Downloaded 15 times

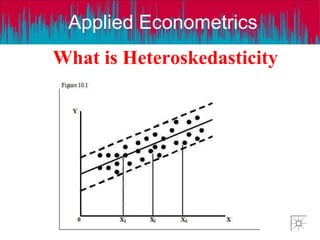

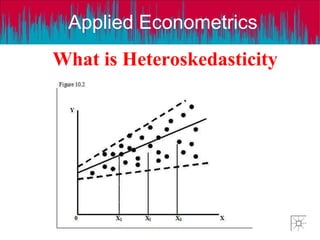

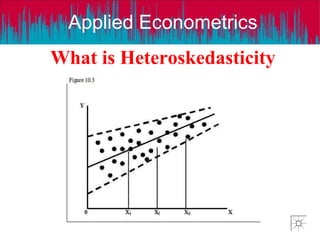

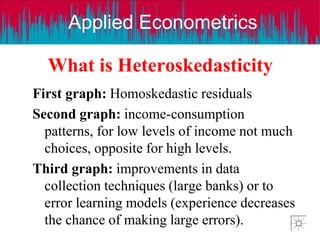

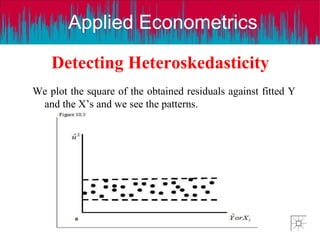

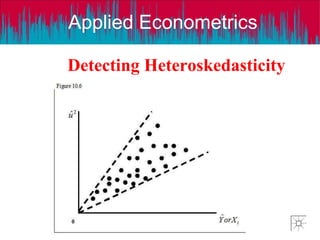

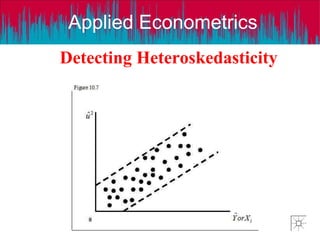

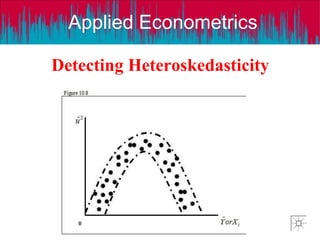

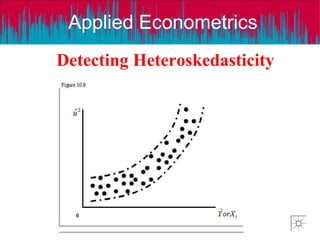

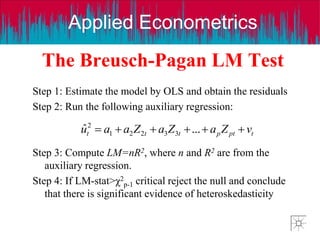

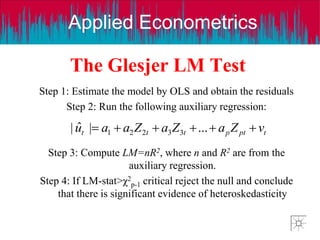

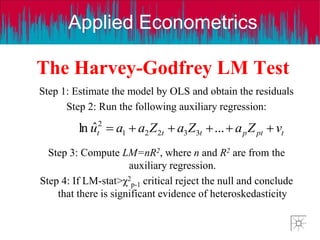

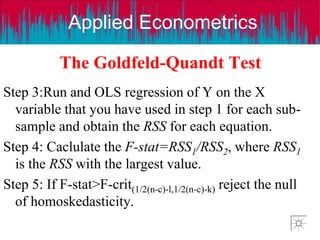

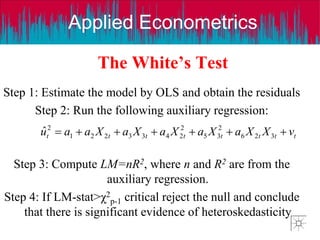

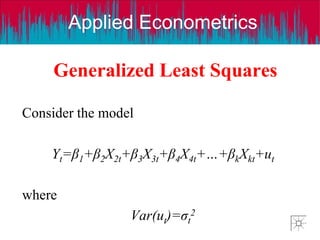

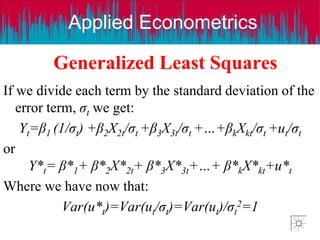

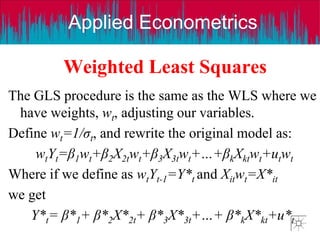

The document discusses heteroskedasticity in econometrics. It defines heteroskedasticity as unequal variance of error terms compared to homoskedasticity which is equal variance. This violates assumptions of ordinary least squares regression. Heteroskedasticity does not bias estimates but makes them inefficient. The document outlines various tests to detect heteroskedasticity including graphical methods and formal tests. It also discusses methods to resolve heteroskedasticity such as generalized least squares, weighted least squares, and heteroskedasticity-consistent standard errors.

![[DSC Europe 25] Andrzej Kowalczyk - AI - how to start small and grow in the f...](https://cdn.slidesharecdn.com/ss_thumbnails/oy1zmo94qv6vpcqjvno2-andrzej-kowalczyk-ai-how-to-start-small-and-grow-in-the-future-1-260119121559-cf093b23-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Bojan Djuricic - Predictive Design Process.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/5awdrbedqdek3gqu2ezy-4-the-predictive-design-bojan-djuricic-260120105856-6c399e9b-thumbnail.jpg?width=640&height=640&fit=bounds)