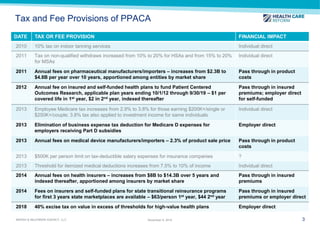

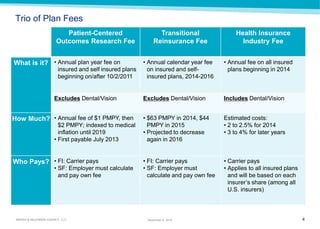

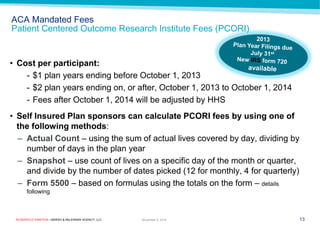

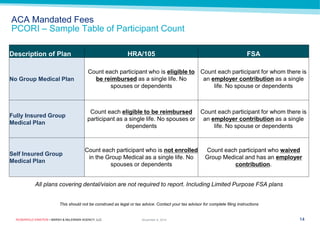

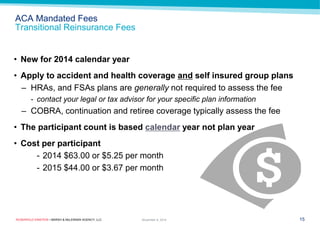

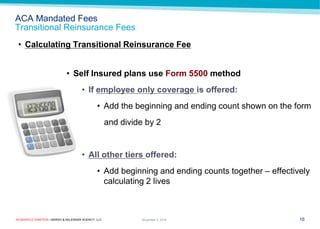

This document summarizes health care reform provisions discussed by Howard Einstein, President of Rosenfeld Einstein/A Marsh & McLennan Agency. It outlines mandated fees and reporting requirements, health plan identifiers, Medicaid expansion, individual and employer mandates, the Cadillac tax, and pay or play strategies. Specific fees and reporting deadlines are provided, including the Patient-Centered Outcomes Research Institute fee, Transitional Reinsurance fee, and Health Insurance Industry fee. Methods of calculating participant counts for fees are also summarized.

![[ON-DEMAND WEBINAR] New Year, New COVID 19 Vaccine, New Unemployment Rules, N...](https://cdn.slidesharecdn.com/ss_thumbnails/hrwebinar-january132021003-210113202803-thumbnail.jpg?width=640&height=640&fit=bounds)