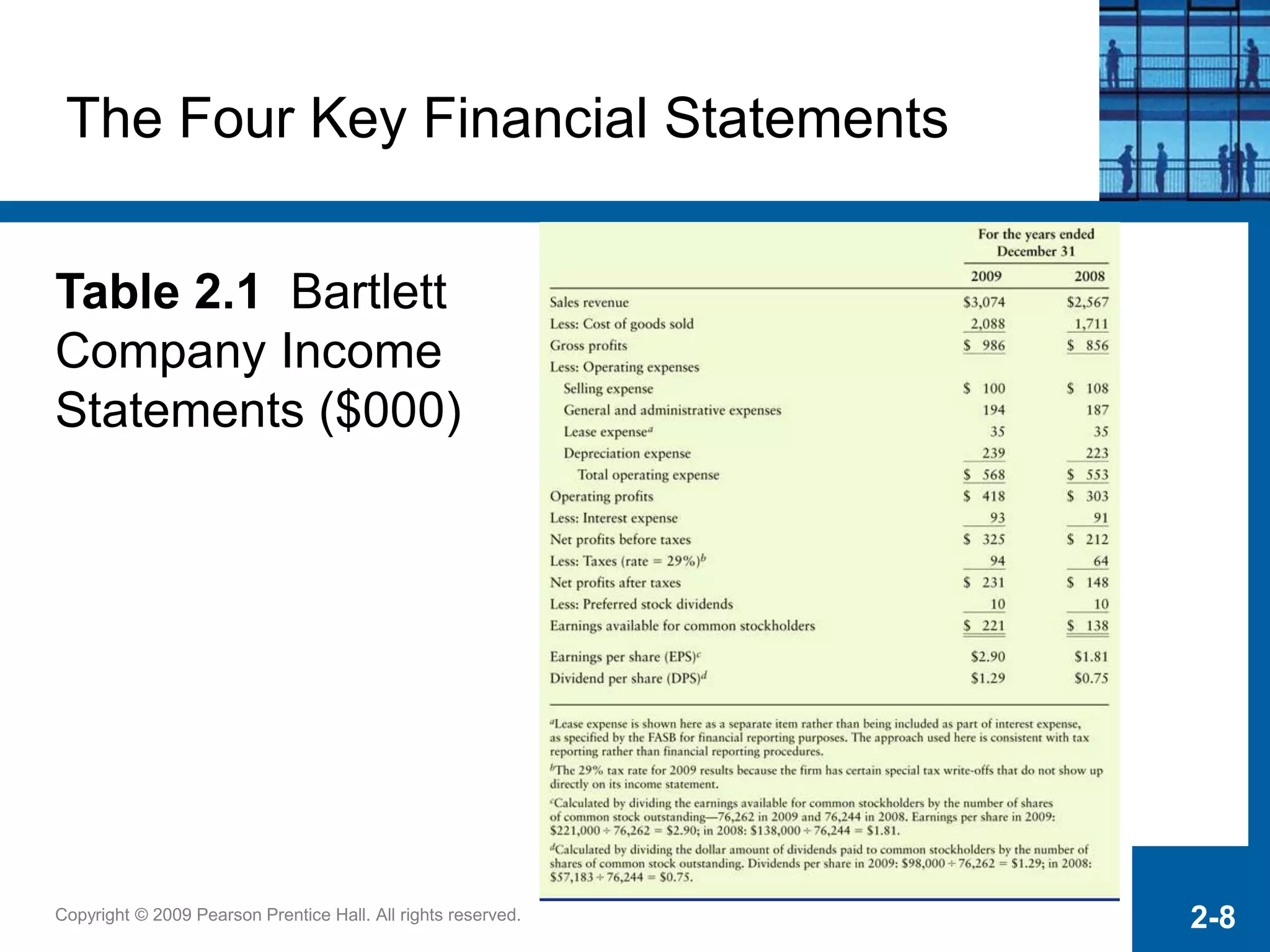

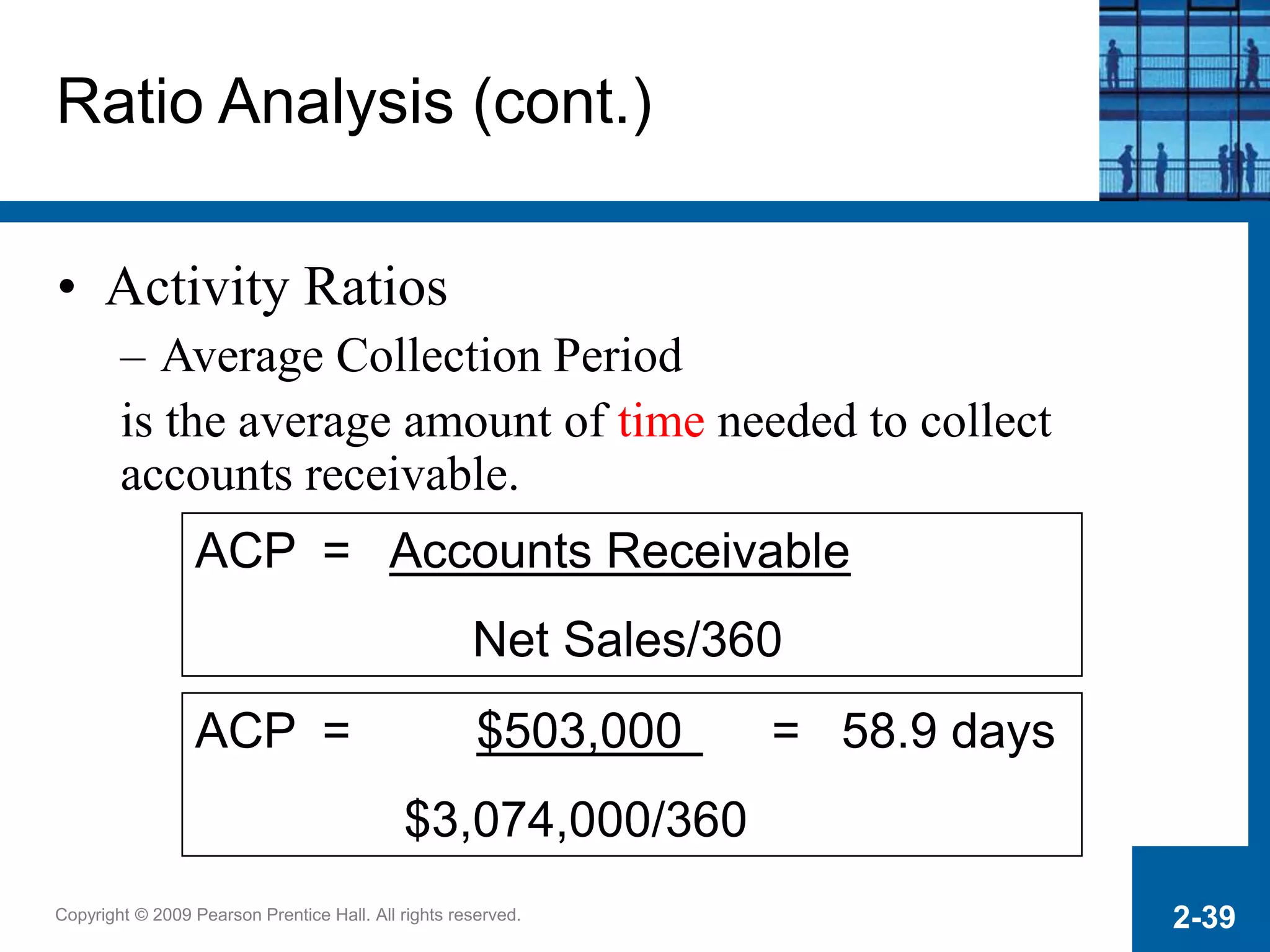

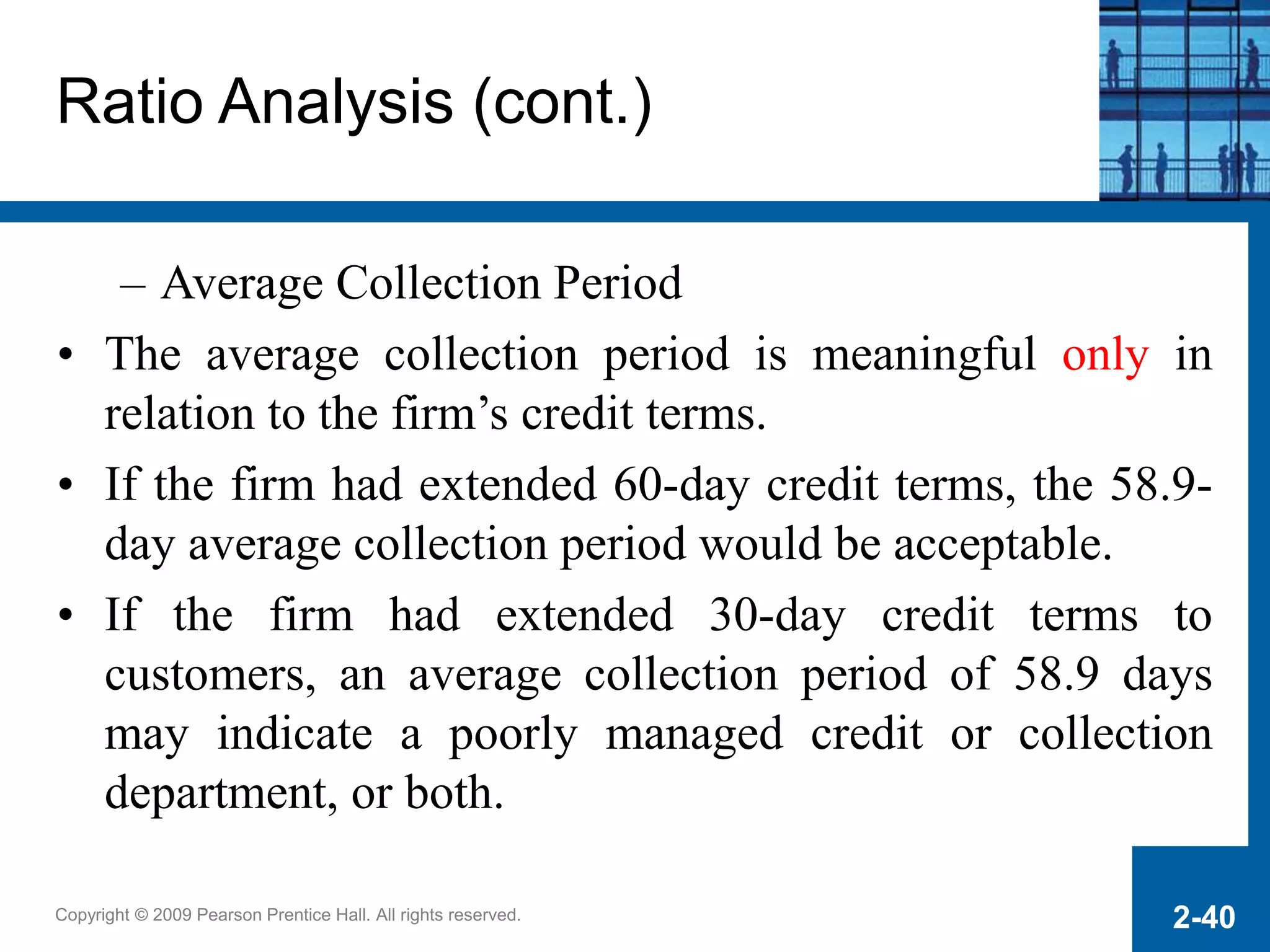

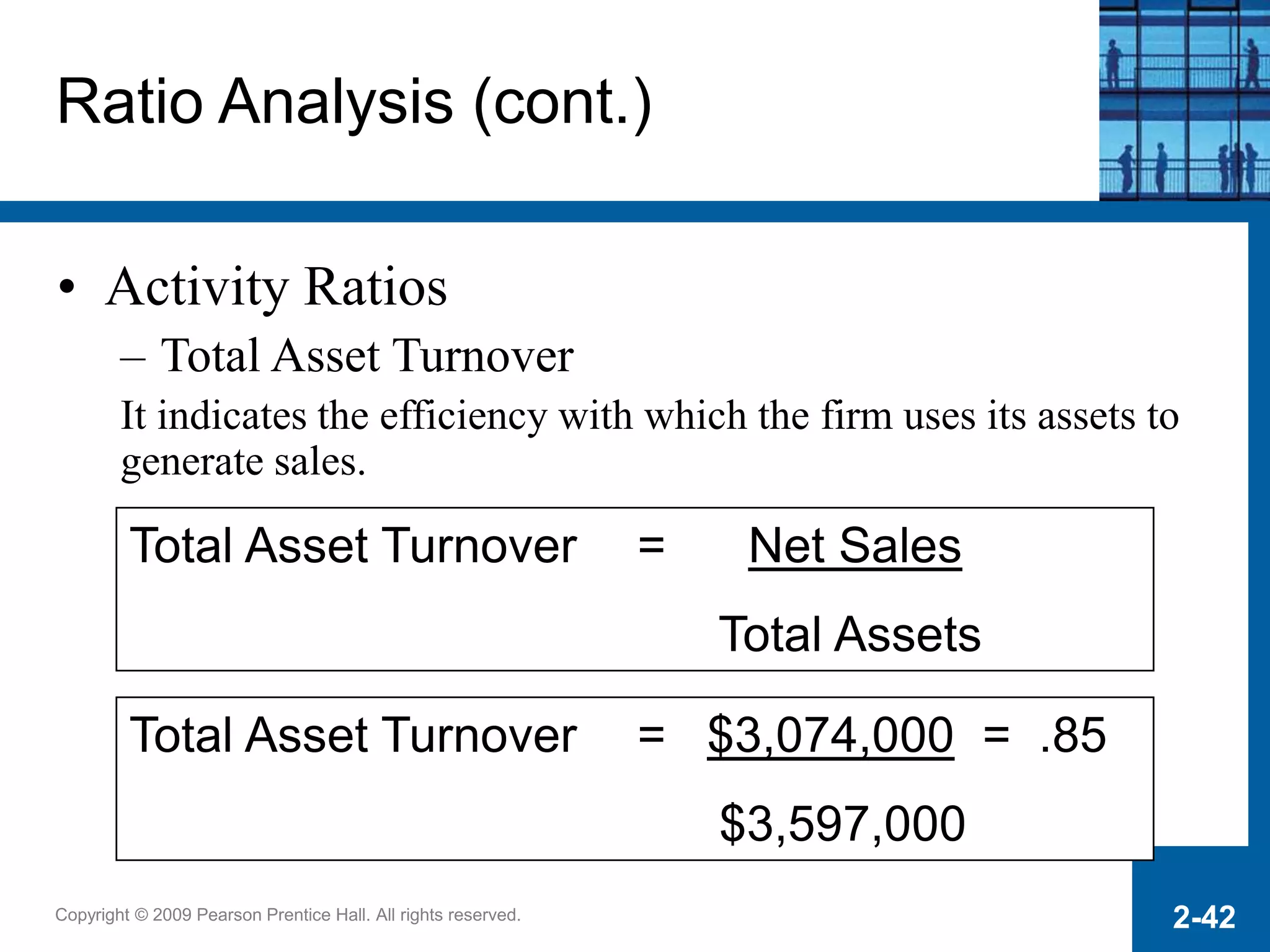

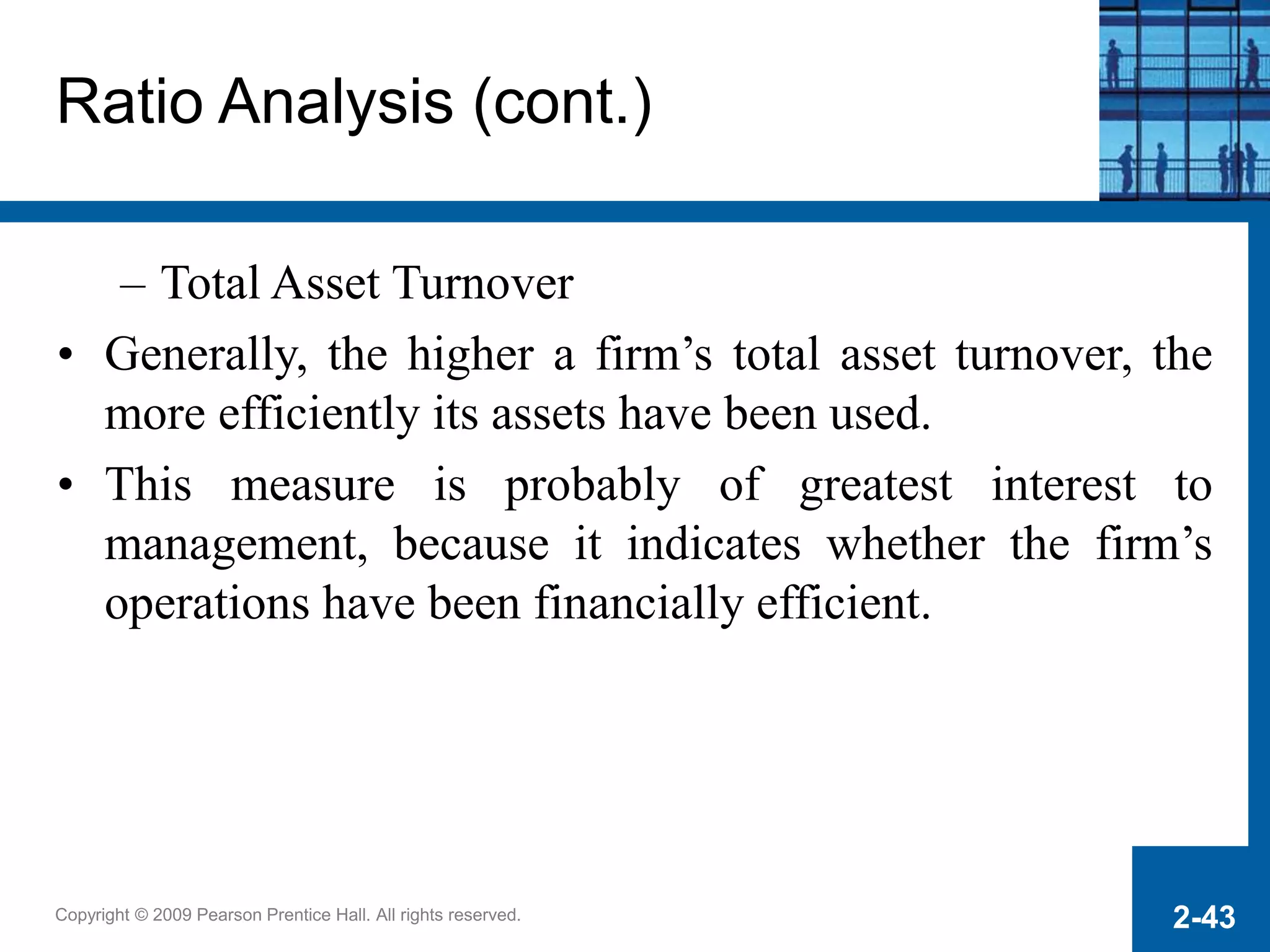

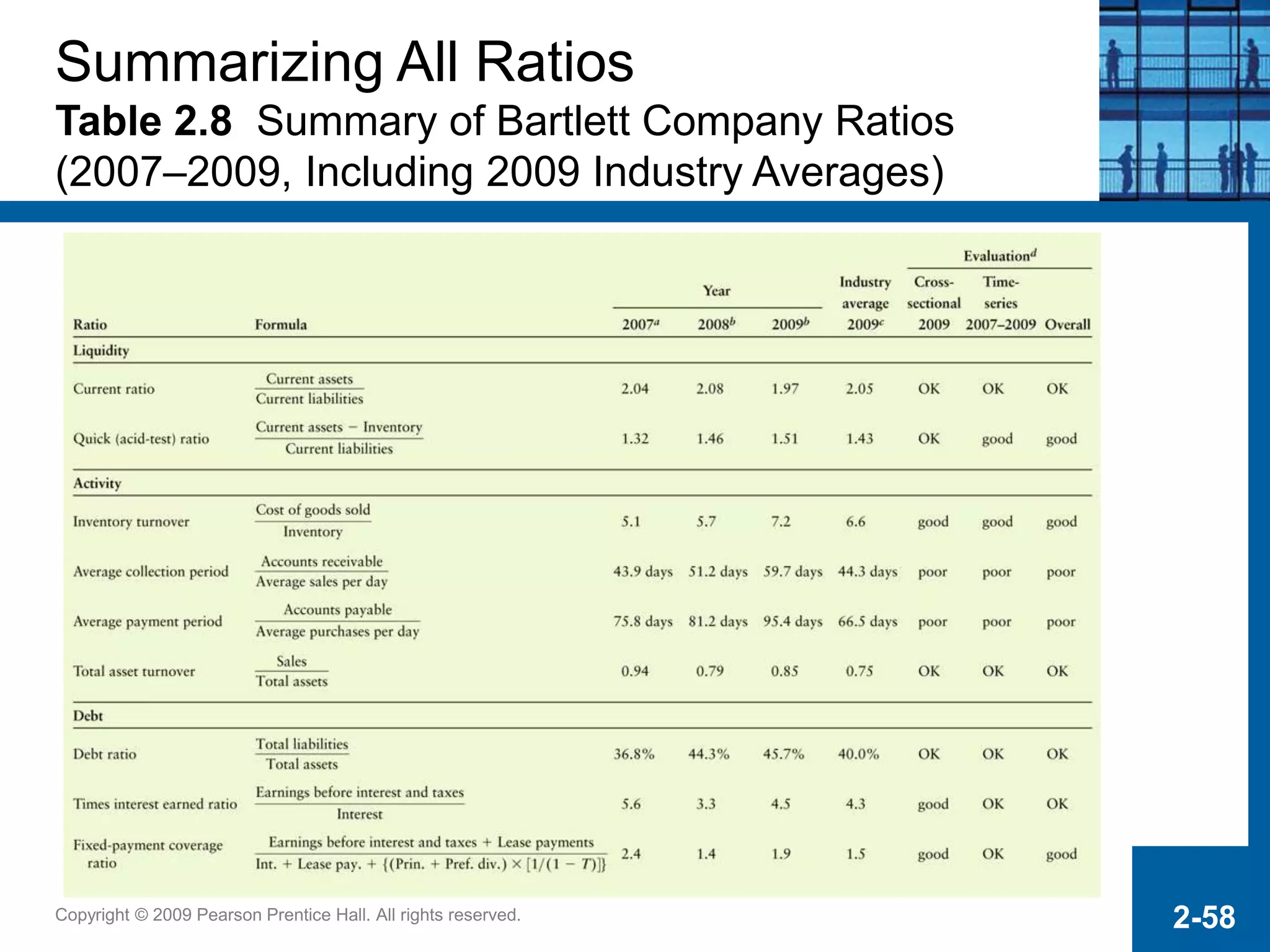

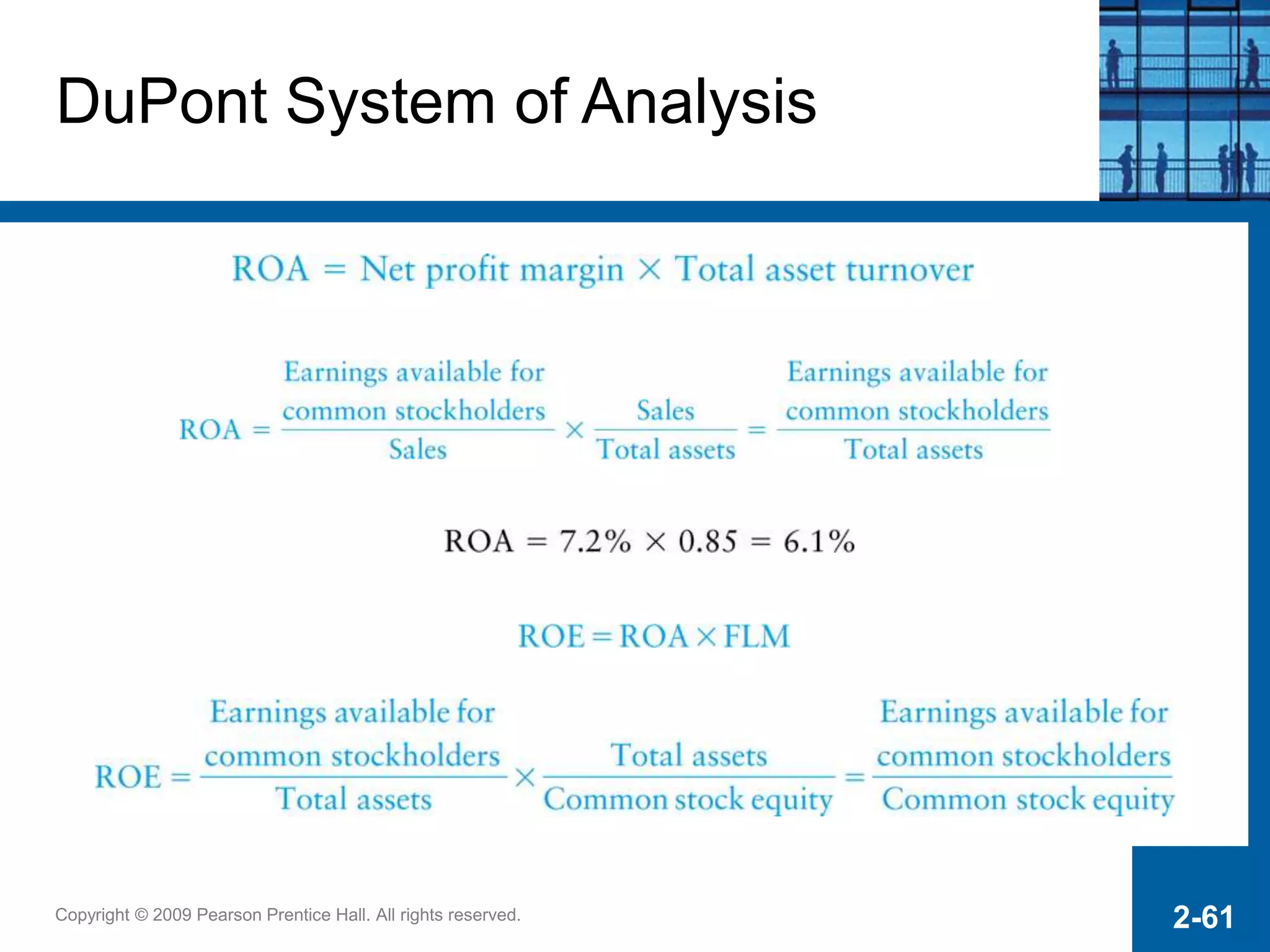

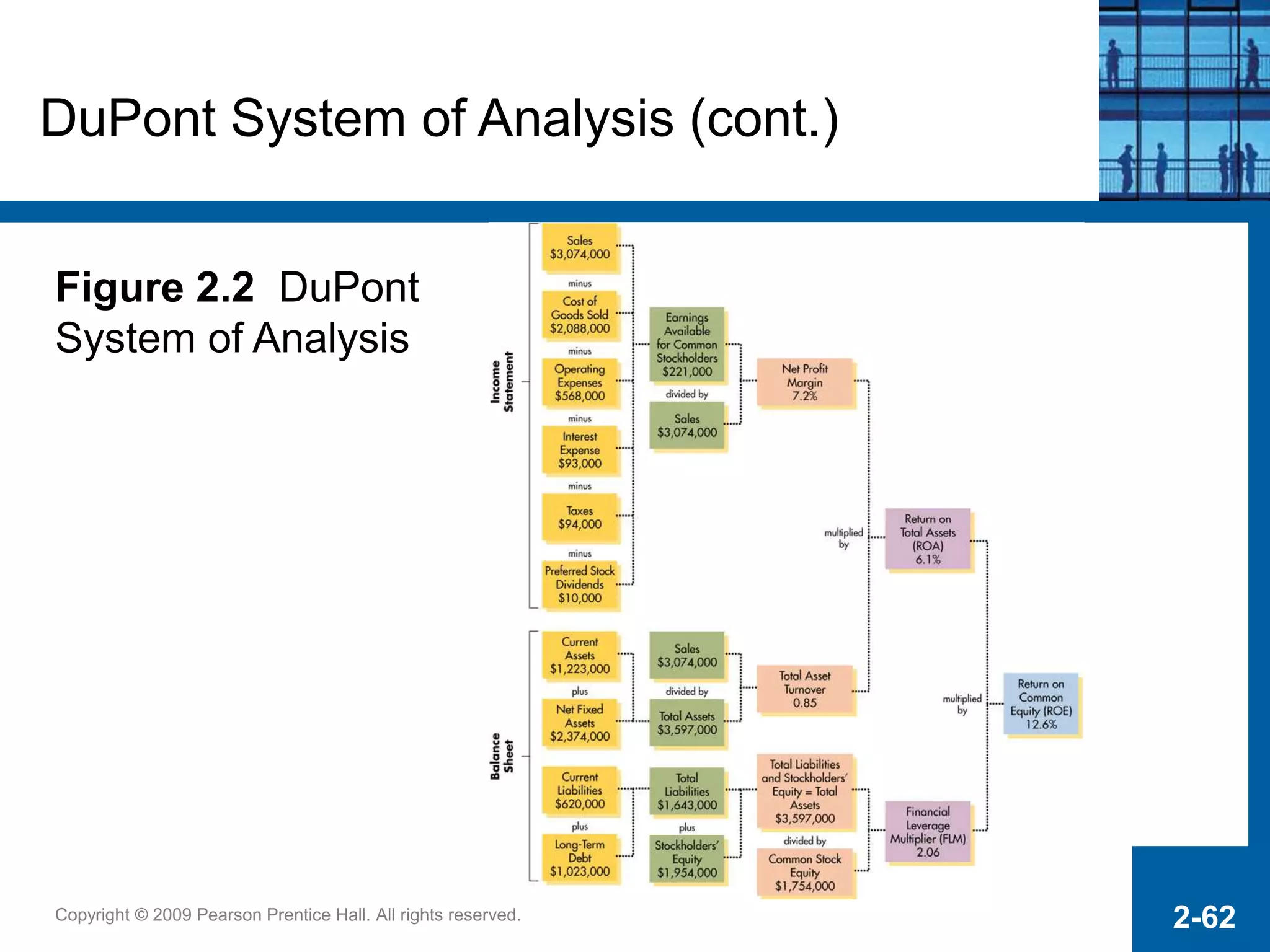

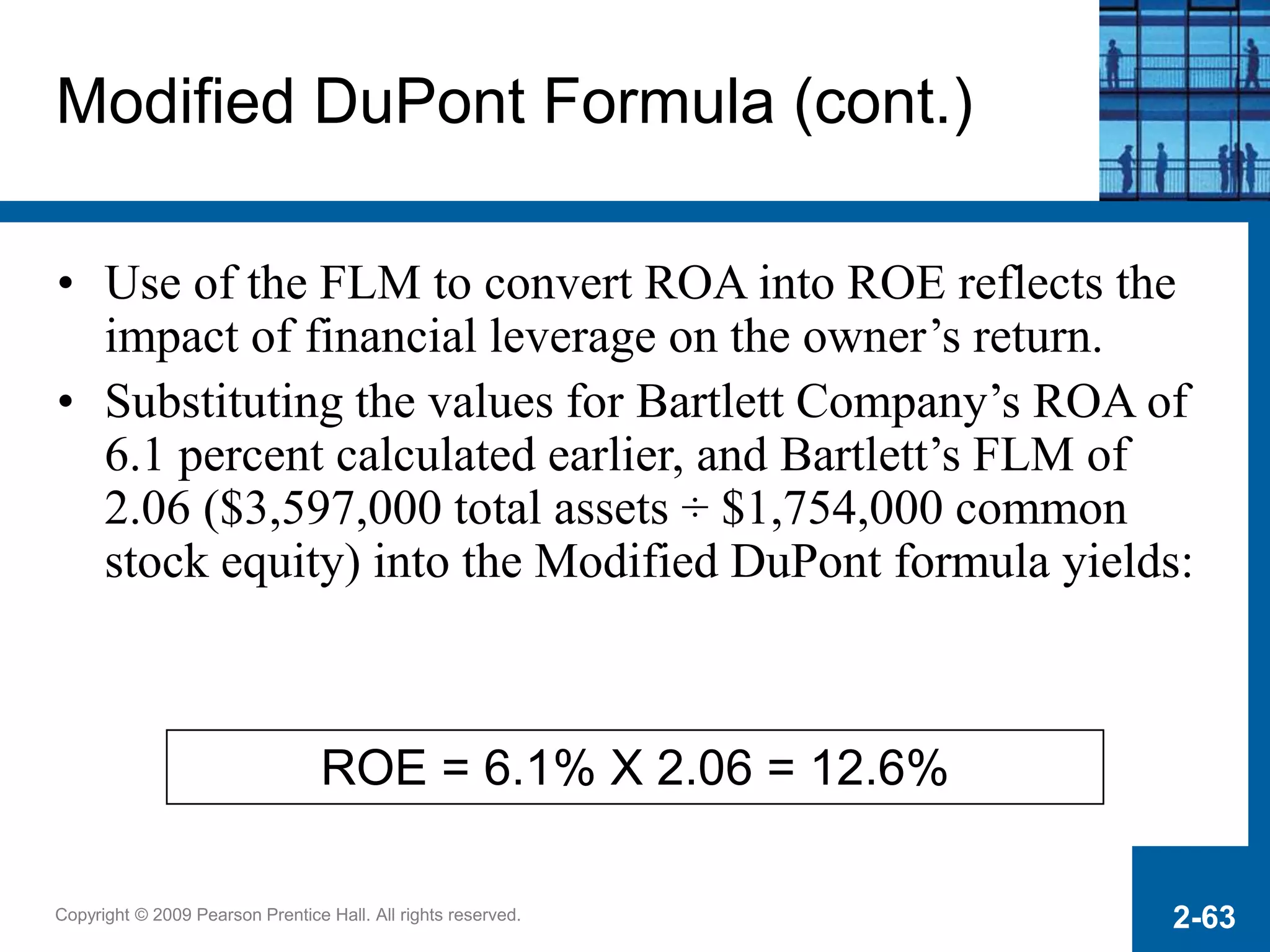

This document discusses key financial statements and ratio analysis. It covers the four main financial statements - the income statement, balance sheet, statement of retained earnings, and statement of cash flows - and what each reports. It then discusses ratio analysis and different types of ratios used to analyze a company's liquidity, debt, profitability, and market value. These ratios include the current ratio and quick ratio. The document provides examples of each financial statement and calculates ratios for a sample company.