Downloaded 57 times

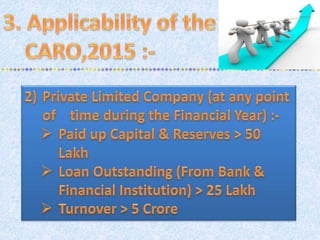

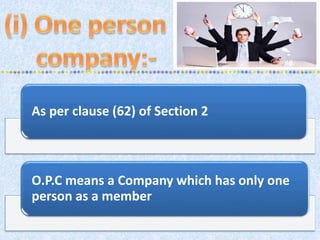

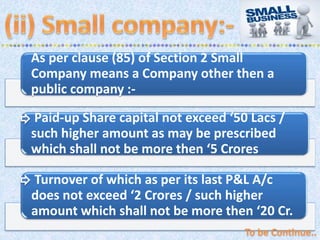

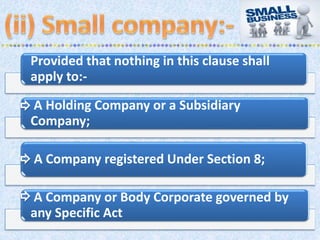

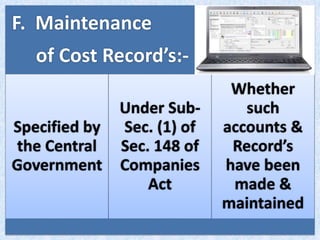

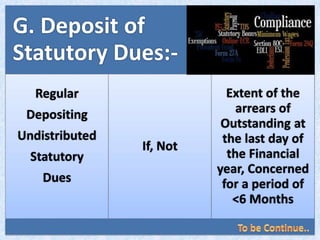

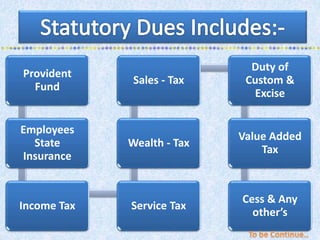

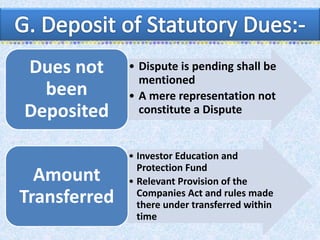

This document outlines the key changes made to the CARO (Companies Auditor's Report Order) reporting requirements in India. It summarizes the evolution from the CARO 2003 to CARO 2015, including changes made to the number of reporting points (from 21 to 12) and the relevant sections of the Companies Act that govern the order. It also provides definitions of key terms like One Person Company, Small Company, and outlines the 12 points that are required to be reported under CARO 2015, such as maintenance of accounts, statutory dues, loans, internal controls, and fraud.