Download to read offline

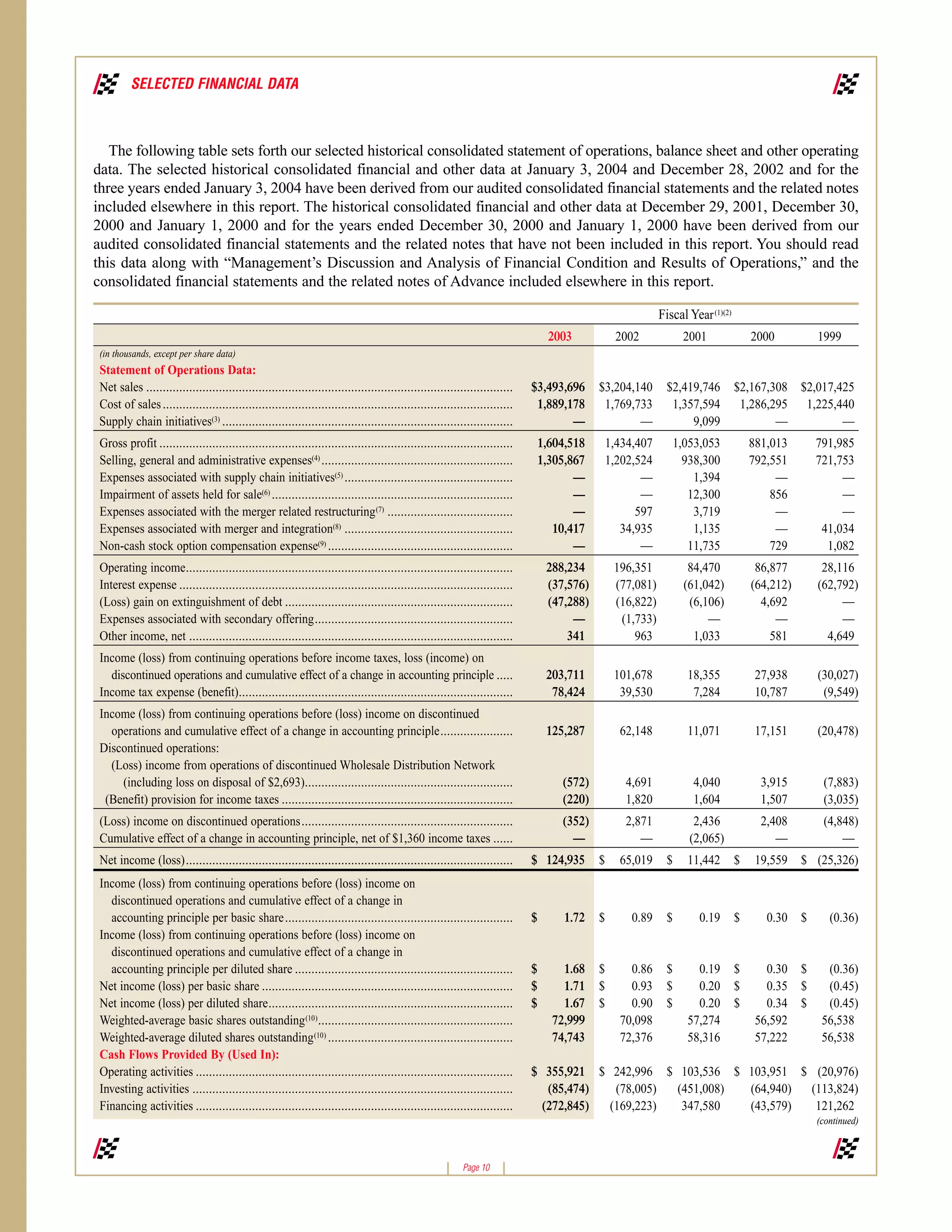

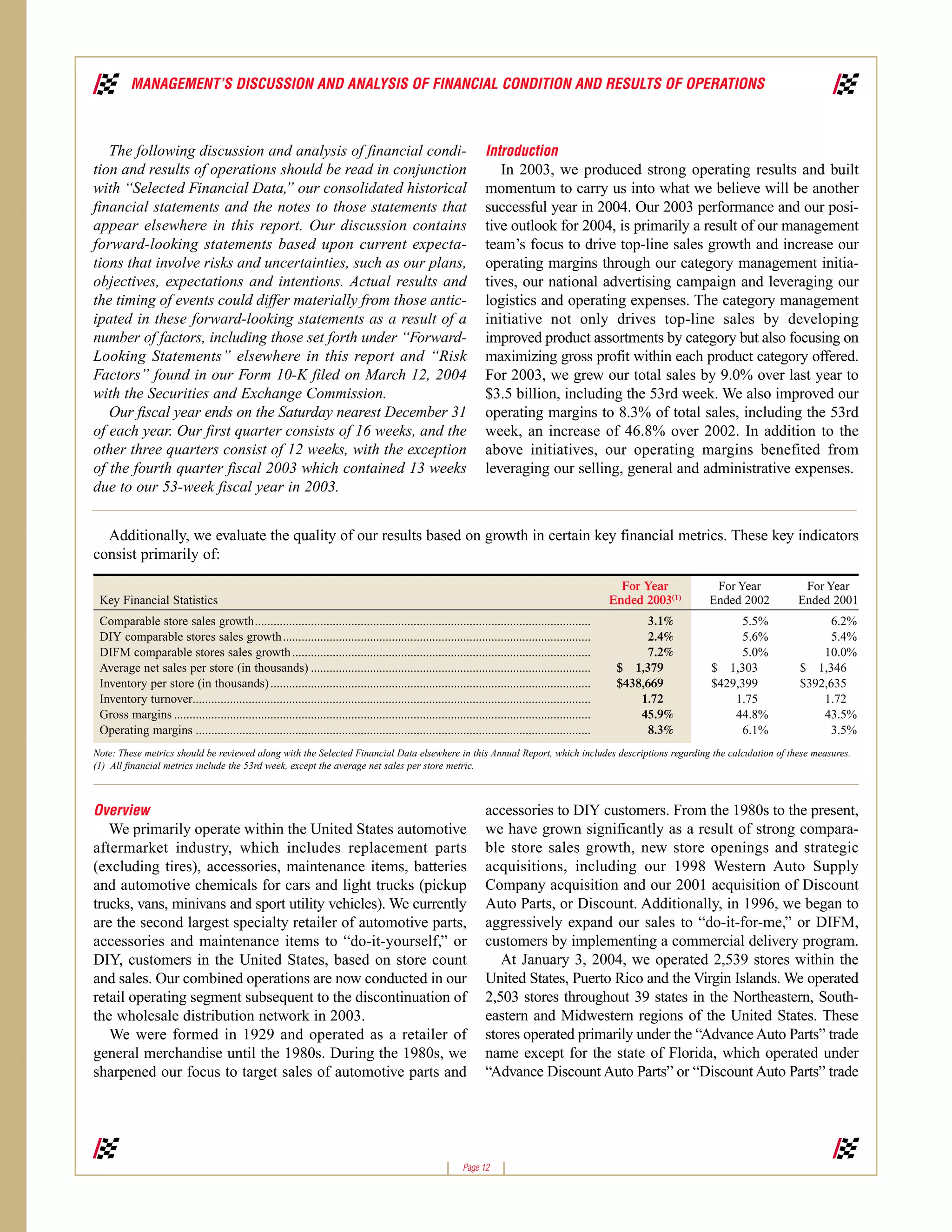

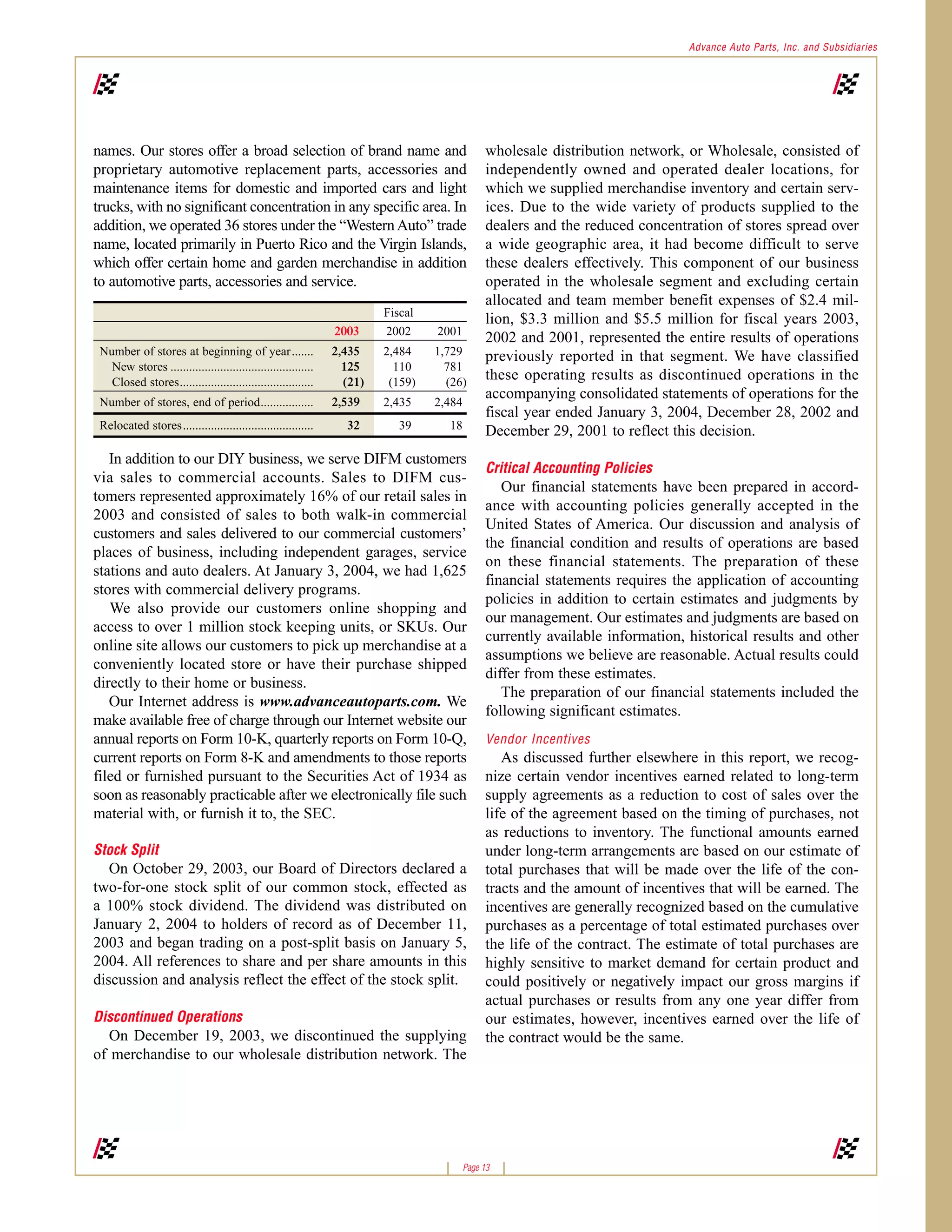

Advance Auto Parts experienced strong growth in 2003, building momentum across key metrics. With over 2,500 stores in 39 states, Puerto Rico and the Virgin Islands, the company served over 200 million customers in 2003. Same store sales grew 3.1% as initiatives like expanded private brands and improved supply chain efficiencies increased the number of customers and average transaction size. Operating margins increased to 8.3% of sales, up from 7.2% the prior year. Earnings per share also grew substantially.

![Videoconferencing[1]](https://cdn.slidesharecdn.com/ss_thumbnails/videoconferencing1-090318194623-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)