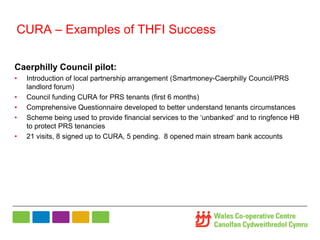

The document discusses a project called Tackling Homelessness through Financial Inclusion (THFI) that aims to prevent homelessness by helping tenants access alternative banking through credit unions to ring-fence benefits for rent payments. The project also provides tenants with support services around budgeting, debt advice, and training to address both short-term rental arrears and long-term financial stability. Case studies show how credit union rent accounts in Wales have successfully increased rental payments and maintained tenancies.