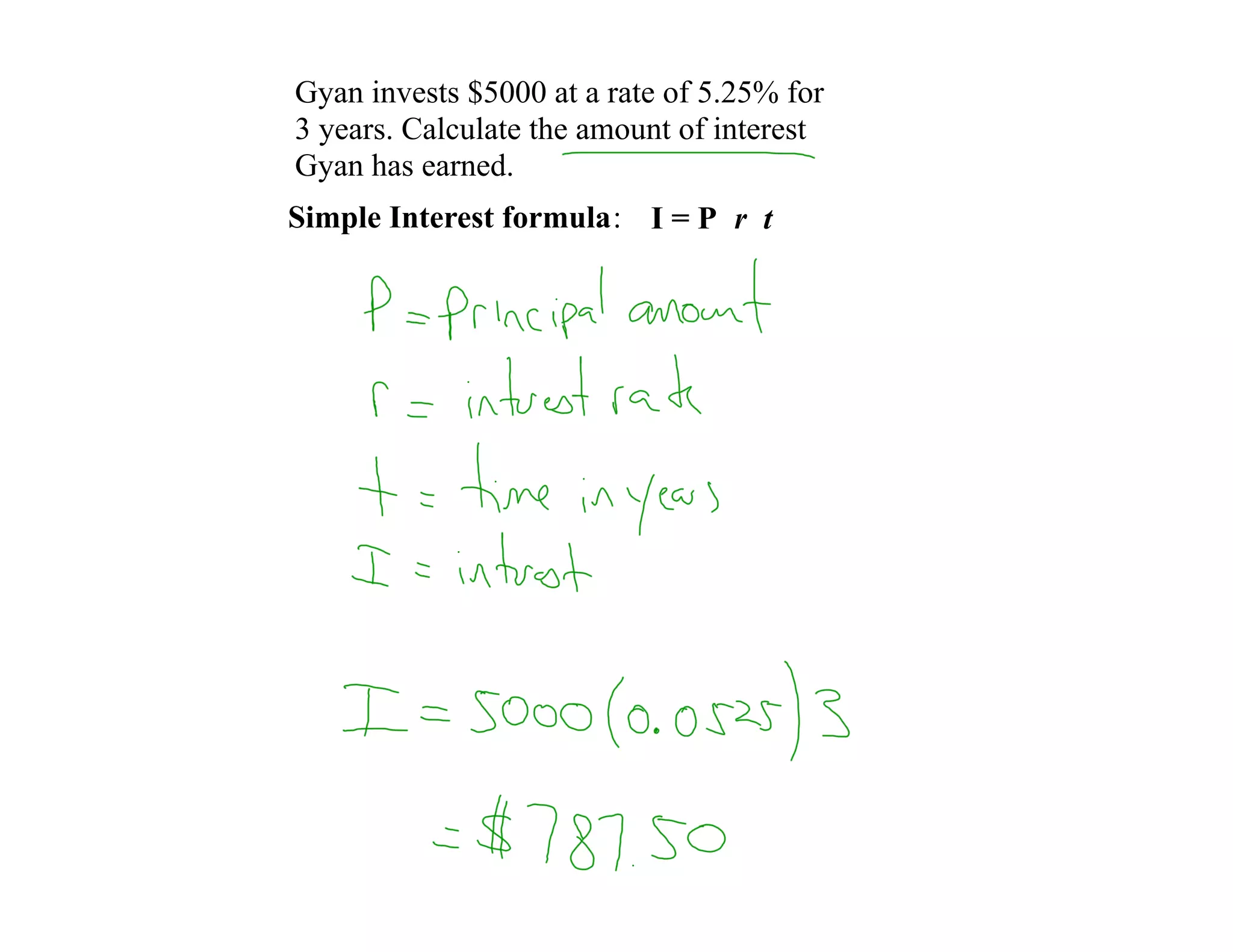

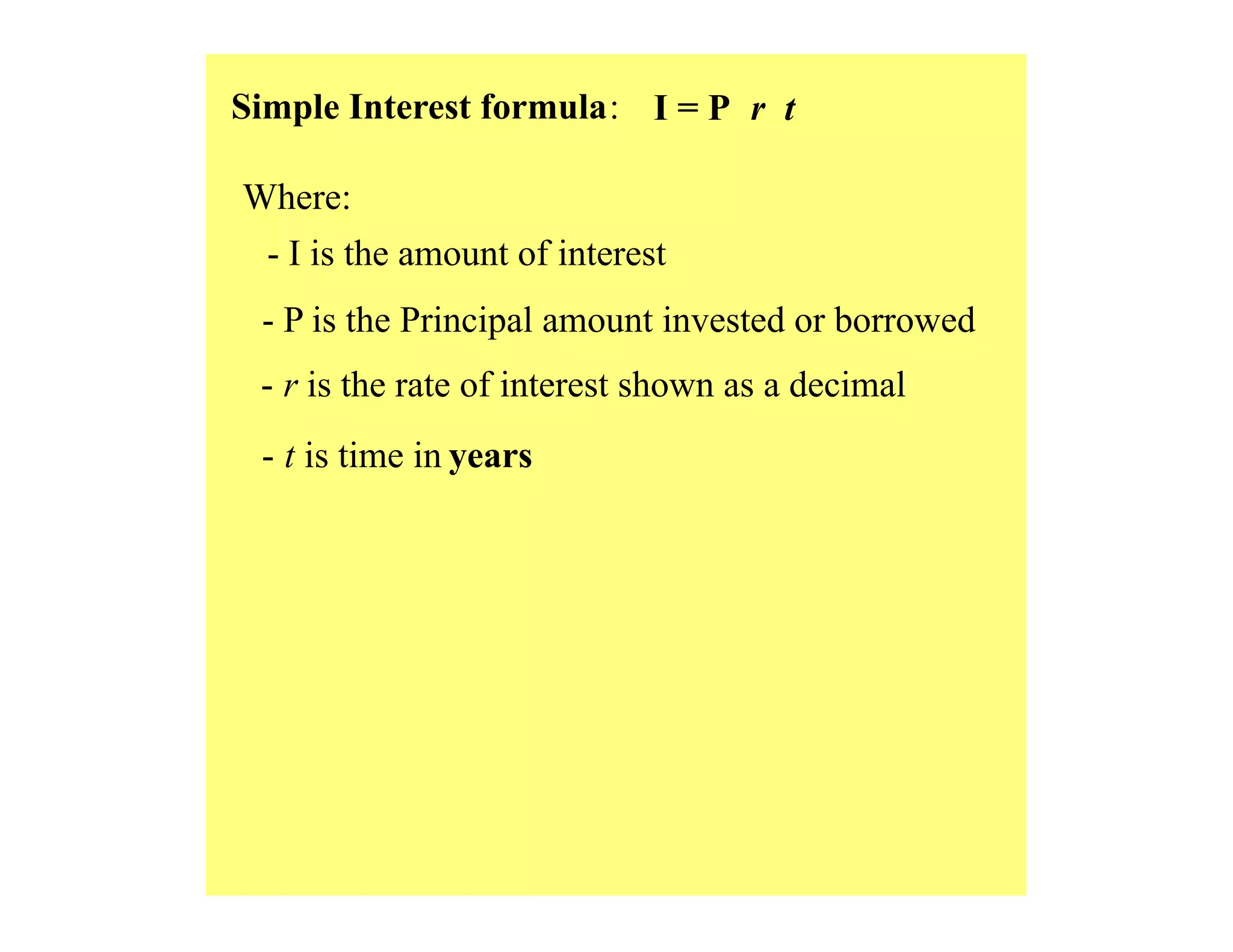

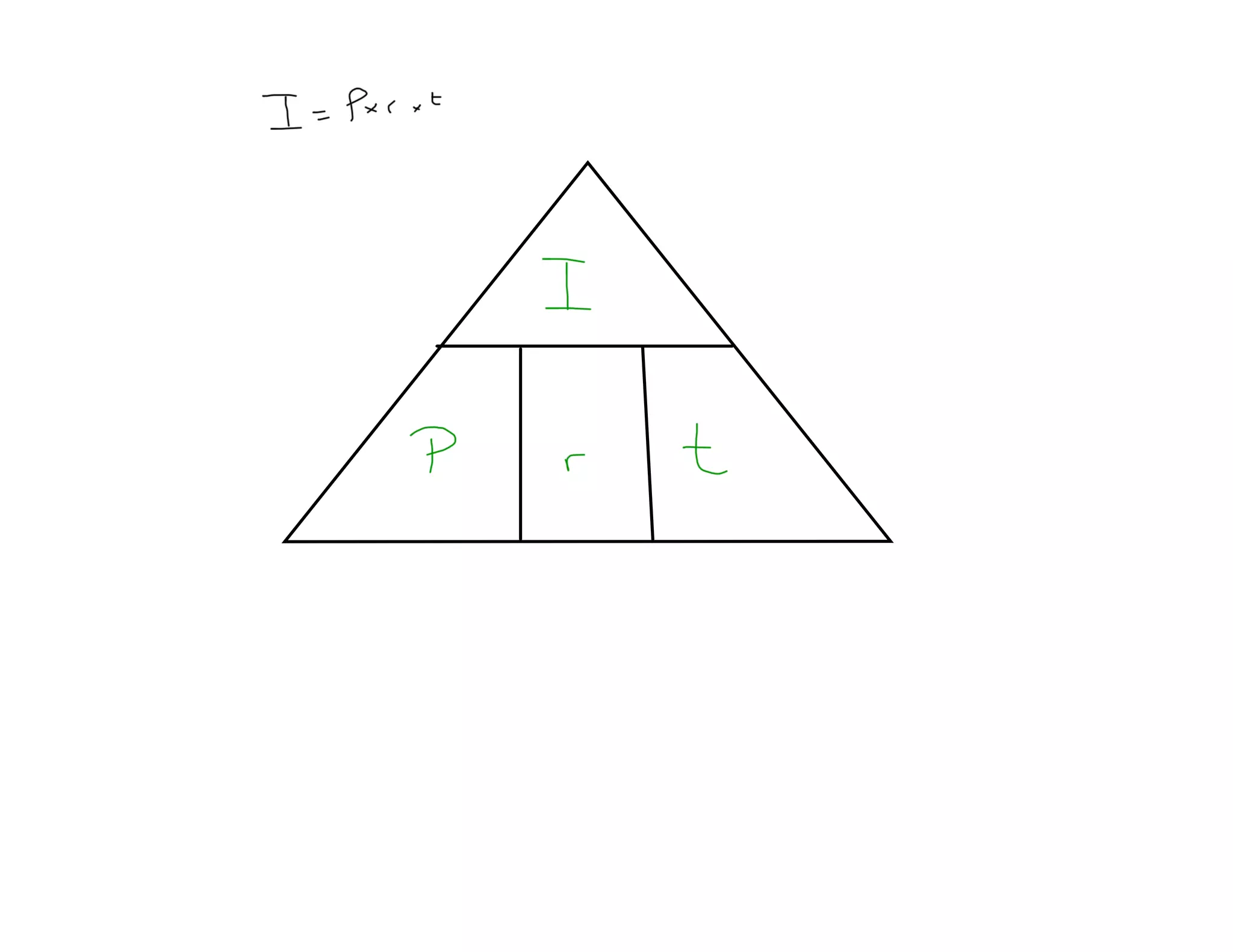

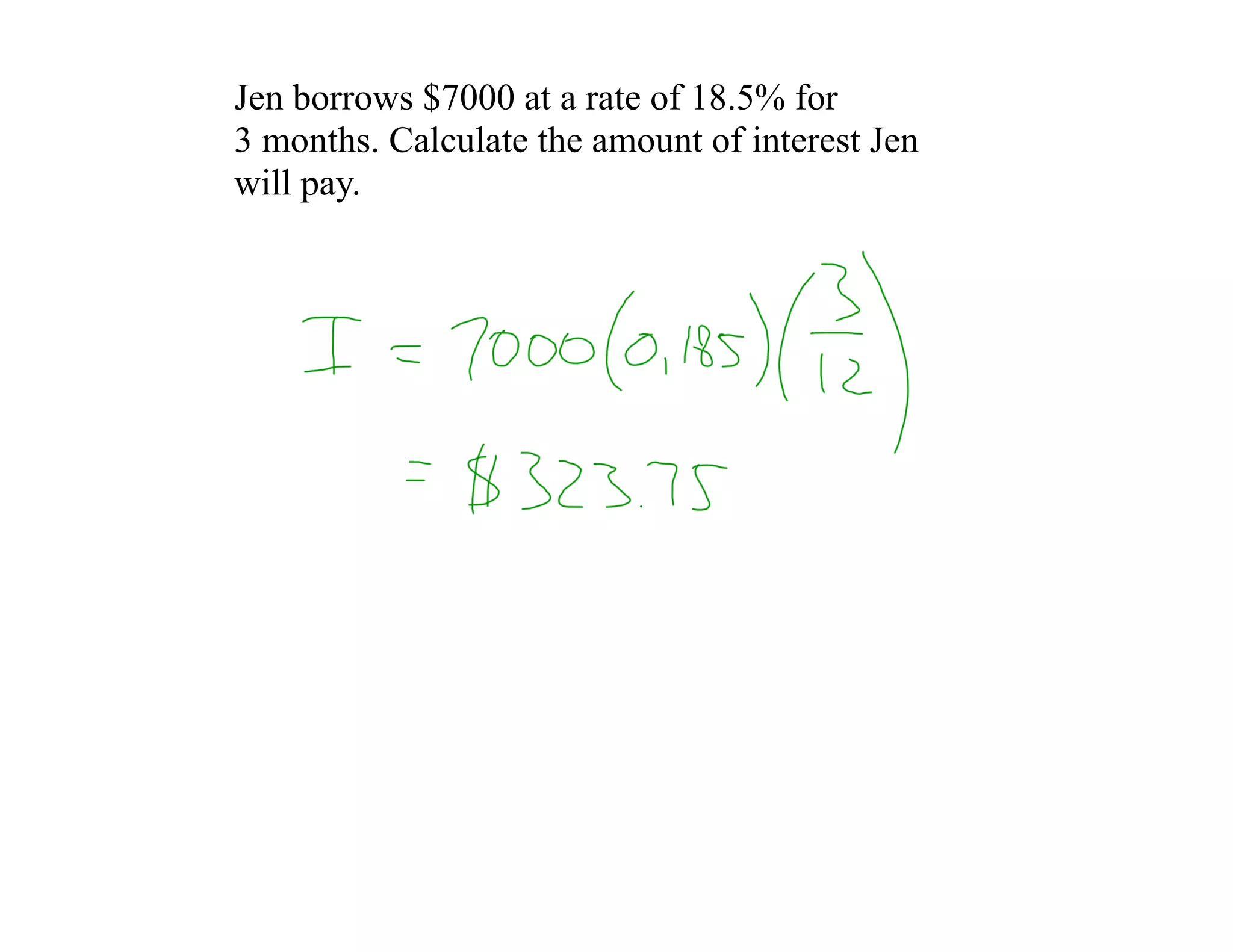

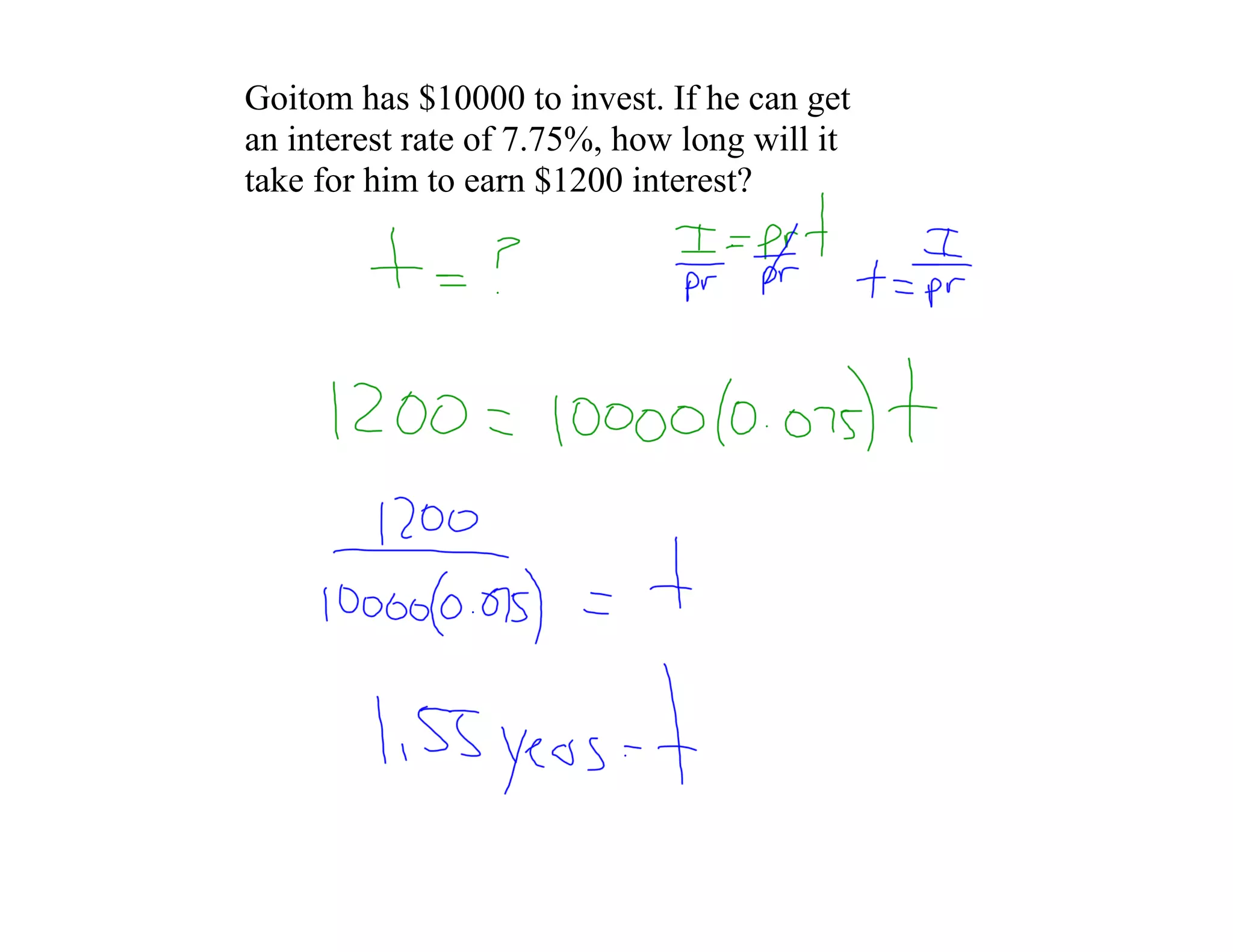

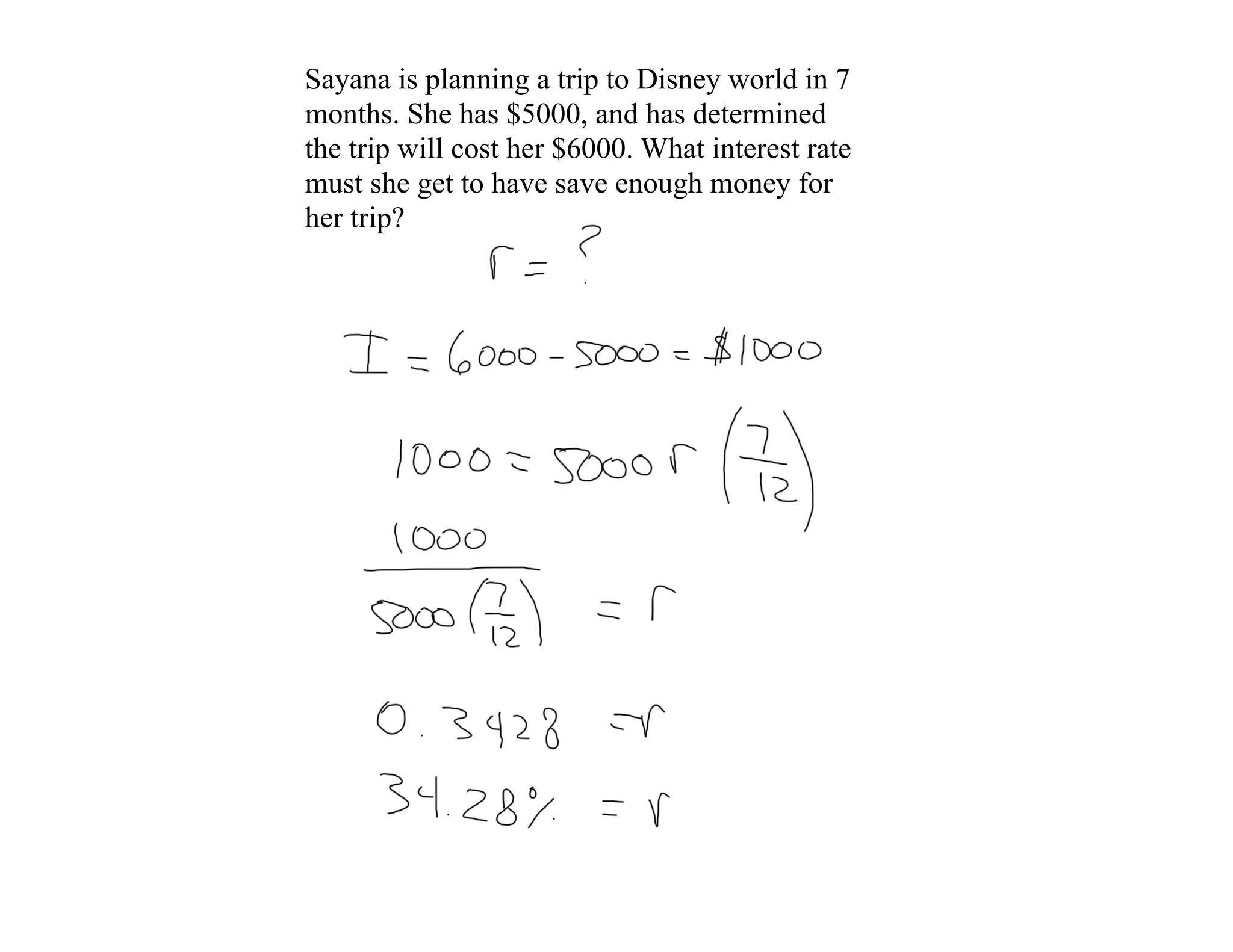

The document provides examples of simple interest rate calculations and questions. It defines the simple interest formula as I = Prt, where I is interest, P is principal, r is interest rate as a decimal, and t is time in years. It then gives examples of calculating interest for different principal amounts invested or borrowed at various rates and times. It omits questions 2b, 5, 6, and 8 from the set of exercises.