Page

14-2

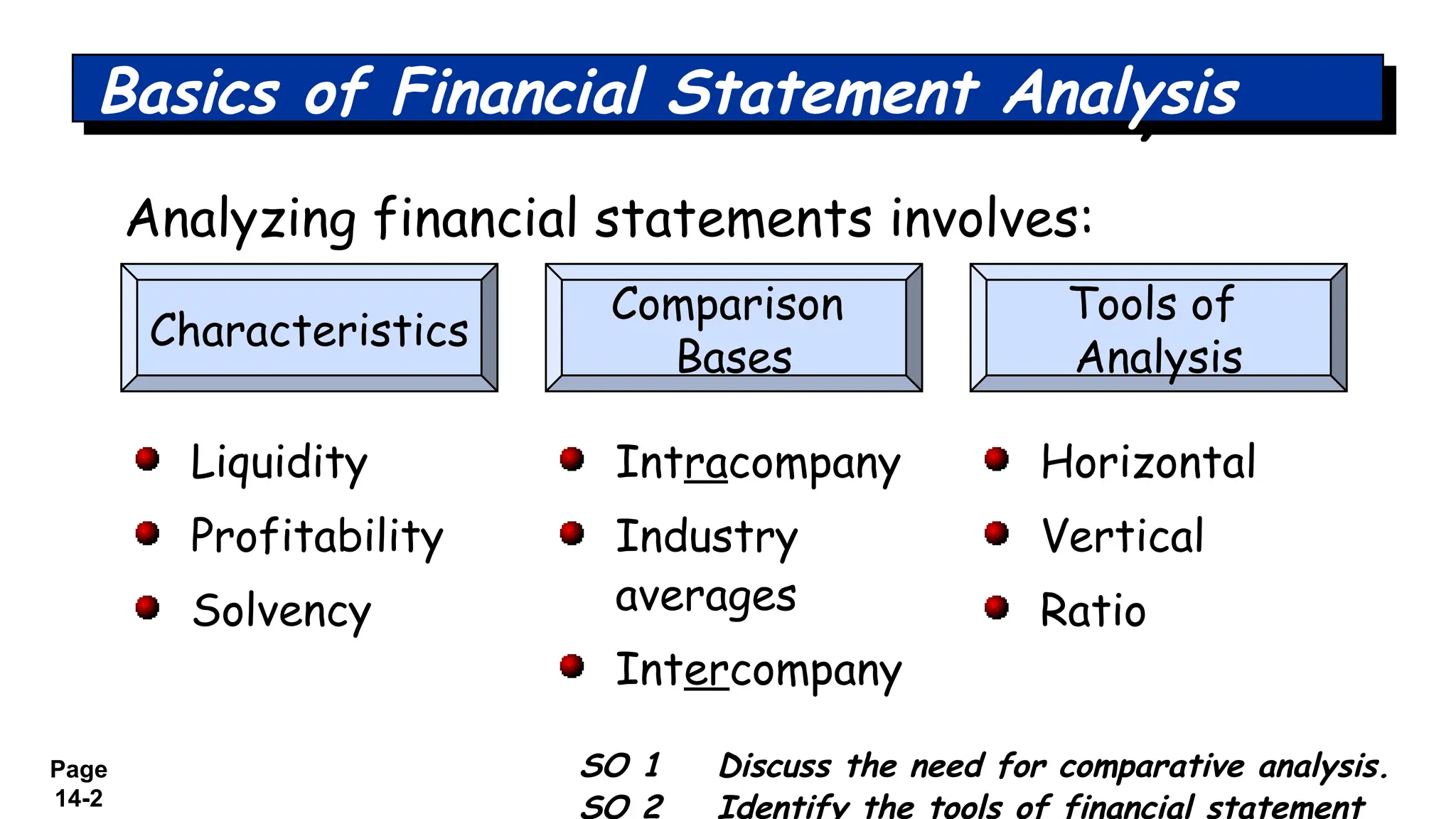

Analyzing financial statementsinvolves:

Basics of Financial Statement Analysis

Characteristics

Comparison

Bases

Tools of

Analysis

Liquidity

Profitability

Solvency

Intracompany

Industry

averages

Intercompany

Horizontal

Vertical

Ratio

SO 1 Discuss the need for comparative analysis.

SO 2 Identify the tools of financial statement

3.

Page

14-3 SO 3Explain and apply horizontal analysis.

Horizontal Analysis

Horizontal analysis, also called trend analysis, is a

technique for evaluating a series of financial

statement data over a period of time.

Its purpose is to determine the increase or decrease

that has taken place.

Horizontal analysis is commonly applied to the balance

sheet, income statement, and statement of retained

earnings.

4.

Page

14-4 SO 3Explain and apply horizontal analysis.

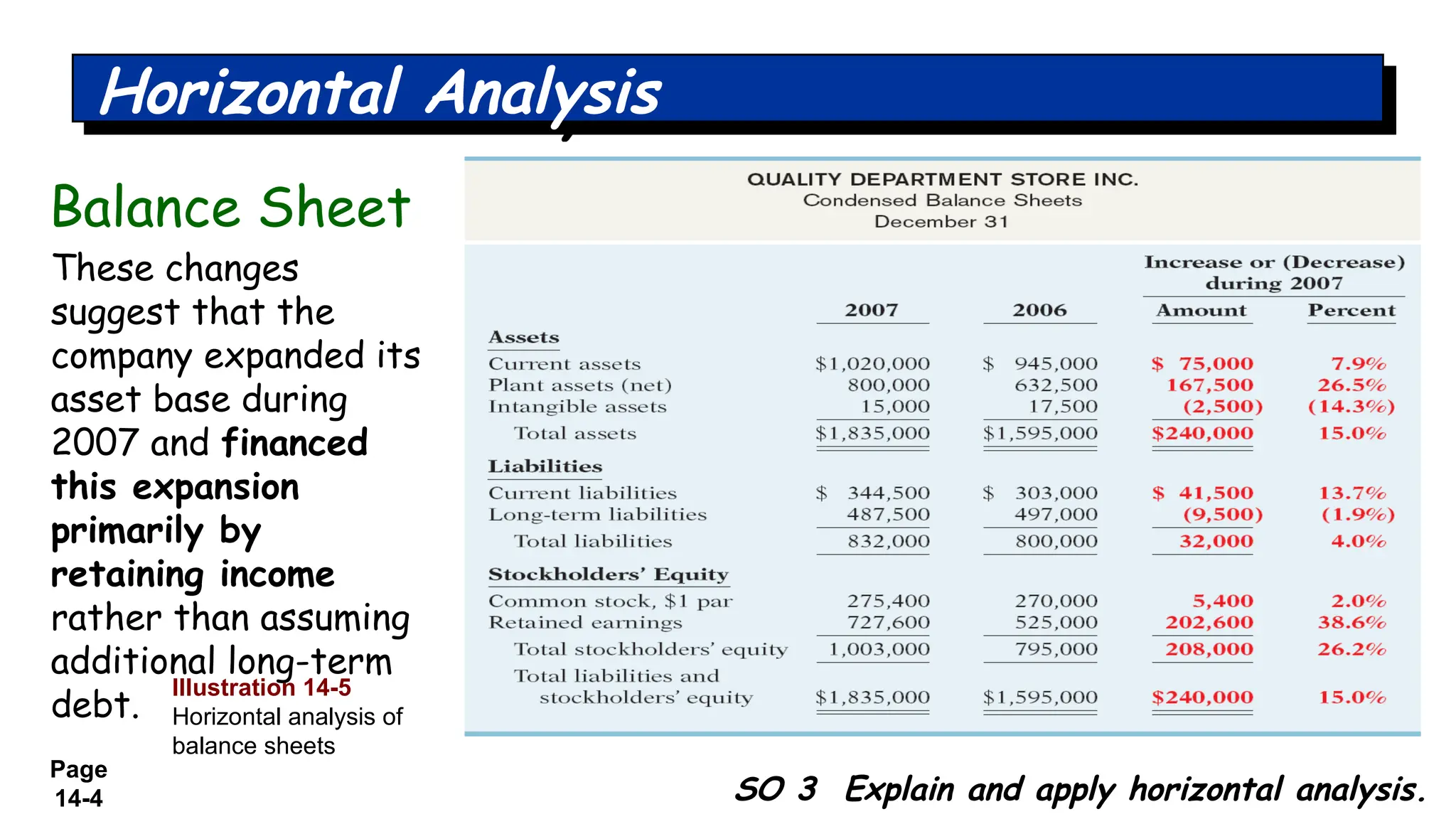

These changes

suggest that the

company expanded its

asset base during

2007 and financed

this expansion

primarily by

retaining income

rather than assuming

additional long-term

debt.

Horizontal Analysis

Balance Sheet

Illustration 14-5

Horizontal analysis of

balance sheets

5.

Page

14-5 SO 3Explain and apply horizontal analysis.

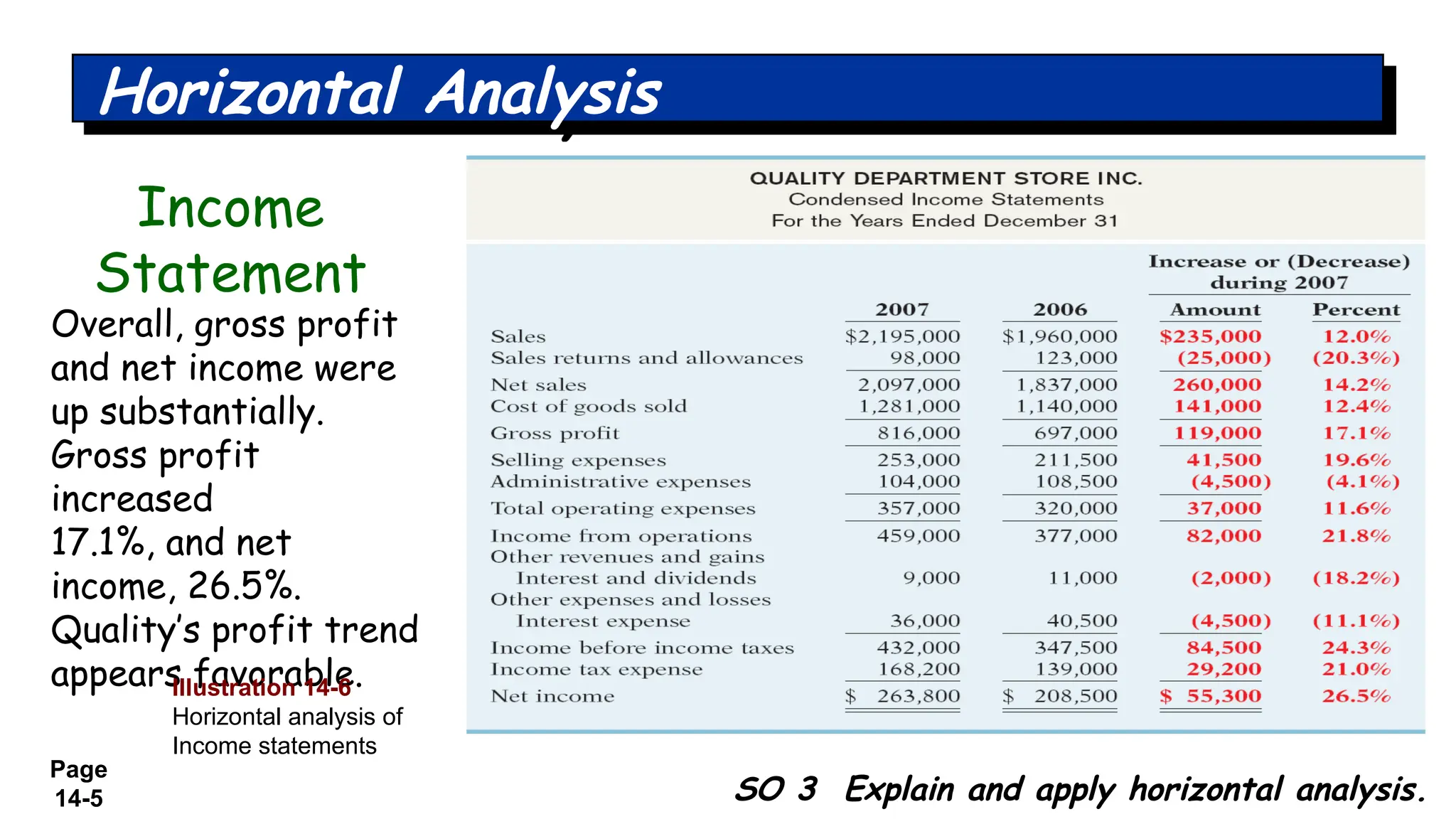

Overall, gross profit

and net income were

up substantially.

Gross profit

increased

17.1%, and net

income, 26.5%.

Quality’s profit trend

appears favorable.

Horizontal Analysis

Income

Statement

Illustration 14-6

Horizontal analysis of

Income statements

6.

Page

14-6 SO 3Explain and apply horizontal analysis.

We saw in the horizontal analysis of the balance sheet that ending retained

earnings increased 38.6%. As indicated earlier, the company retained a

significant portion of net income to finance additional plant facilities.

Horizontal Analysis

Illustration 14-7

Horizontal analysis of

retained earnings

statements

Retained

Earnings

Statement

7.

Page

14-7

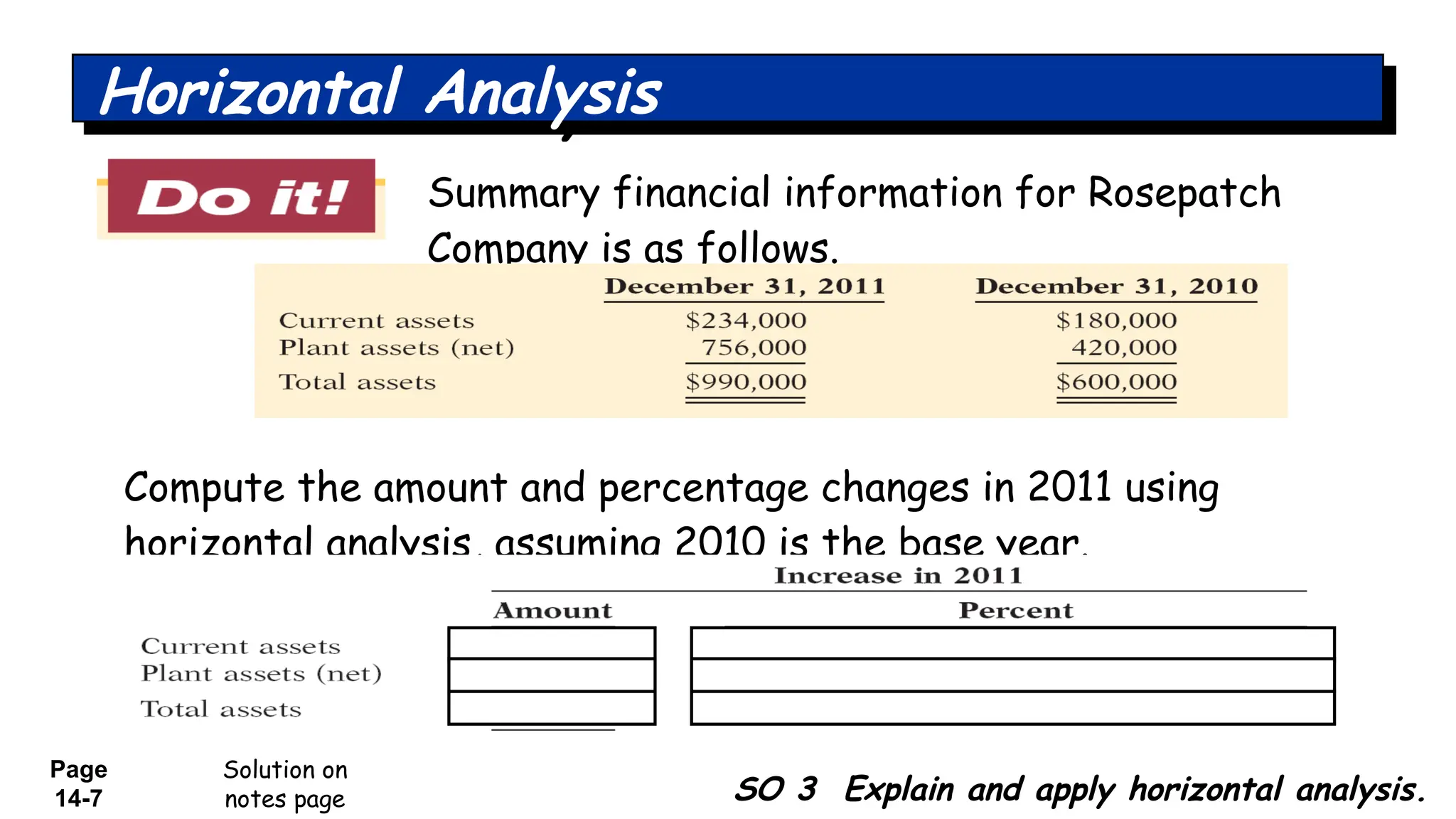

Summary financial informationfor Rosepatch

Company is as follows.

Solution on

notes page SO 3 Explain and apply horizontal analysis.

Horizontal Analysis

Compute the amount and percentage changes in 2011 using

horizontal analysis, assuming 2010 is the base year.

8.

Page

14-8 SO 4Describe and apply vertical analysis.

Vertical Analysis

Vertical analysis, also called common-size analysis, is

a technique that expresses each financial statement

item as a percent of a base amount.

On an income statement, we might say that selling

expenses are 16% of net sales.

Vertical analysis is commonly applied to the balance

sheet and the income statement.

9.

Page

14-9

These results

reinforce the

earlierobservations

that Quality is

choosing to finance

its growth through

retention of

earnings rather

than through

issuing additional

debt.

Balance Sheet

Illustration 14-8

Vertical analysis of

balance sheets

SO 4 Describe and apply vertical analysis.

Vertical Analysis

10.

Page

14-10

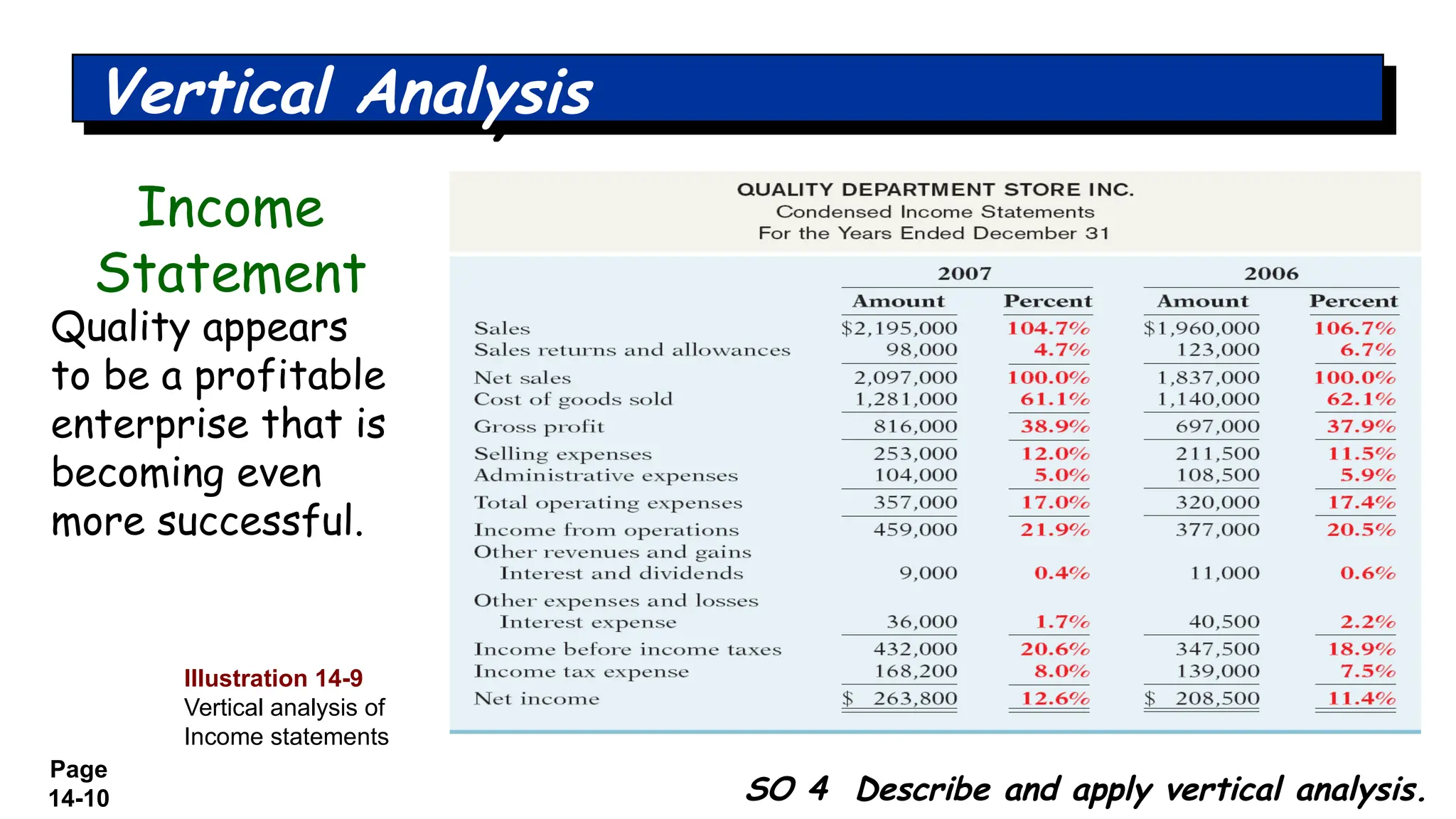

Quality appears

to bea profitable

enterprise that is

becoming even

more successful.

Income

Statement

Illustration 14-9

Vertical analysis of

Income statements

SO 4 Describe and apply vertical analysis.

Vertical Analysis

11.

Page

14-11

Enables a comparisonof companies of different sizes.

Illustration 14-10

Intercompany income

statement comparison

SO 4 Describe and apply vertical analysis.

Vertical Analysis

J.C. Penney earned net income more than 4,208 times larger than Quality’s, J.C.

Penney’s net income as a percent of each sales dollar (5.6%) is only 44% of

Quality’s (12.6%).

12.

Basic Financial Analysis

Ratio analysis involves methods of

calculating and interpreting

financial ratios to assess a firm’s

financial condition and

performance.

It is of interest to shareholders,

creditors, and the firm’s own

management

13.

BASIC FINANCIAL ANALYSIS

Ratio analysis involves methods of calculating and

interpreting financial ratios to assess a firm’s

financial condition and performance.

It is of interest to shareholders, creditors, and the

firm’s own management

14.

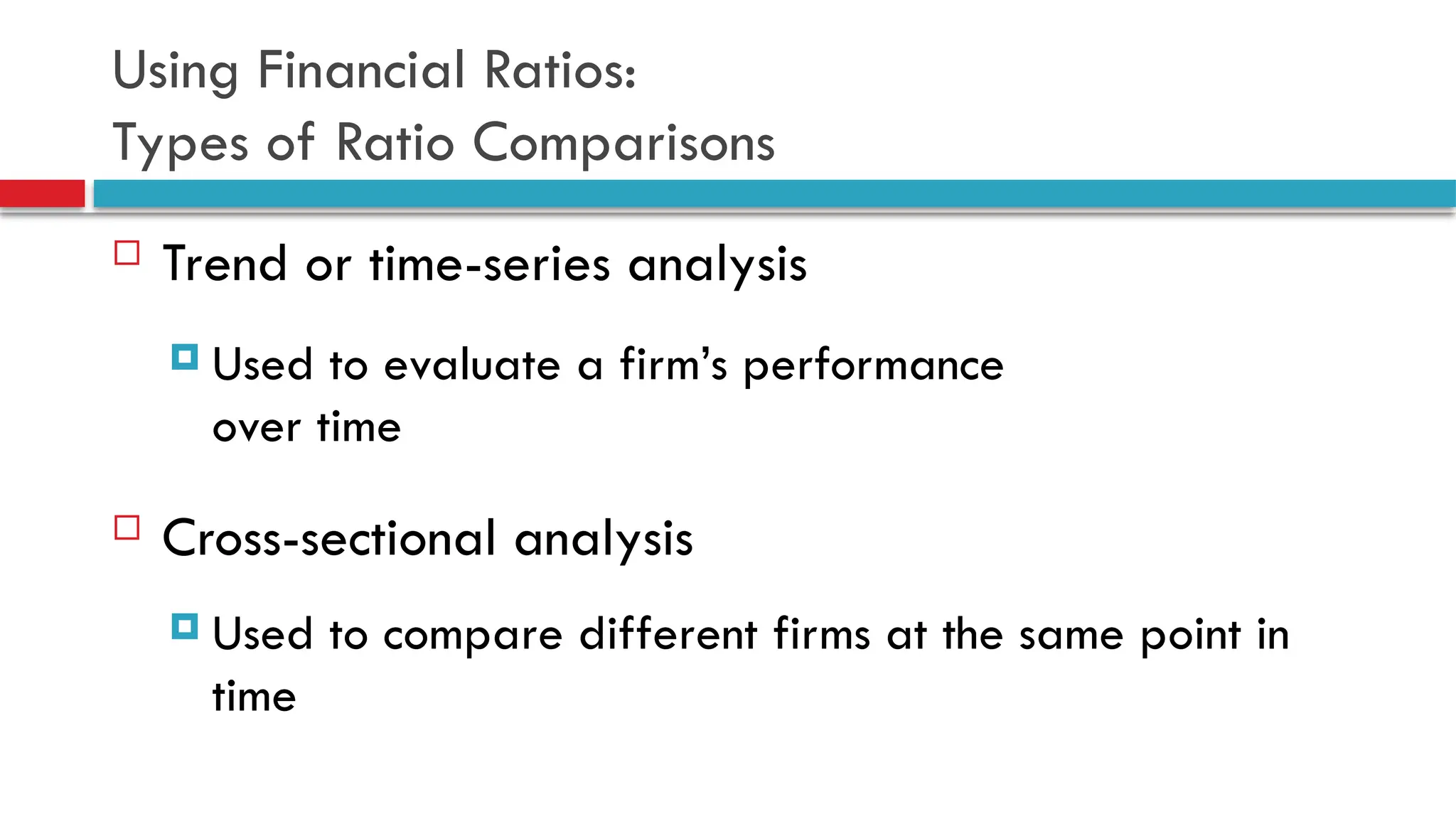

Using Financial Ratios:

Typesof Ratio Comparisons

Trend or time-series analysis

Used to evaluate a firm’s performance

over time

Cross-sectional analysis

Used to compare different firms at the same point in

time

15.

Using Financial Ratios:

Typesof Ratio Comparisons (cont.)

Cross-sectional analysis

Industry comparative analysis

One specific type of cross sectional analysis. Used to compare one

firm’s financial performance to the industry’s average performance

Benchmarking

A type of cross sectional analysis in which the firm’s ratio values are

compared to those of a key competitor or group of competitors that it

wishes to emulate

16.

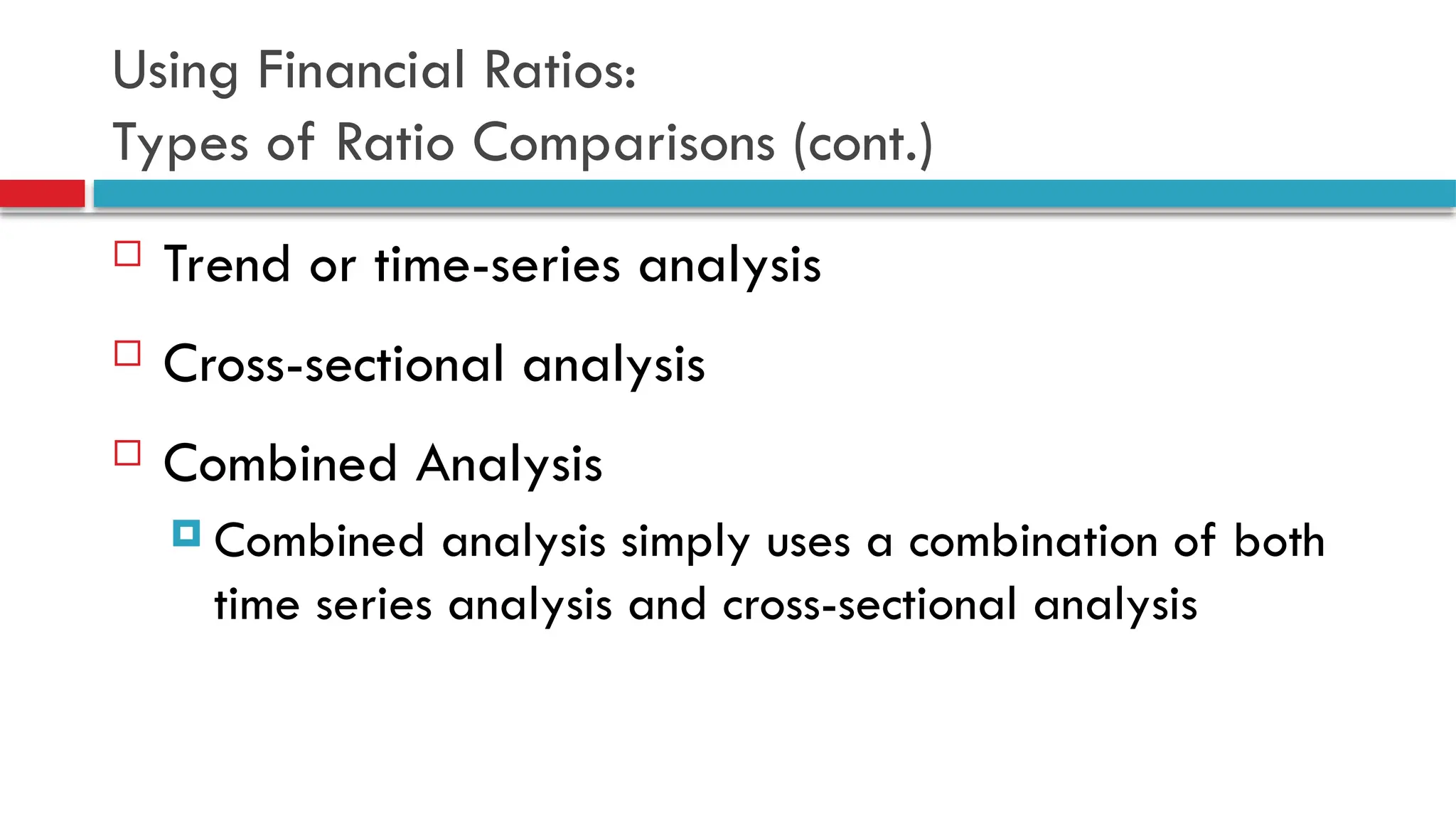

Using Financial Ratios:

Typesof Ratio Comparisons (cont.)

Trend or time-series analysis

Cross-sectional analysis

Combined Analysis

Combined analysis simply uses a combination of both

time series analysis and cross-sectional analysis

17.

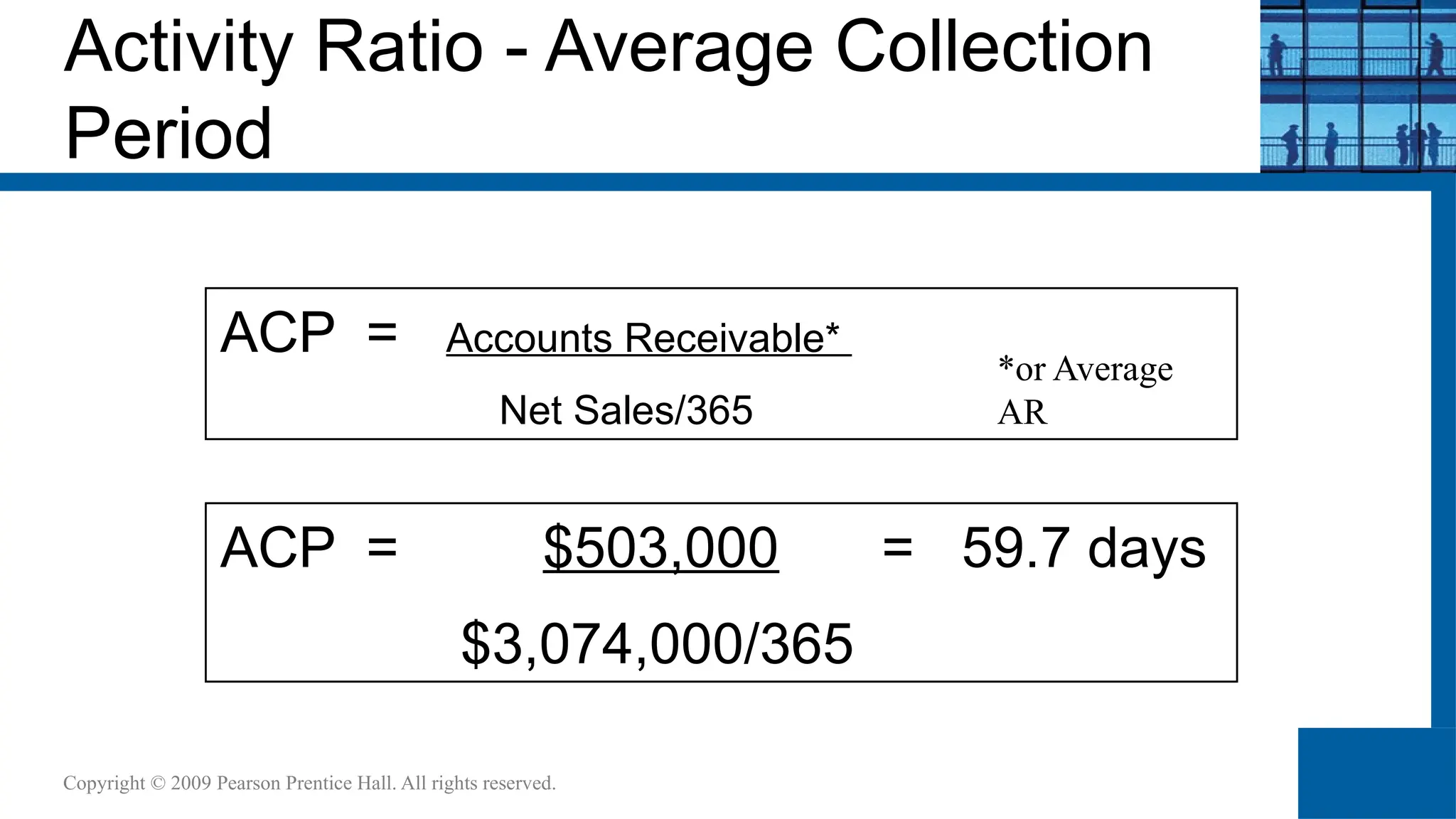

Ratio Analysis

LiquidityRatios – measures capacity to meet short term

obligation

Activity Ratios – measures effective use of resources

Leverage (gearing) Ratios – measures indebtedness

Profitability Ratios – measures overall profitability

Market Ratios – measures based on market price of shares -

important to investors

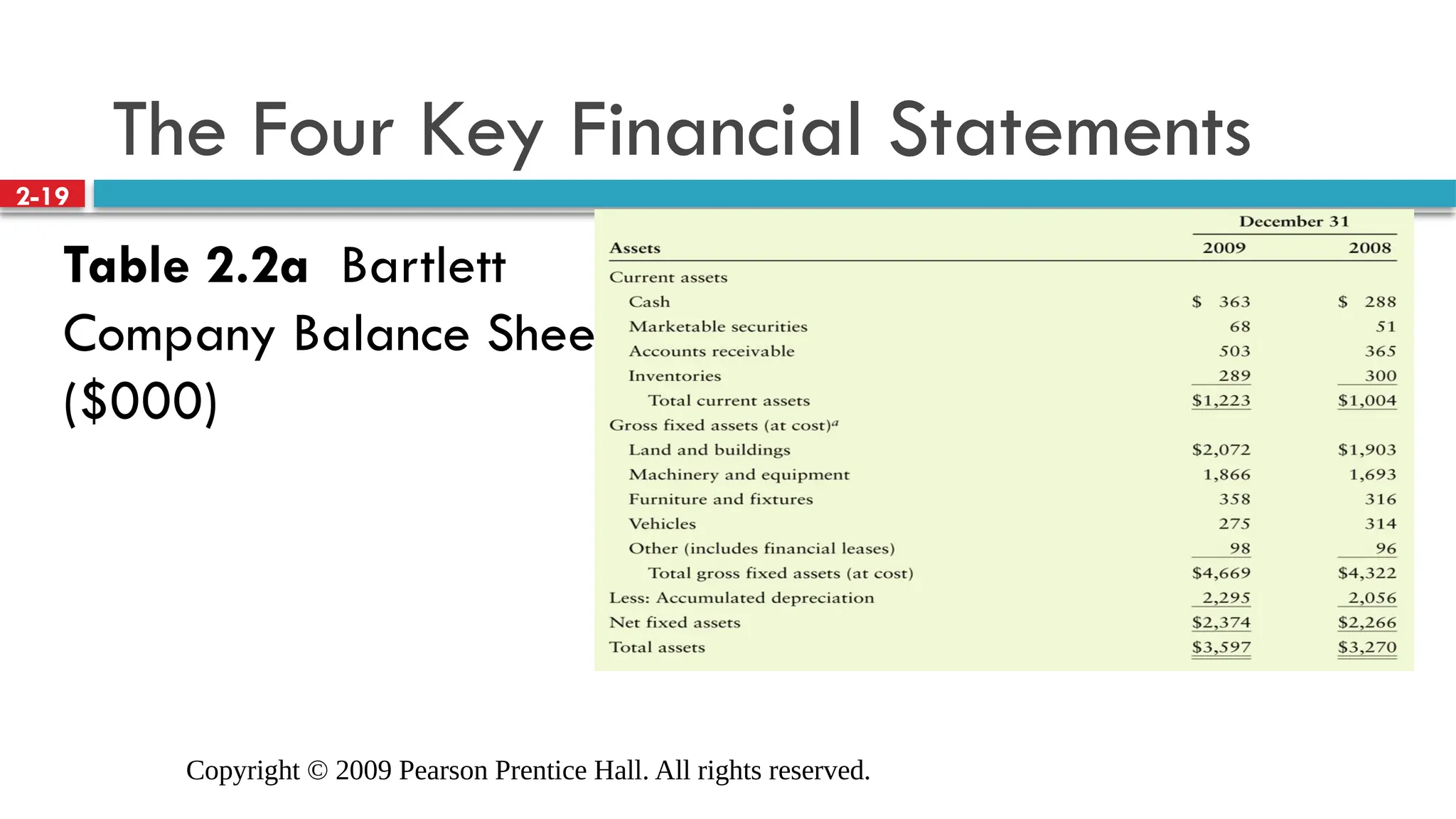

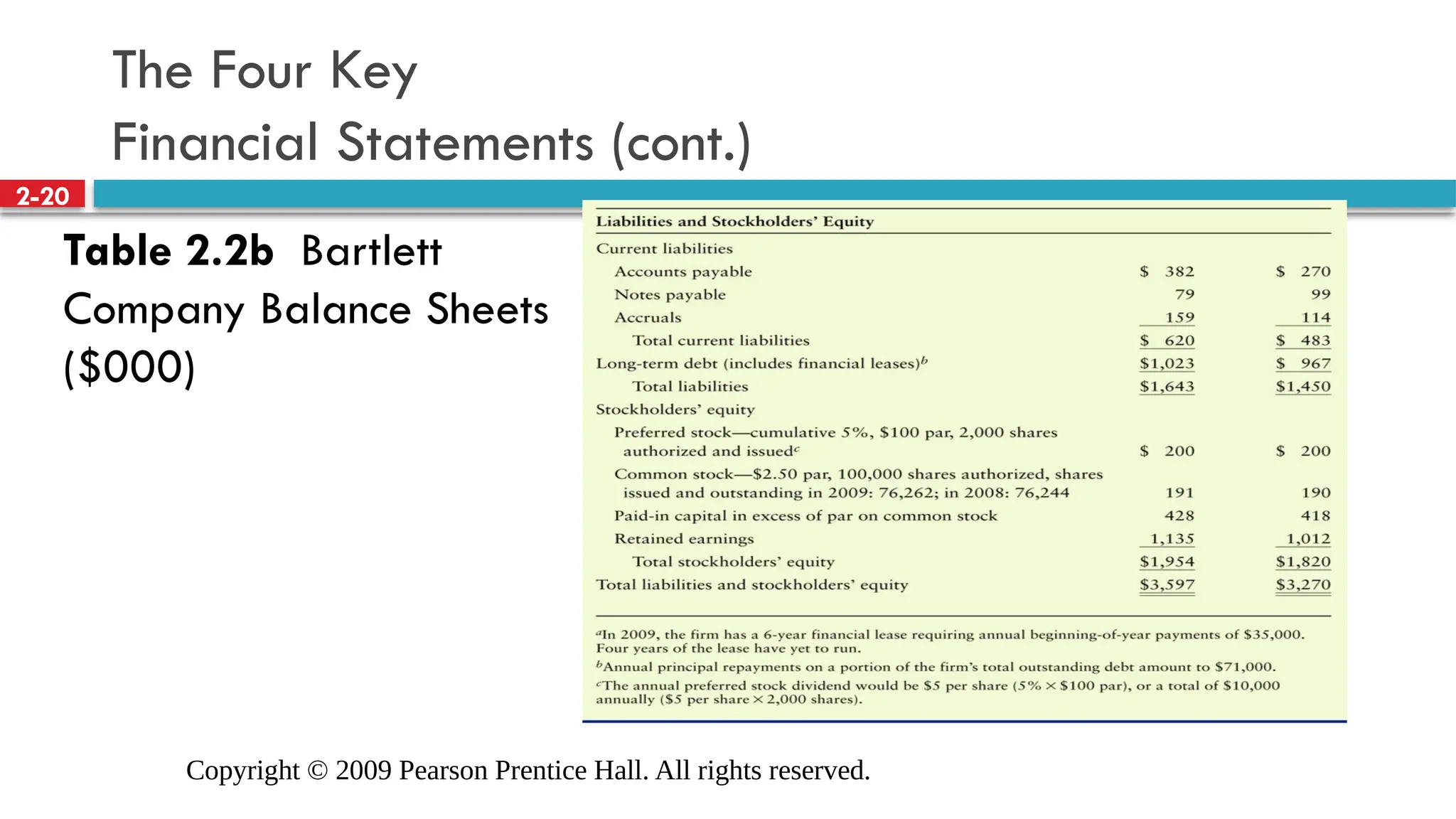

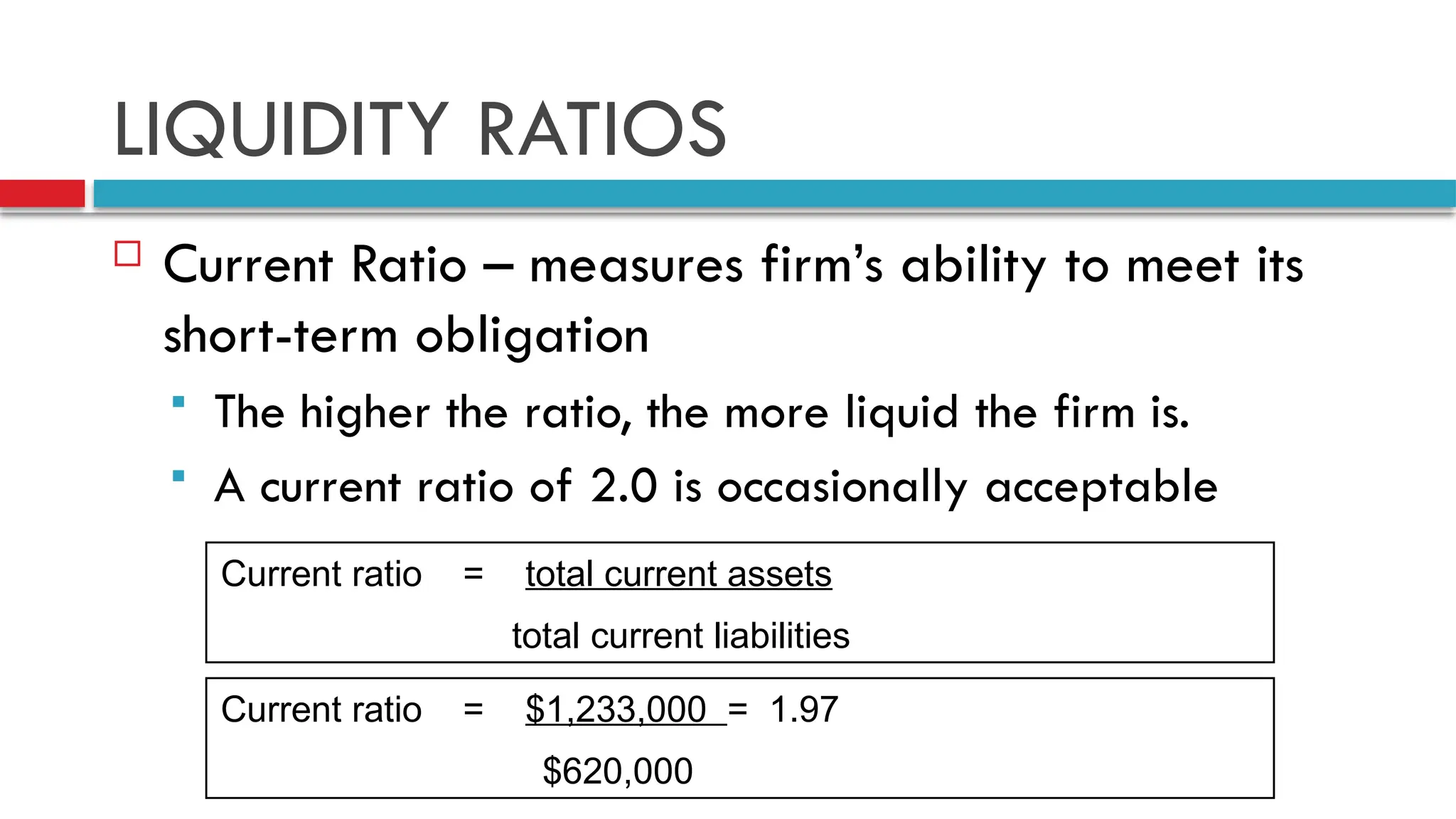

LIQUIDITY RATIOS

CurrentRatio – measures firm’s ability to meet its

short-term obligation

The higher the ratio, the more liquid the firm is.

A current ratio of 2.0 is occasionally acceptable

Current ratio = total current assets

total current liabilities

Current ratio = $1,233,000 = 1.97

$620,000

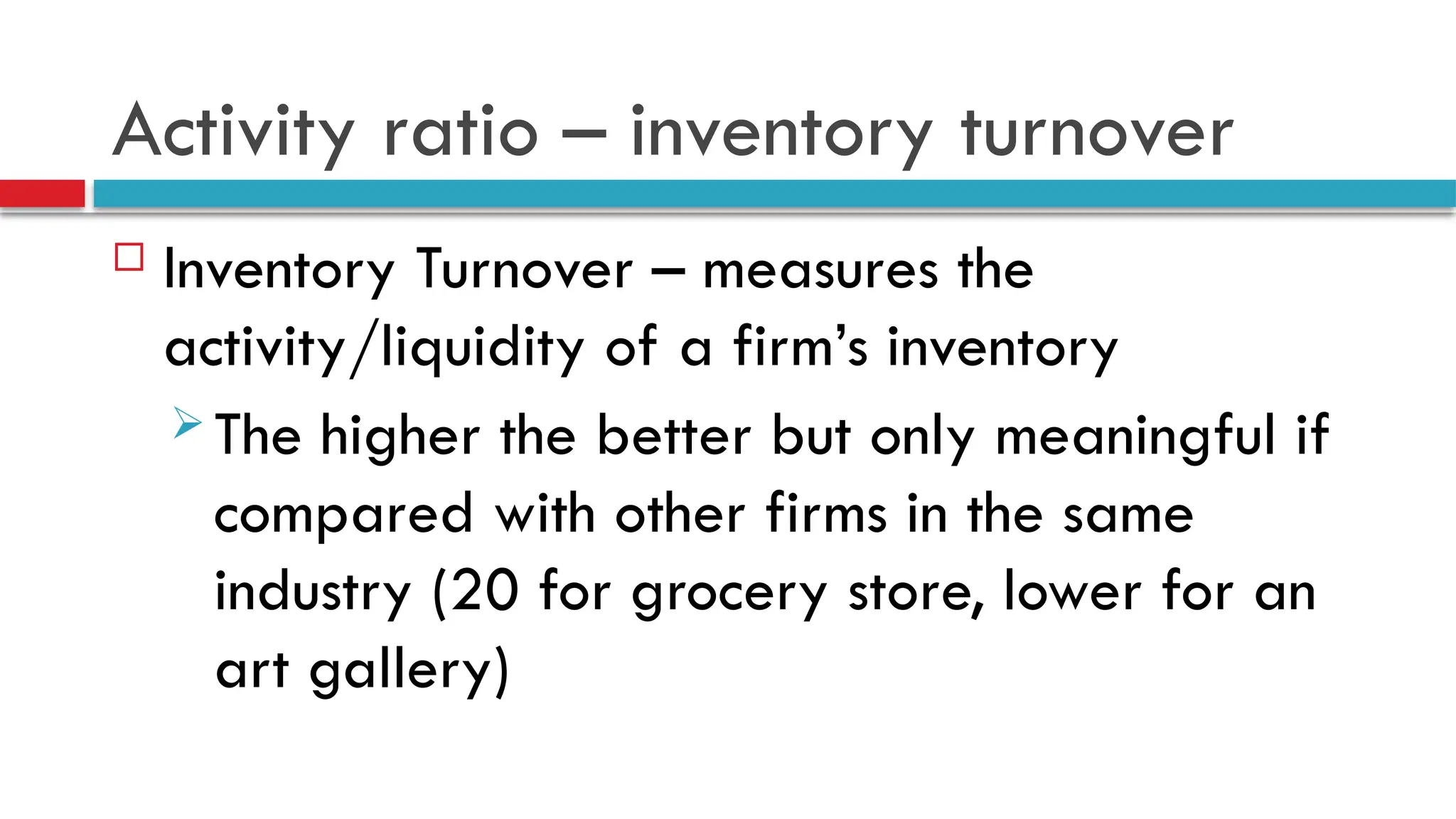

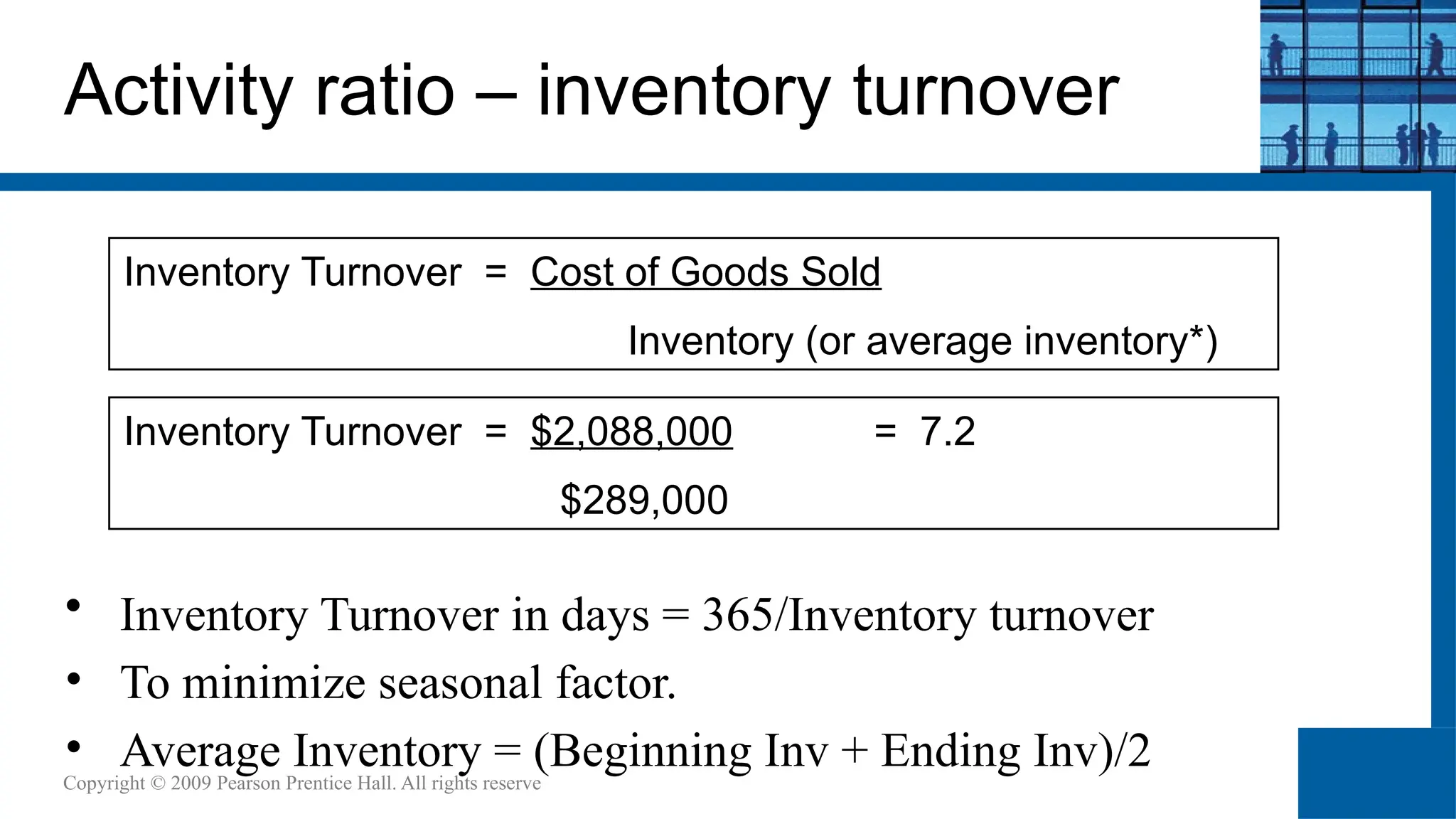

Activity ratio –inventory turnover

Inventory Turnover – measures the

activity/liquidity of a firm’s inventory

The higher the better but only meaningful if

compared with other firms in the same

industry (20 for grocery store, lower for an

art gallery)

Leverage Ratio -Debt Ratio

Debt Ratio (Financial leverage ratio) – measures the

proportion of total assets financed by the firm’s creditors

The higher this ratio, the greater the firms’ degree of

indebtedness, the more financial leverage it has

Debt Ratio = Total Liabilities/Total Assets

Debt Ratio = $1,643,000/$3,597,000 = 45.7%

35.

Debt Ratio –Times Interest Earned Ratio

Times Interest Earned Ratio (interest coverage) – measures

the firms’ ability to make contractual interest payments

The higher the better – a value of at least 3.0 and

preferably closer to 5.0 is often suggested

Times Interest Earned = EBIT (Operating Income)/Interest

Times Interest Earned = $418,000/$93,000 = 4.5

36.

Debt ratio -Fixed-Payment Coverage

Fixed-Payment Coverage Ratio – measures the firms’

ability to meet all fixed-payment obligations (loan

interest and principal, lease payments, preferred stock

dividend)

The higher, the better. Also measures risk, the lower the

ratio, the greater the risk to both lenders and owners

Debt-equity ratio

Measuresthe relationship between the firm’s resources

provided through debt and those provided through

ownership (equity)

The greater the D/E ratio is, the riskier the company is

as an investment

Formula = Total Liabilities

Total stockholders’ equity

39.

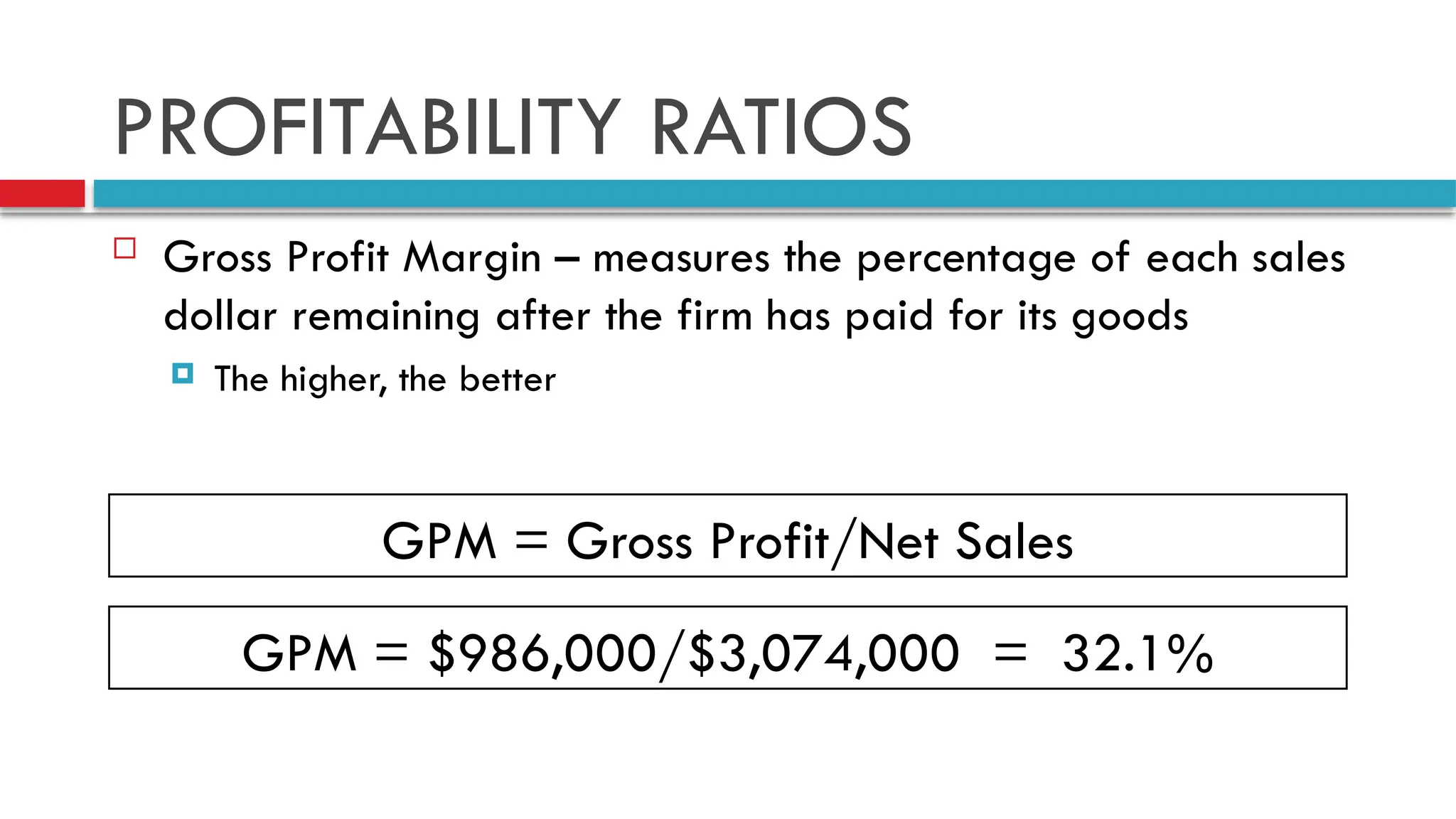

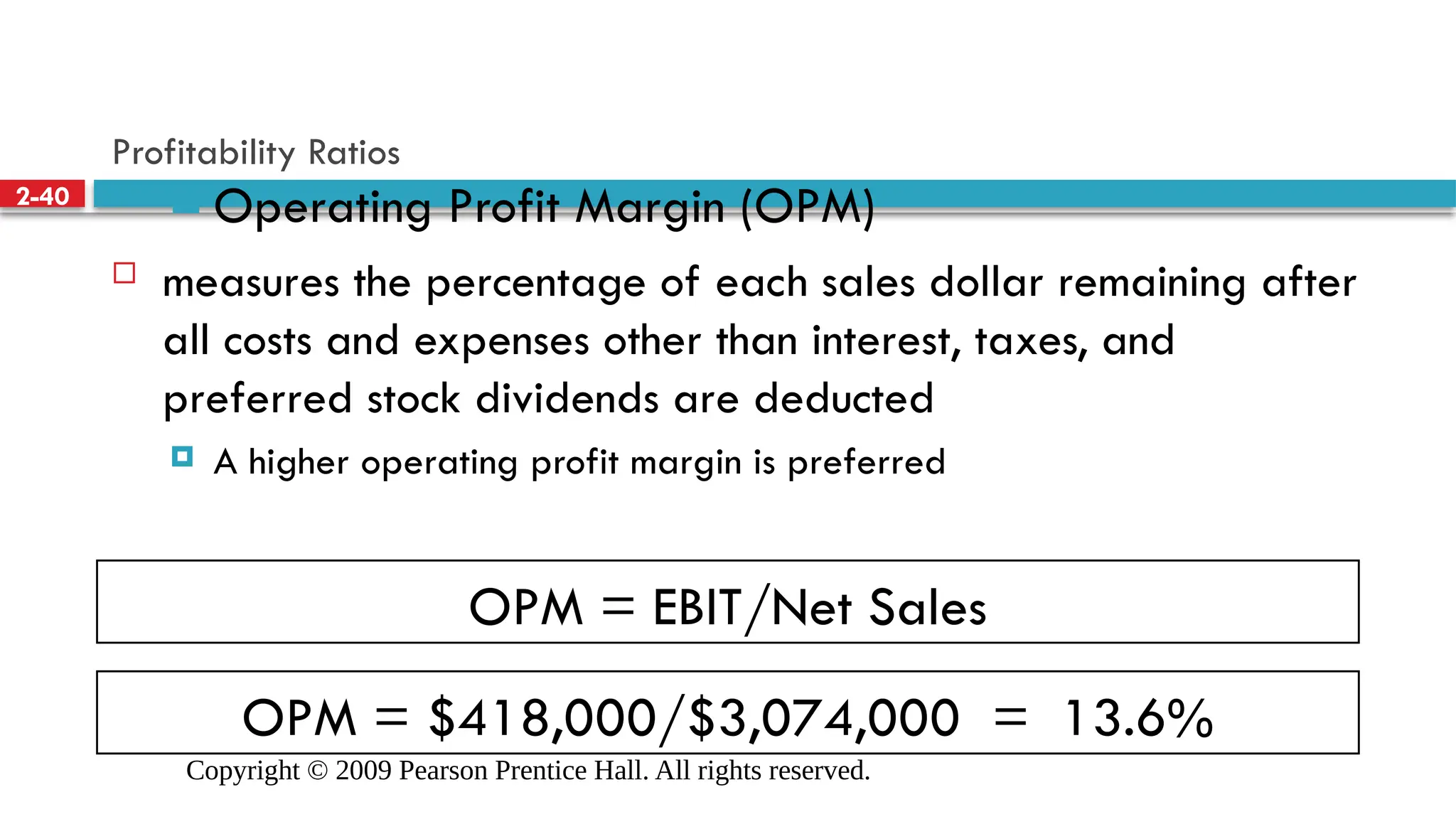

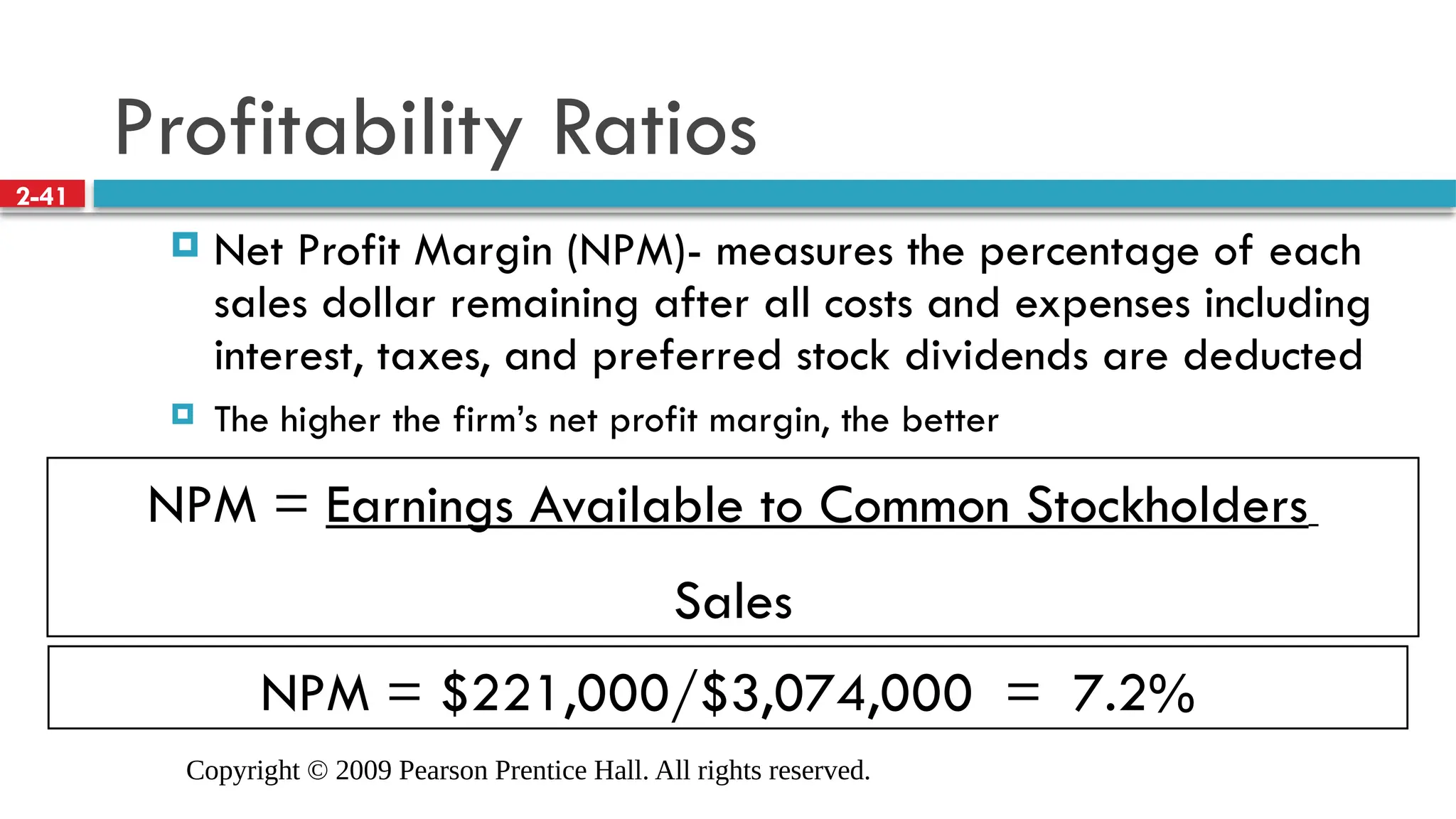

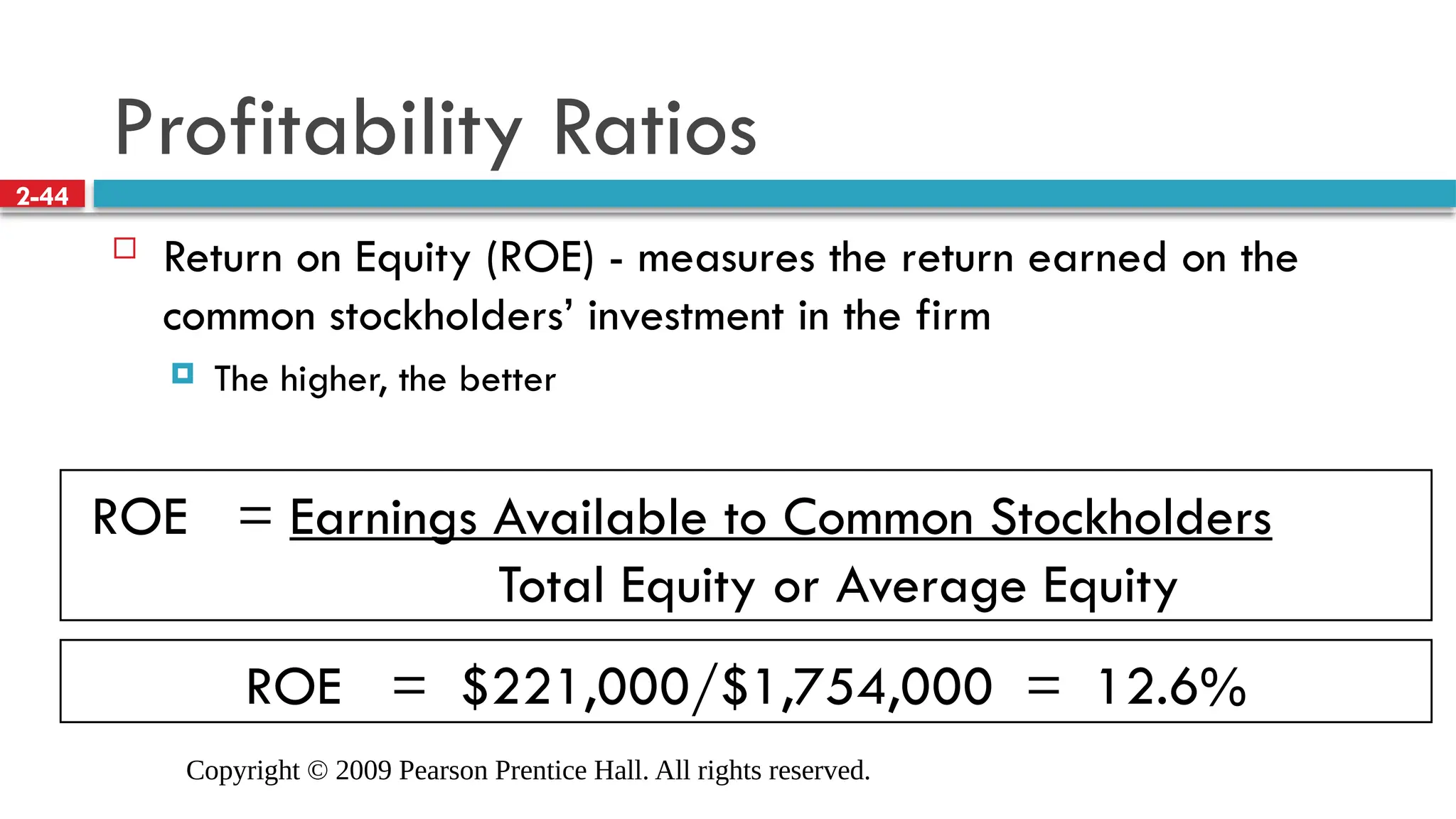

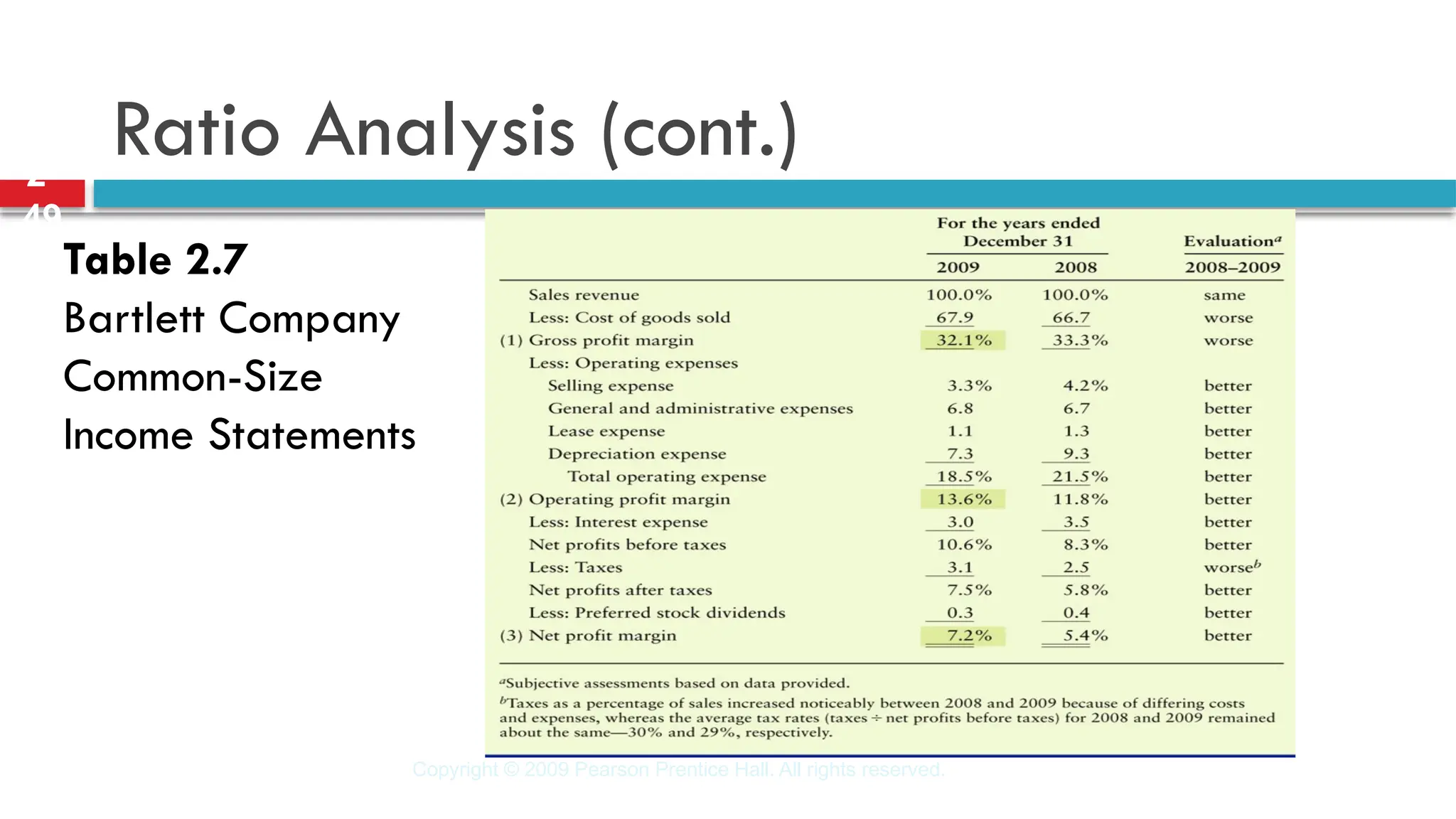

PROFITABILITY RATIOS

GrossProfit Margin – measures the percentage of each sales

dollar remaining after the firm has paid for its goods

The higher, the better

GPM = Gross Profit/Net Sales

GPM = $986,000/$3,074,000 = 32.1%

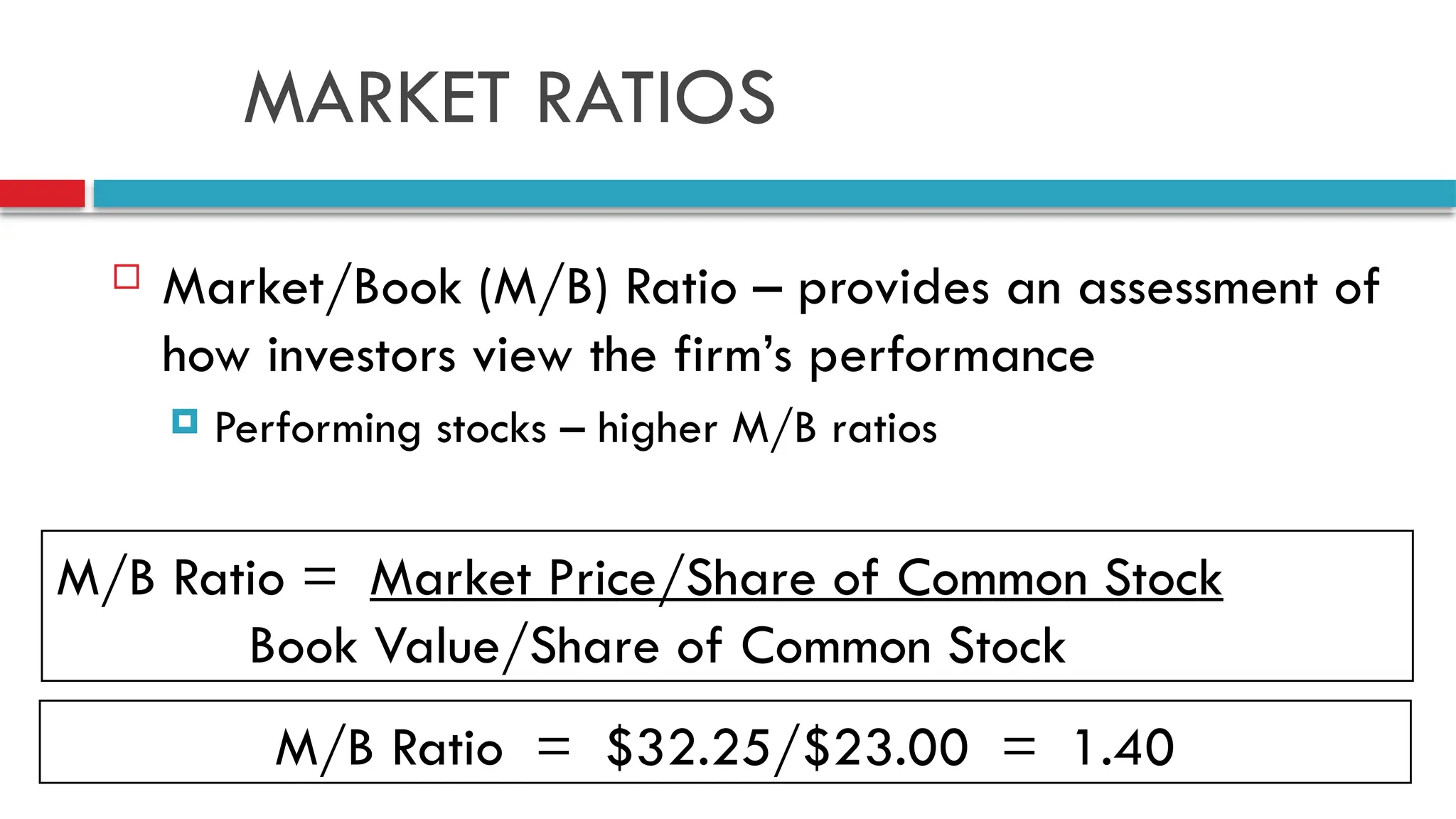

MARKET RATIOS

Market/Book(M/B) Ratio – provides an assessment of

how investors view the firm’s performance

Performing stocks – higher M/B ratios

M/B Ratio = Market Price/Share of Common Stock

Book Value/Share of Common Stock

M/B Ratio = $32.25/$23.00 = 1.40

47.

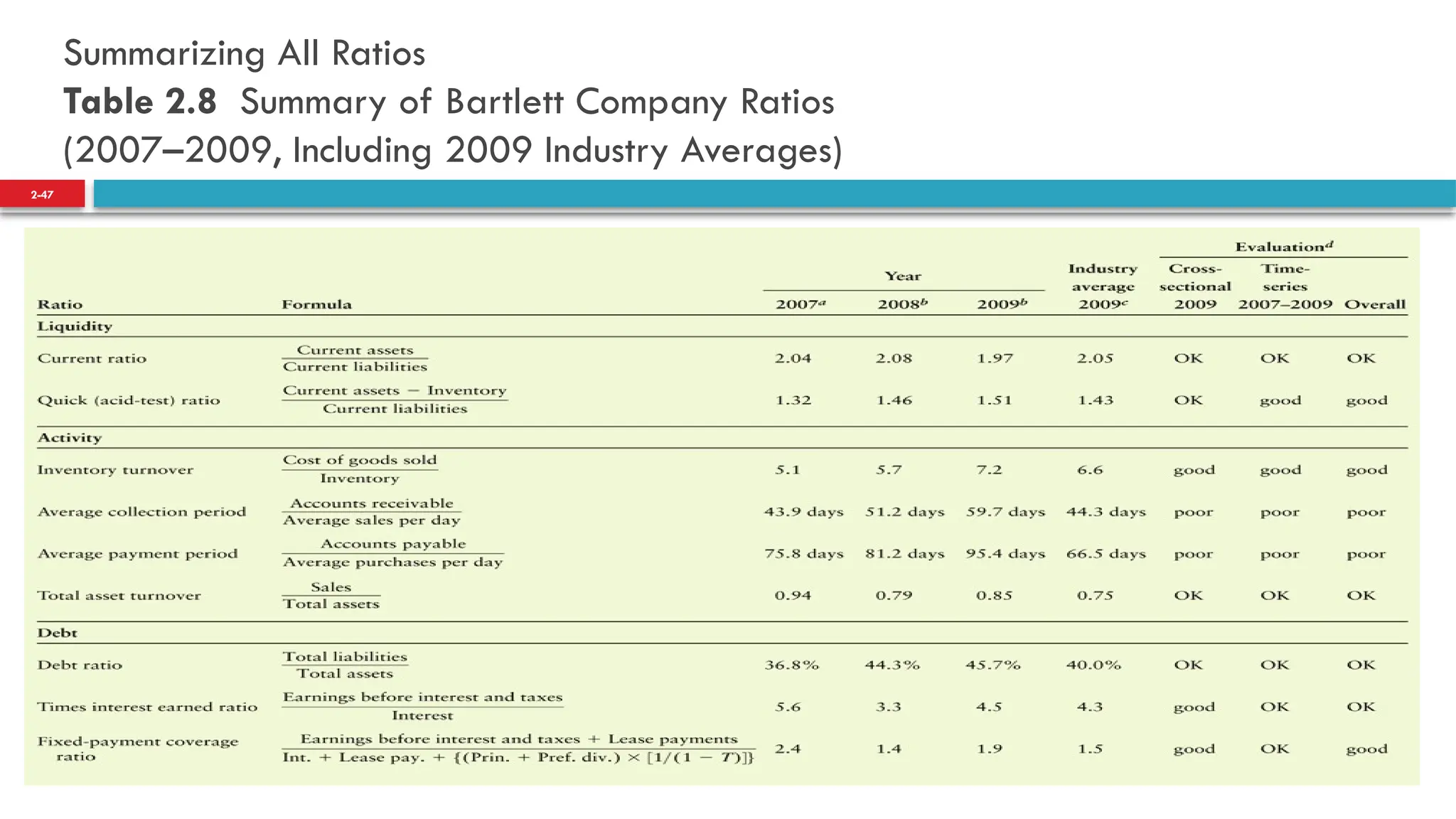

Summarizing All Ratios

Table2.8 Summary of Bartlett Company Ratios

(2007–2009, Including 2009 Industry Averages)

2-47

48.

Summarizing All Ratios(cont.)

Table 2.8 Summary of Bartlett Company Ratios

(2007–2009, Including 2009 Industry Averages)

2-48

![Copyright © 2009 Pearson Prentice Hall. All rights reserved.

2-37

FPCR = EBIT + Lease Payments________________

Interest + Lease Pymts + {(Princ Pymts + PSD) x [1/(1-t)]}

FPCR = $418,000 + $35,000 = 1.9

$93,000 + $35,000 + {($71,000 + $10,000) x [1/(1-.29)]}

Debt Ratio

Fixed-Payment coverage Ratio (FPCR)](https://image.slidesharecdn.com/fsa-250420080857-dcadd451/75/Financial-Statement-Analysis-Annual-Report-Analysis-37-2048.jpg)