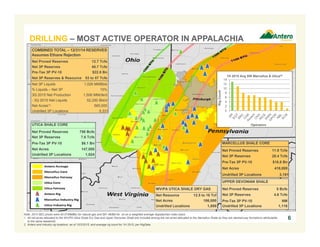

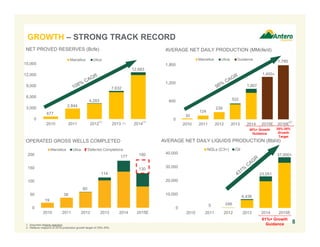

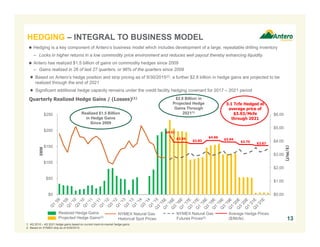

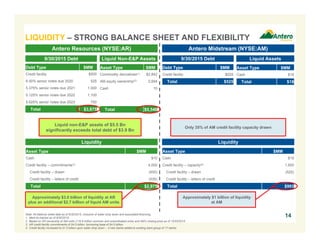

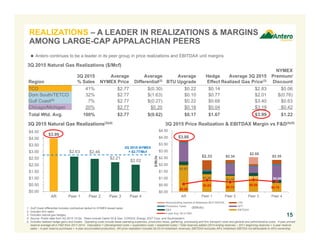

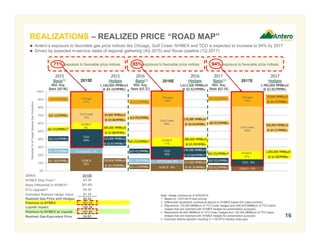

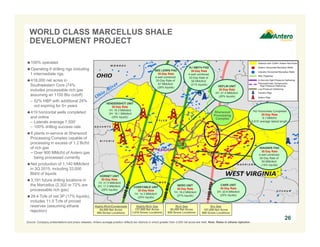

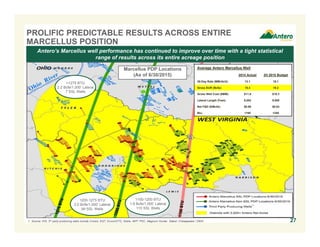

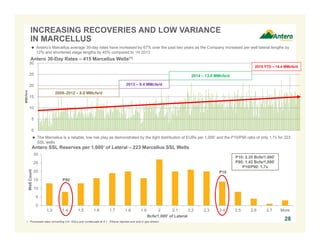

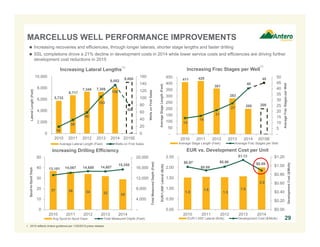

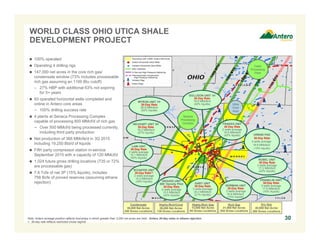

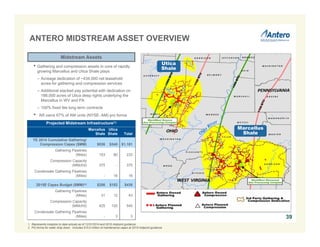

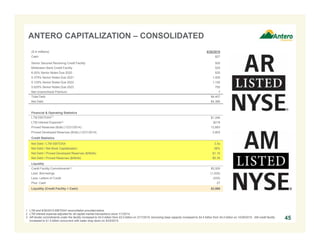

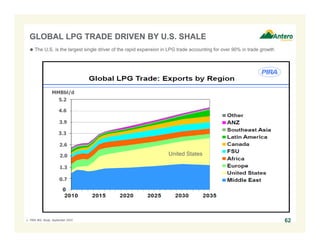

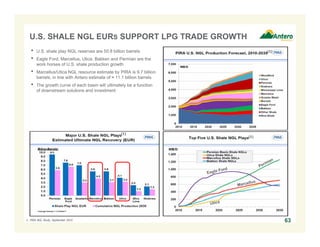

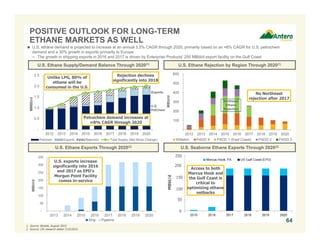

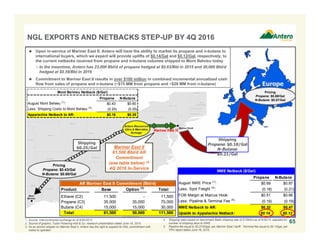

The document provides an overview of Antero Resources Corporation. It contains forward-looking statements regarding estimates, plans, strategies, objectives, anticipated financial and operating results, and risks. These statements are based on certain assumptions made by the company. Actual results may differ materially from forward-looking statements due to risks and uncertainties including commodity price volatility and lack of availability of drilling equipment. The company has over 4,200 undrilled locations that are expected to have returns exceeding the company's weighted average cost of capital under current strip pricing. Antero is the most active driller in the Appalachian basin with over 1 million net acres and over 5,300 undrilled locations as of year-end 2014.