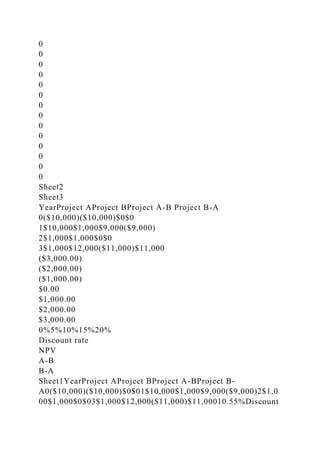

The document explains how to calculate Internal Rate of Return (IRR) and Net Present Value (NPV) using Microsoft Excel functions, detailing their syntax and parameters. It highlights essential considerations in capital budgeting, such as cash flows versus accounting profits, financing costs, working capital, and cash flow estimation methods. Additionally, real-world examples, including a case study on Speedo's LZR-2 swimsuit project, illustrate these concepts in a practical context.

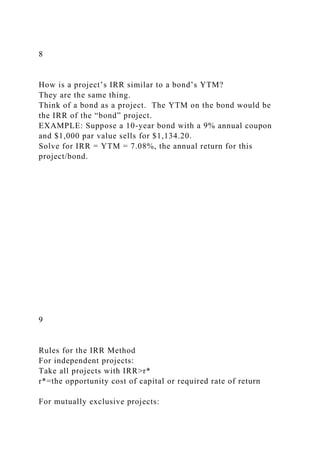

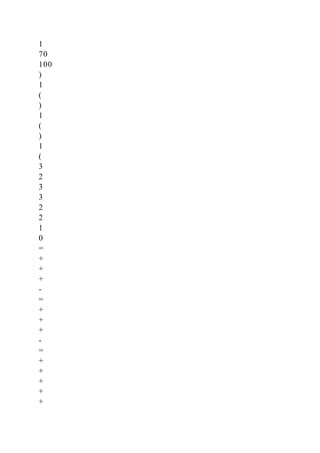

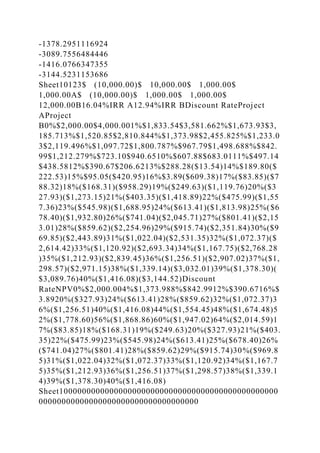

![Compute IRR and NPV in Microsoft Excel

1.IRR Function

Description:

The Microsoft Excel IRR function returns the internal rate of

return for a series of cash flows. The cash

flows must occur at regular intervals, but do not have to be the

same amounts for each interval.

Syntax

The syntax for the IRR function in Microsoft Excel is:

IRR(range, [estimated_irr] )

Parameters or Arguments

range

A range of cells that represent the series of cash flows.

estimated_irr

Optional. It is your guess at the internal rate of return. If this

parameter is omitted, it

assumes an estimated_irr of 0.1 or 10%

Example (as Worksheet Function)

Let's look at some Excel IRR function examples and explore](https://image.slidesharecdn.com/computeirrandnpvinmicrosoftexcel1-221028224510-3822b722/85/Compute-IRR-and-NPV-in-Microsoft-Excel-1-IRR-Function-docx-1-320.jpg)

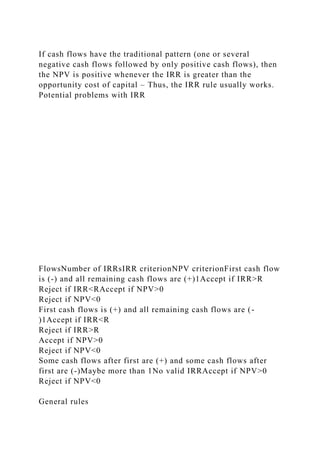

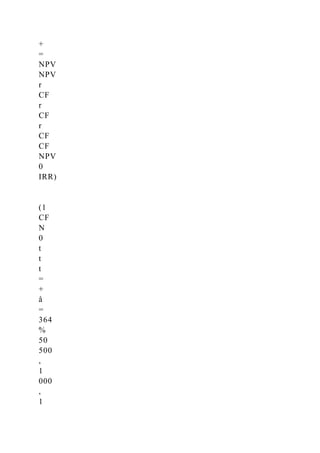

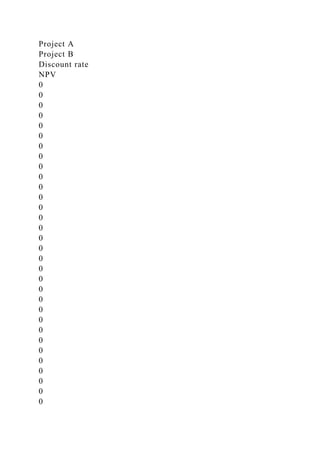

![The syntax for the NPV function in Microsoft Excel is:

NPV( discount_rate, value1, [value2, ... value_n] )

Parameters or Arguments

discount_rate

The discount rate for the period.

value1, value2, ... value_n

The future payments and income for the investment (ie: cash

flows). There can be up

to 29 values entered.

Note

Microsoft Excel's NPV function does not account for the intial

cash outlay, or may account for

it improperly depending on the version of Excel. However, there

is a workaround.

This workaround requires that you NOT include the initial

investment in the future

payments/income for the investment (ie: value1, value2, ...

value_n), but instead, you need to

subtract from the result of the NPV function, the amount of the

initial investment.

The workaround formula is also different depending on whether

the cash flows occur at the

end of the period (EOP) or at the beginning of the period

(BOP).

If the cash flows occur at the end of the period (EOP), you](https://image.slidesharecdn.com/computeirrandnpvinmicrosoftexcel1-221028224510-3822b722/85/Compute-IRR-and-NPV-in-Microsoft-Excel-1-IRR-Function-docx-3-320.jpg)

![1. Payback Period and Net Present Value[LO1, 2] If a project with .docx](https://cdn.slidesharecdn.com/ss_thumbnails/1-221101035238-1d86b81e-thumbnail.jpg?width=640&height=640&fit=bounds)