Download to read offline

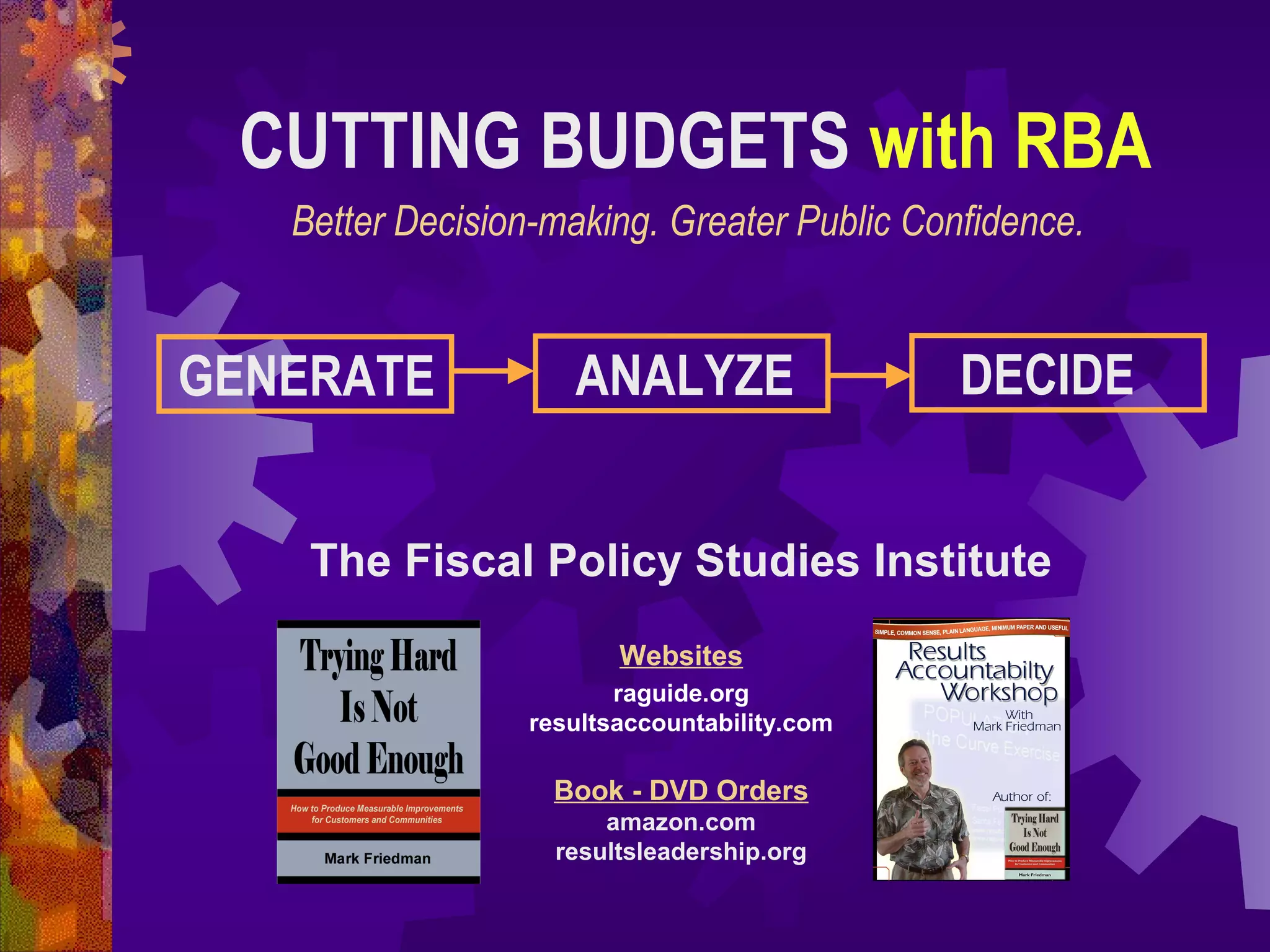

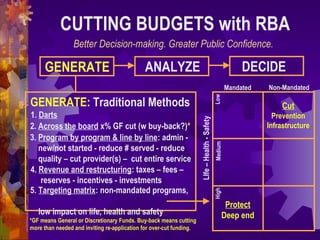

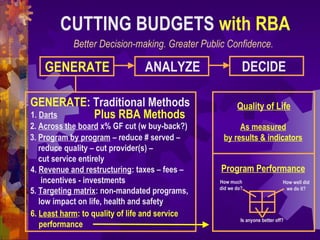

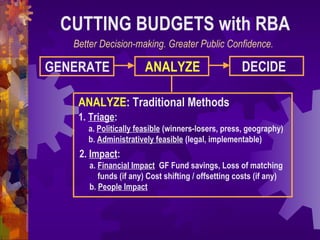

This document discusses traditional and Results Based Accountability (RBA) methods for cutting budgets. Traditional methods include across-the-board cuts, program-by-program cuts, and targeting non-mandated programs with low impacts. RBA methods involve analyzing impacts on population quality of life indicators and program performance measures, and making decisions based on minimizing harm to these outcomes. The document advocates using RBA methods to make budget cut decisions that consider public good over political interests and have greater transparency and accountability.