Downloaded 67 times

![magnifyAnalytic Solutions

magnify • simplify • amplify

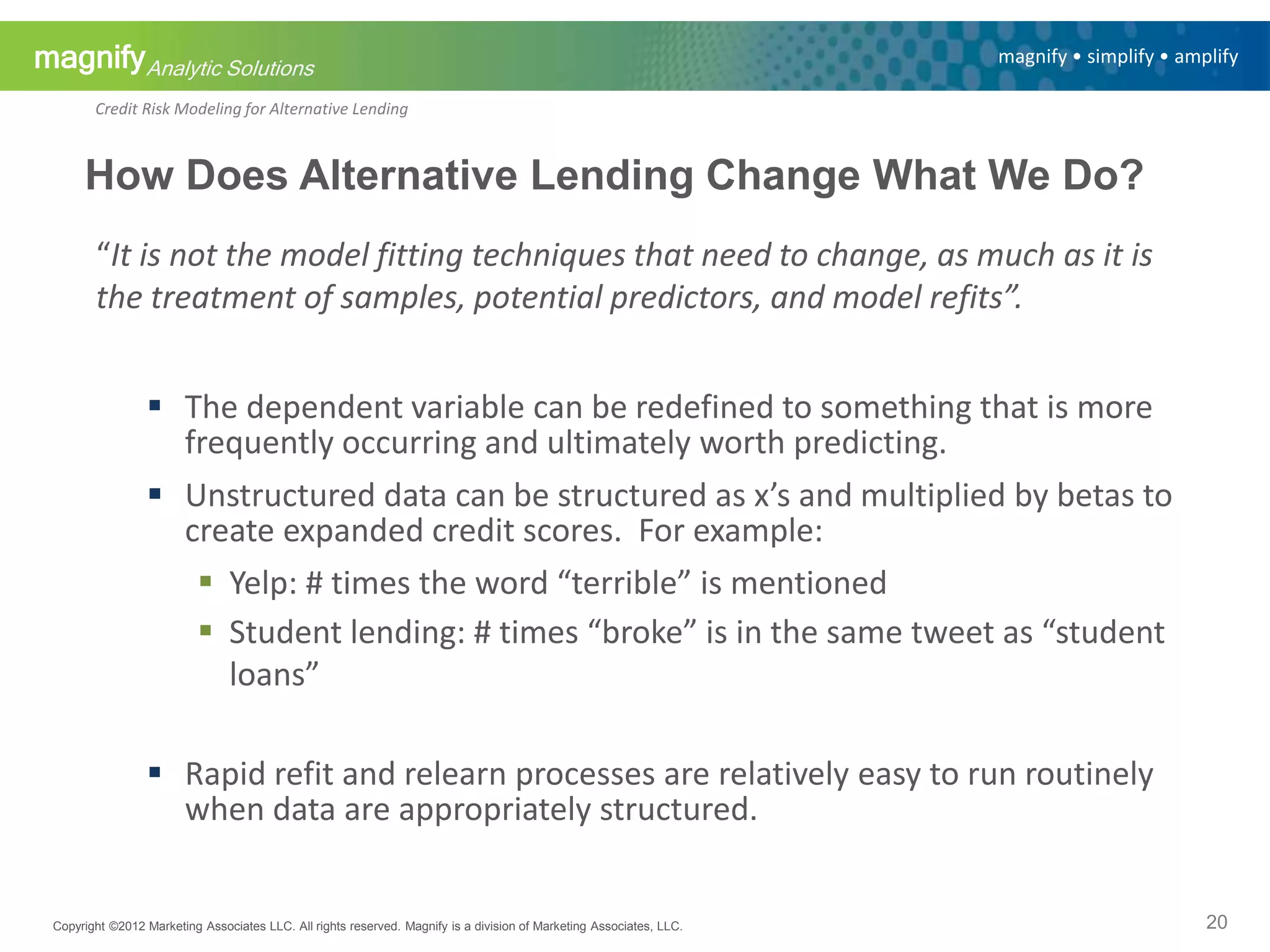

Credit Risk Modeling for Alternative Lending

Logistic regression offers the right construct for estimating risk…

Let PD = “Probability of Default”. Let Y=1 be default and Y=0 be

paid as agreed

PD is related to attributes Xk’s by taking a weighted sum of the

attributes called “xbeta” where xbeta = β0 + β1X1 + … + βnXn and

substituting xbeta into the logistic function

PD = P(Y=1|Xk) =

exp(xbeta)

1+exp(xbeta)

… the logistic function

We need to find the βk’s which best connect the Xk’s to the Y’s

If Y=1, want PD big If Y=0, want 1-PD big

Done by maximizing the likelihood function “L” as a function

of βk’s

Max [ L(β | X) = PDY (1 - PD)1-Y ]

Copyright ©2012 Marketing Associates LLC. All rights reserved. Magnify is a division of Marketing Associates, LLC.

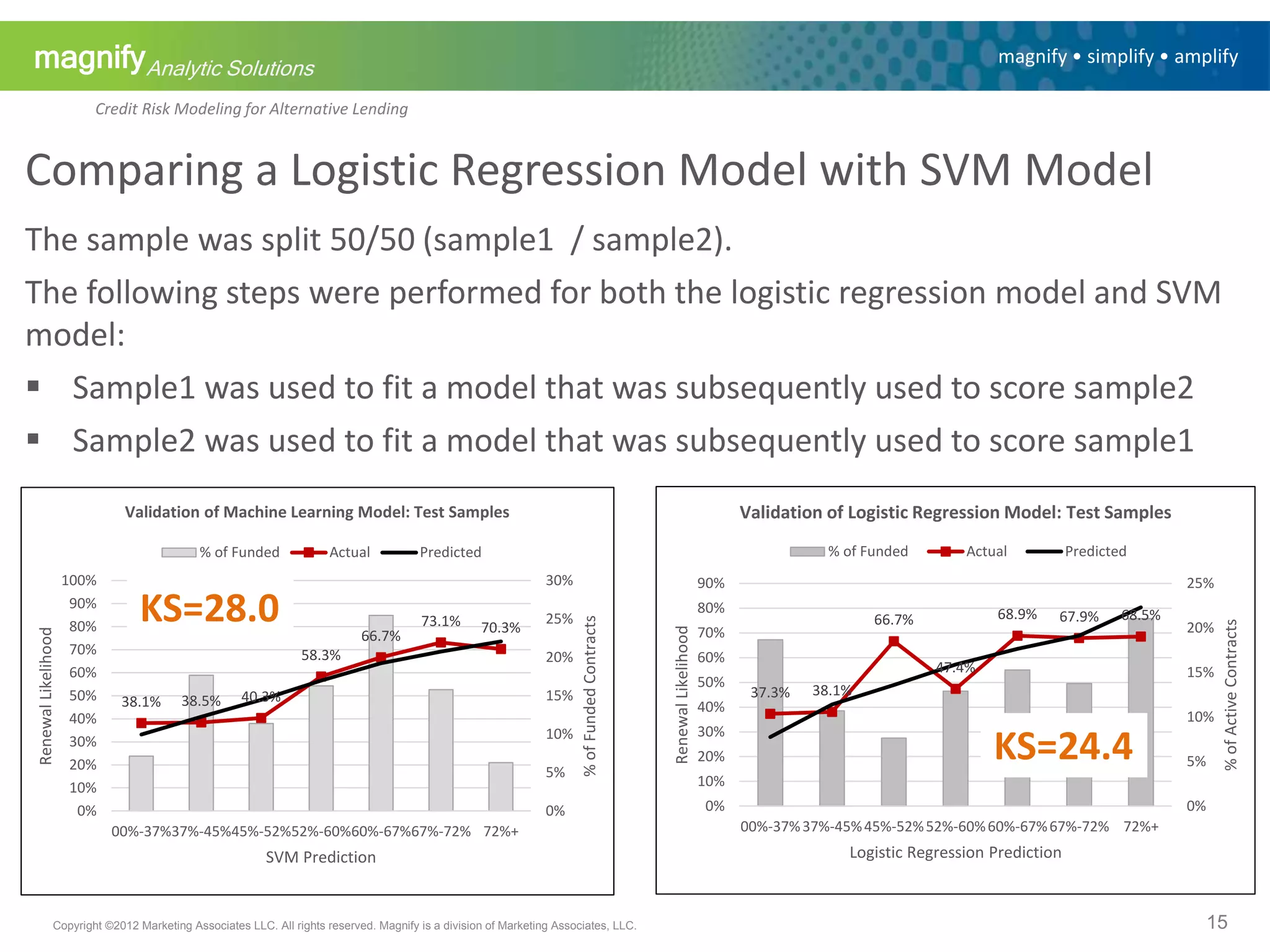

The Continued Relevance of Logistic Regression

13](https://image.slidesharecdn.com/asacsp2016shieldslund-160404165954/75/Credit-Risk-Modeling-for-Alternative-Lending-13-2048.jpg)

The document discusses credit risk modeling for alternative lending, highlighting the differences between traditional banking analytics and alternative lending analytics. Key components include the use of scorecards, cutoff scores, and the importance of logistic regression in predicting defaults. It emphasizes the need for innovative approaches in data handling and modeling to better assess risk and meet regulatory demands.

![[DSC Europe 25] Dobrica Cosic - From Electrons to Innovation: How Granular Da...](https://cdn.slidesharecdn.com/ss_thumbnails/h4qk69zereaumbceubgr-dobrica-cosic-from-electrons-to-innovation-how-granular-data-and-analytics-are--251218085301-b982fb14-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Katherine Forrest - AI NOW: Understanding the Velocity of Cha...](https://cdn.slidesharecdn.com/ss_thumbnails/wvvbruqfrci0sfq9xwgb-4-251212104007-e5ad1987-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Jean Del Rosario - How to Reduce GenAI Costs up to 73.45%.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/zjehcwqsiwjisav1znml-5-251217093201-eae4440a-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Francisco Prado Moreno - Model Validation in the Age of AI: T...](https://cdn.slidesharecdn.com/ss_thumbnails/2igqvkir1yd2yzlhoylg-3-251215095918-6676c4e6-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Uros Pesic - The Reality of AI in Marketing.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/rtkodnmtycovsllvzsyn-9-251215095918-b0c6bfe3-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Hans Kleinsman - The Compliance Gearbox: How Tax Tech Mediate...](https://cdn.slidesharecdn.com/ss_thumbnails/dxdytie1toel0hr90bjs-2-251212103250-174fdbe7-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Debmalya Biswas - Agentification: the art of transforming man...](https://cdn.slidesharecdn.com/ss_thumbnails/r5azlggvtqiaiiusrqdr-4-251212103249-5a12c89b-thumbnail.jpg?width=640&height=640&fit=bounds)