Downloaded 10 times

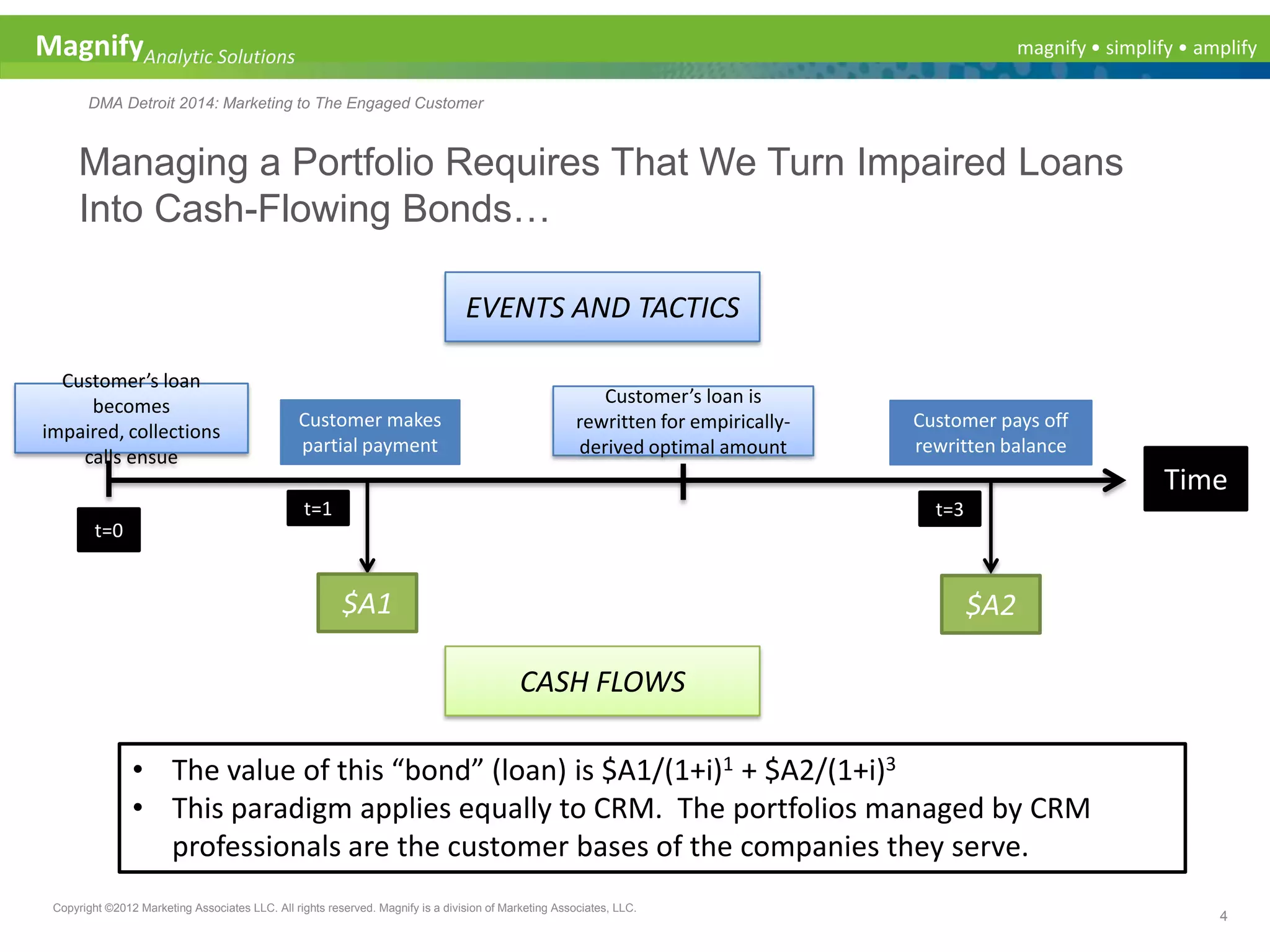

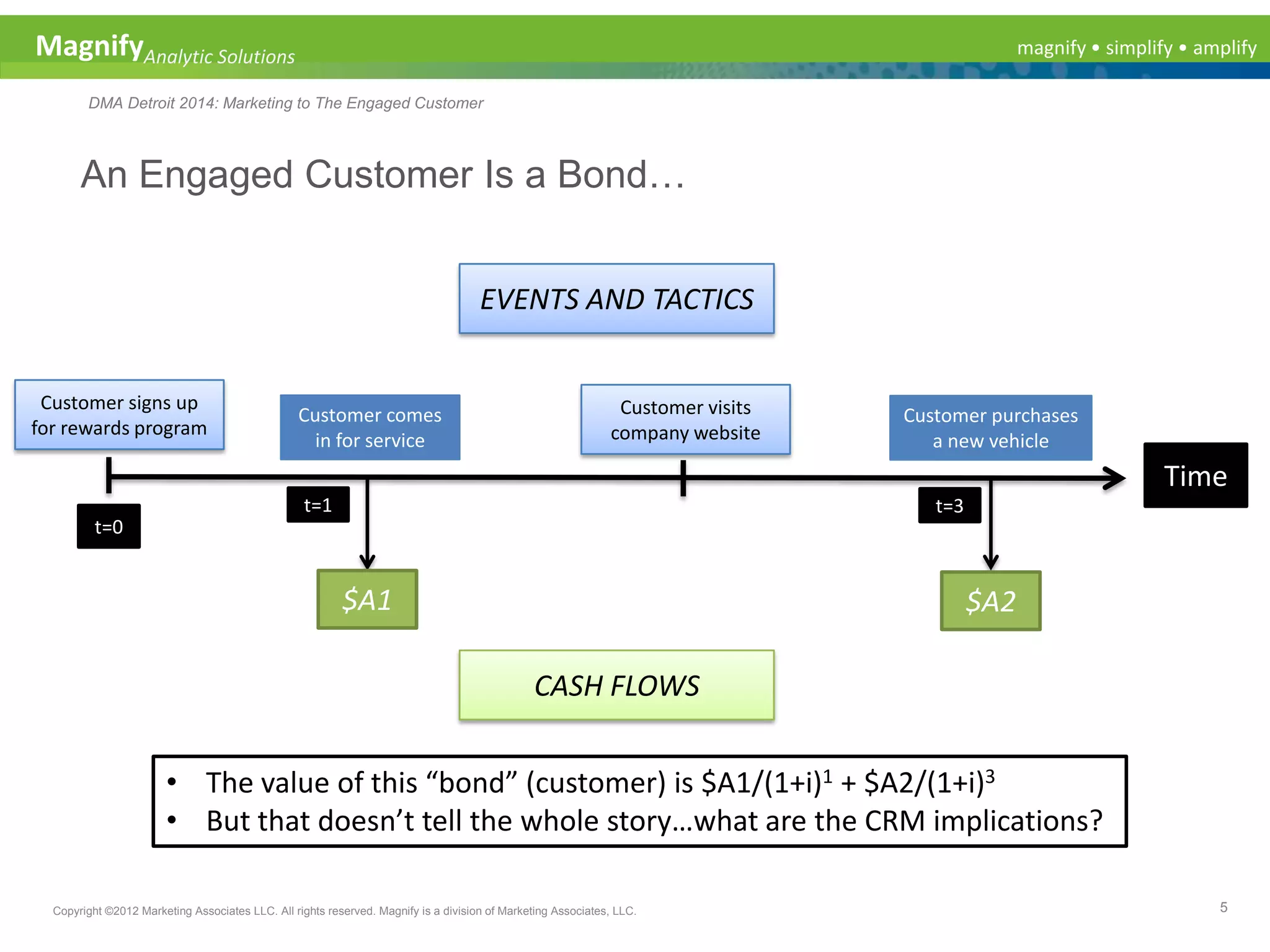

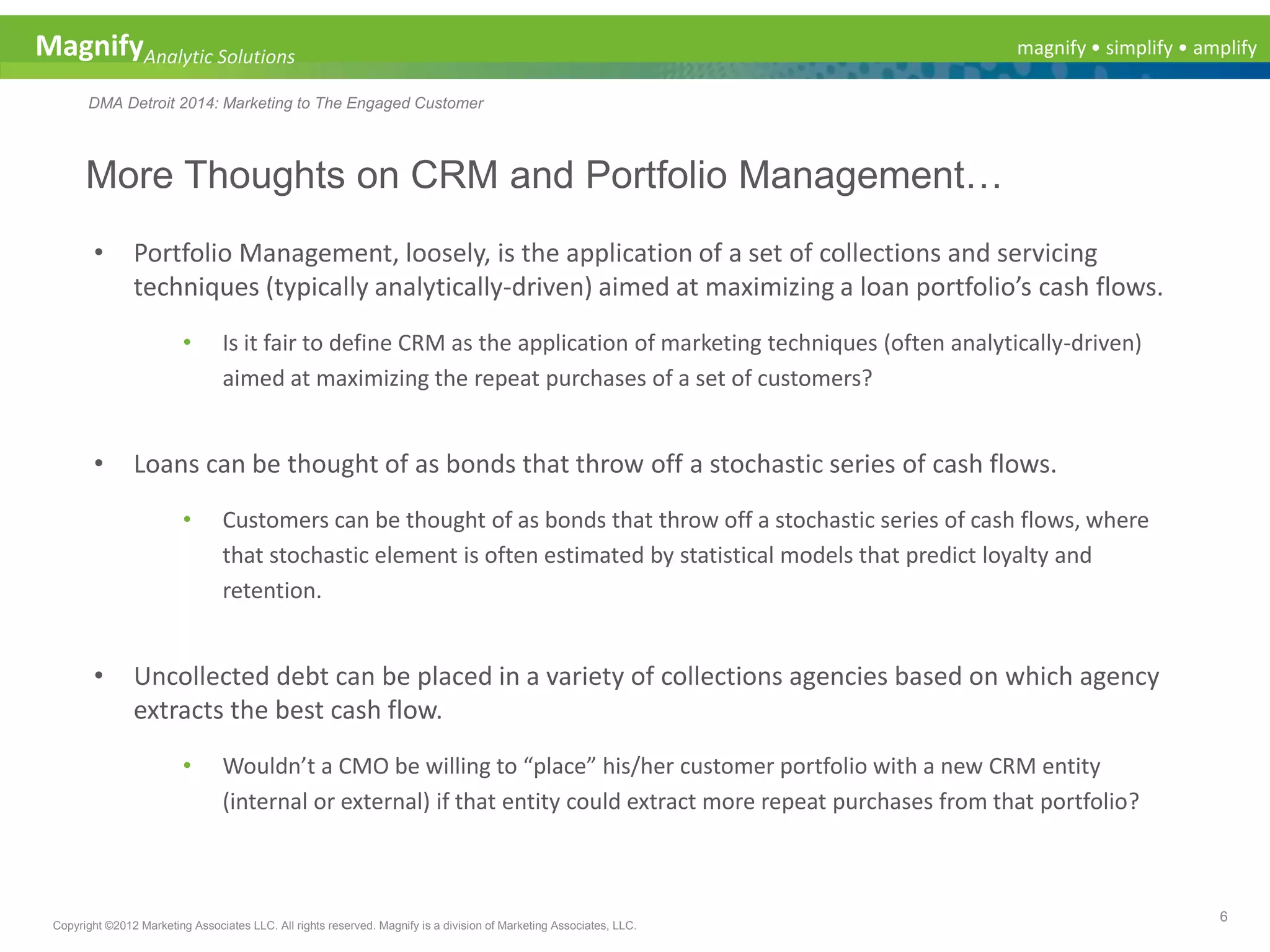

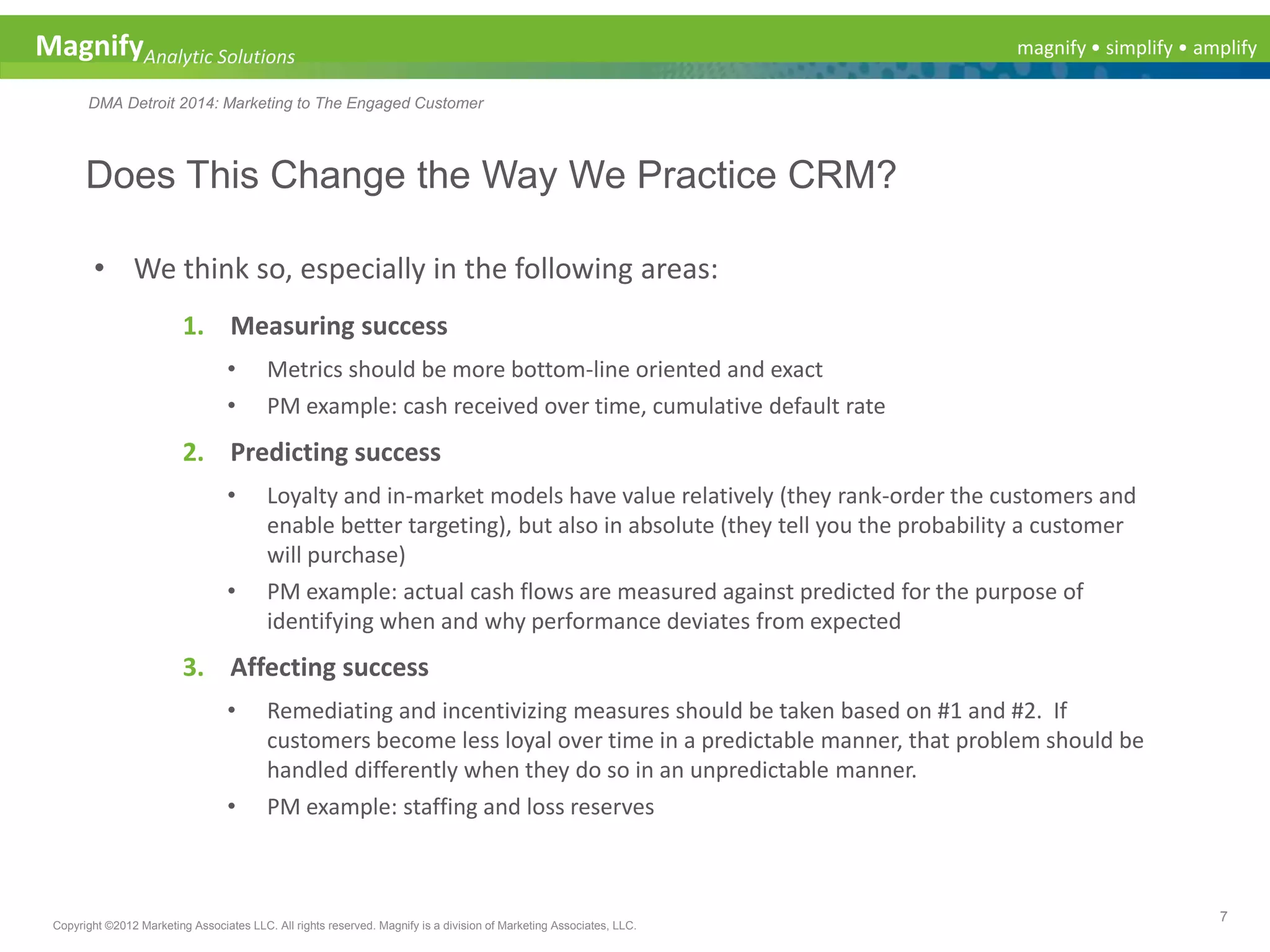

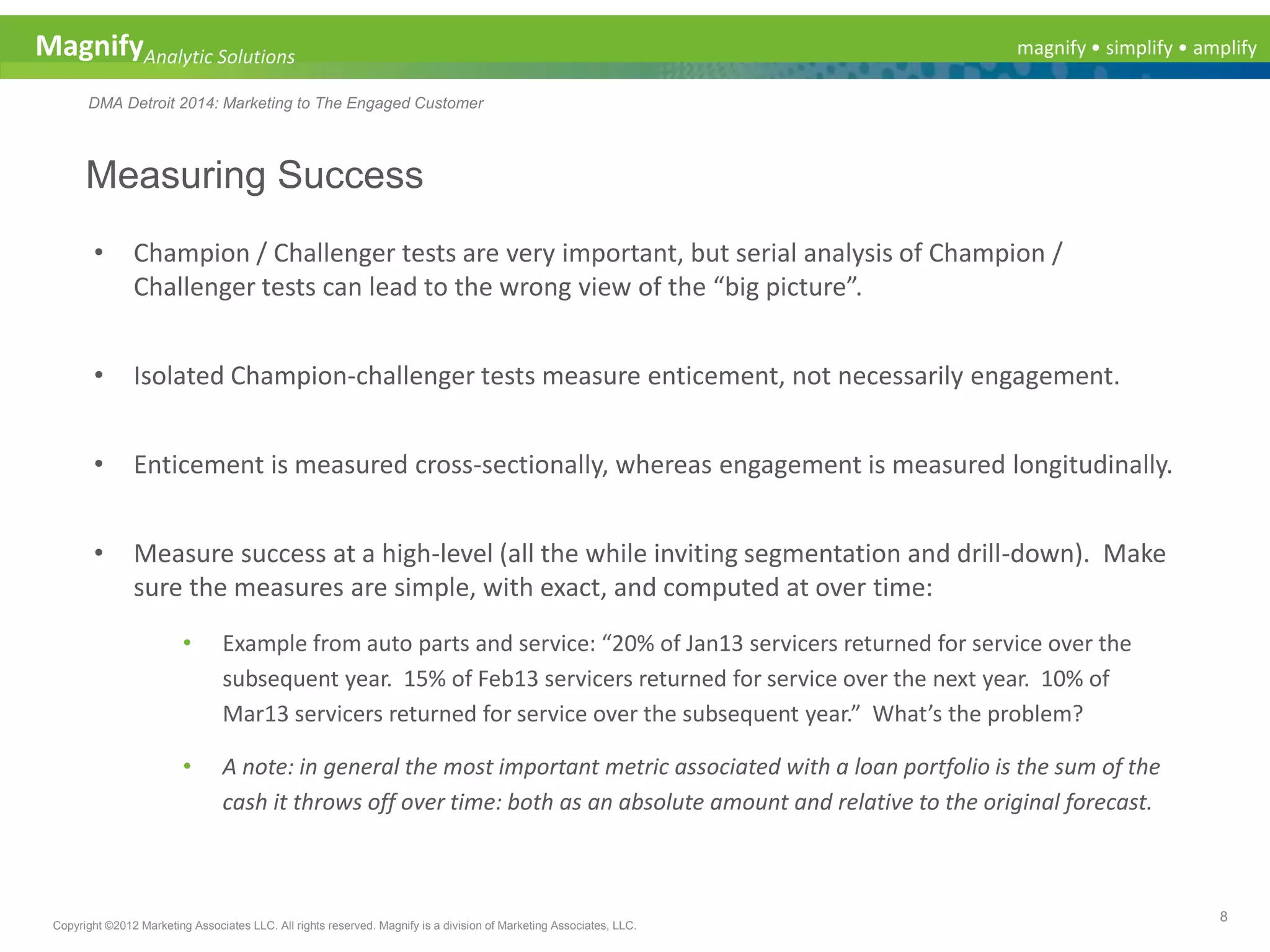

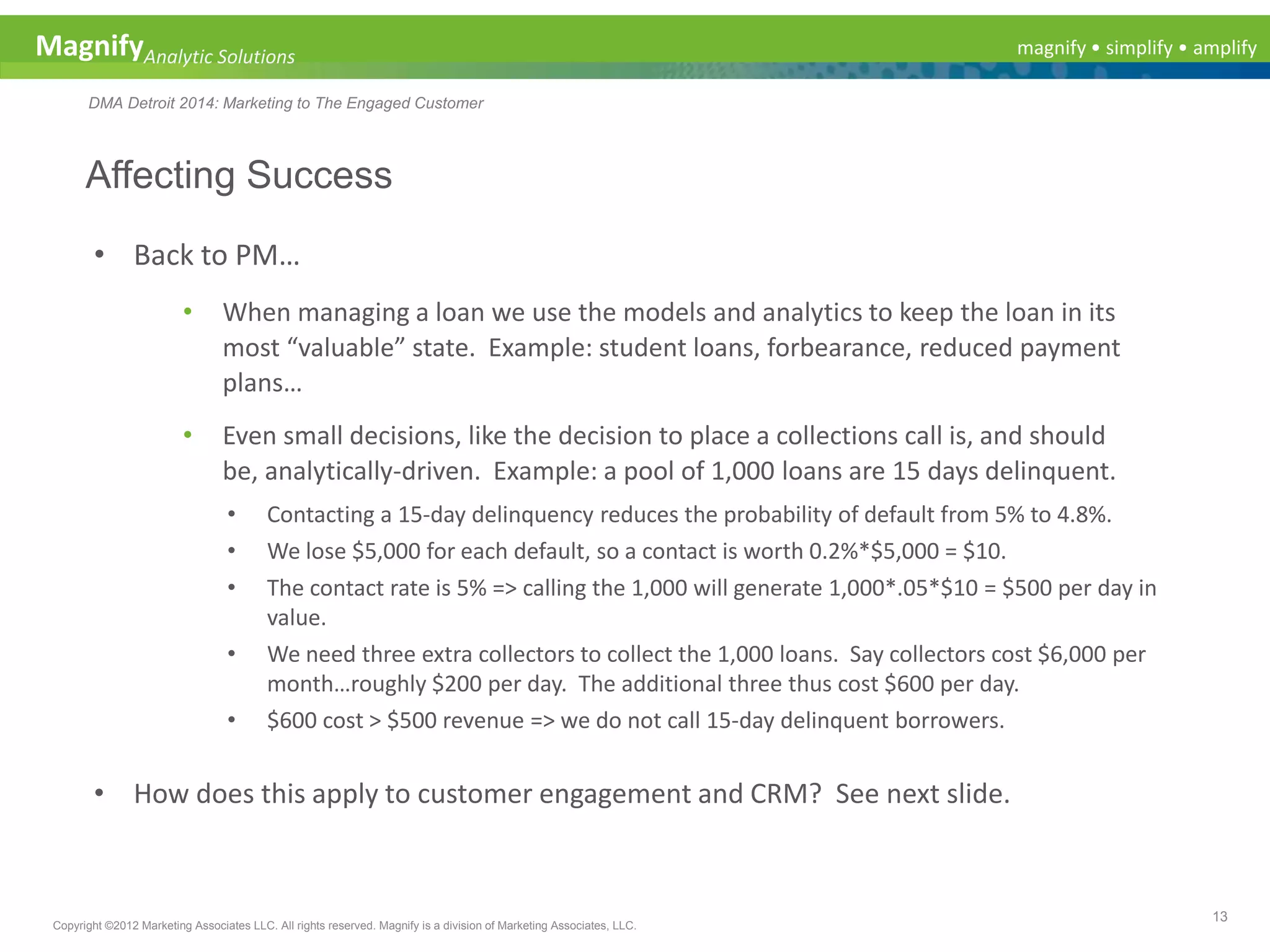

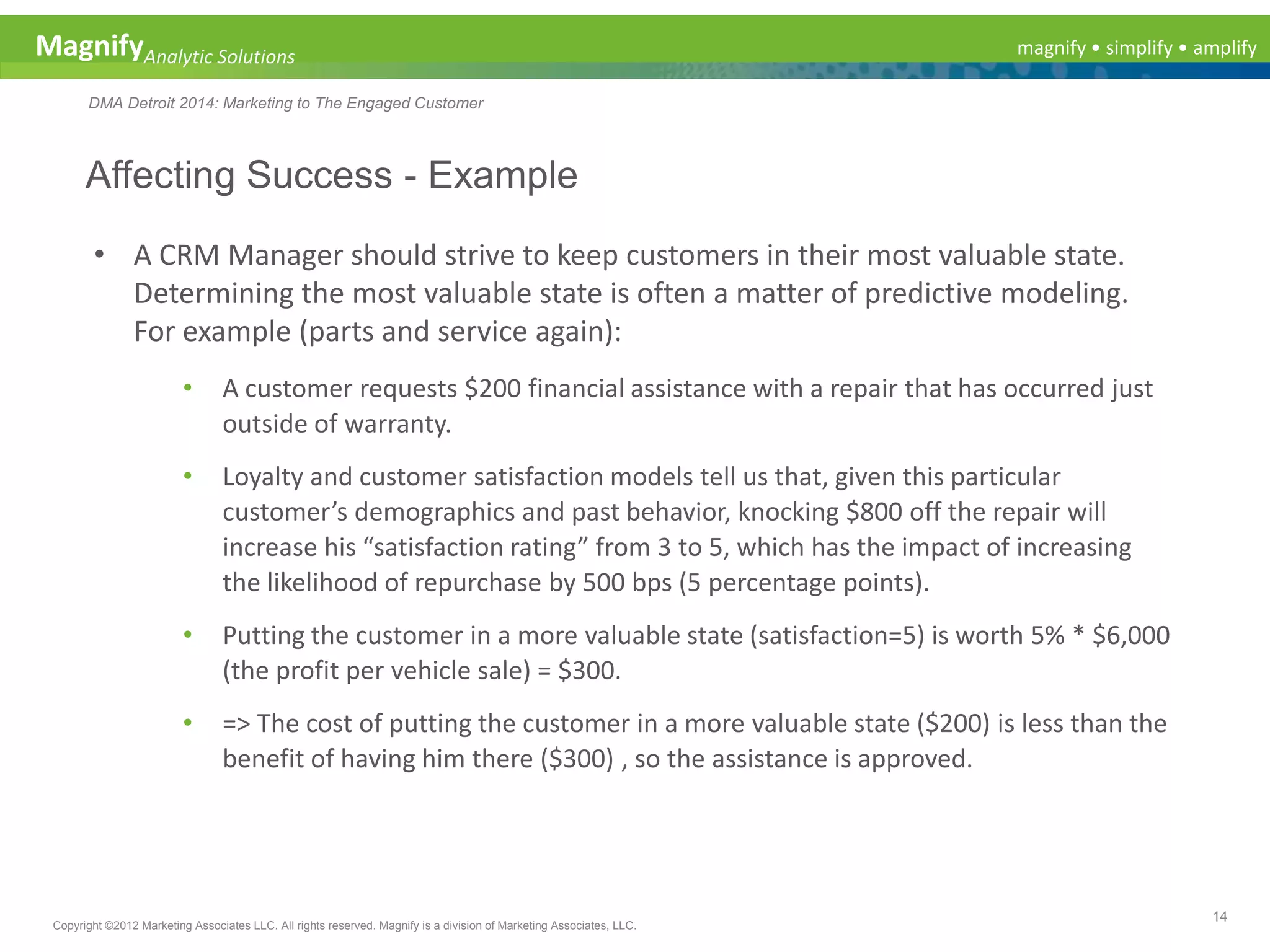

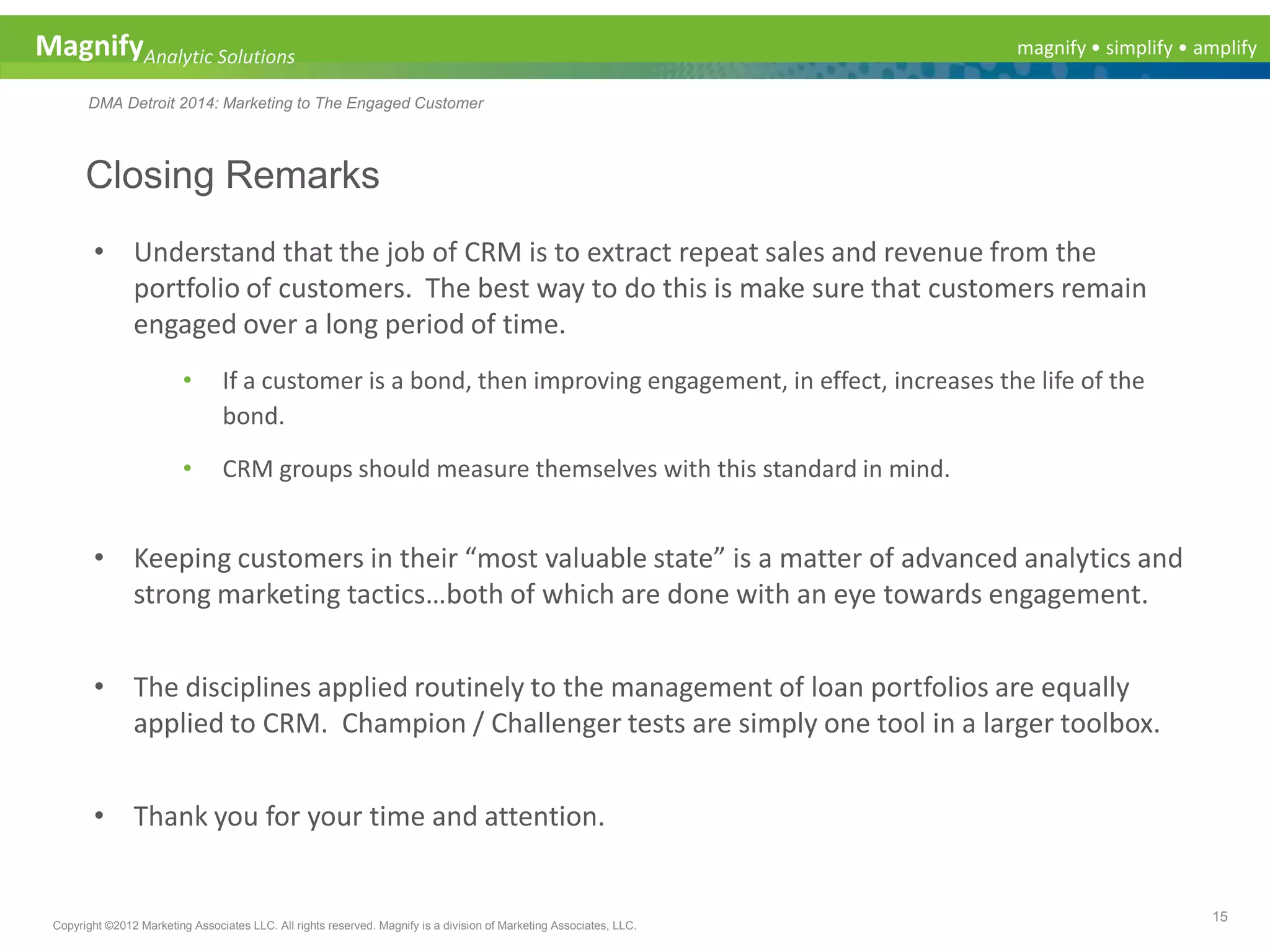

The document discusses applying portfolio management techniques used for loan portfolios to customer relationship management (CRM). It argues that customers can be viewed as bonds that generate cash flows for a company through repeat purchases and visits. This view of CRM as portfolio management aims to keep customers engaged over the long term to maximize their lifetime value. Key aspects of applying this approach include measuring CRM success longitudinally using metrics like repeat purchase rates, predicting customer behavior with loyalty models, and using analytics to determine the most valuable customer states to target with marketing.

![New Customer Acquisition Presentation[1]](https://cdn.slidesharecdn.com/ss_thumbnails/newcustomeracquisitionpresentation1-12699987508146-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Ivan Peric - Intelligence Swarm Logic and Techno-Functional M...](https://cdn.slidesharecdn.com/ss_thumbnails/7my7c97fsduiccadgavw-2-251212103249-5a03f7c6-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Debmalya Biswas - Agentification: the art of transforming man...](https://cdn.slidesharecdn.com/ss_thumbnails/r5azlggvtqiaiiusrqdr-4-251212103249-5a12c89b-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Miodrag Pesovic & Vladislav Radonjic - Federated Data Archite...](https://cdn.slidesharecdn.com/ss_thumbnails/gsbe3y5it5uhndi4e08e-1-251212103249-f1008e0c-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Ivan Petrovic - Is it really that expensive to build an AI sy...](https://cdn.slidesharecdn.com/ss_thumbnails/ybqhdwvusbg7jms3doxh-9-251216105605-7aab5a10-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Hans Kleinsman - The Compliance Gearbox: How Tax Tech Mediate...](https://cdn.slidesharecdn.com/ss_thumbnails/dxdytie1toel0hr90bjs-2-251212103250-174fdbe7-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Marko Djordjevic - AI can help Agriculture.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/c0huq0ztiubmgccem2hc-marko-djordjevic-ai-can-help-agriculture-251218125253-7606f036-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Mathias Halkjær Petersen - The AI workforce revolution.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/3xviexv7q5gojhdsyvat-the-ai-workforce-revolution-251218084820-f3c286ed-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Behzad Hosseini - AI Agents in the Wild: Deploying Models tha...](https://cdn.slidesharecdn.com/ss_thumbnails/3qtejajvsjqrzwfept2c-10-251212103250-7f2b1068-thumbnail.jpg?width=640&height=640&fit=bounds)