Downloaded 142 times

![106

4.4.5. RETURN ON EQUITY (ROE) RATIO:

In real sense, ordinarily shareholders are the real owners of the company. They assume the

highest risk in the company. (Preference share holders have a preference over ordinary

shareholders in the payment of dividend as well as capital. Preference share holders get a fixed

rate of dividend irrespective of the quantum of profits of the company). The rate of dividends

varies with the availability of profits in case of ordinary shares only. Thus ordinary shareholders

are more interested in the profitability of a company and the performance of a company should

be judged on the basis of return on equity capital of the company. Return on equity capital which

is the relationship between profits of a company and its equity, can be calculated as follows.

COMPONENTS:

Equity share capital should be the total called-up value of equity shares. As the profit used for

the calculations are the final profits available to equity shareholders as dividend, therefore the

preference dividend and taxes are deducted in order to arrive at such profits.

SIGNIFICANCE:

This ratio is more meaningful to the equity shareholders who are interested to know profits

earned by the company and those profits which can be made available to pay dividends to them.

Interpretation of the ratio is similar to the interpretation of return on shareholder's investments

and higher the ratio better is.

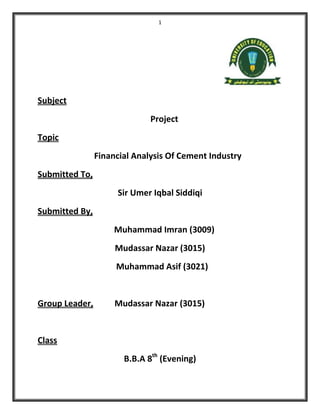

RETURN ON EQUITY RATIO (ROE)

Formula

[(Net profit after tax − Preference dividend) / Equity share capital] ×

100

Years 2015 2014 2013 2012 2011

Pioneer Cement -7.80% -4.46% 29.11% 20.48% 77.81%

Cherat Cement 1.08% 29.77% 54.70% 77.04% 80.08%

Kohat Cement -9.55% 2.09% 34.58% 35.73% 42.09%](https://image.slidesharecdn.com/originalfinalprojectreortoncementindustry-180528110354/85/Final-project-Report-on-cement-industry-106-320.jpg)

![110

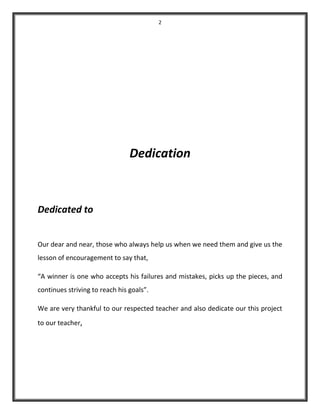

4.4.7. DEBT SERVICE RATIO OR INTEREST COVERAGE RATIO:

Interest coverage ratio is also known as debt service ratio or debt service coverage ratio. This

ratio relates the fixed interest charges to the income earned by the business. It indicates whether

the business has earned sufficient profits to pay periodically the interest charges.

SIGNIFICANCE OF DEBT SERVICE RATIO:The interest coverage ratio is very important from the

lender's point of view. It indicates the number of times interest is covered by the profits available to pay

interest charges.

Formula Net Profit Before Interest and Tax / Fixed Interest Charges]

Years 2015 2014 2013 2012 2011

Pioneer cement 0.39 0.31 5.73 4.26 3.03

Cherat 0.30 4.27 9.94 21.10 30.96

Kohat Cement -4.71 1.23 20.21 25.17 17.22

INTEREST COVERAGE RATIO](https://image.slidesharecdn.com/originalfinalprojectreortoncementindustry-180528110354/85/Final-project-Report-on-cement-industry-110-320.jpg)

This document provides a history of the cement industry in Pakistan from independence in 1947 through recent years. It discusses key developments and ownership changes in the industry during different eras, including nationalization under Bhutto, de-nationalization under Zia-ul-Haq, and privatization under Nawaz Sharif. The cement industry grew significantly from its origins of 4 plants with 0.5 million tons of capacity to over 24 plants with capacity over 8.5 million tons by 1990 through expansions in both the public and private sectors over several decades.