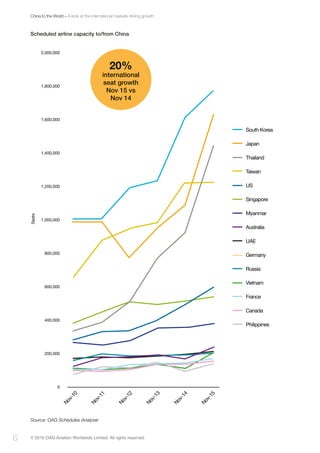

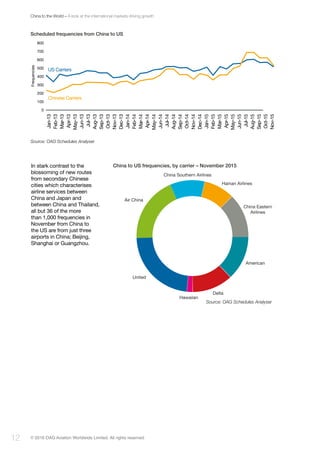

Chinese international airline capacity has grown substantially over the past year, especially to certain key markets. Capacity to South Korea, Japan, Vietnam, and Thailand grew over 50% year-over-year, driven largely by new routes from secondary Chinese airports and increased frequencies from Chinese carriers. Chinese carriers have also strengthened their position in long-haul markets like Australia and the US, now operating over half the flights between China and the US. This rapid growth reflects China's increasing economic and political ties worldwide.