Download to read offline

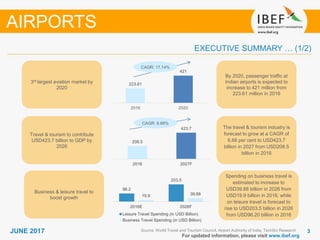

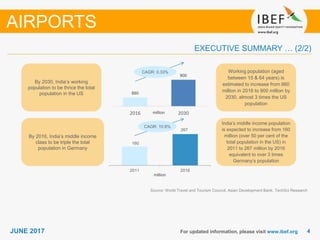

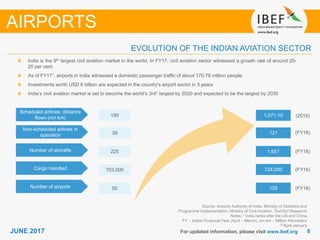

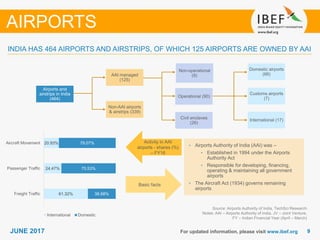

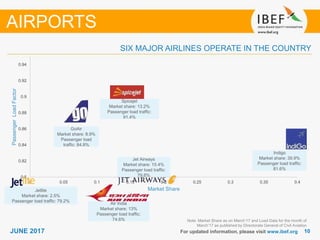

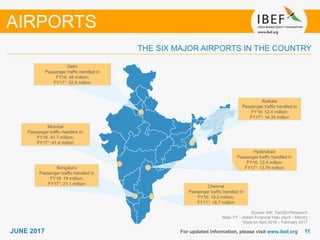

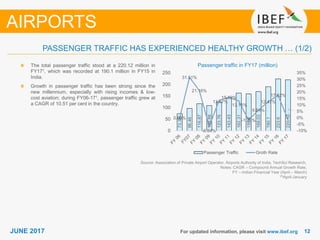

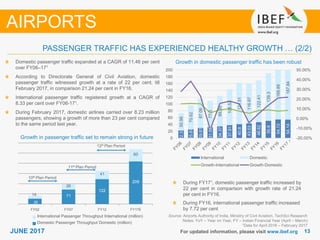

- Passenger traffic at Indian airports is expected to increase from 223.61 million in 2016 to 421 million by 2020, making India the 3rd largest aviation market. - The number of operational airports in India is projected to grow from 44 in FY2015 to 95 by FY2020 to accommodate rising demand from the expanding middle class and growing business sector. - Six major airlines operate in India, with Indigo having the largest market share of 39.9% as of March 2017, while Jet Airways, SpiceJet, Air India, GoAir and Jetlite make up the rest of the top carriers.