The document discusses the objectives, phases and processes of operational audits. It describes the following:

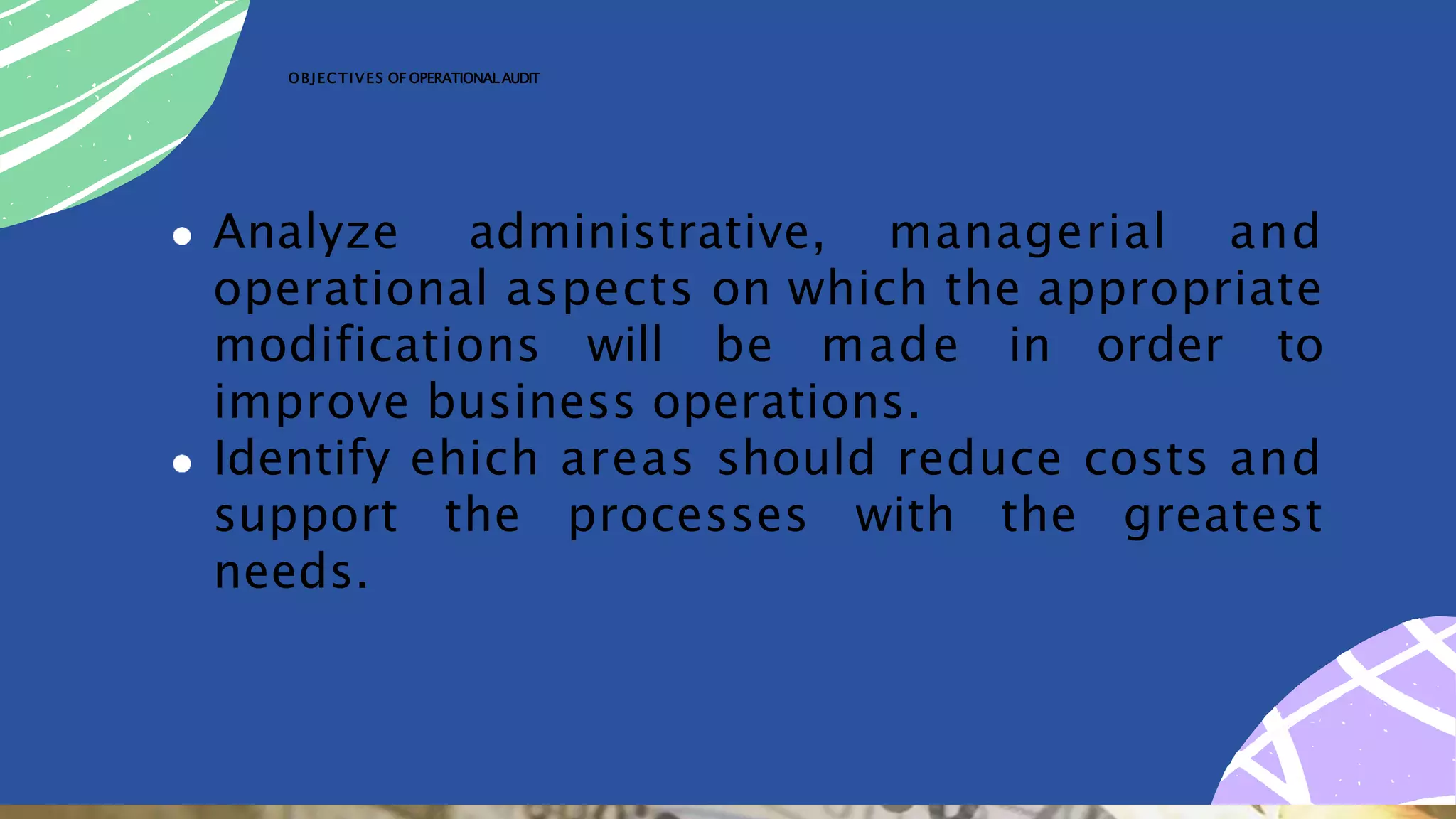

The objectives are to analyze administrative and operational aspects to identify areas for improvement and cost reduction.

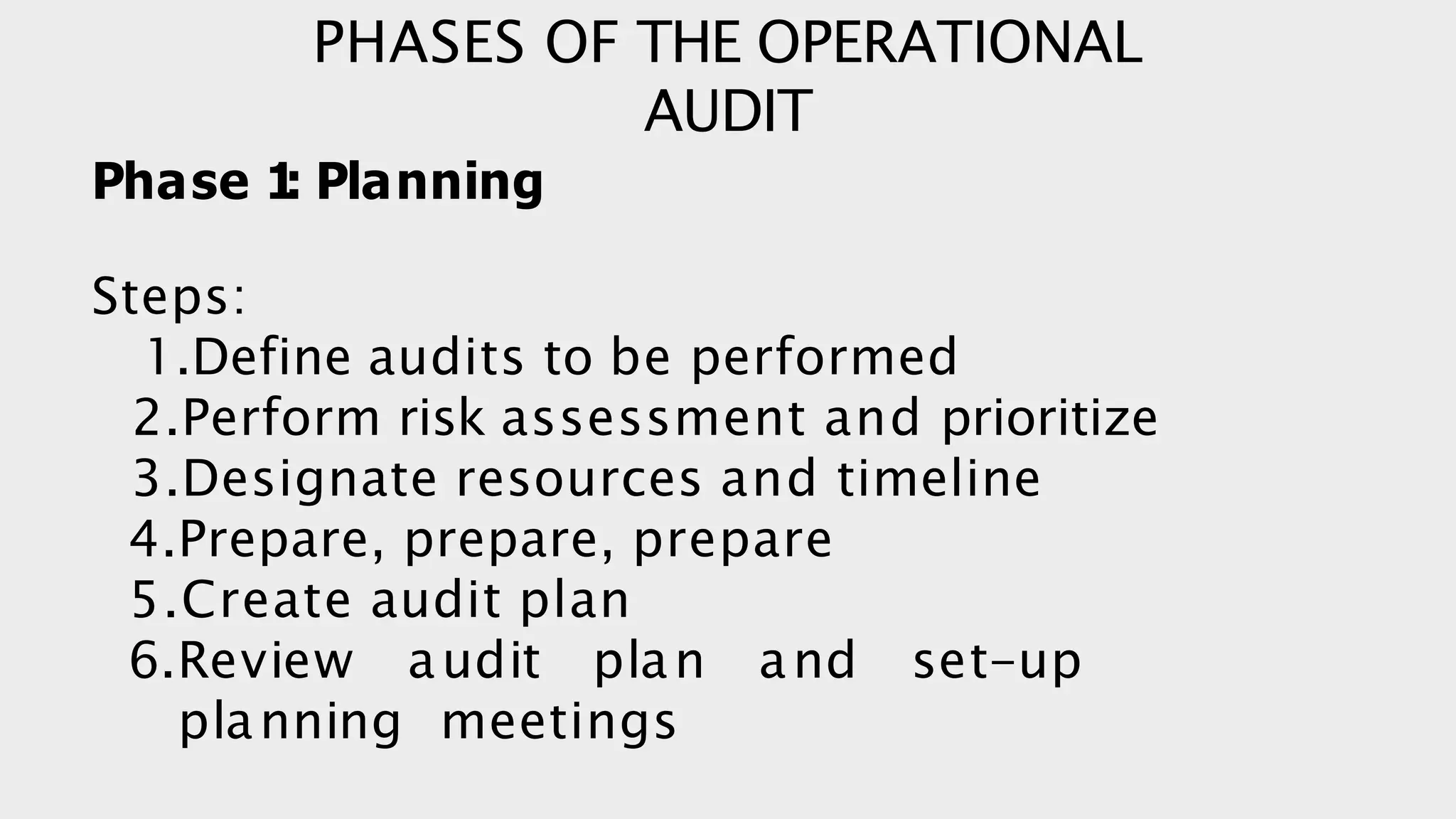

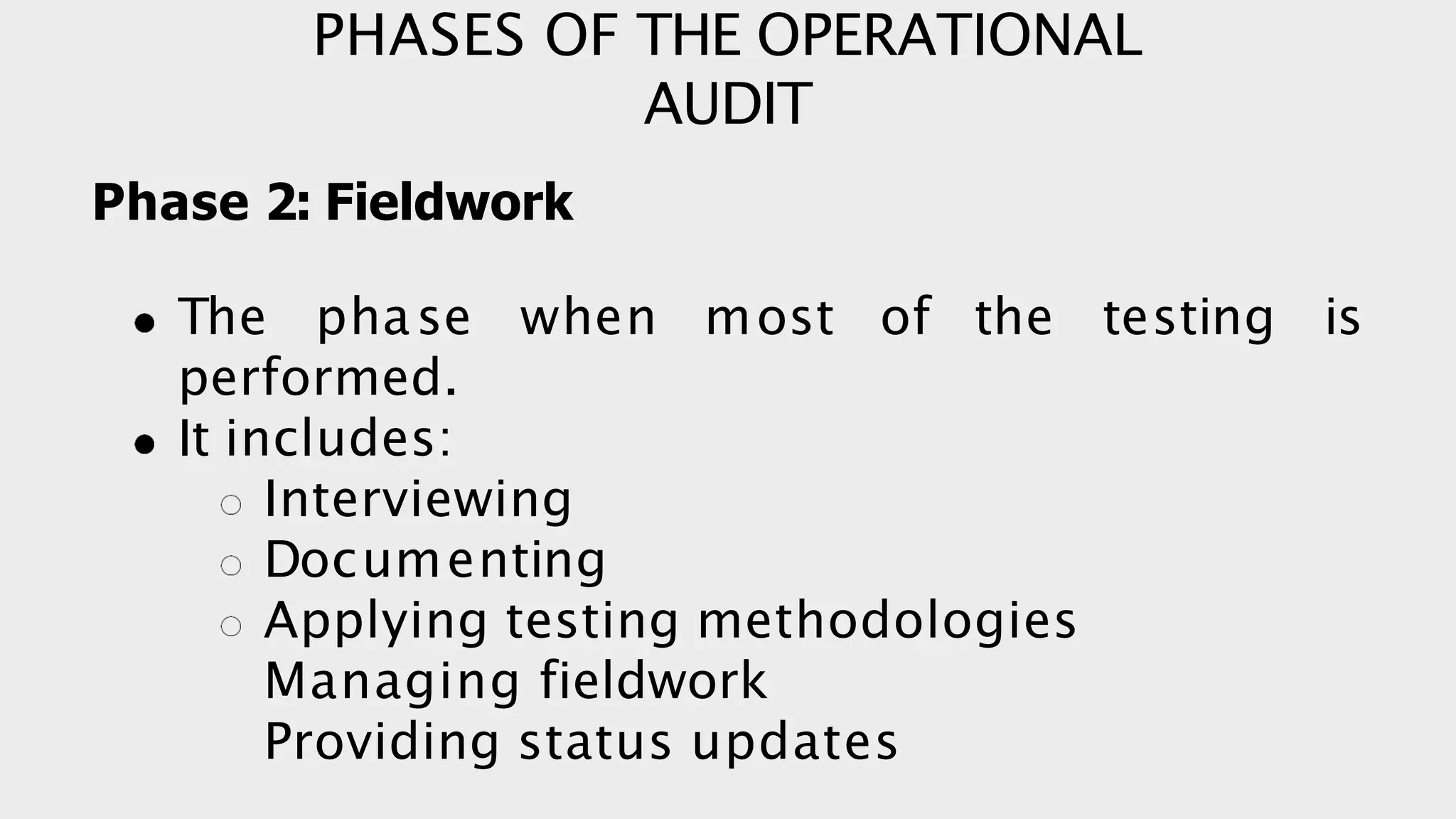

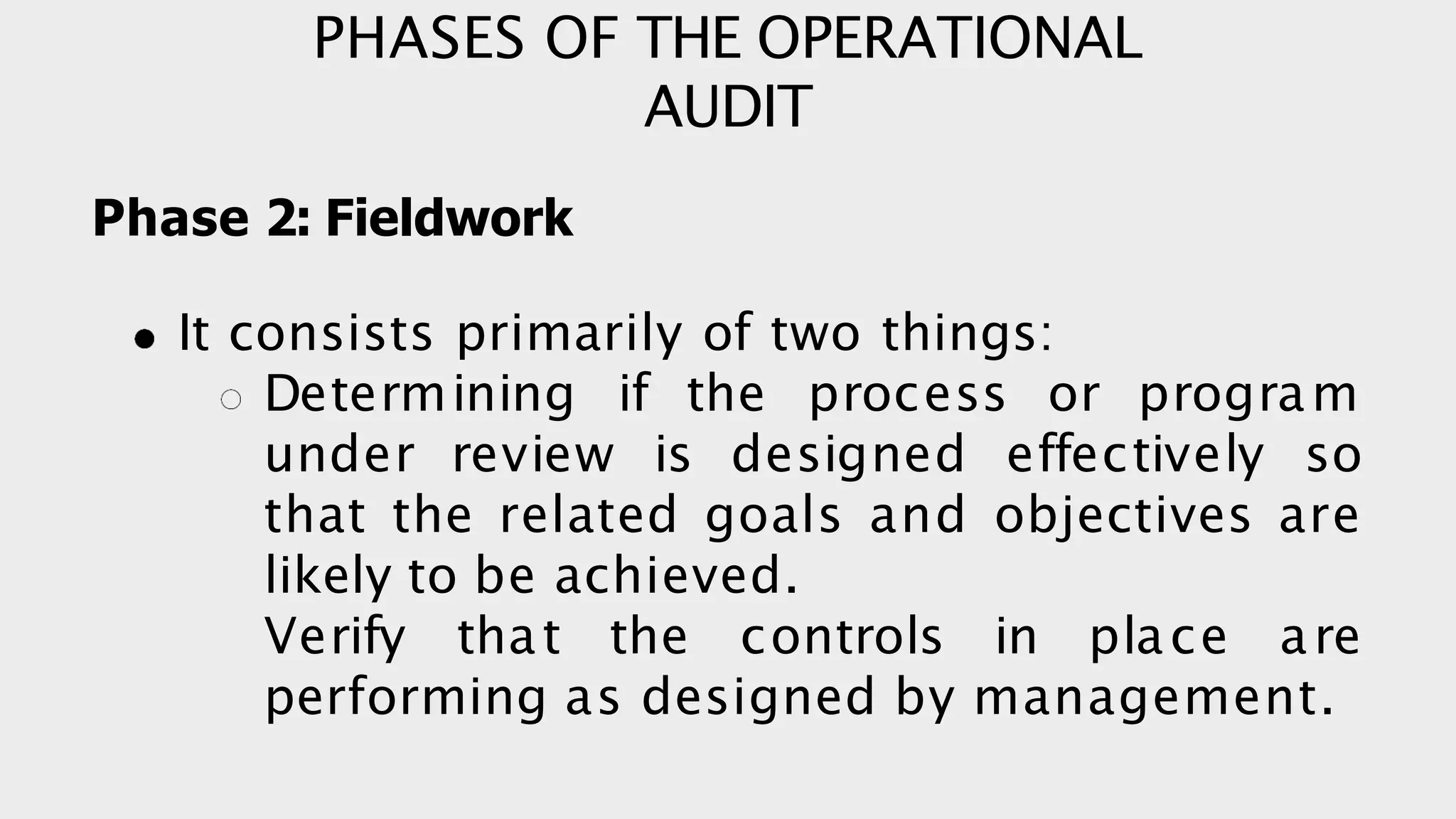

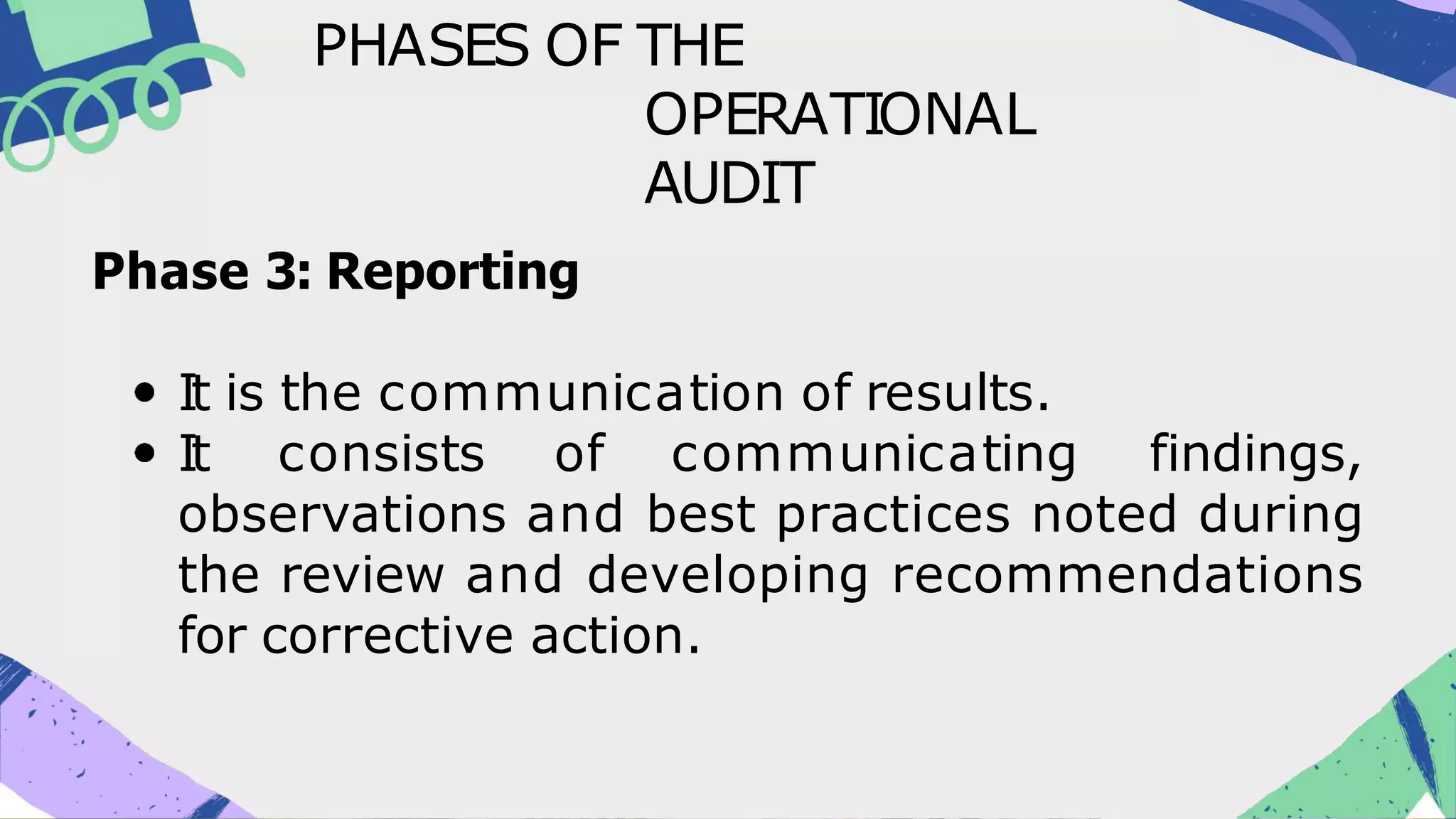

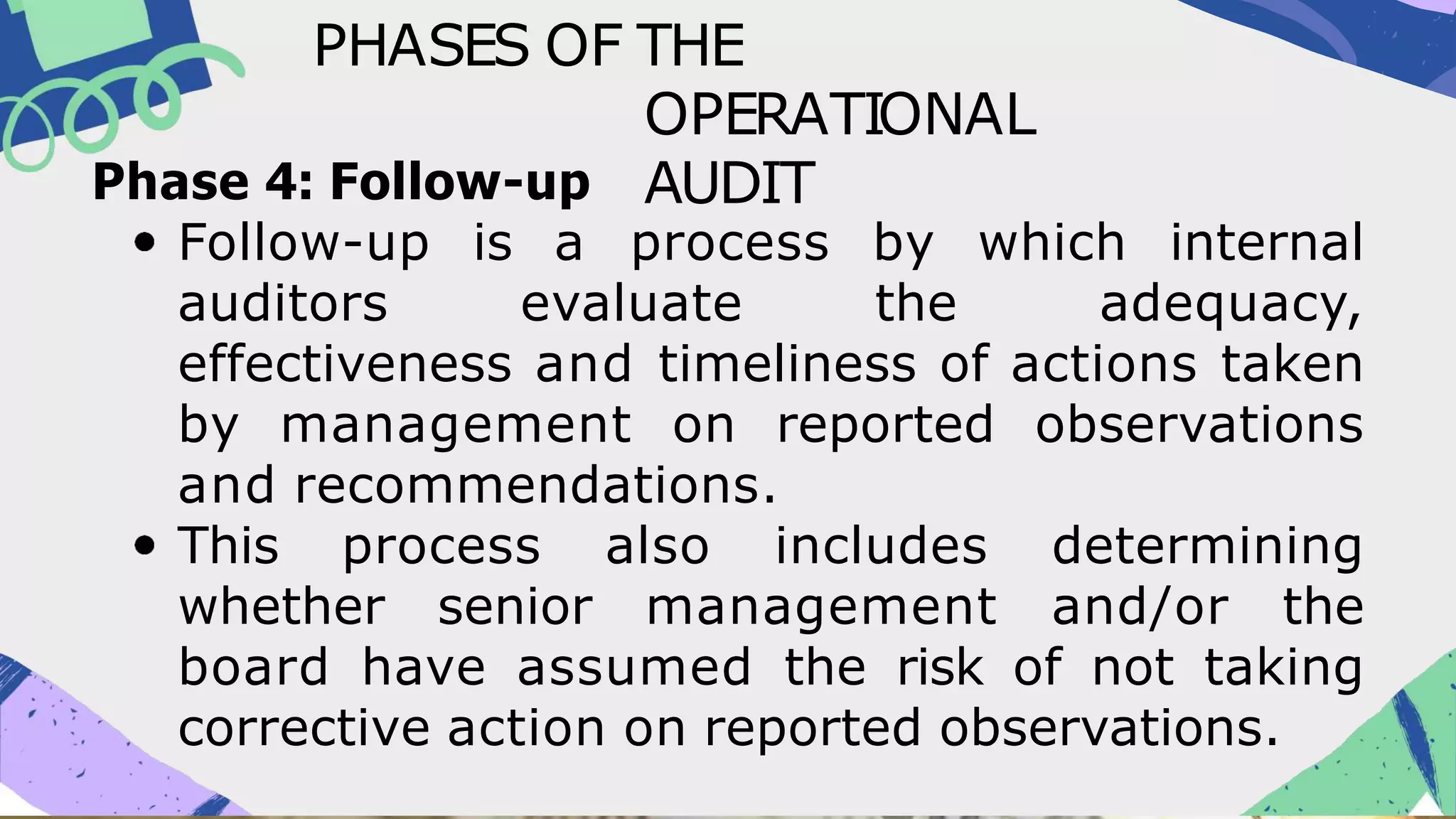

The phases include planning, fieldwork, reporting, and follow-up. Planning involves defining audits, assessing risks, and creating an audit plan. Fieldwork consists of interviews, testing, and gathering evidence. Reporting communicates findings and recommendations. Follow-up ensures corrective actions were implemented.

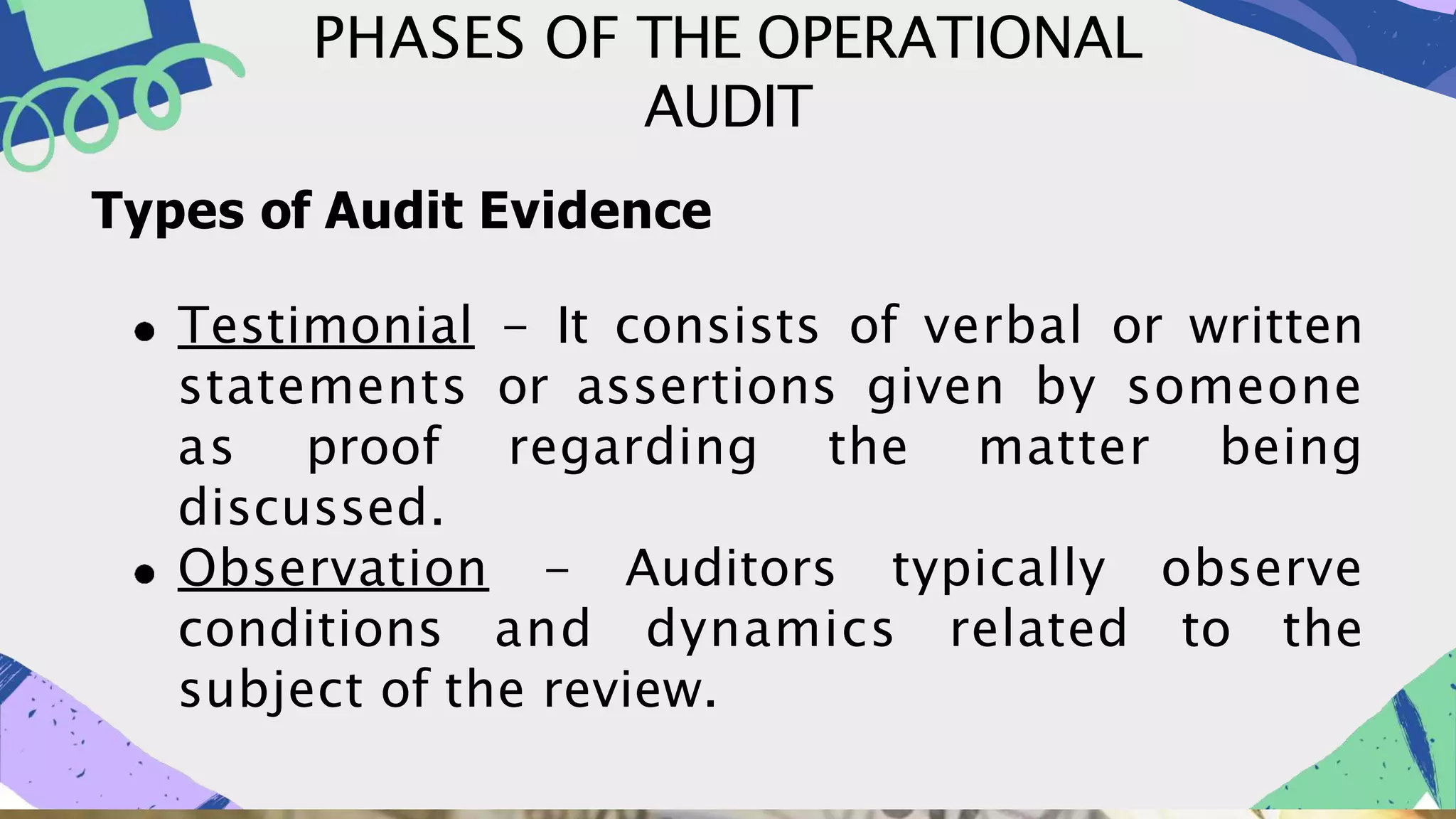

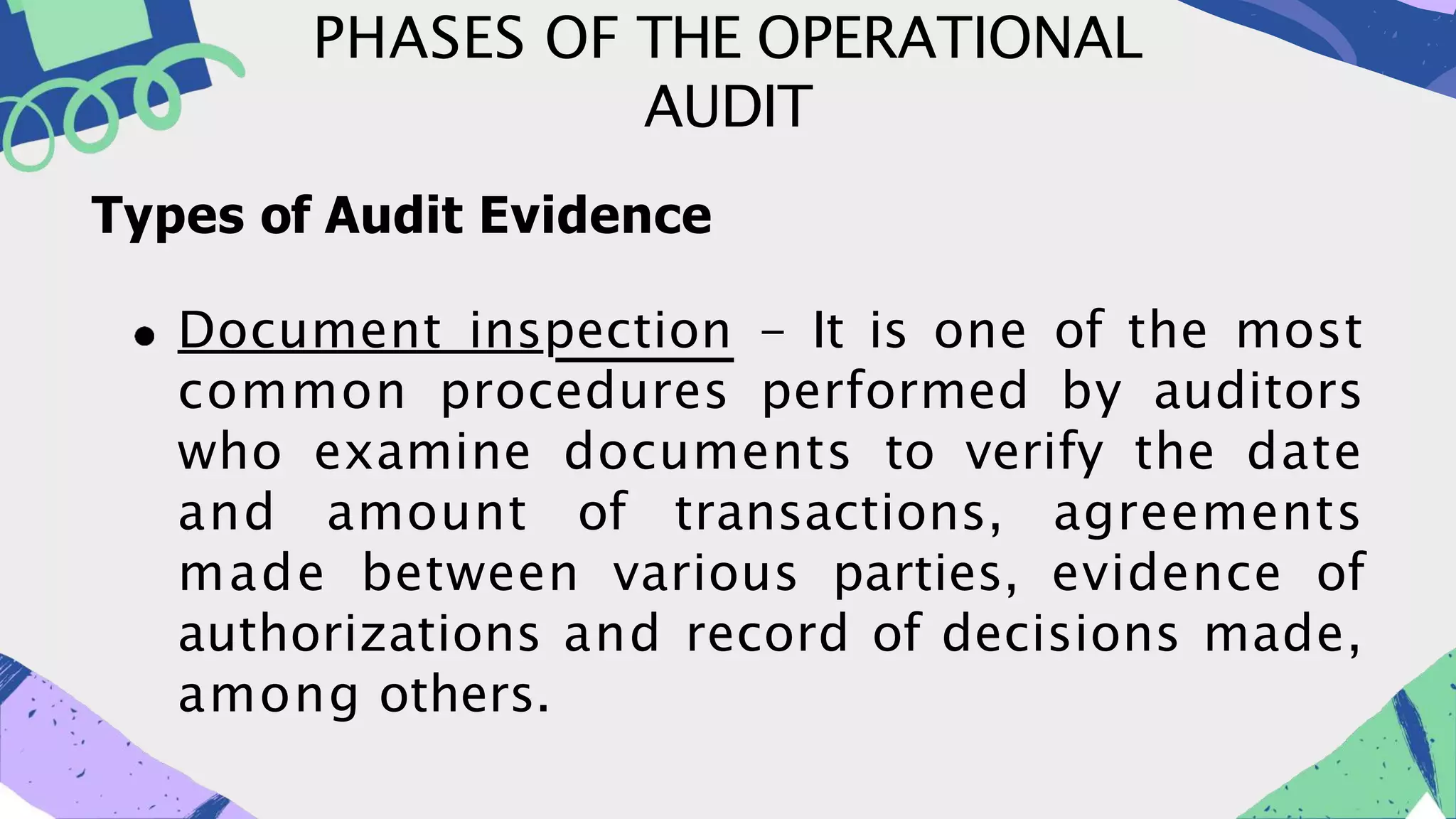

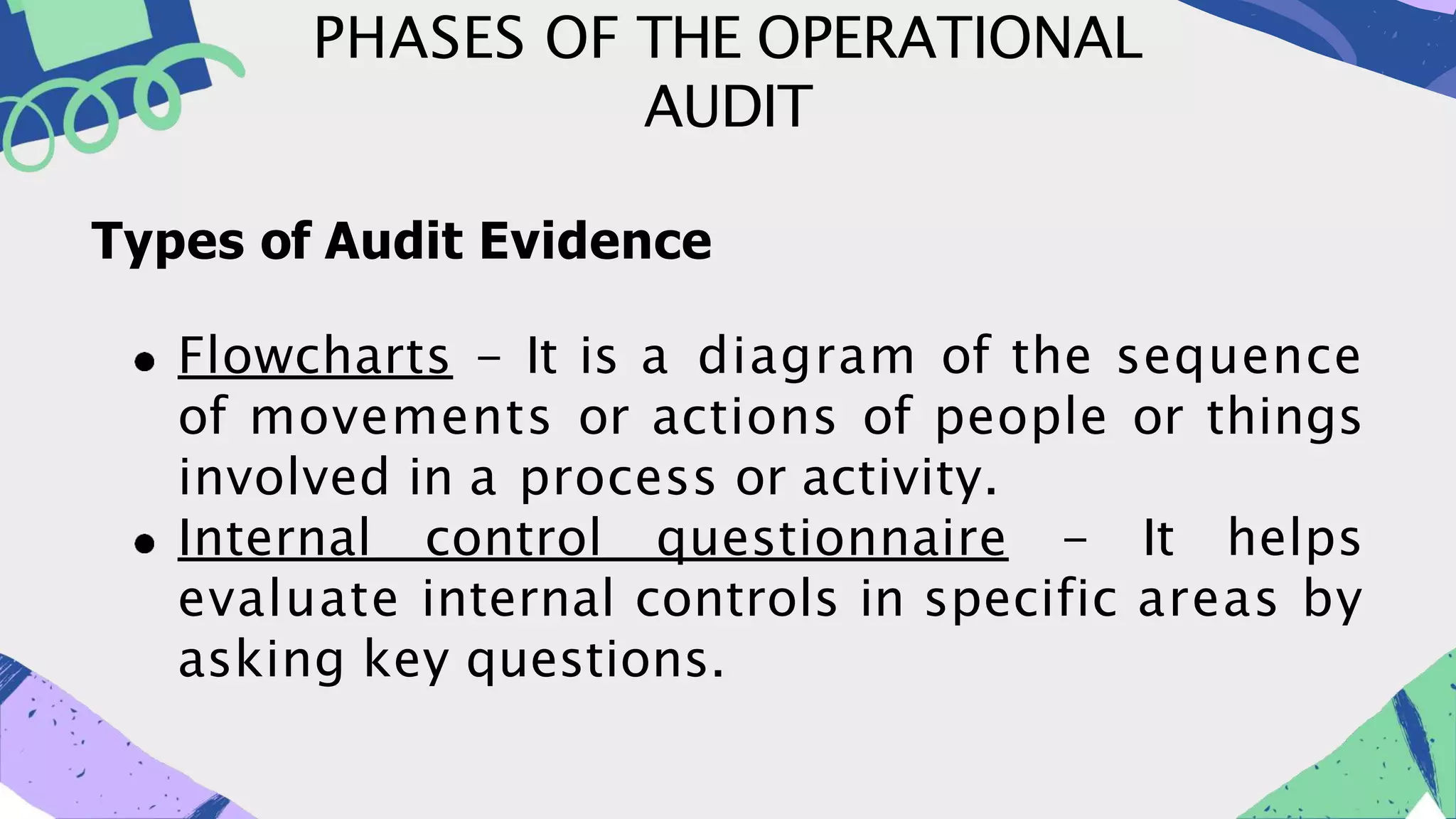

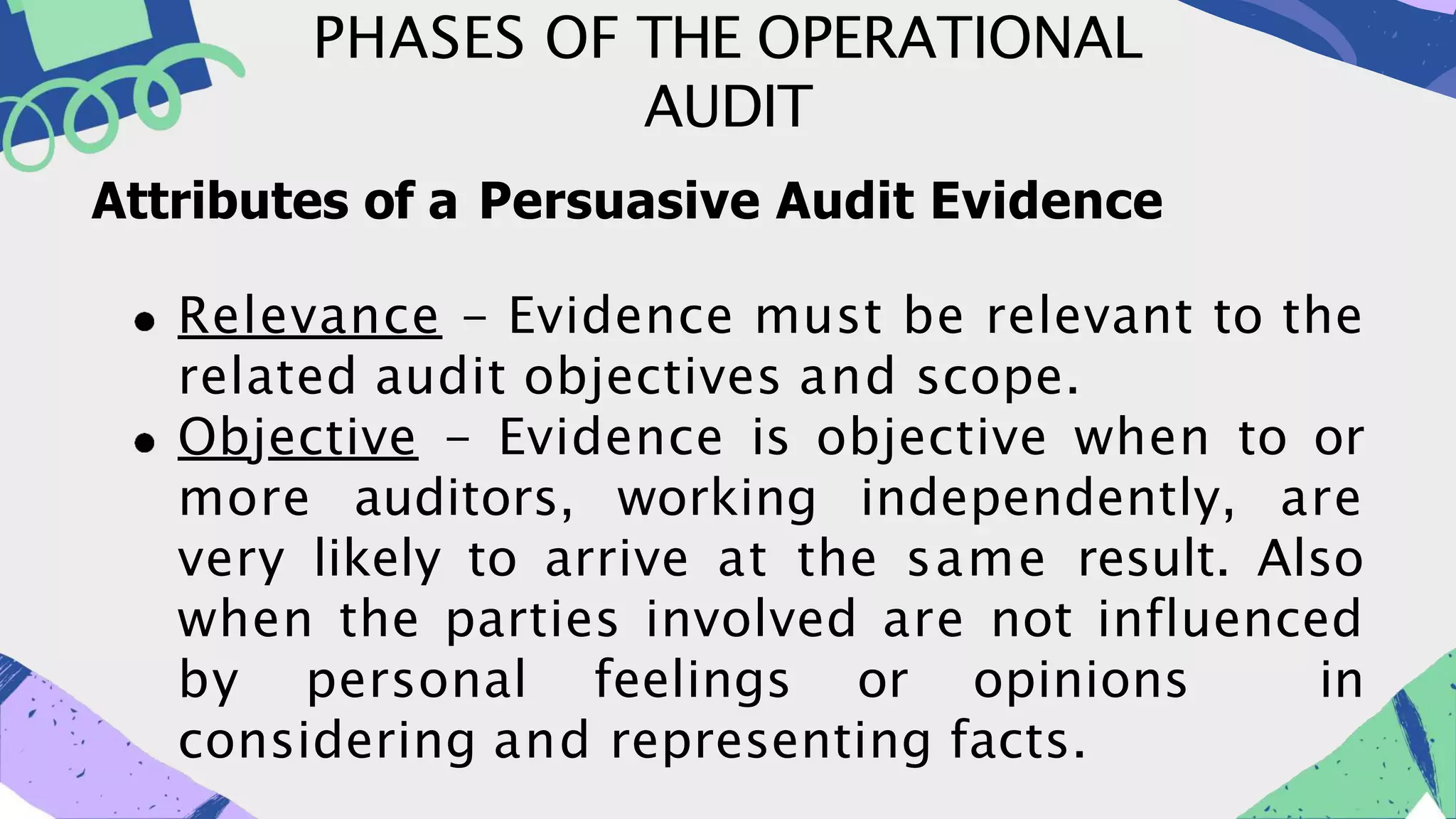

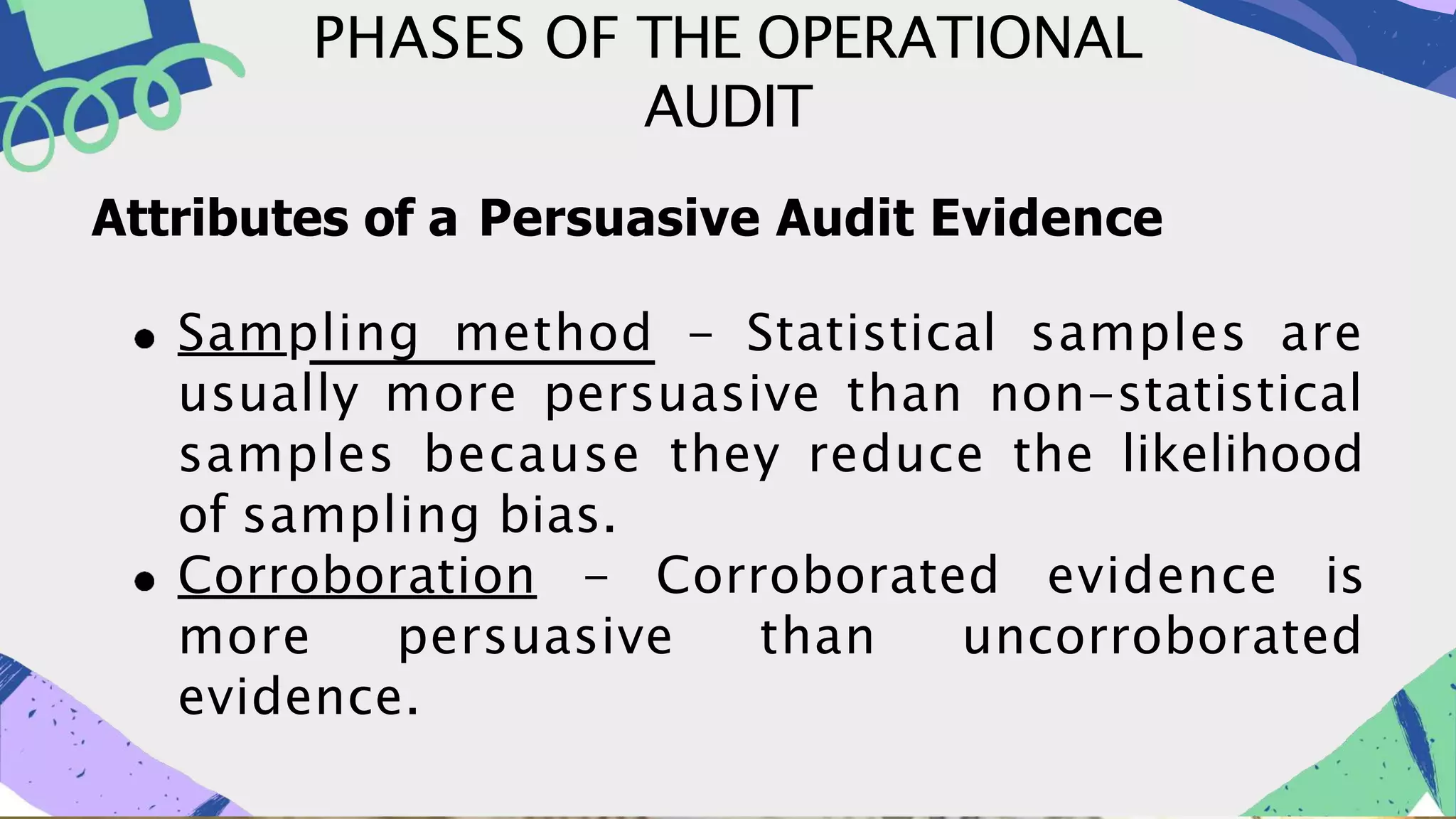

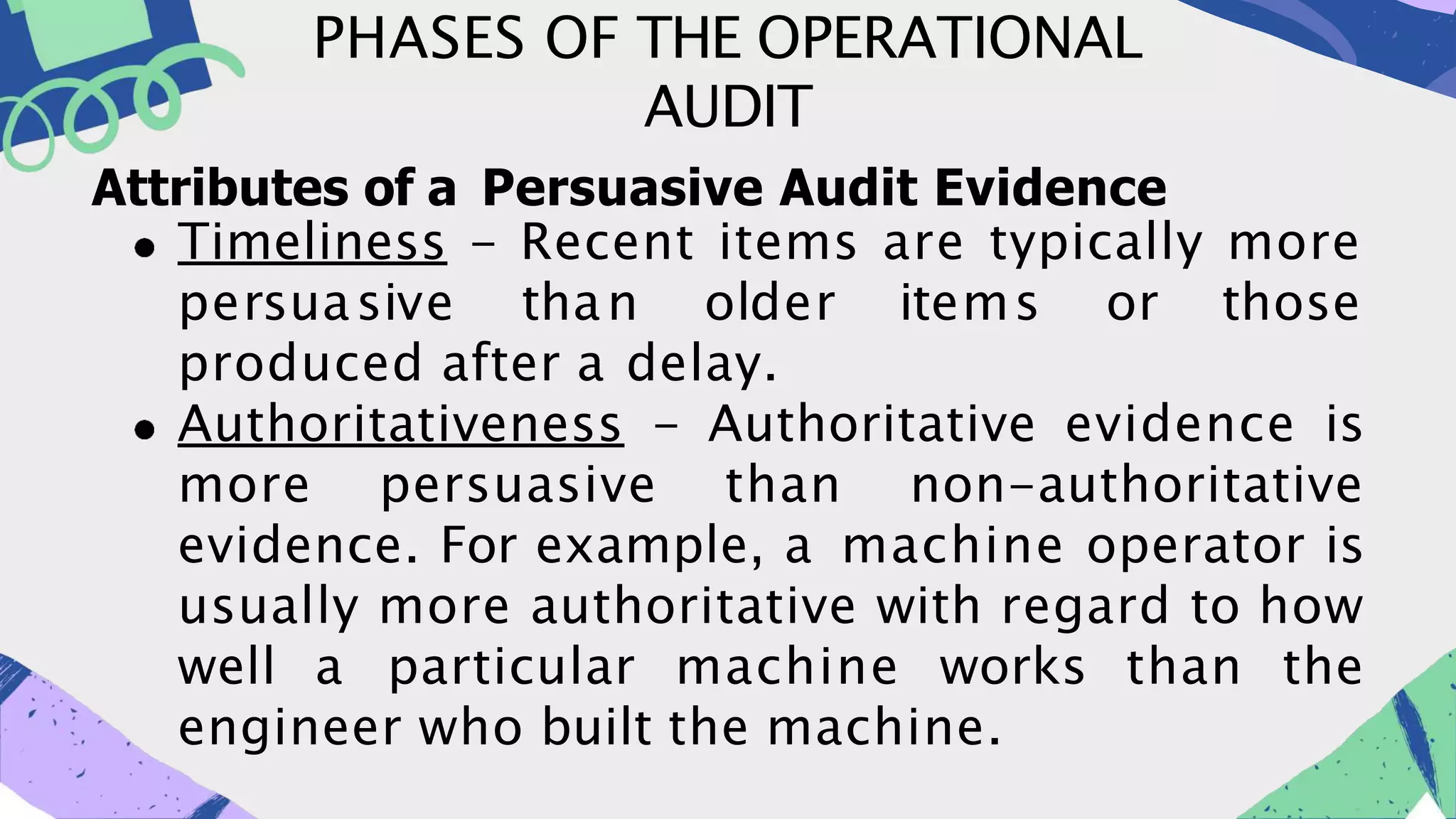

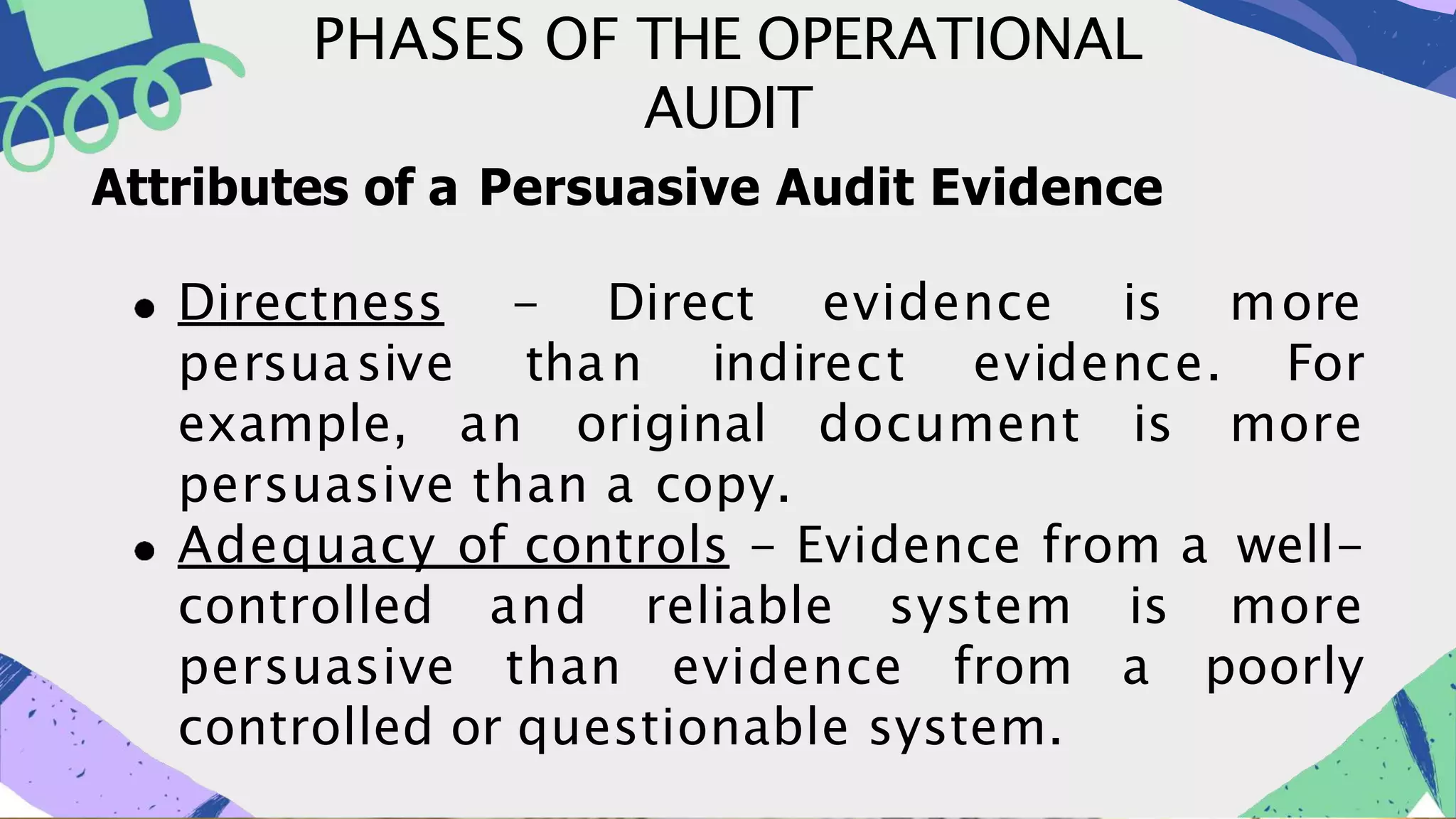

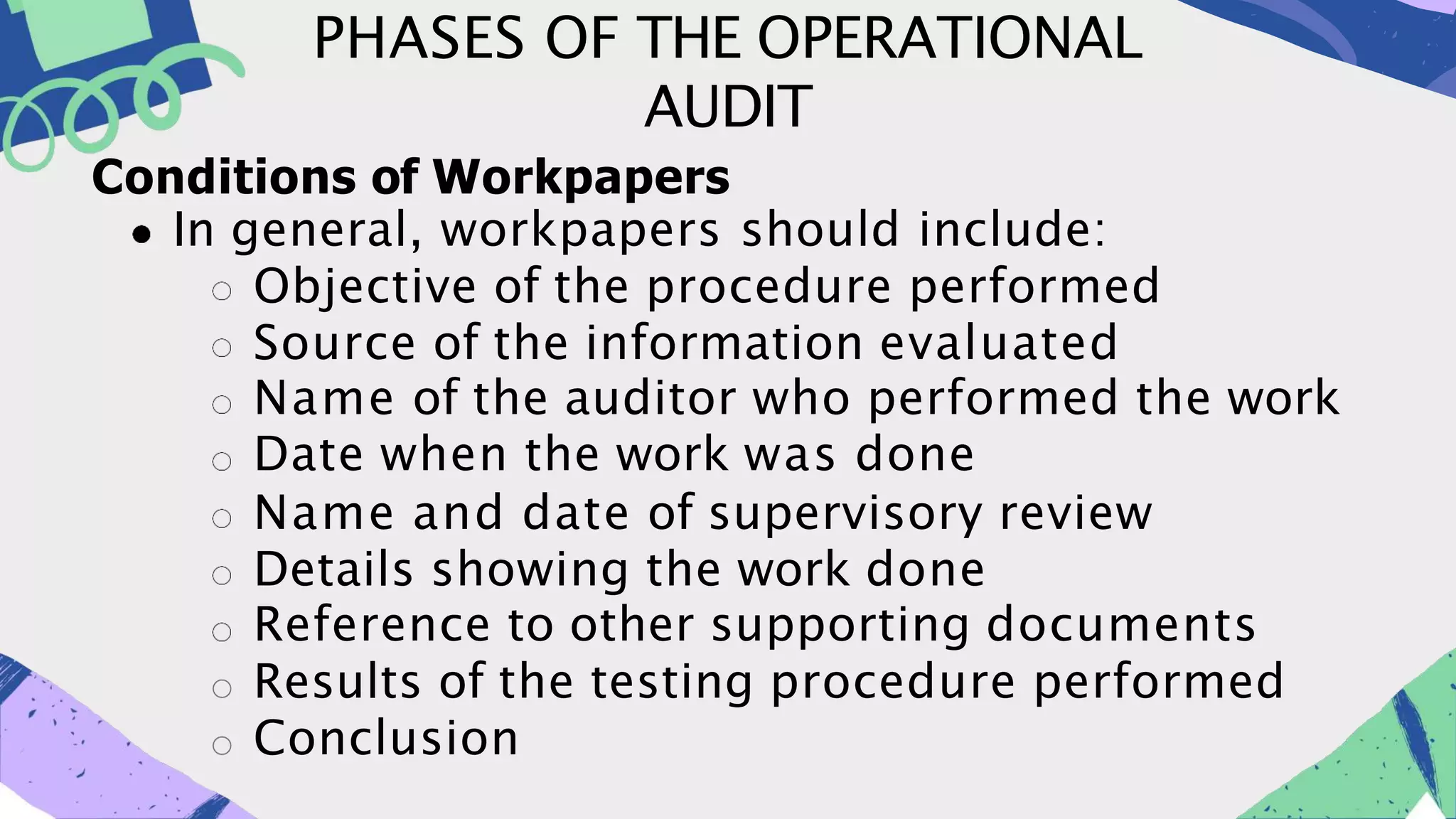

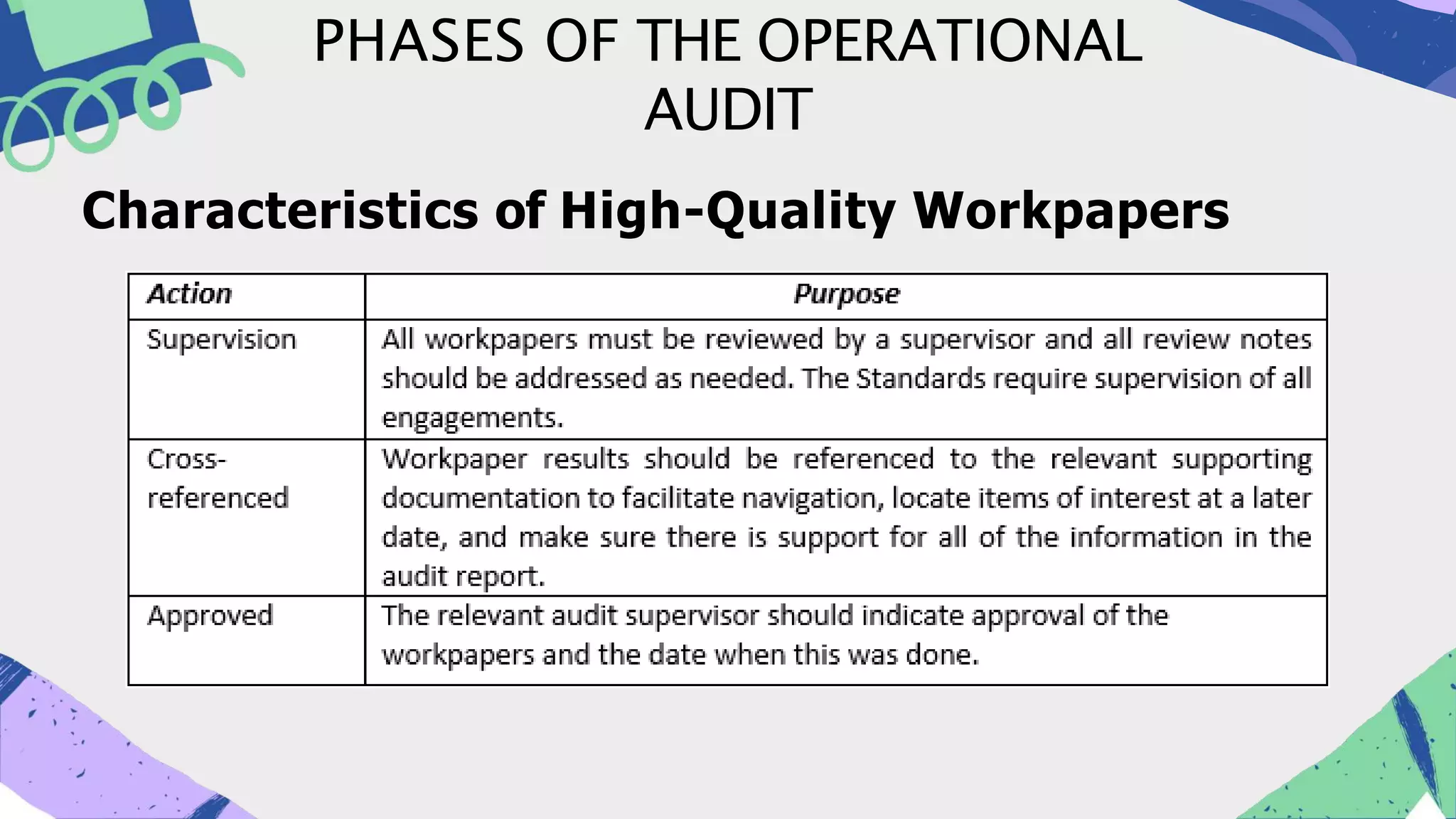

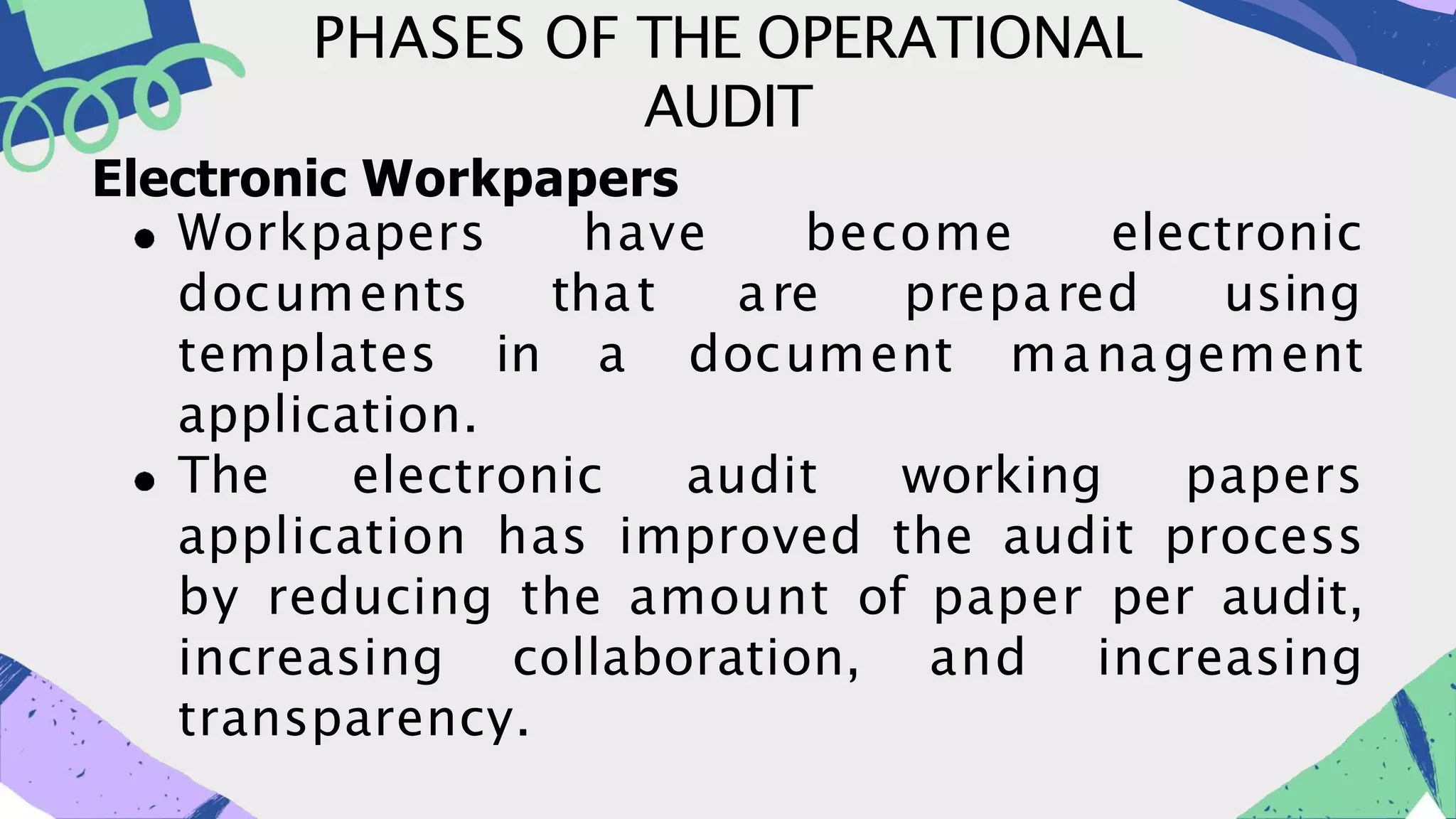

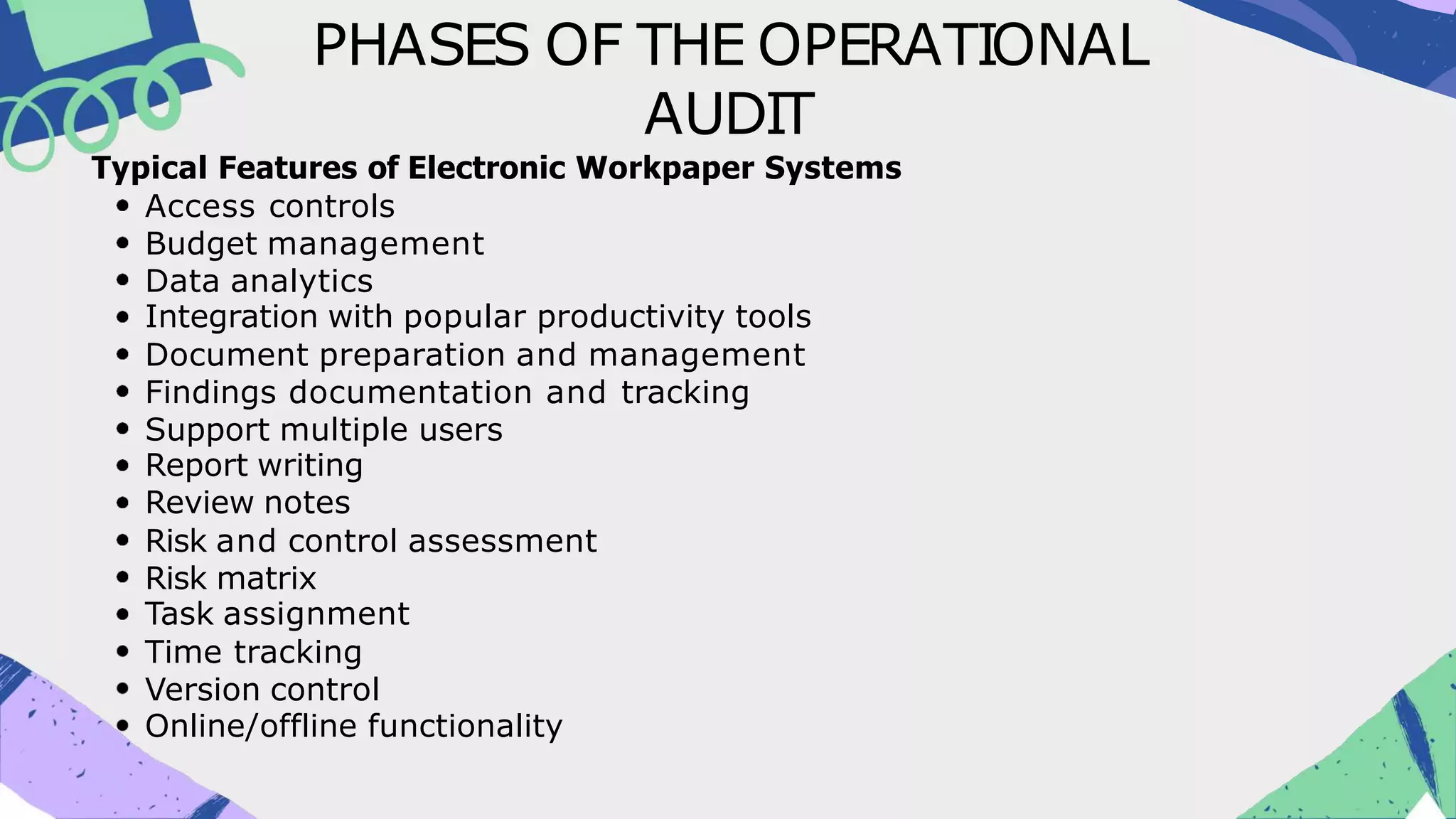

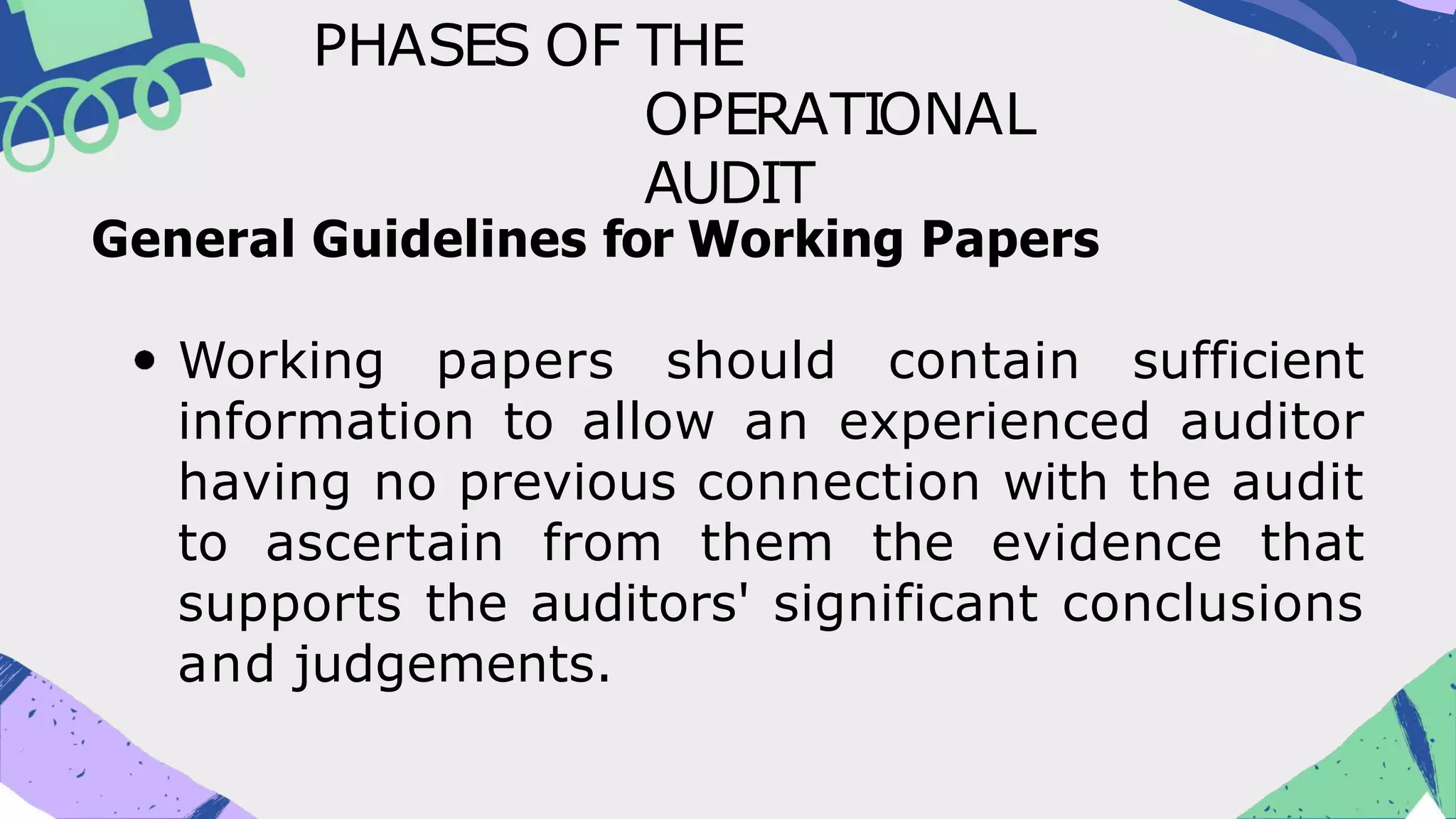

The key aspects of effective audits are persuasive evidence that is relevant, objective, documented, and corroborated. Workpapers should contain sufficient details to support conclusions and be prepared using electronic templates for organization and collaboration.

![AUDIT PLANNING AND PROCEDURES [Autosaved].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/4777auditplanningandproceduresautosaved-240818090542-6370a7b2-thumbnail.jpg?width=640&height=640&fit=bounds)