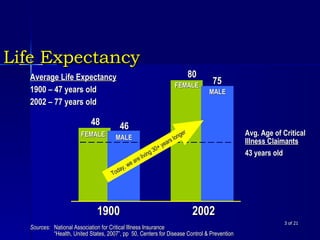

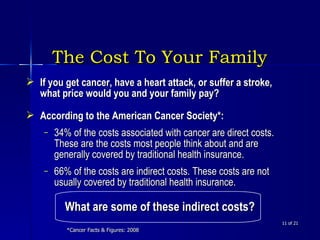

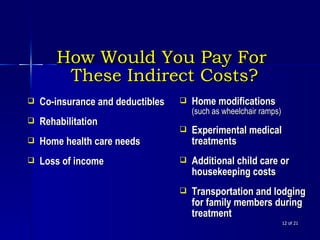

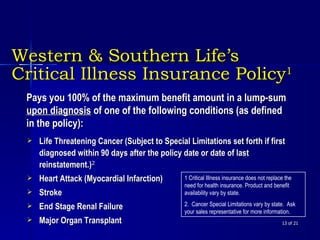

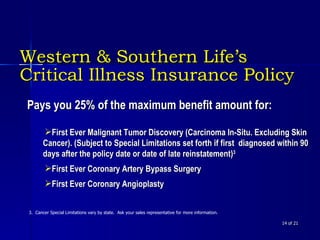

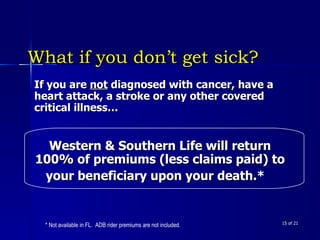

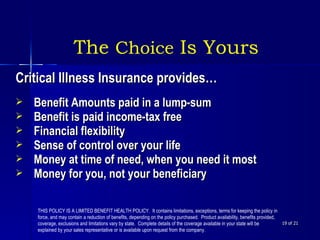

This document summarizes a presentation about critical illness insurance policies offered by Western & Southern Life Insurance Company. It outlines covered critical illnesses including cancer, heart attack, and stroke. It notes that critical illness rates have declined over time but indirect costs associated with treatment can be high, including lost income and home health care. The policy pays a lump sum benefit upon diagnosis of a covered illness to help policyholders pay expenses.