This document discusses a presentation on cost-effectiveness analysis given by a group of four students. It defines cost-effectiveness analysis, explains how it differs from cost-benefit analysis, and when it is useful. It also describes what constitutes a cost in CEA and how to calculate cost-effectiveness ratios and incremental cost-effectiveness ratios. Examples are given of how to use CEA to evaluate both independent and mutually exclusive interventions. The document concludes by listing some applications of CEA and providing references.

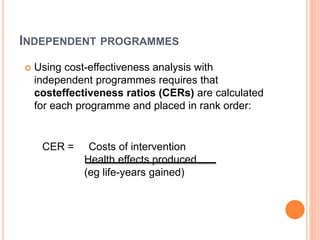

![Programm

e

Costs (£)

[C]

Effects

(life-years

gained)

[E]

Increment

al cost

[∆C]

Increment

al effect

[∆E]

ICER

[∆C/∆E]

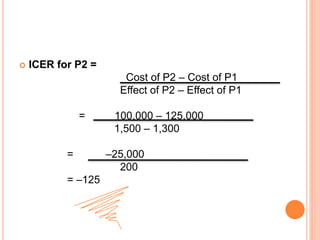

P1 125,000 1,300 125,000 1,300 96.15

P2 100,000 1,500 –25,000 200 –125

P3 160,000 2,000 60,000 500 120

P4 140,000 2,200 –20,000 200 –100

P5 170,000 2,600 30,000 400 75

Incremental cost-effectiveness ratios

Mutually exclusive interventions](https://image.slidesharecdn.com/costeffectivenessanalysis-190329224533/85/Cost-effectiveness-analysis-15-320.jpg)