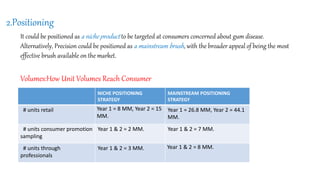

Colgate Palmolive is developing a new toothbrush called the Colgate Precision. It currently has two toothbrush lines and faces competition from Oral-B, Procter & Gamble, and Johnson & Johnson in the premium toothbrush segment. Research shows consumers are replacing toothbrushes more frequently and new product introductions have increased category sales. Colgate will need to define the positioning, branding, and communication strategy for the Precision toothbrush to effectively compete in the market.