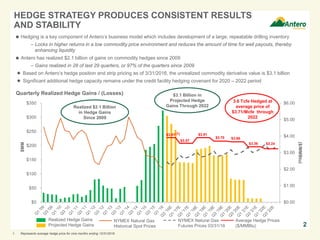

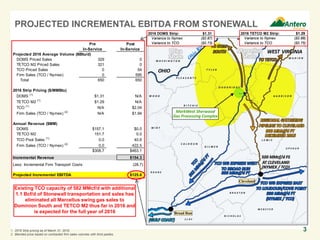

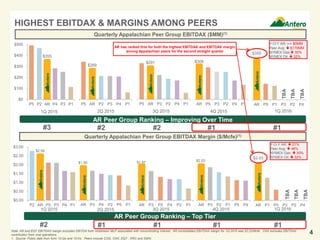

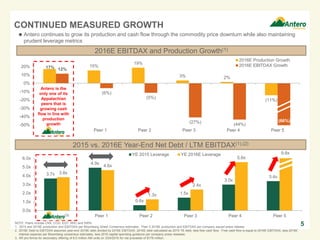

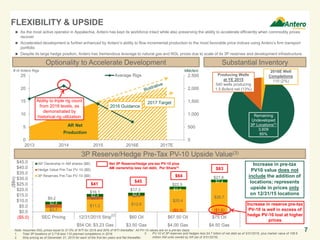

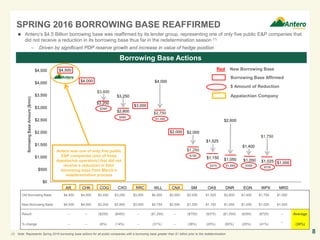

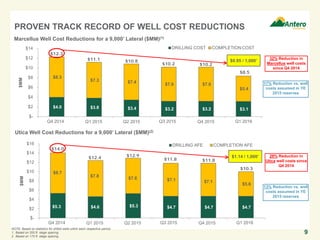

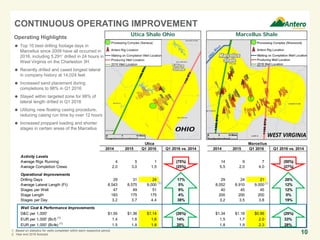

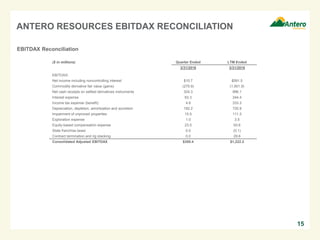

This document is the first quarter 2016 earnings call presentation for Antero Resources Corporation. It contains forward-looking statements and discusses Antero's hedge strategy, which has resulted in $2.1 billion in realized hedge gains since 2009. It also summarizes Antero's projected incremental EBITDA of $125.6 million from its Stonewall project. Additional sections compare Antero's EBITDAX and margins to Appalachian peers, show Antero's continued measured growth, and demonstrate Antero's flexibility and upside in various commodity price scenarios.

![CURRICULUM_VITAE_OF_BONGANI_GLEN[1]](https://cdn.slidesharecdn.com/ss_thumbnails/1ba45a48-431f-46bf-8c34-7e83030a8eb2-160523093427-thumbnail.jpg?width=640&height=640&fit=bounds)