Introduction

• Although thereare many contract types available to projects, most private companies and most

Government agencies typically elect to use only one contract type: the firm-fixed-price (FFP)

contract.

• The reason for this apparent disparity is the feeling of security that comes to management with

the use of FFP contacts, because;

1. you know exactly what you want to buy,

2. you can describe it in precise detail, and

3. you are not apt to later change your requirements.

• However, if you are uncertain about the requirements for a given procurement, and or, you need

flexibility due to project uncertainty, the FFP contract can be overly restrictive.

• The choice of contract type is a critical issue for both the buyer and seller. It is something which

should build on the consideration of many factors, more important issues to consider would

include the;

1. life cycle of the project,

2. the known risks facing the project,

3. Technology challenges, and of course,

4. the ability of the project to describe what it wants to buy, without later changing these requirements

3.

Major Types

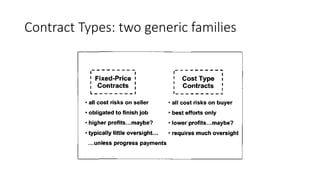

• Thefull spectrum of contract types runs from fixed-price, to cost

reimbursable, with an intermediate hybrid contract type called the

time and materials contracts.

• Each contract type has its advantages and its disadvantages.

• Also, in many cases the project may elect to use multiple contract

forms in a single relationship.

4.

Fixed price contract

•Fixed-price contracts are agreements between a buyer and a seller

where the seller agrees to provide goods or services at a

predetermined price. In these contracts, the price is fixed regardless

of the actual costs incurred by the seller during the project. Fixed-

price contracts are commonly used in various industries, including

construction, consulting, software development, and manufacturing.

• There are several types of fixed-price contracts, including:

5.

1. Firm Fixed-Price(FFP):

• In this type of contract, the price is set and remains fixed

throughout the duration of the contract, regardless of

any changes in the cost of labor, materials, or other

expenses. The seller bears the risk of cost overruns.

• A Firm Fixed-Price (FFP) contract is a type of

procurement contract where the buyer agrees to pay a

predetermined, fixed price to the seller for the goods or

services provided, regardless of the actual costs incurred

by the seller. In an FFP contract, the seller bears the risk

of any cost overruns or unforeseen expenses that may

arise during the performance of the contract.

• Key features of a Firm Fixed-Price contract include:

• Fixed Price: The contract specifies a set price for the

goods or services to be delivered. This price is agreed

upon by both parties before the start of the contract and

remains unchanged, regardless of any fluctuations in

costs or market conditions.

• Scope of Work: The contract clearly defines the scope of

work, outlining the specific deliverables, requirements,

and timelines agreed upon by both parties.

• Risk Allocation: The seller assumes the risk of cost

overruns, delays, or other performance issues. Once the

contract is signed, the seller is obligated to deliver the

goods or services at the agreed-upon price, regardless of

any unforeseen circumstances that may arise.

• Incentives for Efficiency: Since the seller bears the risk

of cost overruns, there is an inherent incentive for the

seller to complete the project efficiently and within

budget.

• Change Management: Any changes to the scope of work

or specifications outlined in the contract may require a

formal change order, with adjustments made to the

contract price and schedule as necessary.

Firm Fixed-Price contracts are commonly used in situations

where the scope of work is well-defined, and there is little

uncertainty regarding the costs and requirements of the

project. They provide both the buyer and seller with a

clear understanding of their respective obligations and

responsibilities, helping to minimize disputes and

uncertainties during contract performance.

6.

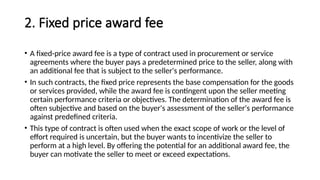

2. Fixed priceaward fee

• A fixed-price award fee is a type of contract used in procurement or service

agreements where the buyer pays a predetermined price to the seller, along with

an additional fee that is subject to the seller's performance.

• In such contracts, the fixed price represents the base compensation for the goods

or services provided, while the award fee is contingent upon the seller meeting

certain performance criteria or objectives. The determination of the award fee is

often subjective and based on the buyer's assessment of the seller's performance

against predefined criteria.

• This type of contract is often used when the exact scope of work or the level of

effort required is uncertain, but the buyer wants to incentivize the seller to

perform at a high level. By offering the potential for an additional award fee, the

buyer can motivate the seller to meet or exceed expectations.

7.

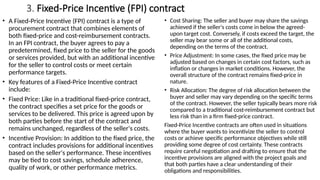

3. Fixed-Price Incentive(FPI) contract

• A Fixed-Price Incentive (FPI) contract is a type of

procurement contract that combines elements of

both fixed-price and cost-reimbursement contracts.

In an FPI contract, the buyer agrees to pay a

predetermined, fixed price to the seller for the goods

or services provided, but with an additional incentive

for the seller to control costs or meet certain

performance targets.

• Key features of a Fixed-Price Incentive contract

include:

• Fixed Price: Like in a traditional fixed-price contract,

the contract specifies a set price for the goods or

services to be delivered. This price is agreed upon by

both parties before the start of the contract and

remains unchanged, regardless of the seller's costs.

• Incentive Provision: In addition to the fixed price, the

contract includes provisions for additional incentives

based on the seller's performance. These incentives

may be tied to cost savings, schedule adherence,

quality of work, or other performance metrics.

• Cost Sharing: The seller and buyer may share the savings

achieved if the seller's costs come in below the agreed-

upon target cost. Conversely, if costs exceed the target, the

seller may bear some or all of the additional costs,

depending on the terms of the contract.

• Price Adjustment: In some cases, the fixed price may be

adjusted based on changes in certain cost factors, such as

inflation or changes in market conditions. However, the

overall structure of the contract remains fixed-price in

nature.

• Risk Allocation: The degree of risk allocation between the

buyer and seller may vary depending on the specific terms

of the contract. However, the seller typically bears more risk

compared to a traditional cost-reimbursement contract but

less risk than in a firm fixed-price contract.

Fixed-Price Incentive contracts are often used in situations

where the buyer wants to incentivize the seller to control

costs or achieve specific performance objectives while still

providing some degree of cost certainty. These contracts

require careful negotiation and drafting to ensure that the

incentive provisions are aligned with the project goals and

that both parties have a clear understanding of their

obligations and responsibilities.

8.

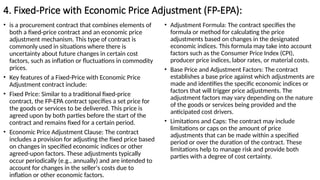

4. Fixed-Price withEconomic Price Adjustment (FP-EPA):

• is a procurement contract that combines elements of

both a fixed-price contract and an economic price

adjustment mechanism. This type of contract is

commonly used in situations where there is

uncertainty about future changes in certain cost

factors, such as inflation or fluctuations in commodity

prices.

• Key features of a Fixed-Price with Economic Price

Adjustment contract include:

• Fixed Price: Similar to a traditional fixed-price

contract, the FP-EPA contract specifies a set price for

the goods or services to be delivered. This price is

agreed upon by both parties before the start of the

contract and remains fixed for a certain period.

• Economic Price Adjustment Clause: The contract

includes a provision for adjusting the fixed price based

on changes in specified economic indices or other

agreed-upon factors. These adjustments typically

occur periodically (e.g., annually) and are intended to

account for changes in the seller's costs due to

inflation or other economic factors.

• Adjustment Formula: The contract specifies the

formula or method for calculating the price

adjustments based on changes in the designated

economic indices. This formula may take into account

factors such as the Consumer Price Index (CPI),

producer price indices, labor rates, or material costs.

• Base Price and Adjustment Factors: The contract

establishes a base price against which adjustments are

made and identifies the specific economic indices or

factors that will trigger price adjustments. The

adjustment factors may vary depending on the nature

of the goods or services being provided and the

anticipated cost drivers.

• Limitations and Caps: The contract may include

limitations or caps on the amount of price

adjustments that can be made within a specified

period or over the duration of the contract. These

limitations help to manage risk and provide both

parties with a degree of cost certainty.

9.

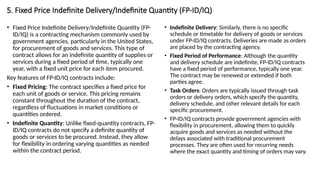

5. Fixed PriceIndefinite Delivery/Indefinite Quantity (FP-ID/IQ)

• Fixed Price Indefinite Delivery/Indefinite Quantity (FP-

ID/IQ) is a contracting mechanism commonly used by

government agencies, particularly in the United States,

for procurement of goods and services. This type of

contract allows for an indefinite quantity of supplies or

services during a fixed period of time, typically one

year, with a fixed unit price for each item procured.

Key features of FP-ID/IQ contracts include:

• Fixed Pricing: The contract specifies a fixed price for

each unit of goods or service. This pricing remains

constant throughout the duration of the contract,

regardless of fluctuations in market conditions or

quantities ordered.

• Indefinite Quantity: Unlike fixed-quantity contracts, FP-

ID/IQ contracts do not specify a definite quantity of

goods or services to be procured. Instead, they allow

for flexibility in ordering varying quantities as needed

within the contract period.

• Indefinite Delivery: Similarly, there is no specific

schedule or timetable for delivery of goods or services

under FP-ID/IQ contracts. Deliveries are made as orders

are placed by the contracting agency.

• Fixed Period of Performance: Although the quantity

and delivery schedule are indefinite, FP-ID/IQ contracts

have a fixed period of performance, typically one year.

The contract may be renewed or extended if both

parties agree.

• Task Orders: Orders are typically issued through task

orders or delivery orders, which specify the quantity,

delivery schedule, and other relevant details for each

specific procurement.

• FP-ID/IQ contracts provide government agencies with

flexibility in procurement, allowing them to quickly

acquire goods and services as needed without the

delays associated with traditional procurement

processes. They are often used for recurring needs

where the exact quantity and timing of orders may vary.

10.

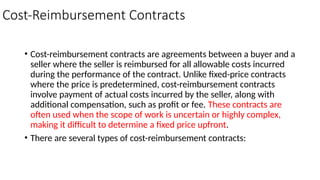

Cost-Reimbursement Contracts

• Cost-reimbursementcontracts are agreements between a buyer and a

seller where the seller is reimbursed for all allowable costs incurred

during the performance of the contract. Unlike fixed-price contracts

where the price is predetermined, cost-reimbursement contracts

involve payment of actual costs incurred by the seller, along with

additional compensation, such as profit or fee. These contracts are

often used when the scope of work is uncertain or highly complex,

making it difficult to determine a fixed price upfront.

• There are several types of cost-reimbursement contracts:

11.

1. Cost PlusFixed Fee (CPFF):

• Cost Plus Fixed Fee (CPFF) is a type of contract used in

procurement, particularly in government contracting and

sometimes in private sector contracts as well. In a CPFF

contract, the contractor is reimbursed for all allowable

costs incurred during the performance of the contract. In

addition to the reimbursement of costs, the contractor

receives a fixed fee, which is predetermined and

negotiated as part of the contract.

• Key features of CPFF contracts include:

• Reimbursement of Costs: The contractor is reimbursed

for all allowable costs incurred during the performance of

the contract. Allowable costs are typically defined in the

contract and must be reasonable, allocable, and

allowable under the applicable regulations and

guidelines.

• Fixed Fee: In addition to the reimbursement of costs, the

contractor receives a fixed fee, which is predetermined

and negotiated as part of the contract. This fixed fee

provides the contractor with a profit margin and is

intended to cover overhead, general and administrative

expenses, and profit.

• Cost Sharing: While the contractor is reimbursed for all

allowable costs, there may be provisions in the contract for cost-

sharing, where the contractor is responsible for covering a

portion of the costs. This encourages the contractor to manage

costs effectively and efficiently.

• Risk Allocation: CPFF contracts allocate certain risks between

the contractor and the contracting agency. Since the contractor

is reimbursed for all allowable costs, the contracting agency

bears the risk of cost overruns. However, the fixed fee provides

the contractor with some level of protection against fluctuations

in costs.

• Performance Incentives: CPFF contracts may include

performance incentives to encourage the contractor to meet or

exceed performance targets, such as cost, schedule, or quality

requirements. These incentives can take various forms, such as

bonuses for early completion or penalties for late delivery.

CPFF contracts are often used for projects where the scope,

schedule, or requirements are uncertain, making it difficult to

establish a fixed price at the outset. They provide flexibility for

both the contractor and the contracting agency, but also require

careful monitoring and oversight to ensure that costs are

reasonable and that the contractor is fulfilling its obligations under

the contract.

12.

2. Cost PlusIncentive Fee (CPIF)

In this contract type, the buyer agrees to reimburse

the seller for all allowable costs incurred in

performing the contract work. Additionally, the seller

receives a predetermined fee, which is structured to

provide an incentive for the seller to meet or exceed

certain performance targets.

The fee structure in a CPIF contract typically includes a

target cost, a ceiling cost, and a fee. Here's a

breakdown of these components:

• Target Cost: This is the estimated total cost of

performing the work. It serves as a baseline for cost

control and performance evaluation. The seller's

reimbursement is based on actual costs incurred,

but it cannot exceed the target cost.

• Ceiling Cost: This is the maximum allowable cost

that the buyer will reimburse. If the actual costs

exceed the ceiling cost, the seller is responsible for

covering the overruns. The ceiling cost provides a

cap on the buyer's financial liability.

• Fee: The fee is the incentive portion of the contract. It is

a predetermined amount that the seller will receive in

addition to reimbursement for costs. The fee is typically

structured such that the seller receives additional

compensation if certain performance targets are met or

exceeded. Conversely, if the actual costs exceed the

target cost, the fee may be reduced or eliminated.

The incentive structure of a CPIF contract encourages the

seller to control costs and deliver the project efficiently. If

the seller completes the work under budget or ahead of

schedule, they stand to earn a higher fee, thus providing

motivation for cost savings and performance

improvement. However, if the seller fails to meet the

performance targets or exceeds the ceiling cost, it may

result in reduced or no additional fee.

CPIF contracts are commonly used in situations where the

scope of work is uncertain or where the buyer wants to

incentivize the seller to achieve specific performance goals

while maintaining cost control. They provide a balance of

risk and reward for both parties involved in the contract.

13.

3. Cost PlusAward Fee (CPAF)

• It is another type of contract used in procurement and

project management. Similar to the Cost Plus Incentive Fee

(CPIF) contract, it involves the reimbursement of allowable

costs incurred by the seller, along with an additional fee.

However, in a CPAF contract, the fee is not predetermined

but is instead determined at the discretion of the buyer

based on the seller's performance.

• Here's how a CPAF contract typically works:

• Allowable Costs: The buyer agrees to reimburse the seller

for all allowable costs incurred in performing the contract

work. These costs may include labor, materials, overhead,

and other expenses directly related to the project.

• Award Fee Pool: Instead of a predetermined fee, the buyer

establishes an award fee pool. This pool of funds is set

aside to provide additional compensation to the seller

based on their performance.

• Performance Evaluation: Throughout the duration of the

contract, the buyer evaluates the seller's performance

against predetermined criteria or performance metrics.

These criteria may include factors such as quality,

timeliness, innovation, and cooperation.

• Award Fee Determination: At specified intervals, typically at the end

of performance periods (e.g., months or quarters), the buyer

assesses the seller's performance and determines the award fee to

be paid. The determination of the award fee is based on the buyer's

subjective evaluation of the seller's performance against the

established criteria.

• Award Fee Payment: Based on the evaluation, the buyer may award

a portion of the award fee pool to the seller. The amount awarded is

intended to incentivize exceptional performance and encourage the

seller to exceed the minimum requirements of the contract.

• Feedback and Improvement: The award fee process provides

feedback to the seller, highlighting areas of strength and areas

needing improvement. This feedback loop can help foster

continuous improvement and collaboration between the buyer and

the seller.

CPAF contracts are often used when the buyer seeks to incentivize

superior performance or when the project involves significant

complexity or innovation. By tying a portion of the seller's

compensation to their performance, CPAF contracts aim to promote

accountability, excellence, and alignment of interests between the

parties involved. However, the subjective nature of award fee

determinations can sometimes lead to disagreements or disputes

between the buyer and the seller. Therefore, it's essential for both

parties to have a clear understanding of the evaluation criteria and

expectations outlined in the contract.

14.

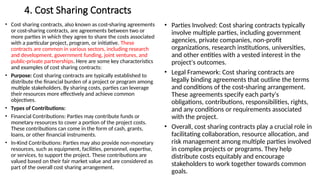

4. Cost SharingContracts

• Cost sharing contracts, also known as cost-sharing agreements

or cost-sharing contracts, are agreements between two or

more parties in which they agree to share the costs associated

with a particular project, program, or initiative. These

contracts are common in various sectors, including research

and development, government funding, joint ventures, and

public-private partnerships. Here are some key characteristics

and examples of cost sharing contracts:

• Purpose: Cost sharing contracts are typically established to

distribute the financial burden of a project or program among

multiple stakeholders. By sharing costs, parties can leverage

their resources more effectively and achieve common

objectives.

• Types of Contributions:

• Financial Contributions: Parties may contribute funds or

monetary resources to cover a portion of the project costs.

These contributions can come in the form of cash, grants,

loans, or other financial instruments.

• In-Kind Contributions: Parties may also provide non-monetary

resources, such as equipment, facilities, personnel, expertise,

or services, to support the project. These contributions are

valued based on their fair market value and are considered as

part of the overall cost sharing arrangement.

• Parties Involved: Cost sharing contracts typically

involve multiple parties, including government

agencies, private companies, non-profit

organizations, research institutions, universities,

and other entities with a vested interest in the

project's outcomes.

• Legal Framework: Cost sharing contracts are

legally binding agreements that outline the terms

and conditions of the cost-sharing arrangement.

These agreements specify each party's

obligations, contributions, responsibilities, rights,

and any conditions or requirements associated

with the project.

• Overall, cost sharing contracts play a crucial role in

facilitating collaboration, resource allocation, and

risk management among multiple parties involved

in complex projects or programs. They help

distribute costs equitably and encourage

stakeholders to work together towards common

goals.

15.

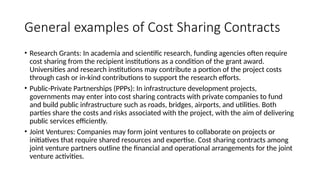

General examples ofCost Sharing Contracts

• Research Grants: In academia and scientific research, funding agencies often require

cost sharing from the recipient institutions as a condition of the grant award.

Universities and research institutions may contribute a portion of the project costs

through cash or in-kind contributions to support the research efforts.

• Public-Private Partnerships (PPPs): In infrastructure development projects,

governments may enter into cost sharing contracts with private companies to fund

and build public infrastructure such as roads, bridges, airports, and utilities. Both

parties share the costs and risks associated with the project, with the aim of delivering

public services efficiently.

• Joint Ventures: Companies may form joint ventures to collaborate on projects or

initiatives that require shared resources and expertise. Cost sharing contracts among

joint venture partners outline the financial and operational arrangements for the joint

venture activities.

16.

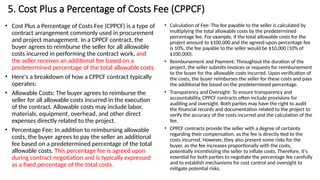

5. Cost Plusa Percentage of Costs Fee (CPPCF)

• Cost Plus a Percentage of Costs Fee (CPPCF) is a type of

contract arrangement commonly used in procurement

and project management. In a CPPCF contract, the

buyer agrees to reimburse the seller for all allowable

costs incurred in performing the contract work, and

the seller receives an additional fee based on a

predetermined percentage of the total allowable costs.

• Here's a breakdown of how a CPPCF contract typically

operates:

• Allowable Costs: The buyer agrees to reimburse the

seller for all allowable costs incurred in the execution

of the contract. Allowable costs may include labor,

materials, equipment, overhead, and other direct

expenses directly related to the project.

• Percentage Fee: In addition to reimbursing allowable

costs, the buyer agrees to pay the seller an additional

fee based on a predetermined percentage of the total

allowable costs. This percentage fee is agreed upon

during contract negotiation and is typically expressed

as a fixed percentage of the total costs.

• Calculation of Fee: The fee payable to the seller is calculated by

multiplying the total allowable costs by the predetermined

percentage fee. For example, if the total allowable costs for the

project amount to $100,000 and the agreed-upon percentage fee

is 10%, the fee payable to the seller would be $10,000 (10% of

$100,000).

• Reimbursement and Payment: Throughout the duration of the

project, the seller submits invoices or requests for reimbursement

to the buyer for the allowable costs incurred. Upon verification of

the costs, the buyer reimburses the seller for these costs and pays

the additional fee based on the predetermined percentage.

• Transparency and Oversight: To ensure transparency and

accountability, CPPCF contracts often include provisions for

auditing and oversight. Both parties may have the right to audit

the financial records and documentation related to the project to

verify the accuracy of the costs incurred and the calculation of the

fee.

• CPPCF contracts provide the seller with a degree of certainty

regarding their compensation, as the fee is directly tied to the

costs incurred. However, they also present some risks for the

buyer, as the fee increases proportionally with the costs,

potentially incentivizing the seller to inflate costs. Therefore, it's

essential for both parties to negotiate the percentage fee carefully

and to establish mechanisms for cost control and oversight to

mitigate potential risks.

Other General ContractTypes of Importance

• Time and Materials (T&M) contracts are a type of procurement contract used in various industries, particularly

in situations where the scope, schedule, or requirements of a project are not well-defined or subject to change.

In a T&M contract, the buyer pays the seller for the time spent by the seller's personnel and for the materials

used in performing the work. Here's an overview of T&M contracts:

• Billing Rate for Labor: The contractor or seller charges an agreed-upon hourly or daily rate for the labor of its

personnel assigned to the project. This rate typically includes the cost of wages, benefits, and overhead.

• Reimbursement for Materials: The buyer reimburses the seller for the cost of materials used in the project. This

may include raw materials, equipment, supplies, and any other tangible items necessary for the work.

• Flexibility: T&M contracts offer flexibility in terms of project scope and requirements. They are suitable for

projects where the scope may evolve over time or where it's challenging to accurately estimate the extent of

work needed upfront.

• Risk Sharing: T&M contracts share risk between the buyer and the seller. The buyer bears the risk of project

delays or changes in requirements, while the seller is compensated for the actual time and materials expended.

• Transparency and Control: T&M contracts provide transparency as the buyer can track the hours worked and

the materials used in real-time. This allows for better control over project costs and progress.

• Change Management: Since T&M contracts are often used for projects with evolving requirements, effective

change management processes are essential to handle scope changes, additional work, or deviations from the

original plan.

19.

Cont…

• Not-to-Exceed (NTE)Limits: To provide some level of cost control, T&M contracts may

include not-to-exceed (NTE) limits, where the seller agrees not to exceed a specified

maximum amount for labor and materials without the buyer's approval.

• Documentation and Reporting: Proper documentation and reporting are critical in T&M

contracts to ensure accurate billing, track project progress, and provide evidence of

work performed and materials used.

• Regulatory Compliance: Depending on the industry and location, T&M contracts may

need to comply with specific regulations or standards, particularly concerning labor

practices, safety, and procurement procedures.

• Overall, Time and Materials contracts offer flexibility but require careful

management to ensure that both parties' interests are protected and that the

project stays within budget and schedule constraints. Effective communication,

clear expectations, and regular monitoring are essential for successful

outcomes in T&M contracts.

20.

Labor-hour contracts

• Labor-hourcontracts are a type of contract used in procurement and project management where the

contractor is reimbursed based on the actual labor hours expended, along with an additional fee for

overhead and profit. This type of contract is commonly used when the scope of work is difficult to define

precisely, making it challenging to establish a fixed price or when the project requires a high degree of

flexibility in terms of labor resources.

• Here are some key characteristics of labor-hour contracts:

• Reimbursement for Labor Hours: In a labor-hour contract, the contractor is reimbursed for the actual

hours worked by labor personnel assigned to the project. These hours are typically tracked and recorded

by the contractor and verified by the buyer.

• Hourly Rates: The contract may specify different hourly rates for various categories of labor, such as

skilled labor, unskilled labor, and supervisory personnel. These rates may include wages, benefits, and

overhead costs associated with the labor.

• Additional Fee for Overhead and Profit: In addition to reimbursement for labor hours, the contractor

may receive an additional fee to cover overhead costs and to provide a profit margin. This fee is typically

calculated as a percentage of the total labor costs.

• Flexibility: Labor-hour contracts offer flexibility to both the contractor and the buyer, as they allow for

adjustments to the scope of work, staffing levels, and project requirements throughout the duration of

the contract. This flexibility is particularly advantageous in projects where the scope is likely to change or

evolve over time.

21.

• Risk Sharing:Labor-hour contracts involve a degree of risk-sharing between the

contractor and the buyer. While the contractor bears the risk of fluctuations in labor

costs and productivity, the buyer assumes the risk of changes in the scope of work and

project requirements.

• Transparency and Documentation: To ensure transparency and accountability, labor-

hour contracts typically require detailed documentation of labor hours, rates, and

expenses. Both parties may have the right to audit the contractor's records to verify

the accuracy of the charges.

Labor-hour contracts are often used in industries such as construction, information

technology, consulting, and professional services, where the nature of the work makes it

challenging to determine a fixed price upfront. While they offer flexibility and

transparency, labor-hour contracts also require careful monitoring and oversight to

control costs and ensure that the project stays within budget.

22.

Letter Contracts:

• Aletter contract, also known as a letter of intent or a preliminary agreement, is a type of contract used in

procurement and business transactions. It serves as a temporary arrangement between two parties to

authorize the commencement of work or the provision of goods or services before a formal contract is

finalized. Letter contracts are commonly used in situations where it is necessary to expedite the start of

work or to provide interim authorization while negotiating the terms of a formal contract.

• Here are some key characteristics of letter contracts:

• Interim Authorization: A letter contract provides interim authorization for the contractor to begin work or

provide goods or services before a formal contract is executed. It allows the parties to initiate the project

or transaction promptly, without waiting for the completion of the entire contracting process.

• Temporary Nature: Letter contracts are temporary agreements that are intended to be replaced by a

formal contract once the terms and conditions have been fully negotiated and agreed upon by both

parties. They typically have a limited duration and are subject to specific terms and conditions outlined in

the letter.

• Basic Terms: While letter contracts are less formal than traditional contracts, they typically include

essential terms and conditions such as the scope of work, pricing, delivery schedule, and any other key

terms necessary to initiate the project or transaction.

• Negotiation of Formal Contract: After the letter contract is issued and work begins, the parties continue

to negotiate the terms of the formal contract. Once the negotiations are complete, the parties execute

the formal contract, which supersedes the letter contract.

23.

• Risks andLimitations: Letter contracts carry certain risks and limitations for both

parties. Since the terms and conditions are not fully defined at the outset, there is a

risk of misunderstandings or disputes arising during the course of the work.

Additionally, letter contracts may limit the contractor's ability to recover costs or claim

compensation if the formal contract negotiations are unsuccessful.

• Regulatory Compliance: In government contracting, letter contracts are subject to

specific regulations and guidelines, including those outlined in the Federal Acquisition

Regulation (FAR) in the United States. These regulations govern the use of letter

contracts and specify the circumstances under which they may be used.

• Overall, letter contracts provide a flexible and expedited way to initiate work or

transactions while formal contract negotiations are ongoing. However, they require

careful management and oversight to ensure that the terms and conditions are fully

defined and agreed upon before the work progresses too far.

24.

Basic Ordering Agreements(BOAs)

• Basic Ordering Agreements (BOAs) are widely used in government contracting, particularly in the United

States, as well as in some commercial sectors. BOAs are pre-established agreements between a buyer

(typically a government agency or a large organization) and a seller (usually a supplier or contractor).

These agreements outline the terms and conditions under which future orders for goods or services will

be issued.

• Here are the key features and characteristics of Basic Ordering Agreements:

• Framework Agreement: A BOA serves as a framework or umbrella agreement between the buyer and the

seller. It establishes the terms and conditions that will govern future transactions between the parties.

• Flexible Ordering Process: Instead of negotiating individual contracts for each order, the buyer can issue

purchase orders or task orders against the BOA as needed. This streamlines the procurement process and

reduces administrative burden for both parties.

• Scope of Work: The BOA defines the scope of work, including the types of goods or services to be

provided, pricing, delivery terms, performance standards, and any other relevant terms and conditions.

• Duration: BOAs typically have a fixed duration, often spanning multiple years. During this period, the buyer

can issue orders against the BOA as needed, up to the maximum value specified in the agreement.

• Price and Payment Terms: BOAs may include pricing mechanisms, such as fixed prices, ceiling prices, or

discounts, for the goods or services covered by the agreement. Payment terms, invoicing procedures, and

other financial arrangements are also specified in the BOA.

25.

• Competition Requirements:BOAs may or may not require competitive procedures for individual orders,

depending on the regulations and policies governing the procurement process. In some cases, multiple

suppliers may compete for orders issued against the BOA, while in others, the BOA may be awarded on a

sole-source basis.

• Terms and Conditions: BOAs include terms and conditions that govern the relationship between the buyer

and the seller. These may cover various aspects such as warranties, intellectual property rights, dispute

resolution mechanisms, and termination provisions.

• Regulatory Compliance: BOAs in government contracting are subject to specific regulations and guidelines,

such as those outlined in the Federal Acquisition Regulation (FAR) in the United States. These regulations

govern the use of BOAs and prescribe requirements for their establishment, administration, and use.

• Overall, Basic Ordering Agreements provide a flexible and efficient mechanism for government agencies and

large organizations to procure goods and services from pre-approved suppliers. They help streamline the

procurement process, promote competition, and facilitate long-term business relationships between buyers

and sellers.