Download to read offline

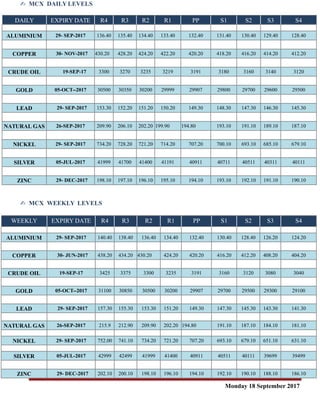

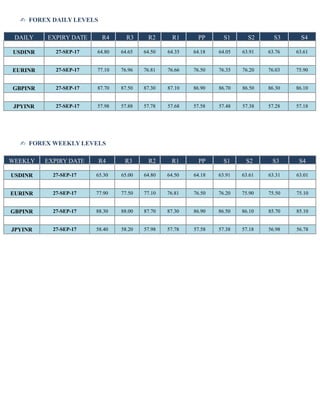

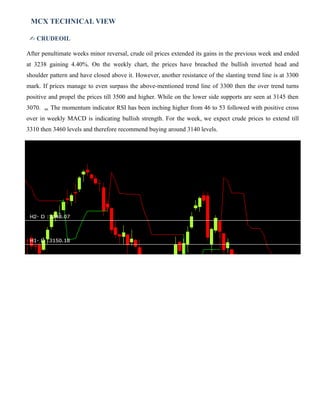

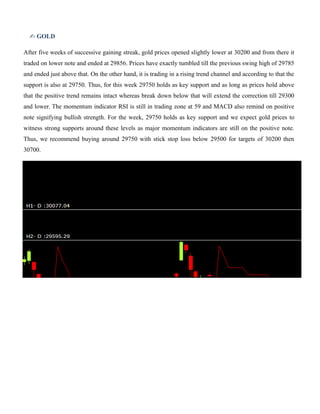

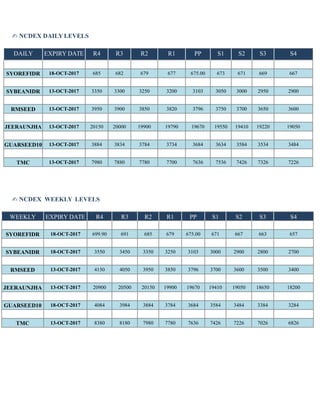

The document provides daily and weekly technical analysis and market review for various commodities traded on MCX and NCDEX exchanges in India. For crude oil, support is seen at Rs. 3145 and Rs. 3070, with resistance at Rs. 3300. Gold support is at Rs. 29750, with resistance at Rs. 30200 and Rs. 30700. In NCDEX, cardamom and jeera traded positively while guar complex, cotton and coriander traded lower. The technical outlook is bullish for crude oil and gold if key support levels are respected.