Downloaded 25 times

The document is a comprehensive guide on the audit of internal financial control over financial reporting (IFCR), outlining methodologies for auditors including planning, testing, and reporting. It emphasizes the importance of internal controls for reliable financial reporting and the auditor's responsibilities in assessing these controls. Key sections of the guide cover the processes involved in auditing, the risk control matrix, and the relationship between internal controls and financial statements.

Introduction to Internal Financial Control (IFCR) audit guidelines and objectives.

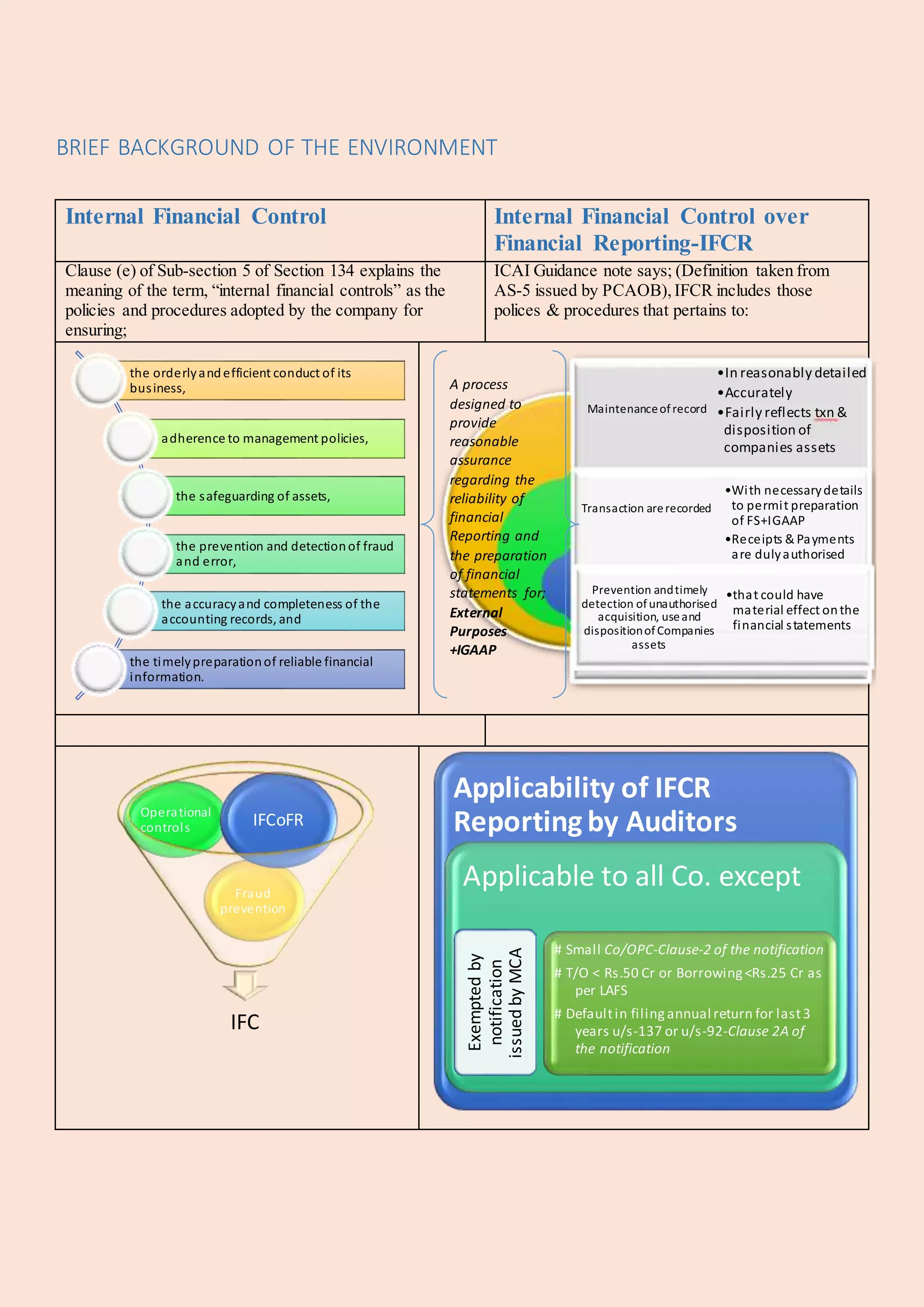

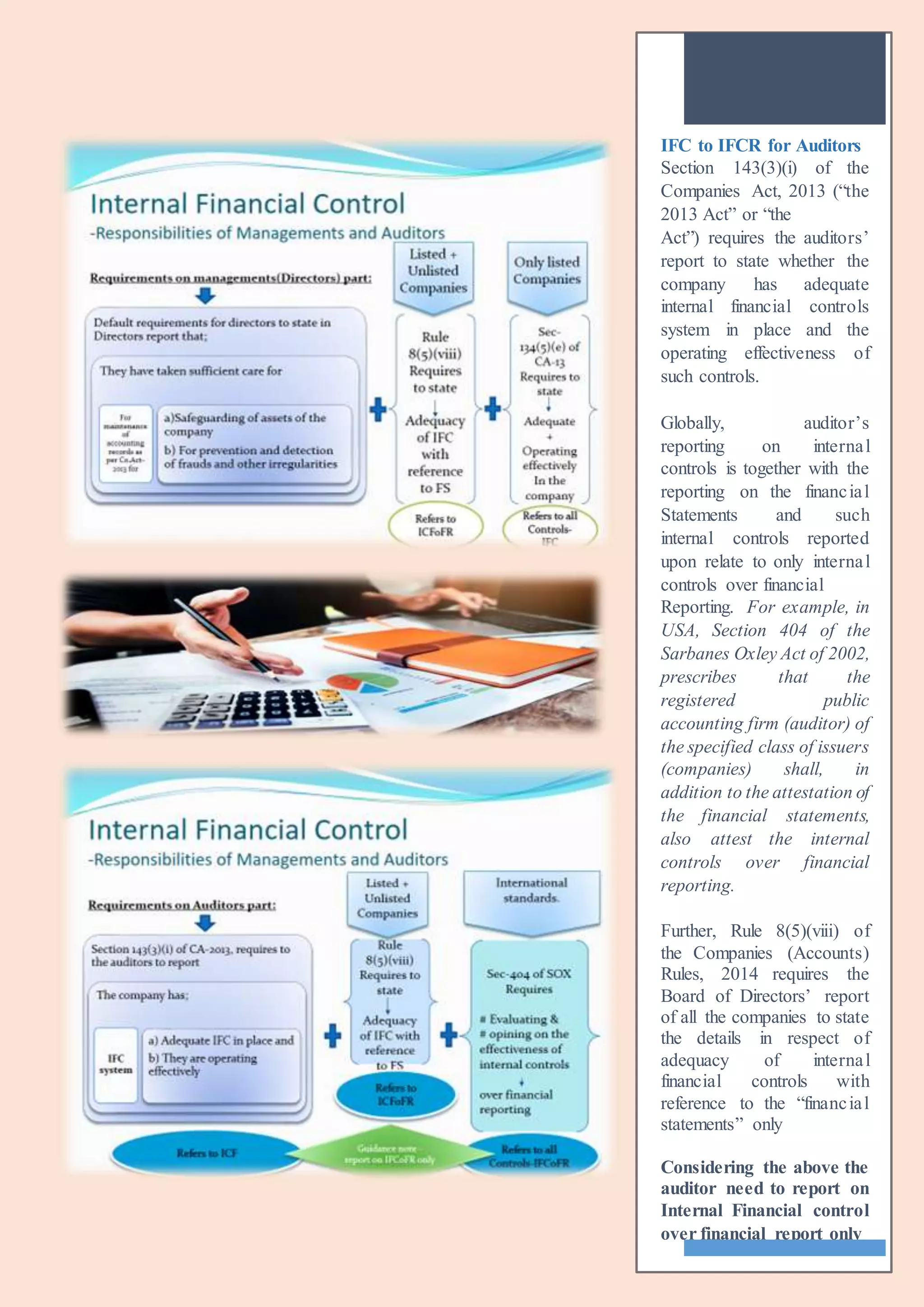

Details on internal financial controls, their definitions, applicability, and auditor's reporting requirements.

Procedural overview for planning audits, combining audits, and assessing risks of fraud.

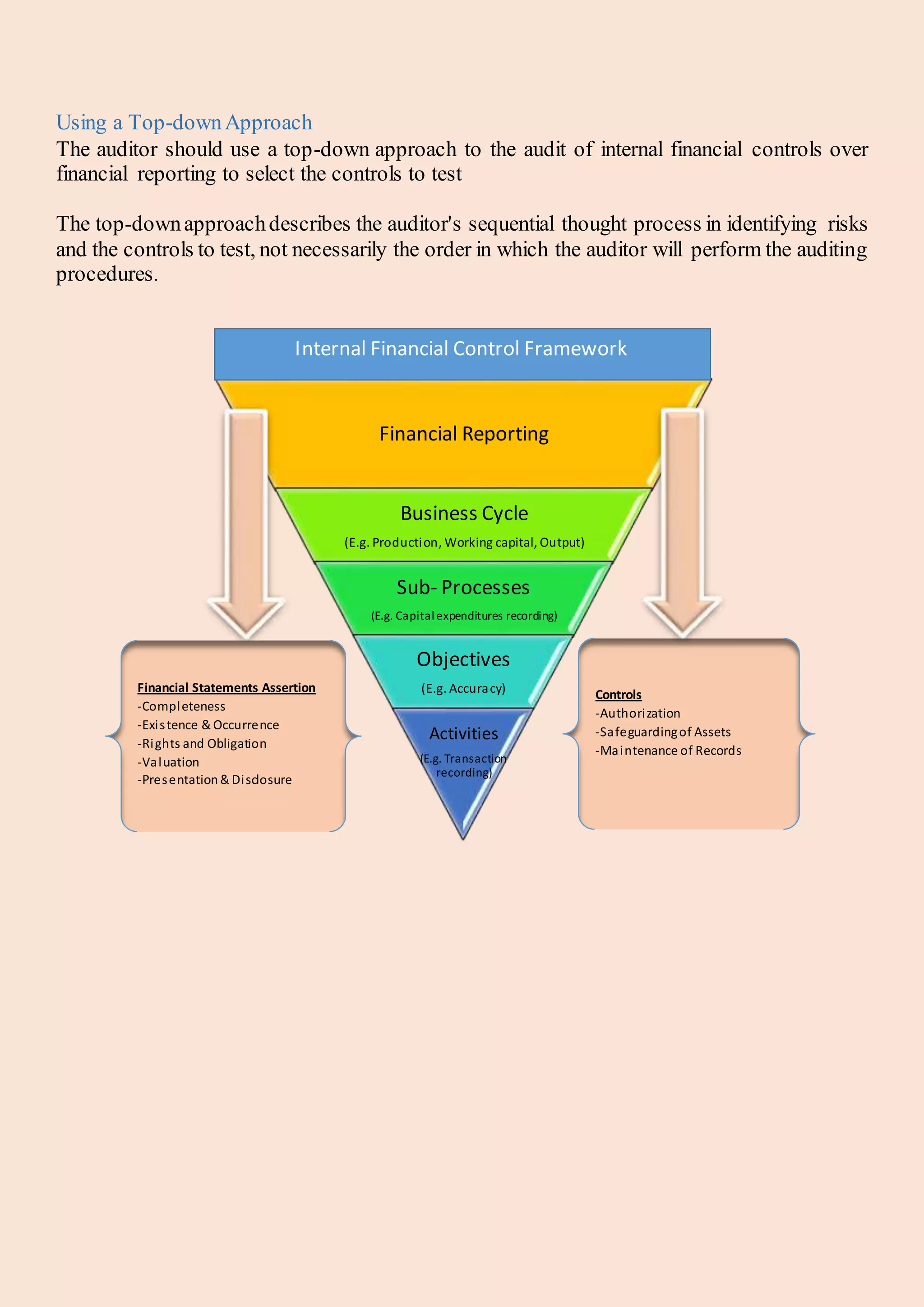

Utilization of a top-down approach for audits, flow diagrams for audit processes, and control testing.

Risk Control Matrix detailing documentation for risks and controls, alongside templates for risk of material misstatements.