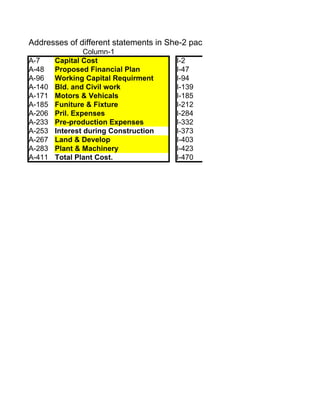

This document contains summaries of capital costs, proposed financial plan, and working capital requirements for a boutique and garment factory project. The total fixed capital cost is Rs. 4,666,000 and total project cost is Rs. 7,121,000 to be funded entirely by equity. The initial working capital requirement is Rs. 2,455,000 calculated based on raw materials, salaries, utilities, expenses and inventory levels over different periods. Building and civil works, motors and vehicles are estimated to cost Rs. 0 as per the details provided in appendices.