The document discusses Current Expected Credit Loss (CECL) modeling introduced by the FASB in ASU No. 2016-13, which aims for timely recognition of credit losses by measuring expected losses based on historical data and forecasts. It highlights the need for adjustments in existing credit risk models to meet CECL requirements, as well as the importance of defining a reasonable and supportable (R&S) period to accurately reflect expected credit losses. The presentation emphasizes that CECL does not prescribe specific methodologies for expected credit loss estimates, allowing the use of common modeling approaches while requiring proper adjustments for compliance.

Current Expected CreditLoss (CECL)

Modeling

May 17th 2018

Xiaoling (Sean) Yu

SVP, Director of Model Validation

KeyBank

7th Annual Risk Americas 2018

2.

2

Disclaimer

7th Annual RiskAmericas 2018

The views expressed in this presentation are those of the

speaker and do not necessarily reflect the views of

KeyCorp or its subsidiaries in all respects.

3.

3

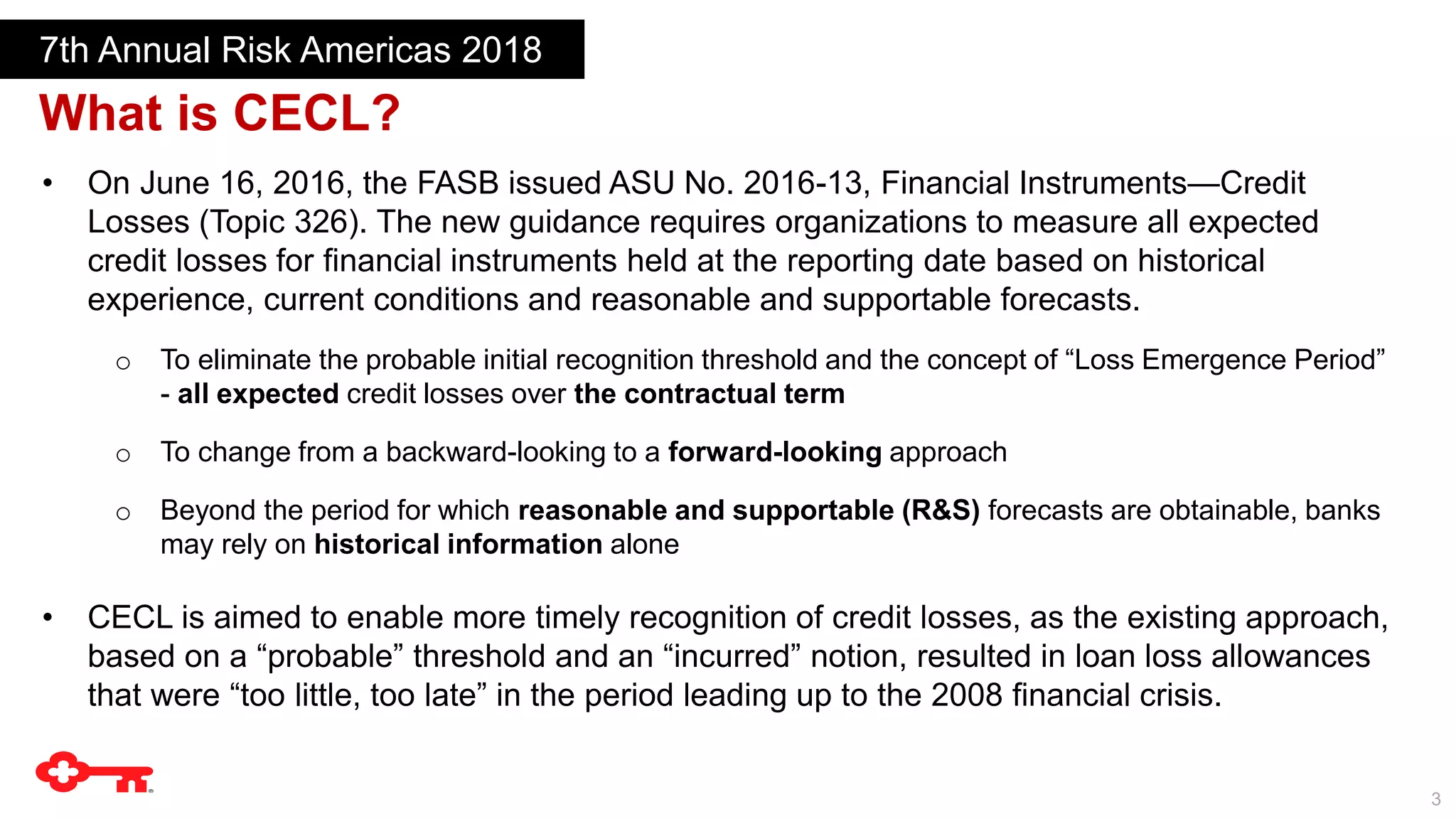

What is CECL?

7thAnnual Risk Americas 2018

• On June 16, 2016, the FASB issued ASU No. 2016-13, Financial Instruments—Credit

Losses (Topic 326). The new guidance requires organizations to measure all expected

credit losses for financial instruments held at the reporting date based on historical

experience, current conditions and reasonable and supportable forecasts.

o To eliminate the probable initial recognition threshold and the concept of “Loss Emergence Period”

- all expected credit losses over the contractual term

o To change from a backward-looking to a forward-looking approach

o Beyond the period for which reasonable and supportable (R&S) forecasts are obtainable, banks

may rely on historical information alone

• CECL is aimed to enable more timely recognition of credit losses, as the existing approach,

based on a “probable” threshold and an “incurred” notion, resulted in loan loss allowances

that were “too little, too late” in the period leading up to the 2008 financial crisis.

4.

4

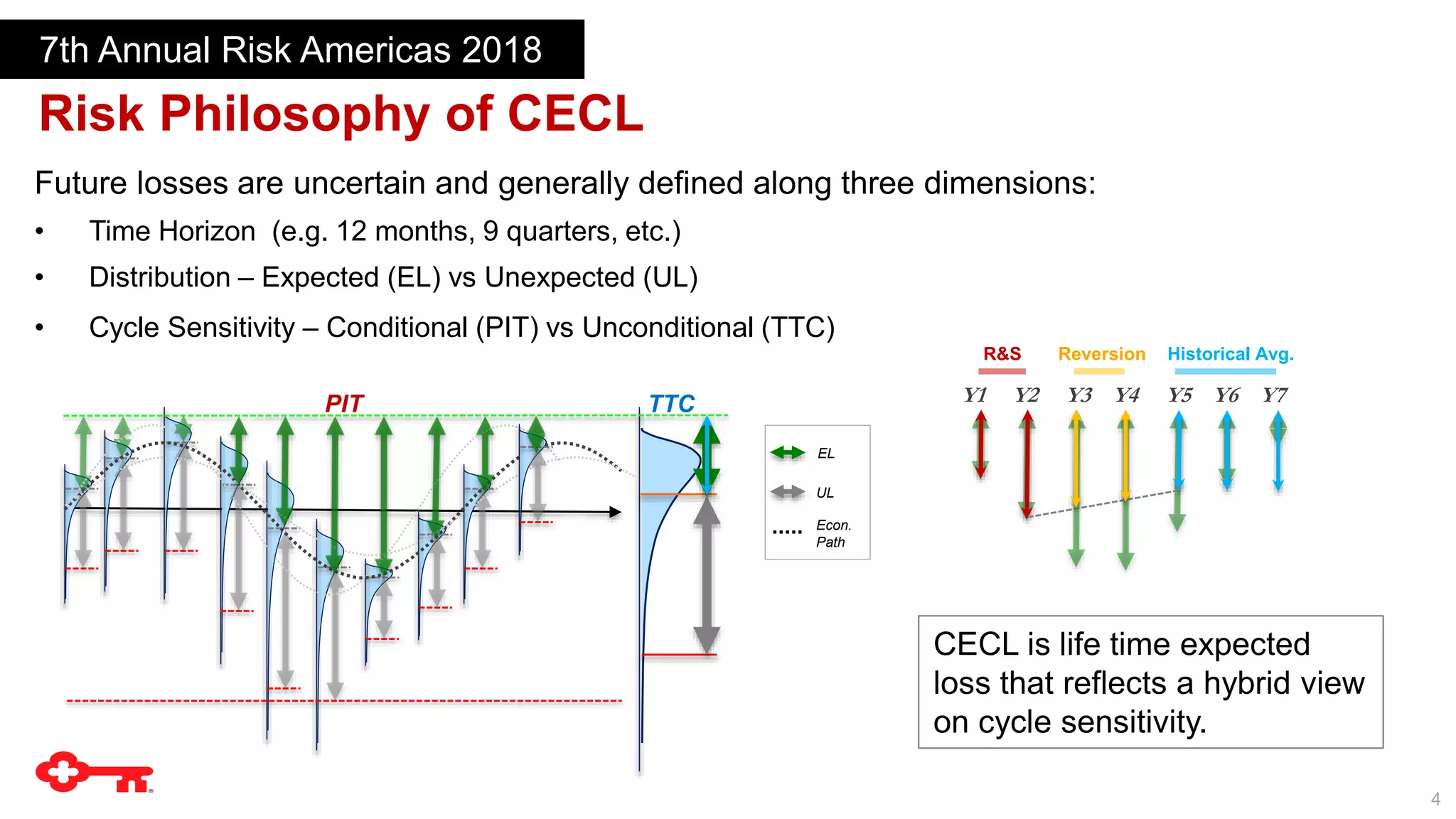

Risk Philosophy ofCECL

7th Annual Risk Americas 2018

Future losses are uncertain and generally defined along three dimensions:

• Time Horizon (e.g. 12 months, 9 quarters, etc.)

• Distribution – Expected (EL) vs Unexpected (UL)

• Cycle Sensitivity – Conditional (PIT) vs Unconditional (TTC)

PIT TTC

EL

UL

Econ.

Path

R&S

CECL is life time expected

loss that reflects a hybrid view

on cycle sensitivity.

Y1 Y2 Y3 Y4 Y5 Y6 Y7

Reversion Historical Avg.

5.

5

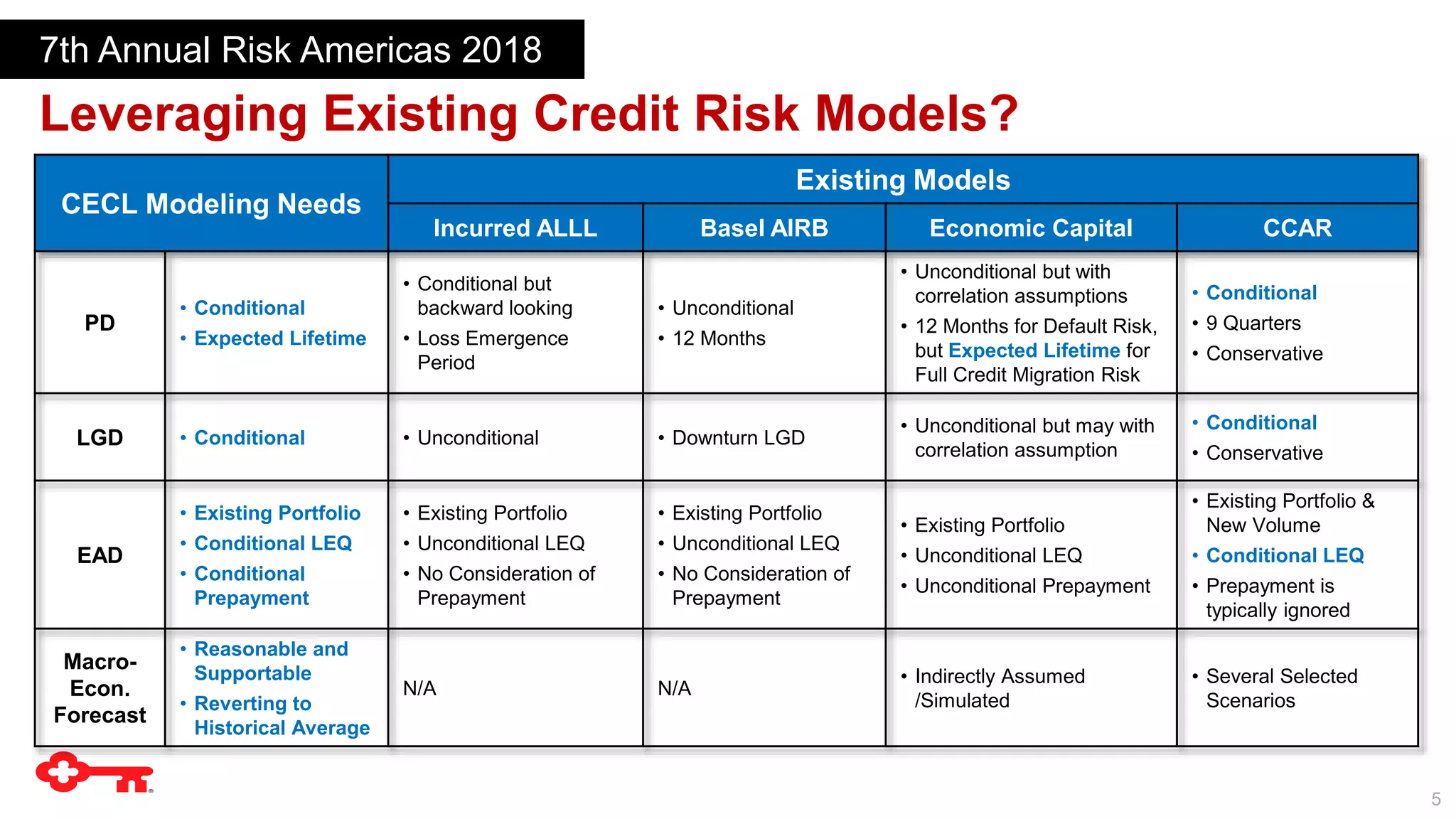

Leveraging Existing CreditRisk Models?

7th Annual Risk Americas 2018

CECL Modeling Needs

Existing Models

Incurred ALLL Basel AIRB Economic Capital CCAR

PD

• Conditional

• Expected Lifetime

• Conditional but

backward looking

• Loss Emergence

Period

• Unconditional

• 12 Months

• Unconditional but with

correlation assumptions

• 12 Months for Default Risk,

but Expected Lifetime for

Full Credit Migration Risk

• Conditional

• 9 Quarters

• Conservative

LGD • Conditional • Unconditional • Downturn LGD

• Unconditional but may with

correlation assumption

• Conditional

• Conservative

EAD

• Existing Portfolio

• Conditional LEQ

• Conditional

Prepayment

• Existing Portfolio

• Unconditional LEQ

• No Consideration of

Prepayment

• Existing Portfolio

• Unconditional LEQ

• No Consideration of

Prepayment

• Existing Portfolio

• Unconditional LEQ

• Unconditional Prepayment

• Existing Portfolio &

New Volume

• Conditional LEQ

• Prepayment is

typically ignored

Macro-

Econ.

Forecast

• Reasonable and

Supportable

• Reverting to

Historical Average

N/A N/A

• Indirectly Assumed

/Simulated

• Several Selected

Scenarios

6.

6

Reasonable and Supportable(R&S) Period?

7th Annual Risk Americas 2018

Para 326-20-30-9:

• “When an entity uses historical loss information, it shall consider the need to adjust historical

information to reflect the extent to which management expects current conditions and reasonable and

supportable forecasts to differ from the conditions that existed for the period over which historical

information was evaluated.”

• “An entity shall not adjust historical loss information for existing economic conditions or expectations of

future economic conditions for periods that are beyond the reasonable and supportable period.”

Quantitative Interpretation:

• The R&S Period may be defined by the acceptable level of model error. For instance, R&S period can

be determined when further extending it will not lead to material change in the level of forecast error.

• R&S Period could be product/asset specific, and/or cycle specific.

• The model error consists of two components: the error in macroeconomic forecast and the error in loss

forecast conditional on given macroeconomic variables.

• Economists do not have a good track record in forecasting recessions, and the range of forecast

variances can be large.

7.

7

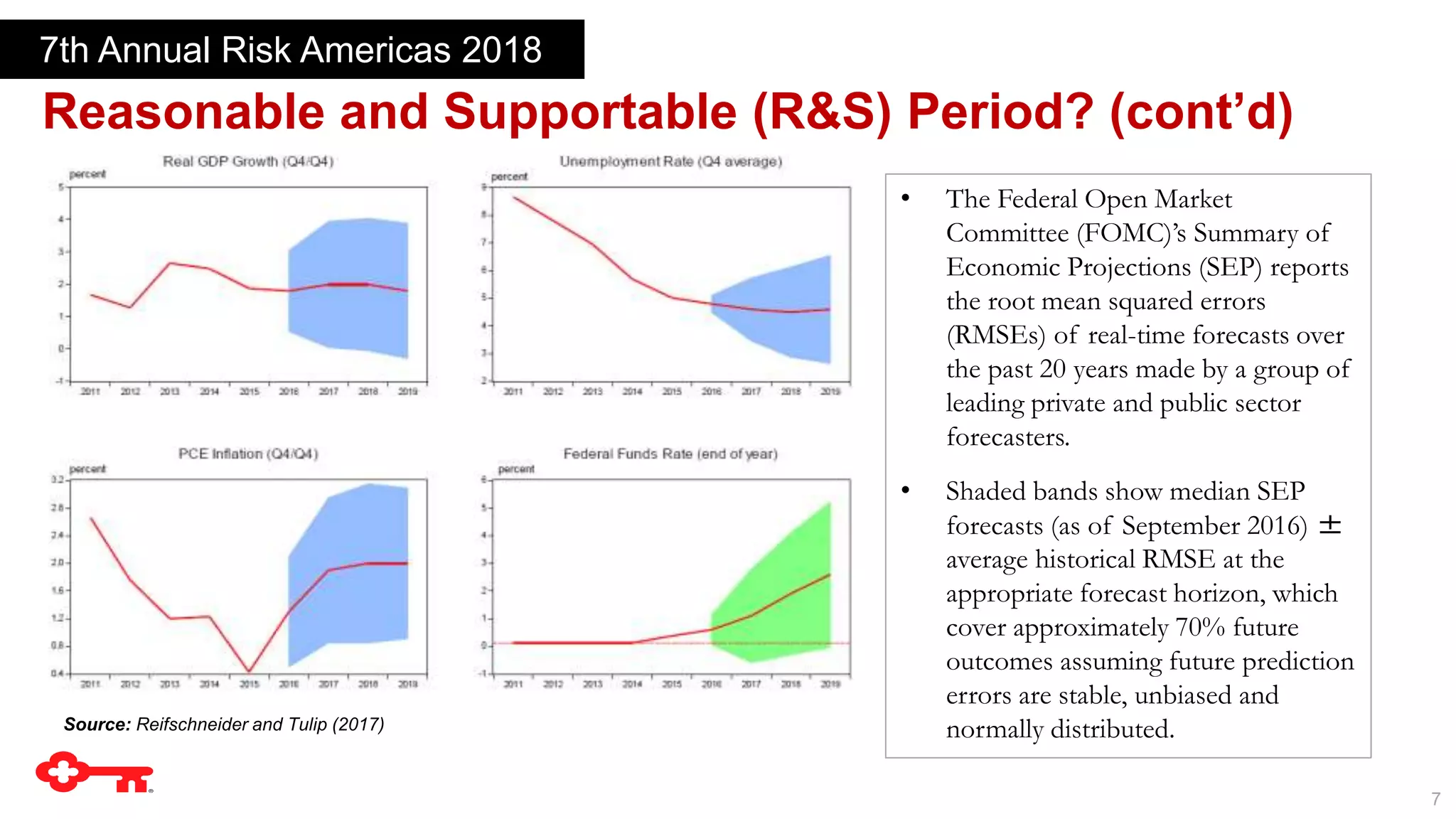

Reasonable and Supportable(R&S) Period? (cont’d)

7th Annual Risk Americas 2018

• The Federal Open Market

Committee (FOMC)’s Summary of

Economic Projections (SEP) reports

the root mean squared errors

(RMSEs) of real-time forecasts over

the past 20 years made by a group of

leading private and public sector

forecasters.

• Shaded bands show median SEP

forecasts (as of September 2016) ±

average historical RMSE at the

appropriate forecast horizon, which

cover approximately 70% future

outcomes assuming future prediction

errors are stable, unbiased and

normally distributed.Source: Reifschneider and Tulip (2017)

8.

8

Reasonable and Supportable(R&S) Period? (cont’d)

7th Annual Risk Americas 2018

Qualitative Interpretation:

• R&S period is more of a process and governance concept instead of a quantitative concept.

• It has to be consistent with the time horizons of other internal processes, e.g. strategic planning.

• R&S period has to be long enough to capture the near future loss, especially when entering into a

recession.

Current Practices:

• Majority of the institutions are considering 2-3 years of R&S period, while others may select either one

year or 5-6 years.

• Majority of the institutions are considering to apply the same R&S period across asset classes.

Conclusion:

• R&S period cannot be a pure quantitative or qualitative concept.

• R&S period has to be consistent with the time horizons of other processes across the organization.

• The rationale and process followed in determining R&S period should be clearly documented, with

transparent discussion on its quantitative implication.

• R&S period has to be periodically reviewed and challenged.

9.

9

Modeling Approach

7th AnnualRisk Americas 2018

• CECL does not require specific approaches when developing the estimate of expected

credit losses.

• Commonly used CCAR modeling approaches, e.g. Hazard Rate model for retail and

Transition Matrix Model for commercial, can be leveraged in principle.

• However, CCAR models tend to produce conservative outcomes, especially under base

scenario. How to design proper adjustment has to be thought through.

• In addition, efforts need to be made to ensure CCAR models are adjusted to meet CECL

requirements.

o ASU requires the estimate to be based on a financial asset’s amortized cost. If only the unpaid

principal balance (UPB) write-offs are considered in loss history, adjustments would need to be

considered for LGD and EAD modeling.

o While prepayments, extensions, renewals, and modifications are typically not well considered in

commercial CCAR modeling, they need to be carefully examined for CECL.

10.

10

Macroeconomic Variable Selection

7thAnnual Risk Americas 2018

CCAR:

• Fed scenarios specifies 16 domestic macroeconomic variables that measure economic activity and

prices, asset prices or financial conditions, and interest rates.

• CCAR models typically leverage many more macroeconomic variables to capture portfolio specific

sensitivities to different regions, markets, asset types, etc.

• Macroeconomic models are used to translate and expand Fed scenarios. For instance, Moody’s

Analytics produces a forecast for 1,800 variables based on Fed scenarios.

CECL:

• All macroeconomic variables within R&S period have to be forecasted.

• Macroeconomic variables should be selected not only by their explanatory power of credit loss, but also

by how well they can be forecasted.

• Many specific/granular variables that were extrapolated from fundamental ones may not be fit-for-use.

Conclusion:

• CECL models may leverage different macroeconomic variables from those used in CCAR models.

11.

11

Model Performance Testing

7thAnnual Risk Americas 2018

• Similar as for CCAR models, the accuracy of loss forecast models within the R&S period

can be assessed through back-testing against predefined acceptance criteria.

• And the accuracy of macroeconomic forecast model within the R&S period can also be

assessed through back-testing.

• However, given that CECL represent a hybrid view on cycle sensitivity, accuracy may not

be an appropriate measure of model performance beyond R&S period.

• In addition, since CECL required to significantly expand disclosure about credit risk by

credit quality indicators and years of the asset’s origination (i.e. vintage), the model

performance will need to be assessed at granular level as well.