Download to read offline

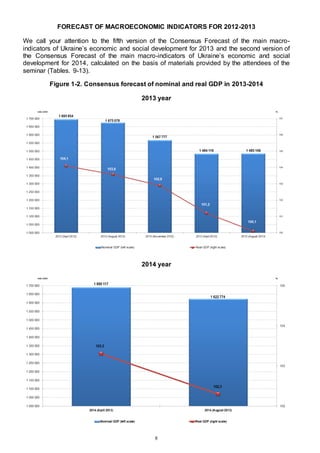

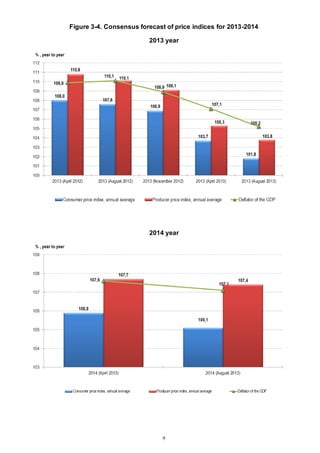

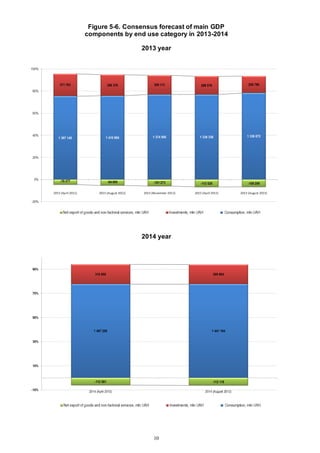

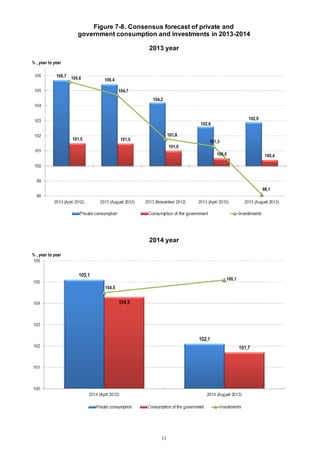

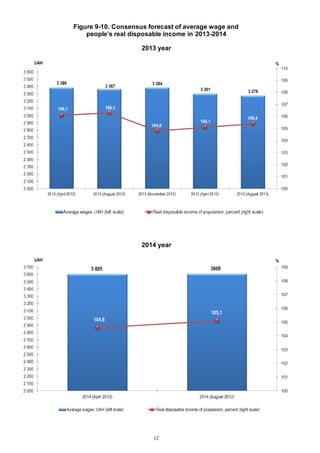

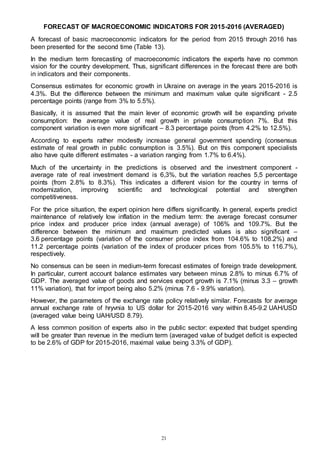

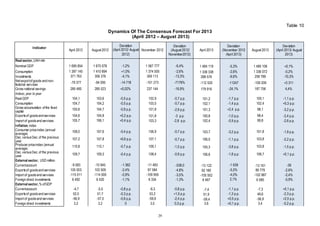

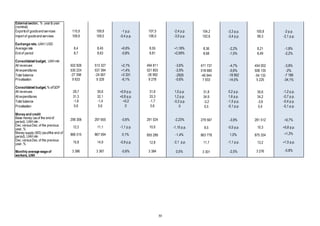

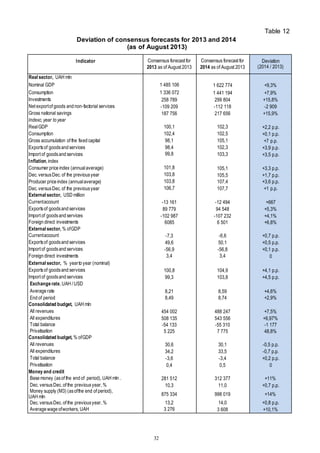

This document presents the consensus forecast for macroeconomic indicators in Ukraine from 2013-2016 as agreed upon by experts from various Ukrainian government institutions, international organizations, research institutes, and private sector organizations. The consensus forecast was developed through a seminar where experts discussed forecasts, economic trends, and research results to reach agreement on key indicators. The document provides the consensus forecasts for GDP growth, inflation, budget balances, trade, currency exchange rates, and other indicators for 2013-2014 in detail and average forecasts for 2015-2016. It also discusses risks to the forecasts for 2013-2014.