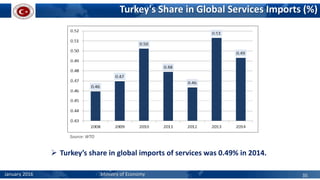

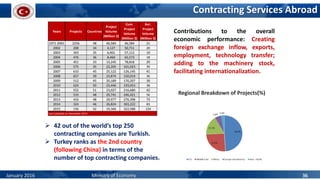

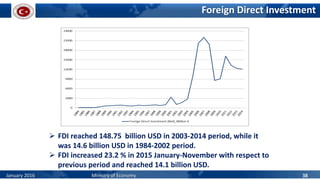

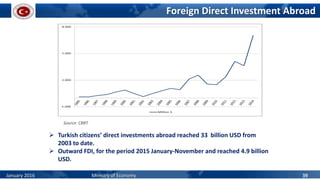

Download as PDF, PPTX

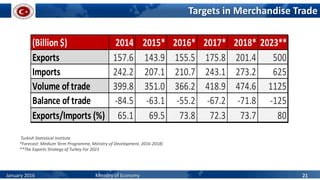

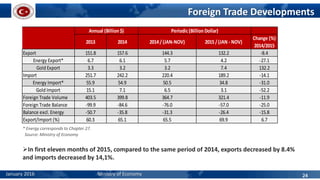

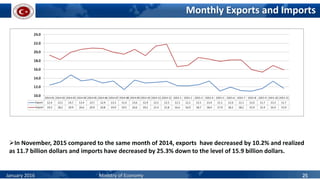

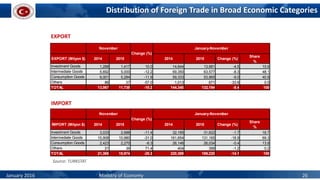

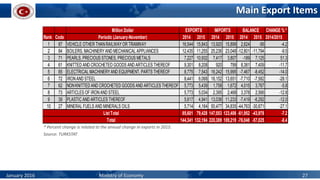

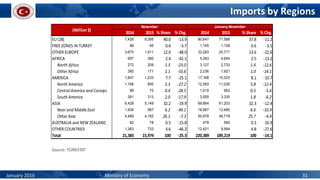

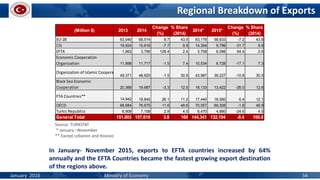

The document provides an economic outlook from the Ministry of Economy of Turkey for January 2016. It includes macroeconomic forecasts from international organizations showing Turkey's GDP growth expected around 3% in 2015-2016. The medium term program targets 4.5% GDP growth in 2016 with a reduced current account deficit. Exports decreased 8.4% in the first 11 months of 2015 while imports decreased 14.1%. Top exports include vehicles, machinery, precious metals and textiles, while machinery, intermediate goods and consumption goods dominate imports.